TAST - Carrols Stock: A Discounted Tasty Treat

2023-10-23 10:11:25 ET

Summary

- Carrols Restaurant Group is a major franchisee of Burger King and Popeyes, operating over 1,000 restaurants in the US.

- The company has been reporting negative net profits since 2019 due to high corporate expenses and margin contraction.

- However, recent improvements in pricing have led to a rebound in profitability and a strong stock performance.

Carrols Restaurant Group Inc. ( TAST ) is a leading restaurant group in the U.S., operating close to 1,100 quick-serve restaurants, mostly under the Burger King banner.

Financial performance for Carrols has been poor, as franchise economics are mostly eaten up by G&A expenses. However, the company's valuation reflects its low profitability.

Overall, Carrols' stock price looks attractively priced, as it is implying per restaurant value of $1.4 million vs. replacement cost of $1.8 million. Furthermore, with expanding margins due to price increases, Carrols' financial results have been on an uptrend. I rate TAST a speculative buy .

Company Overview

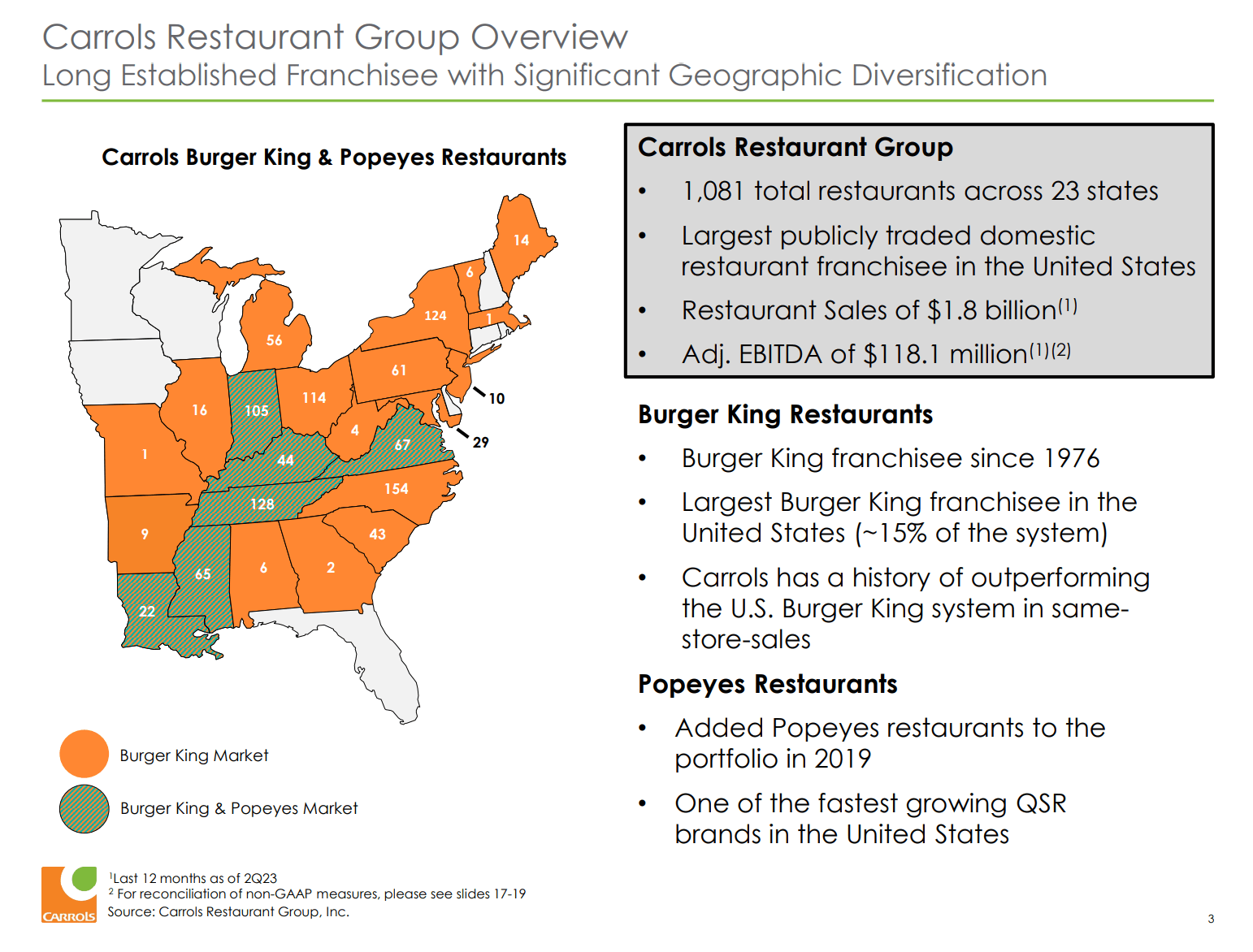

Carrols Restaurant Group Inc. is one of the largest restaurant companies in the United States operating close to 1,100 Burger King and Popeyes restaurants in 23 states (Figure 1).

Figure 1 - Carrols overview (TAST investor presentation)

{kind=link}

Carrols is the largest Burger King franchisee in the U.S. operating 1,022 Burger King restaurants as of January 1, 2023. It is also the 8th largest franchisee of Popeyes restaurants in the U.S. based on the number of restaurants operated.

Burger King and Popeyes are two globally recognized brands in the quick-serve restaurant space owned by Restaurant Brands International Inc. ( QSR ). Carrols has been operating Burger King restaurants since 1976 and operates 15% of the U.S. restaurants in the Burger King system. Executives from QSR sit on Carrols' board and QSR owns preferred stock in Carrols that can be converted into approximately 15.1% of Carrols' common shares.

Dis-Economies Of Scale

Owning a franchise restaurant has been a well-trodden path to wealth for many middle-class Americans. According to a survey by Franchise Business Review, the average franchisee makes profits of $120,000 per year for businesses that have been opened for more than 2 years. So if an average franchise can make $120,000 in profits, then a company owning over 1,000 franchises of nationally recognized restaurant chains like Burger King and Popeyes must be 'rolling in profits', right?

