TAST - Carrols Restaurant: Not Inexpensive But Significant Upside Potential

Summary

- Carrols Restaurant which is the largest franchisee of Burger King in the US has seen its stock price fall 75% in the past 18 months.

- The company has been hit hard by inflation which has led expense growth to outpace revenue causing EBITDA to plummet.

- To make matters worse, the company is highly leveraged with debt at nearly 9x current EBITDA.

- While Carrols is highly leveraged, it has no upcoming maturities until 2026, low interest rates, and lax covenants. Further, the company has access to ample liquidity.

- While Carrols is a poor-to-mediocre business, I don't expect the company to go bankrupt in the near term. Should profitability revert to historical levels, shares could double.

Overview

Carrols Restaurant Group ( TAST ) operates 1,022 Burger King Restaurants in the US (Carrols represents 14% of total US Burger King restaurants) as well as 65 Popeye's Restaurants. Burger King's Parent company, Restaurant Brands ( QSR ), owns 15% of Carrols.

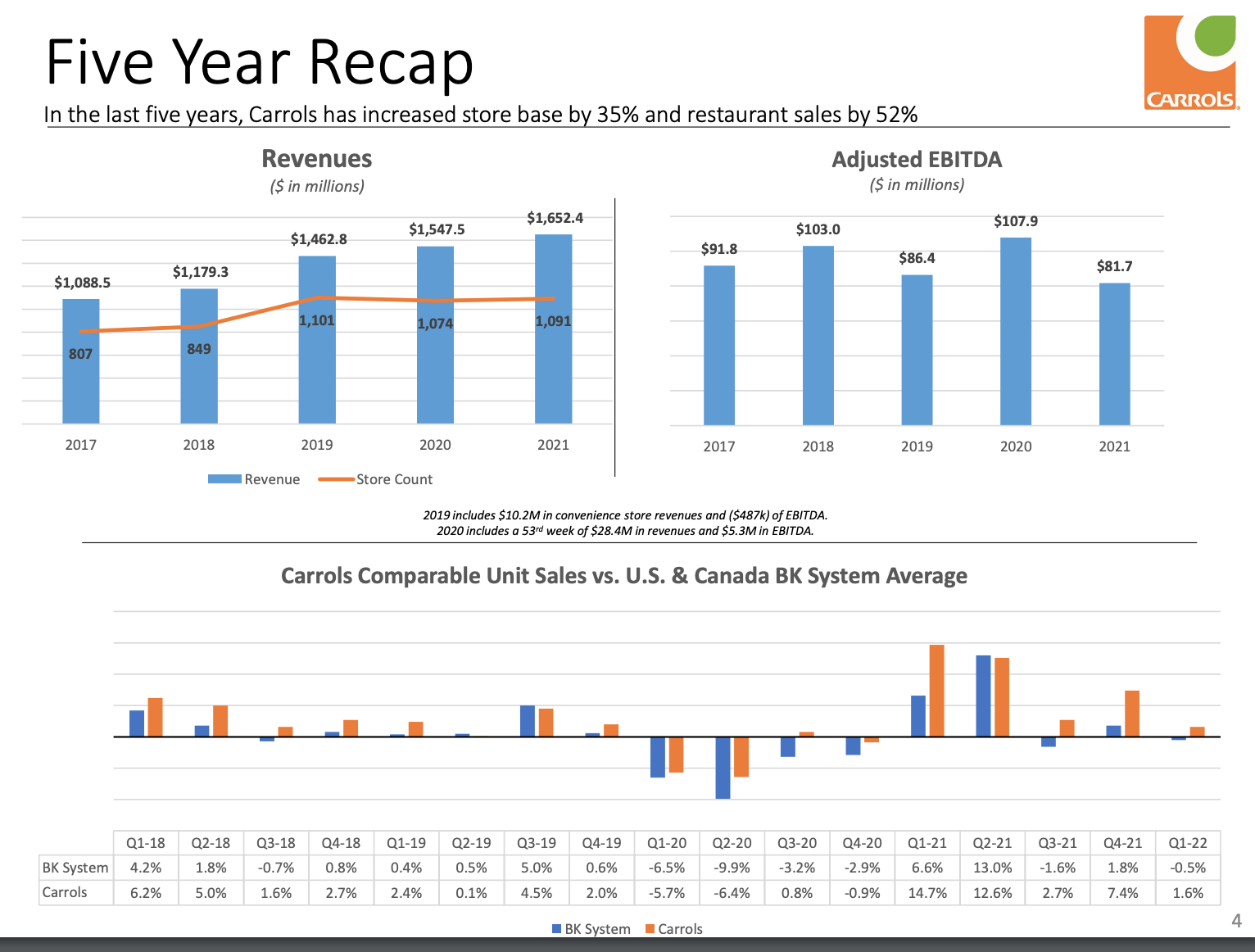

While the company is currently going through a rough patch (described below), as show below, historically Carrols has outperformed the Burger King system as a whole.

{kind=link}

Long Term Same Store Performance (Investor Presentation)

Current Results

While Adjusted EBITDA for the first 3 quarters of 2022 is down ~40% year-over-year. The company has been hit hard by inflation which has led expense growth to outpace revenue causing EBITDA to plummet. Further, inflation has put the most pressure on lower income consumers (target market). While Carrols has seen positive same store sales over the past year, this has all been driven by price (inflation), while transactions have declined.

While it has been a tough 12-18 months for Carrols, things seem to have stabilized - 3Q22 year-over-year adjusted EBITDA was down just 5% versus 3Q21 and increased sequentially versus 2Q22.