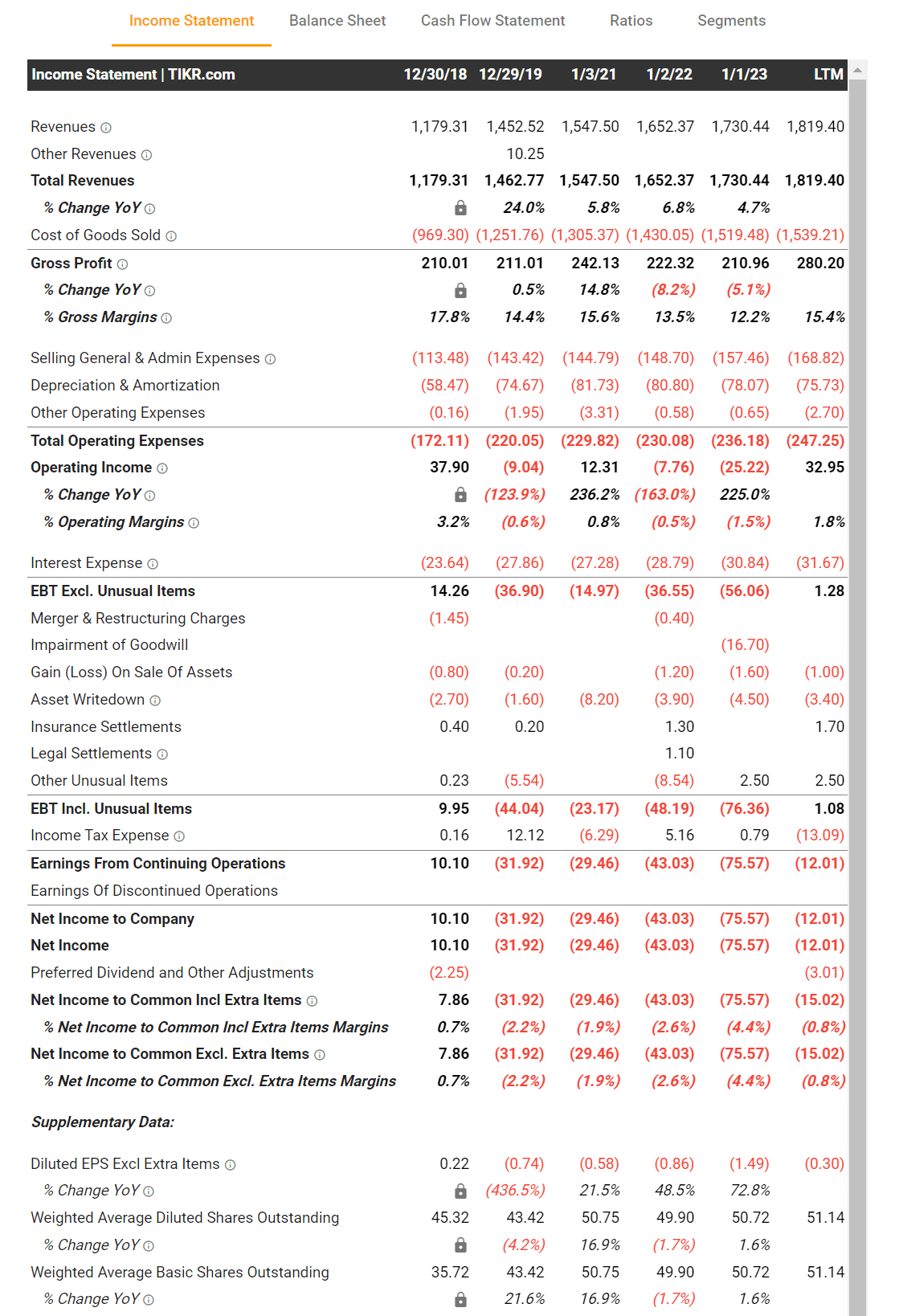

Unfortunately, in the case of Carrols, the answer is a resounding 'no'. Despite owning over 1,000 franchised Burger King and Popeyes restaurants, Carrols have been reporting negative net profits since 2019 (Figure 2).

Figure 2 - Carrols financial overview (tikr.com)

{kind=link}

What is Carrols doing wrong?

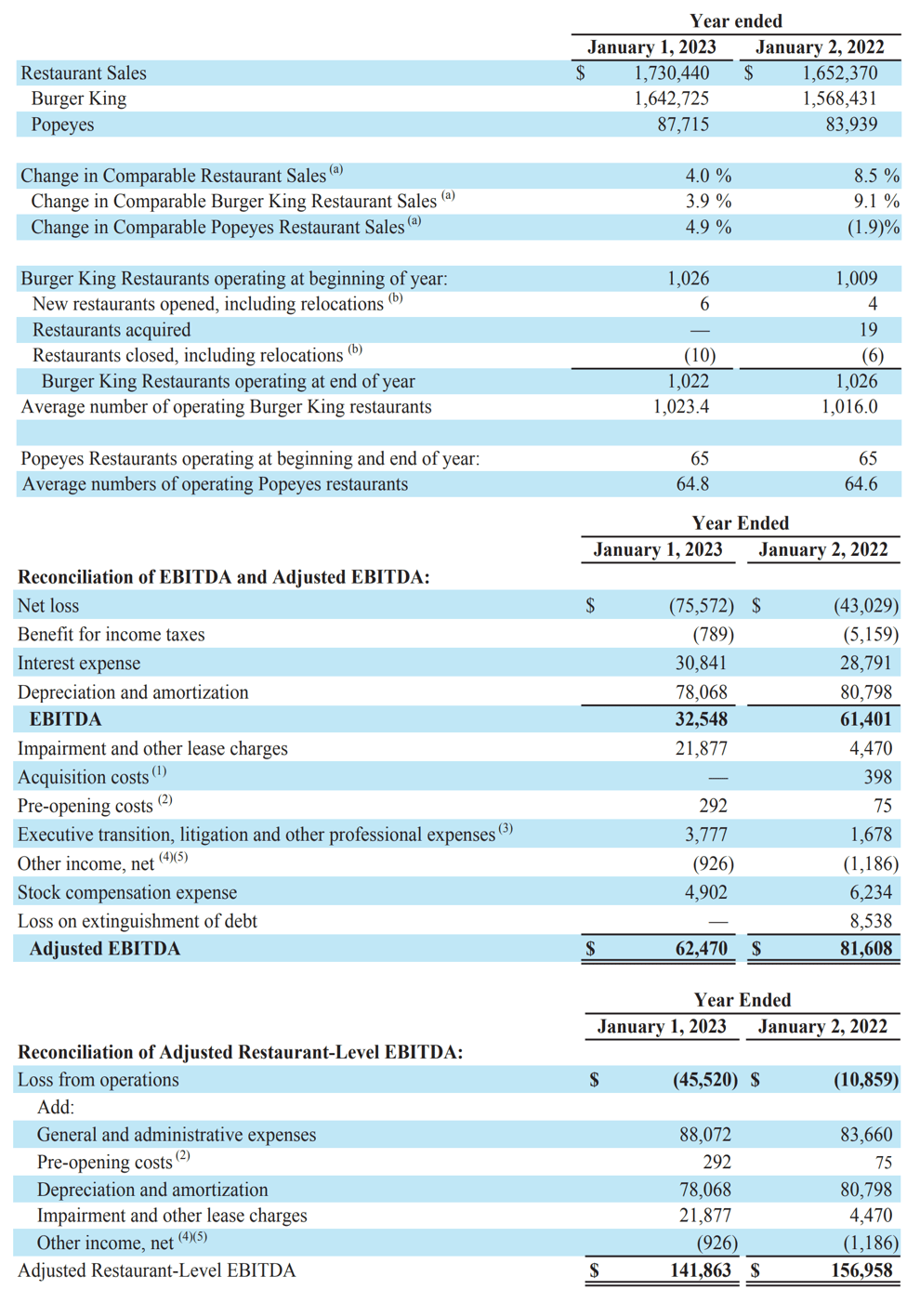

Studying the company's financials, some line items stand out. For example, in the fiscal year 2022 (year-ended January 1, 2023), Carrols generated $1.73 billion in sales or $1.6 million per restaurant (Figure 3). At a restaurant level, EBITDA was $142 million or 8.2%.

Figure 3 - Carrols financial overview, 2022 (TAST 2022 annual report)

{kind=link}

While 8.2% restaurant EBITDA margin is not great, it is a respectable figure that should lead to net profits. Restaurant EBITDA margin was actually higher at 9.5% in 2021 and 12.4% in 2020. So why does Carrols lose money every year on the bottom line?

The culprit is Corporate General and Admin Expenses and Impairment Charges. G&A and impairments combined for $110 million in 2022 and $88 million in 2021, or 6.4% and 5.3% of sales respectively.

While the owner of a single restaurant franchise is the often the sole manager and decision-maker, when the business scales to dozens and hundreds of restaurants, we end up with layers upon layers of management, including regional managers, district managers, VP of operations, COO, CFO, CEO, and so on and so forth. The restaurant franchising business has 'dis-economies of scale' in my view, since restaurant-level costs are relatively fixed (food and staffing costs are often dictated by the brand owner, royalty fees are fixed, and rent is dependent on local market conditions) but management expenses scale with the number of restaurants.

Carrols Caught By Inflation

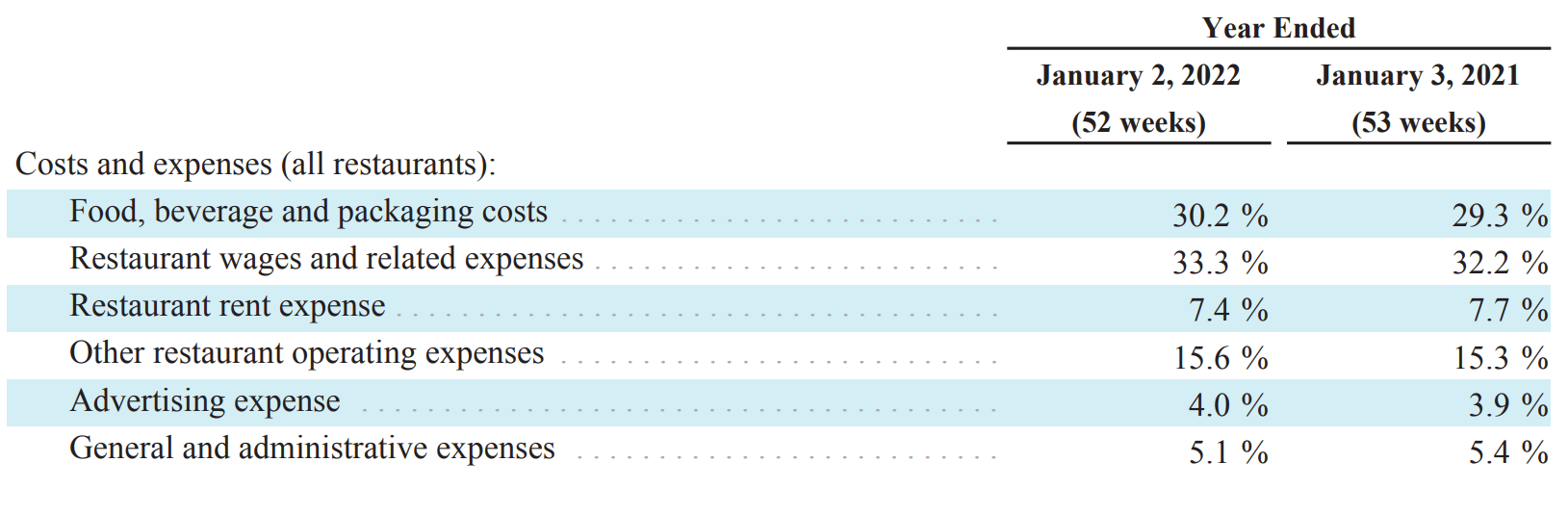

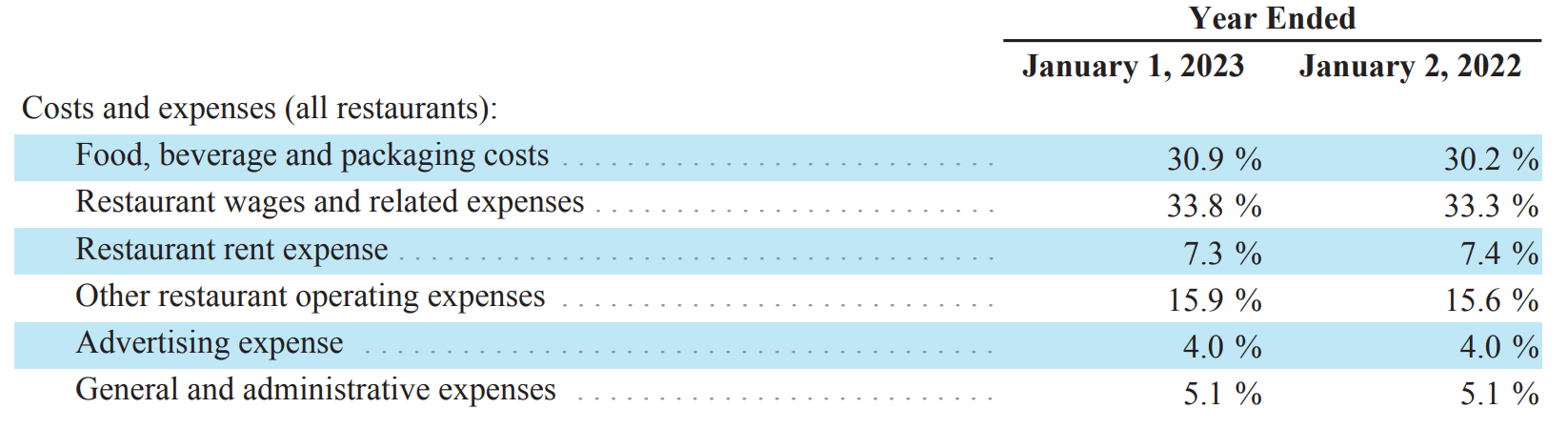

In the past few years, Carrols' financial results were especially impacted by soaring inflation that ate into margins. Although total sales increased by 18.6% from $1.46 billion in 2020 to $1.73 billion in 2022, Food and wages grew at an even faster pace such that as a percentage of sales, food increased from 29.3% of sales in 2020 to 30.9% in 2022 while wages increased from 32.2% in 2020 to $33.8% in 2022 (Figure 4 and 5).

Figure 4 - TAST 2020/2021 costs as % of sales (TAST 2021 annual report) Figure 5 - TAST 2021/2022 costs as % of sales (TAST 2022 annual report)

{kind=link}

{kind=link}

The 3.2% combined increase in food and labor costs cut into Carrols already razor-thin margins, causing the company to report $75 million in net loss for the year for 2022.

Financial Performance Turning The Corner

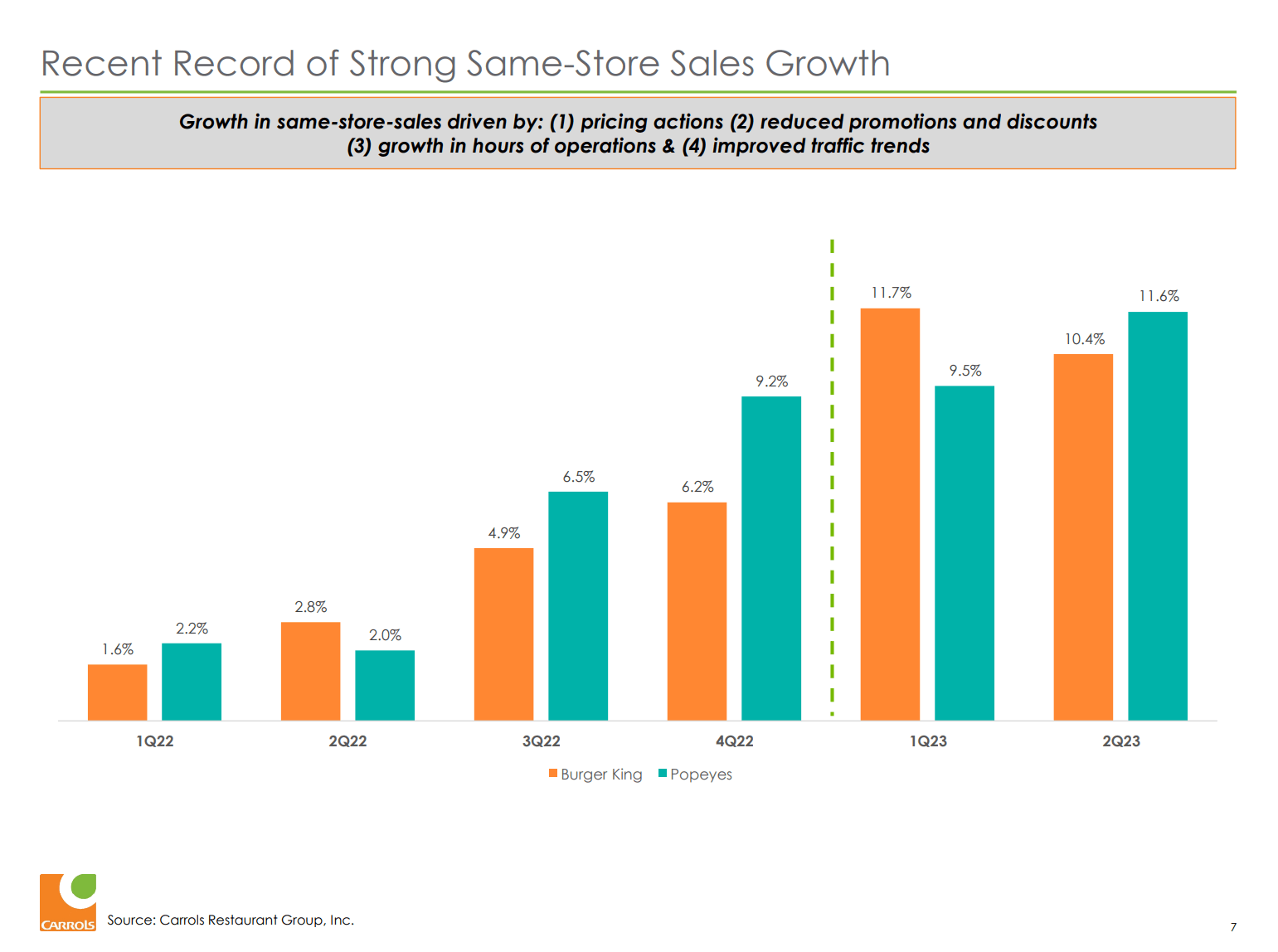

However, in the past few months, financial performance for Carrols may be finally turning the corner, as QSR's national marketing campaigns have driven strong top-line growth for Carrols' restaurants (Figure 6).