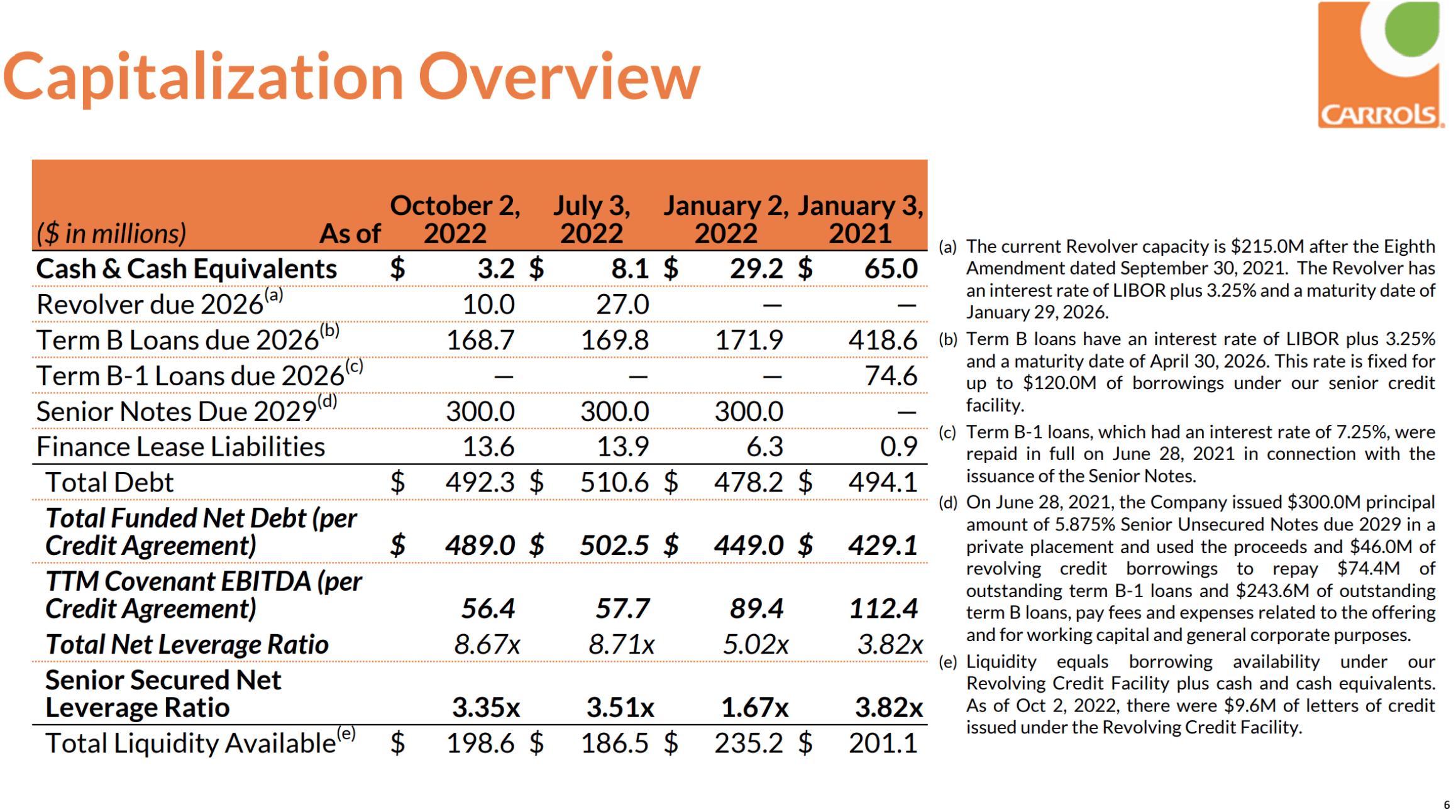

Balance Sheet - Pros & Cons

{kind=link}

Carols Debt Overview (Investor Presentation)

The left side of the slide above shows that Carrols is very highly leveraged with Net Debt to EBITDA approaching 9x. This is a very high level of leverage, especially for a challenged business like Carrols. However, the notes on the right side of the above slide contain important information which makes me reasonably comfortable that Carrols will not file for bankruptcy for several years.

- The company does not face any upcoming maturities until 2026.

- Carrols took advantage of last year's ultra low interest rates to issue $300 million in fixed rate debt at the low rate of 5.875% for debt which doesn't mature until 2029.

- 70% of Carrols Term B loan is fixed rate. Again this debt does not mature until 2026.

- The company has nearly $200 million in liquidity available under its revolving debt facility.