Figure 6 - SSSG has inflected higher for BK restaurants (TAST investor presentation)

{kind=link}

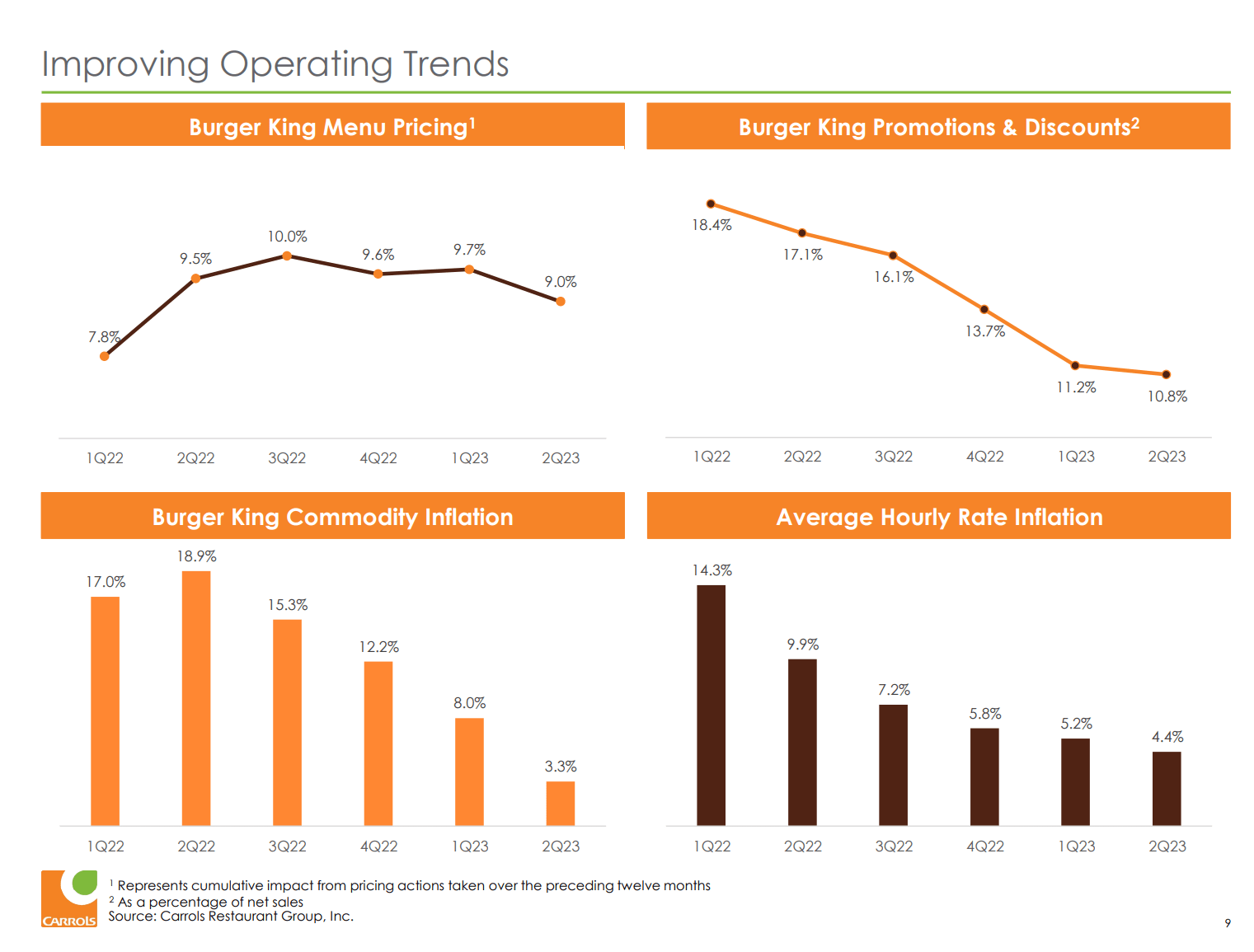

Furthermore, double digit cost inflation appears to be finally easing (Figure 7).

Figure 7 - Food and wage inflation appears to be slowing (TAST investor presentation)

{kind=link}

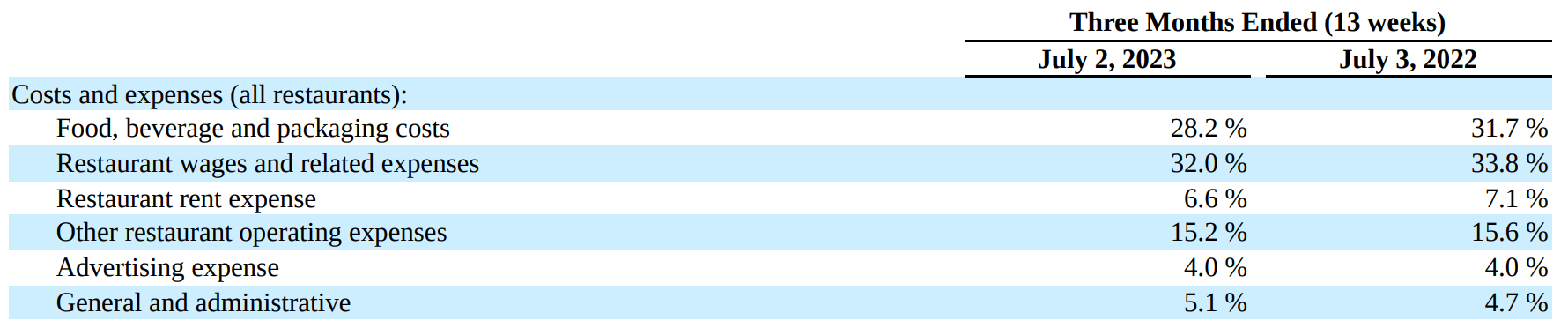

The net result is a decrease in food and wage costs to 60.2% of sales for the latest quarter, a 4.6% improvement YoY (Figure 8).