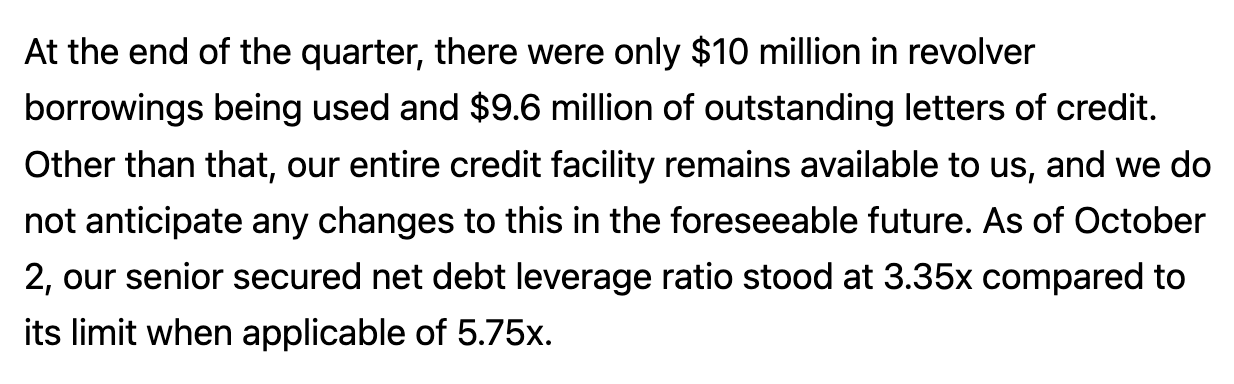

- Despite the company's poor results and high leverage, Carrols remains within covenants as noted on the most recent quarterly conference call:

{kind=link}

CFO covenant commentary (3Q22 conference call from Seeking Alpha)

Factors which could improve operating performance in the next 2-3 years:

- The company has a new CEO Paulo Pena who previously had run 800 McDonald's ( MCD ) company owned locations. Historically McDonald's has outperformed Burger King and Paulo may be able to improve operating performance at Carrols.

- Reduced inflation / possible deflation in some categories - while wages are sticky and only move upward, other commodities fluctuate in price. While for the past two years these costs have steadily marched upward, it is possible that these costs could moderate (some could even fall).