Figure 8 - Q2/23 costs as % of sales (TAST Q2/23 10Q report)

{kind=link}

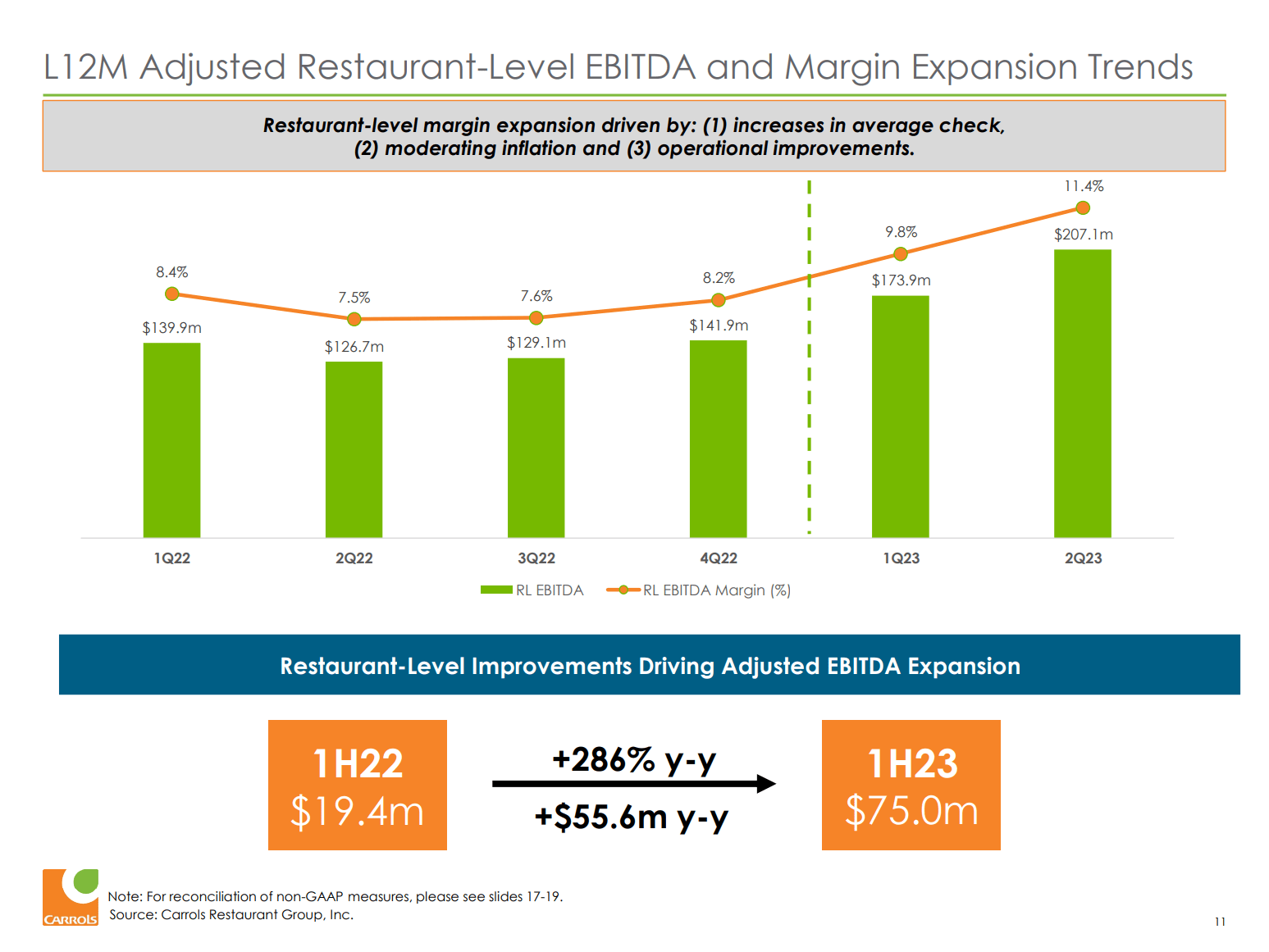

This has led to a rebound in trailing-twelve month restaurant-level EBITDA margin to 11.4% (Figure 9).

Figure 9 - TTM EBITDA margin is rebounding (TAST investor presentation)

{kind=link}

Full Year Profit Expected

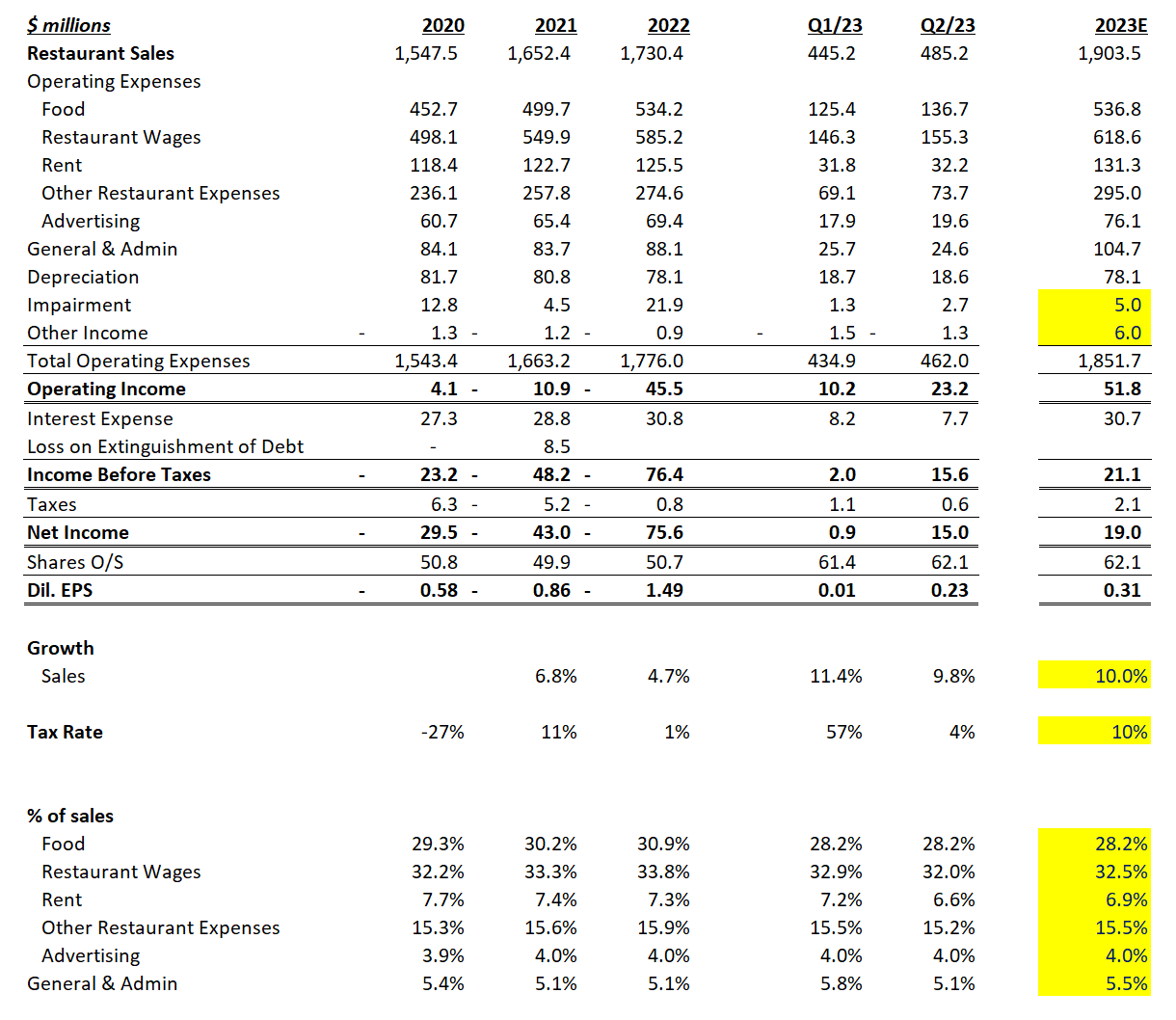

In fact, if I apply YTD 2023 margins to an expected 10% increase in sales, I come up with estimate of $0.31 in dil. EPS for Carrols for the full year (Figure 10).

Figure 10 - TAST 2023 forecasted financials (Author created)

{kind=link}

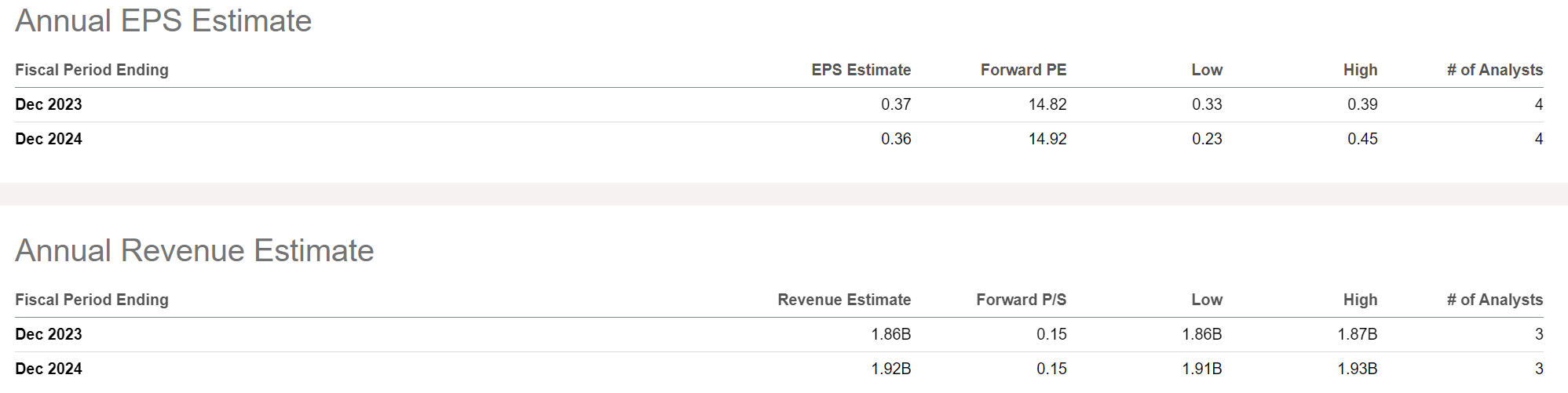

Wall Street analysts expect revenues of $1.86 billion and $0.37 in EPS for 2023, so my model is definitely in the ball park (Figure 11).

Figure 11 - Consensus estimates for TAST (Seeking Alpha)

{kind=link}

Stock Has Rallied Off The Lows

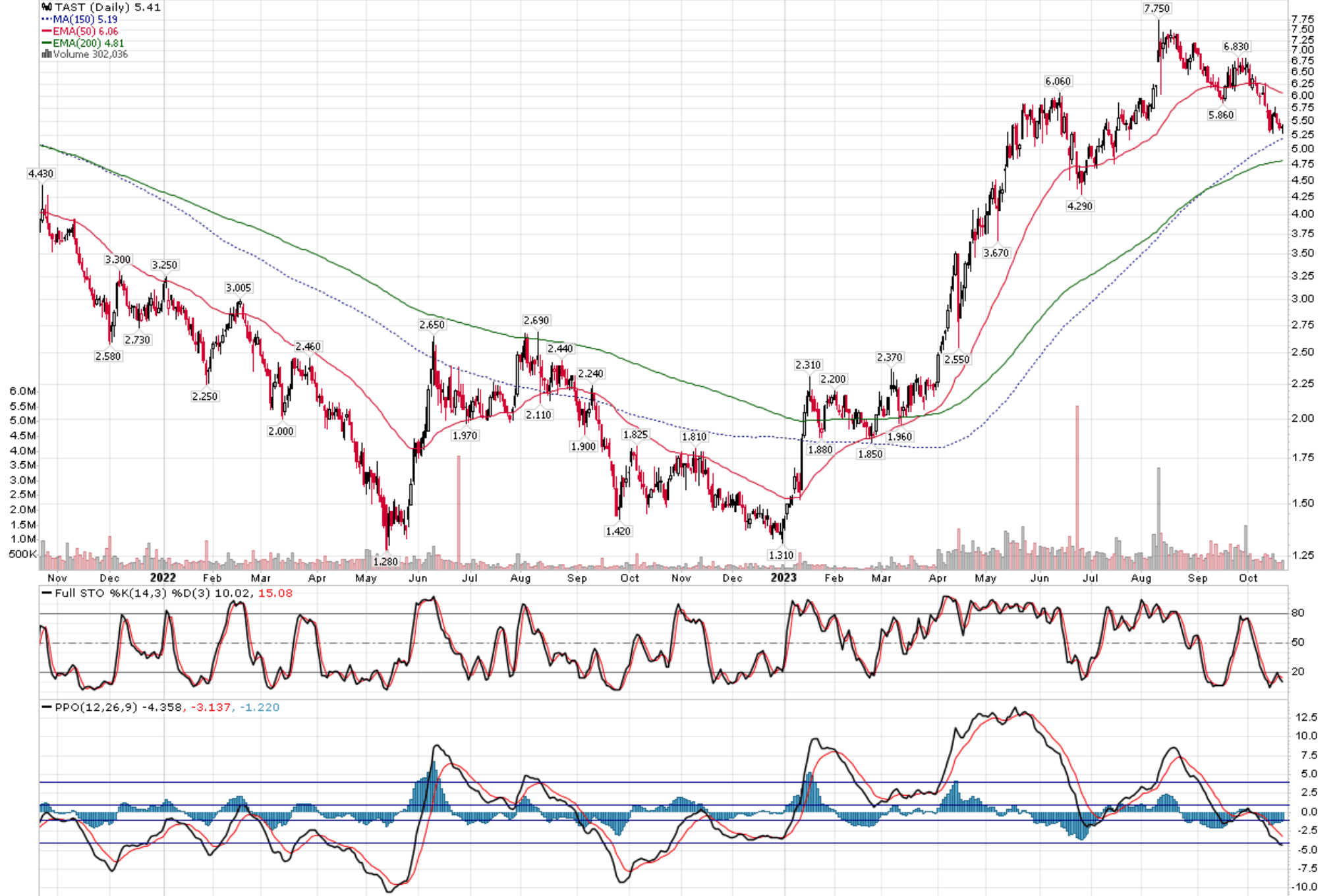

Carrols' improving financial performance has made its stock one of the best performing restaurant stock of 2023, with a YTD return of 280%, from a December low of $1.31 to a recent price of $5.41 (Figure 12).

Figure 12 - TAST's stock price has rebounded sharply (stockcharts.com)

{kind=link}

The key question is, is the stock a good buy at current levels?

Valuation Remains Cheap

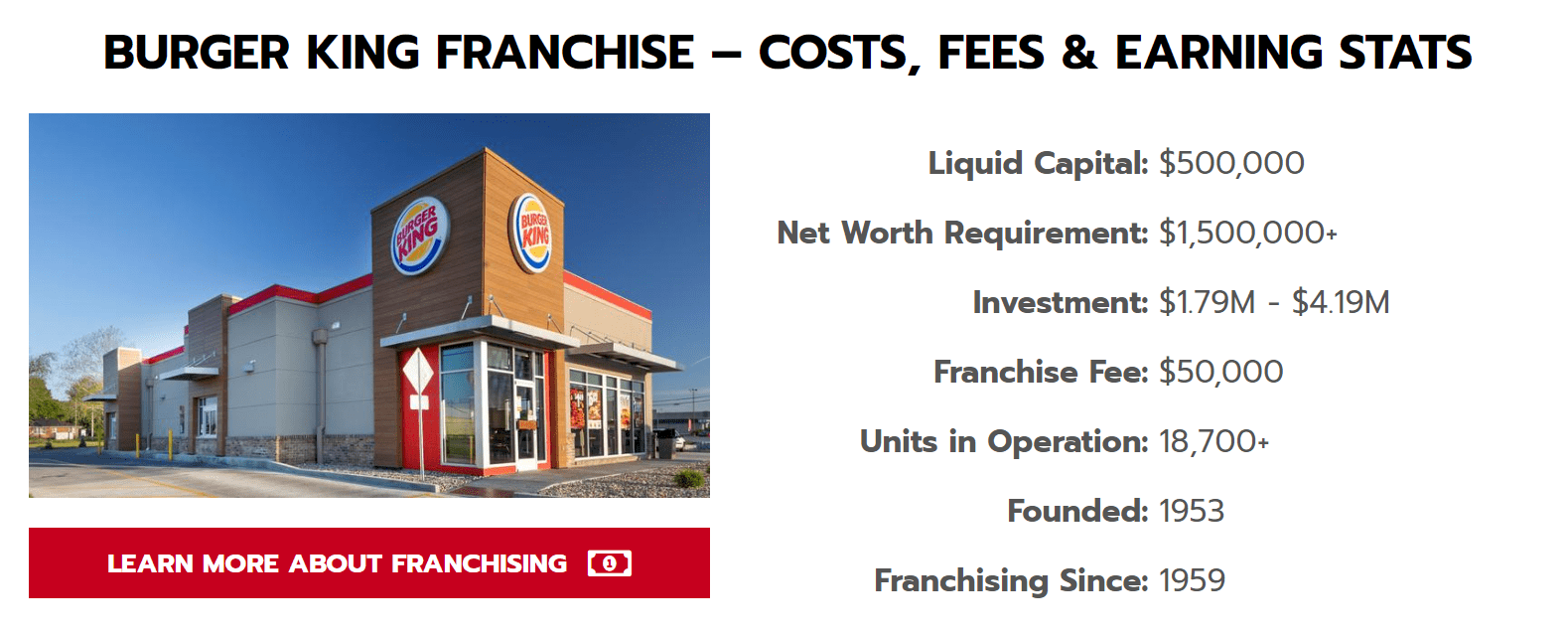

At first glance, Carrols' valuation looks dirt cheap. The company is only trading at a market cap of $280 million or less than $250,000 per restaurant. This compares to the average replacement cost of $1.8 million to $4.2 million to open a Burger King restaurant (Figure 13).