- Price hikes - Overall, Carrols has hiked prices ~10% in the past year at Burger King locations. Carrols is looking to get more granular in its pricing strategy by product and location which could result in higher revenue and profitability.

- Customers trading down to Burger King - in economic parlance, Burger King could be considered an inferior good, one for which there is greater demands as a person's income falls. A recession could lead some consumers to trade down.

- Increased adoption of technology to lower labor costs, in particular mobile phone app based ordering and in restaurant kiosk ordering. App and kiosk ordering can significantly reduce the cost of in restaurant labor (fewer cashiers).

- Improved menu /Potential for a hit product- Burger King is working to create new products which appeal to customers. To be fair, this has been true for decades but to the extent that the company successfully creates and markets a hit new product, this could drive better same store sales and improved operating margins.

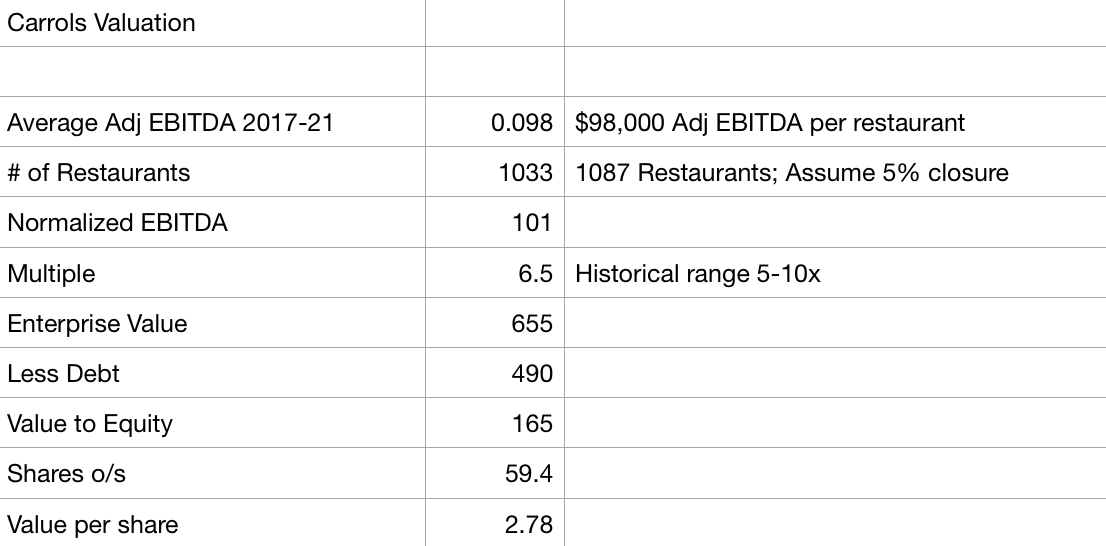

Valuation

While Carrols does not come across as inexpensive based on current financial performance, I see a reasonable probability that either through the company's own initiatives (improved operations, new products, more effective advertising) or changes to the external environment (lower commodity costs, improved customer traffic as inflation recedes) that results return to historical levels.

During the most recent 5 year period (2017-2021) prior to the surge in inflation, Carrols was able to generate $98,000 in adjusted EBITDA for each restaurant it operated.

{kind=link}

Carrols Valuation (Company Filings; Author Estimates)

If we assume that the company must close 5% of its total restaurants (assume they are structurally unprofitable) but that the company is able to achieve historical profitability levels on its remaining restaurant base, Carrols would generate $101 million in adjusted EBITDA (slightly below 2020 levels). Assuming a 6.5x EV/EBITDA multiple (which is toward the very low end of its historical trading range of 6-12x) and deducting debt gets me to a value of $2.78 per share which is nearly 100% upside.

Conclusion

Carrols is a highly leveraged, low quality business suffering in a difficult economic environment. That said, I believe that the company's debt maturity and liquidity profile will enable it to survive and that EBITDA levels will eventually revert back to recent historical levels. Should this occur, as I show above, there is a path to nearly 100% upside. Given my belief that the company does not face near-term bankruptcy risk and the attractive level of upside, I've taken a small position in the stock.

For further details see:

Carrols Restaurant: Not Inexpensive But Significant Upside Potential