Figure 13 - Burger King franchise costs (wolfoffranchises.com)

{kind=link}

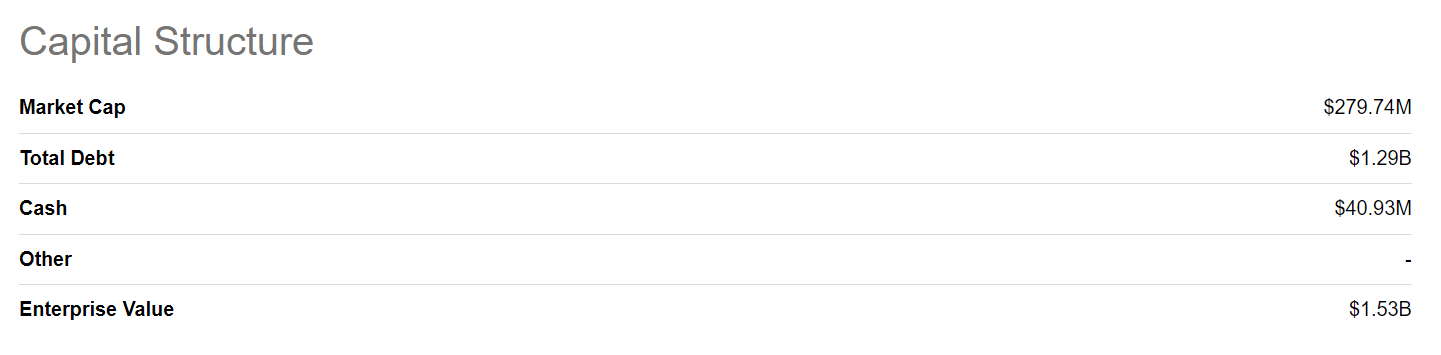

However, market cap is not the right metric to look at for Carrols. In addition to equity, Carrols also has $1.3 billion in debt and capital leases, or a total enterprise value of $1.5 billion (Figure 14).

Figure 14 - TAST enterprise value (Seeking Alpha)

{kind=link}

On a per restaurant basis, Carrols is trading at $1.4 million of enterprise value, still a discount to the average replacement cost of its restaurants, but not grossly undervalued.

However, investors should note that Carrols' financial results do have a lot of operating and financial leverage. For example, as we showed above, with a few percentage improvement in food and wage costs, our estimates for Carrols' earnings swing from a $1.49 / share loss in 2022 to a forecast of a $0.31 / share profit in 2023.

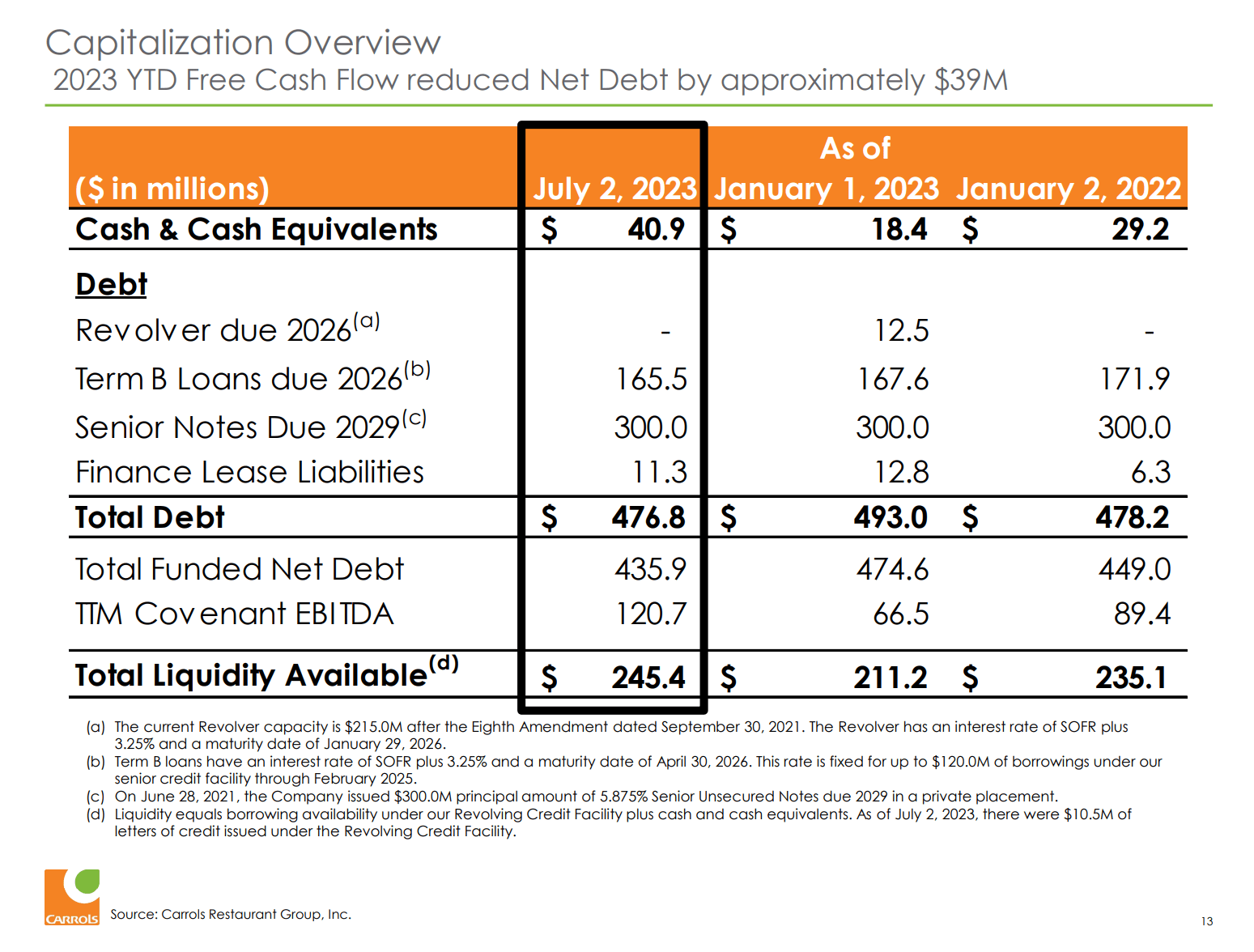

Mountain Of Debt Is A Concern

Speaking of leverage, Carrols' balance sheet is heavily levered, with $477 million in long-term debt outstanding against LTM corporate EBITDA of $121 million (Figure 15).

Figure 15 - Carrols has a lot of debt (TAST investor presentation)

{kind=link}

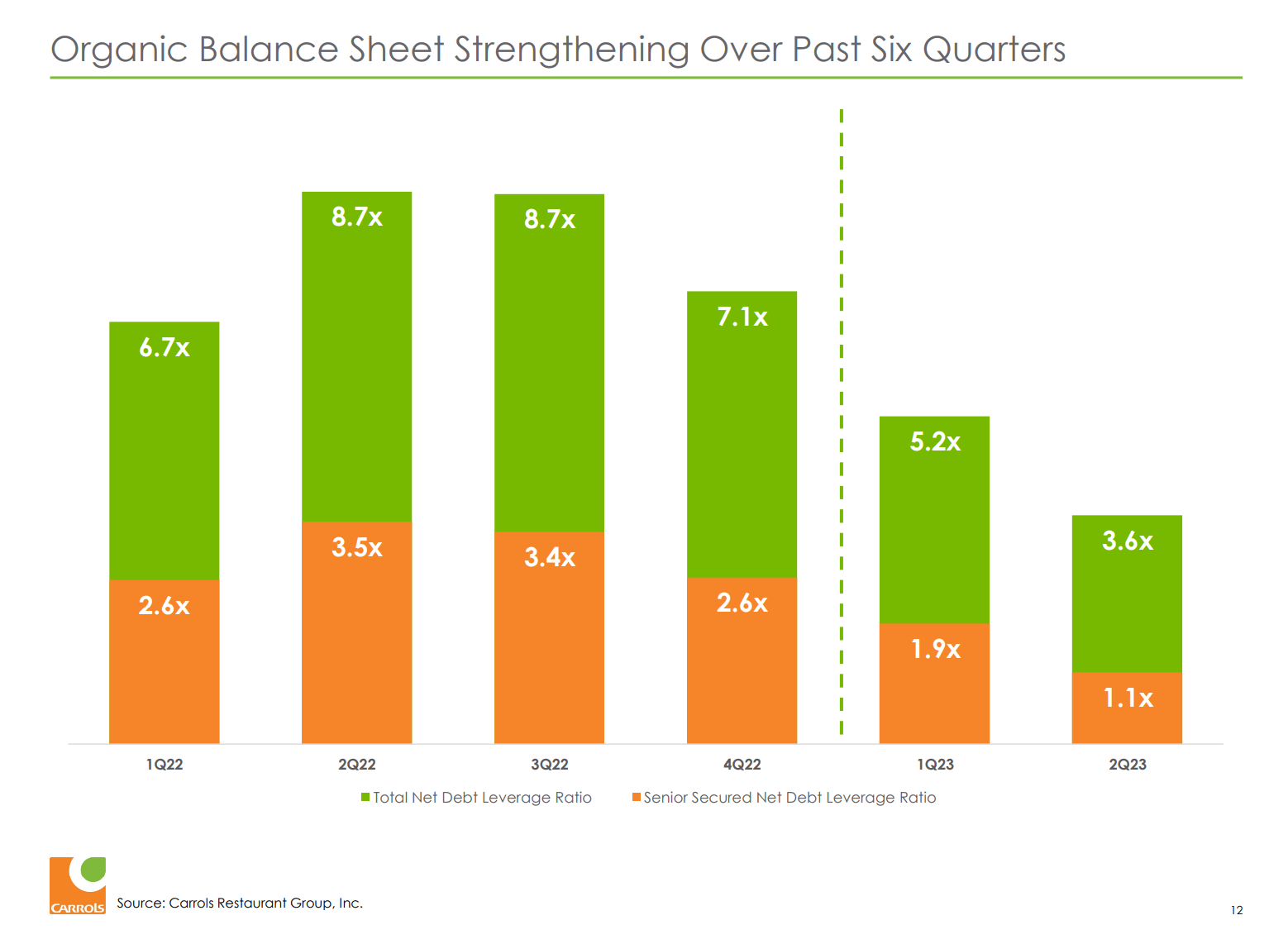

Net debt to EBITDA stood at 3.6x at the end of Q2, a vast improvement from the middle of 2022, when Carrols was at bankruptcy's doors with a 8.7x Net debt / EBITDA ratio (Figure 16).

Figure 16 - Carrols' net debt / EBITDA has improved with increased margins (TAST investor presentation)

{kind=link}

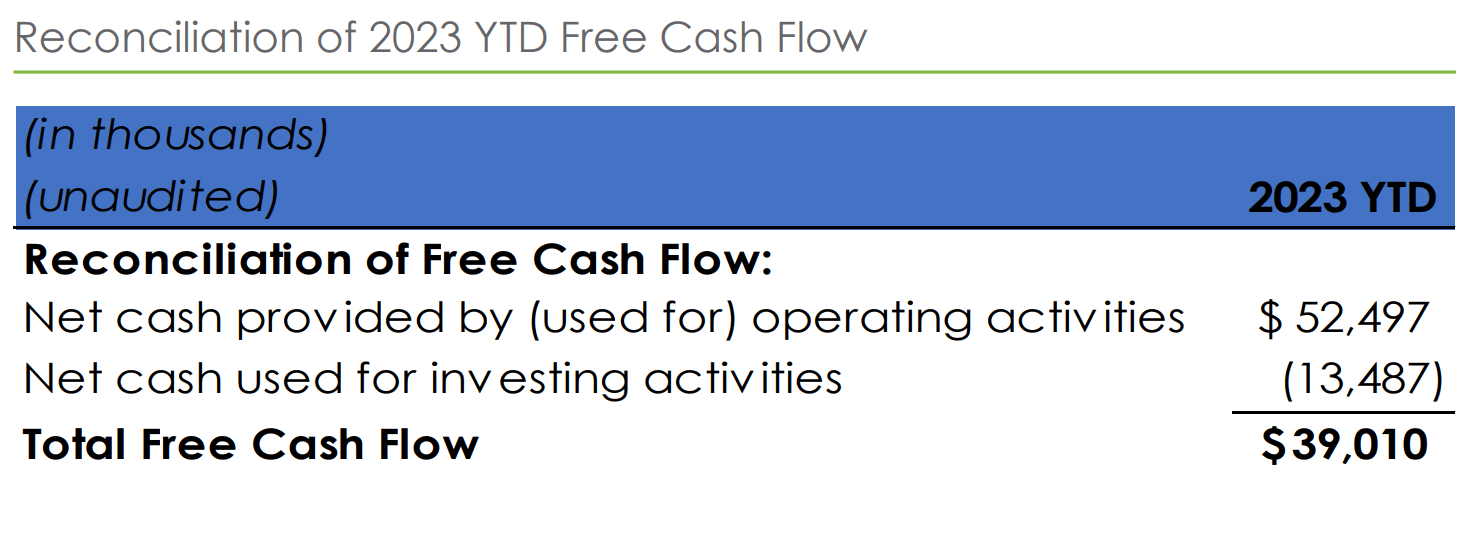

As long as Carrols' margin improvements are sustainable, the company's leverage should be quickly reduced, as the company generated $39 million in free cash flows in the 6 months YTD (Figure 17).

Figure 17 - Carrols' was able to generate $39 million in free cash flows in H1/23 (TAST investor presentation)

{kind=link}

Risks To Carrols

In addition to leverage, other risks to Carrols include inflation and the economy. While inflation has been trending lower in recent quarters, it is still a major concern. If wage and food inflation were to inflect higher, Carrols may once again face margin pressure.

Furthermore, inflation is beginning to pinch the pocketbooks of the U.S. consumer, with Carrols noting that wealthy customers have been trading down from higher priced casual dining to Burger King.

While this may improve Burger King's results in the short-term, it is also a worrisome trend, especially as Burger King's core customer may be priced out of eating out altogether. The restart of student debt repayments is expected to affect millions of Americans and will likely act as a headwind to consumer spending in the coming quarters.

Conclusion

Carrols is a leading restaurant operator in the U.S., owning close to 1,100 Burger King and Popeyes restaurants. Financially, Carrols' performance has swung from deep operating losses to an operating profit on the back of increased pricing in its Burger King restaurants. If these margin improvements are sustainable, then Carrols' stock looks like a decent buy, as Carrols' is only trading at EV/restaurant of $1.4 million, a discount to the replacement cost of ~$1.8 million.

However, Carrols does have a lot of debt that could be an issue if operating results turn south due to margin pressures or a bad economy. I rate Carrols a speculative buy .

For further details see:

Carrols Stock: A Discounted Tasty Treat