NLCP - Cash COWs: 11 High-Yield REITS With Very Safe Dividends

2023-12-11 09:30:00 ET

Summary

- Some high-yielding REITs have unsafe dividends, leading to potential dividend cuts and decline in share value.

- This article provides a list of 11 cash COW REITs with safe dividends, including companies from the cannabis and office sectors.

- There is also a list of high-yield REITs with slightly more risk but still considered safe by the Seeking Alpha Quant Ratings system.

Don't worry. She won't hurt you. Unless she steps on your foot.

There are two ways you can make money as an investor:

- Gain

- Yield

Gain is the change in the share price. Yield is the cash dividend, as a percentage of the purchase price.

Here's the problem. Gain and yield tend to move in opposite directions. That is to say, by and large, the lower the Yield, the higher the Gain, and vice-versa. If they moved in the same direction, investing would be easy. We would all just invest in the stocks with the highest yield. We would all get rich without effort, and there would be no need for analysts, stock market experts, or services like Seeking Alpha.

So at some point, you have to choose which is more important to you as an investor: Yield? or Gain? And that is purely a matter of taste. There is no one correct answer for all investors. Quite the opposite. Every investor has to find the balance that is right for him or her.

There are investors who are only interested in Yield. They are looking for COWs (Cash Only Wanted). So I call them COWhands. They are not concerned about the underlying price of the shares, as long as the COW keeps squirting out the same bucket of cash on the appointed day.

But here's the thing about Yield. What you see isn't always what you get. Companies can and will cut dividends at any time. Although they tend to avoid dividend cuts if possible, sometimes it becomes inevitable. And when the dividend is cut, not only do you get a significant reduction in Yield, but COWhand investors almost always dump their shares like a load of manure. So you end up with the worst of both worlds:

A) a dividend cut, so you don't get the cash flow you signed up for, accompanied by

B) a swift and sharp decline in share value, leaving you with little recourse but to sell at a loss or hold for a very long time, in hopes of getting back even.

You thought you were getting a COW, but you got the horns instead.

These companies go by various names, chief among them being "Yield trap," "Mouse trap," and "Sucker yield". You only have to get burned once to understand why.

Here is a current list of 8 likely Mouse traps . The odds are 2-to-1 they will cut their dividends, and the odds are 50-50 the cut will happen within the next 12 months , according to Steven Cress , who pioneered the Seeking Alpha Quant Ratings system.

Regardless whether you are a COWhand or a FROG hunter , the safety of the dividend is of great importance to your return on investment.

Furthermore, there is an inverse relationship between Yield and Dividend Safety. By and large, all else equal, the higher the Yield, the riskier the dividend. The safest dividend is no dividend at all, since it can never be cut. (At least, no one has yet managed to sell a stock with a negative dividend, to my knowledge.) The next safest would be one penny per share, and so on.

But there are exceptions, and they are worth hunting. So if you want a high yield that is safe from a cut, where do you turn?

Currently, risk-averse investors can get a very safe 5.0%, thanks to the Fed's two-year rate-hiking spree. Are there REITs that yield more than 5.5%, that offer similar safety?

Turns out the answer is Yes. The Seeking Alpha Quant ratings system provides a Dividend Safety grade on every company, ranging from A to F. Companies with Dividend Safety grades between A+ and B- have only about a 1 out of 50 chance of suffering a dividend cut in the next 12 months. Who are these reliable cash COWs?

Moooo!

Here is a list of 11 cash COW REITs yielding 5.5% or better, with Dividend Safety grades of B- or better, ranked first by Dividend Safety grade, then by Yield. As you can see, somewhat surprisingly, 6 of the companies on this list come from the two most beaten-down sectors in REITdom: Cannabis and Office. Also included are one Hotel, one Casino, and three Net Lease REITs.

| Company |

| Ticker |

| Sector |

| Div. Safety |

| Yield |

| NewLake Capital Partners |

| ( NLCP ) |

| Cannabis |

| A+ |

| 11.64% |

| Innovative Industrial Properties |

| ( IIPR ) |

| Cannabis |

| A |

| 8.45% |

| Kilroy Realty |

| ( KRC ) |

| Office |

| A |

| 5.90% |

| Cousins Properties |

| ( CUZ ) |

| Office |

| A |

| 5.85% |

| Apple Hospitality |

| ( APLE ) |

| Hotel |

| A- |

| 5.81% |

| Douglas Emmett |

| ( DEI ) |

| Office |

| B+ |

| 5.50% |

| VICI Properties |

| ( VICI ) |

| Casino |

| B+ |

| 5.49% |

| Broadstone Net Lease |

| ( BNL ) |

| NNN |

| B |

| 6.86% |

| City Office |

| ( CIO ) |

| Office |

| B- |

| 7.56% |

| EPR Properties |

| ( EPR ) |

| NNN |

| B- |

| 7.23% |

| Realty Income |

| ( O ) |

| NNN |

| B- |

| 5.62% |

Source: Seeking Alpha Premium and Hoya Capital Income Builder

The rest of this article will take just a quick look at the companies on the list above, to get just a feel for why their dividends are considered so safe by the Seeking Alpha Quant ratings system. In brief, dividends come from AFFO (Adjusted Funds From Operations), out of which a company also pays back its debts and retains some earnings for expansion. So dividend safety is largely a function of debt and revenue growth, relative to the company's sector.

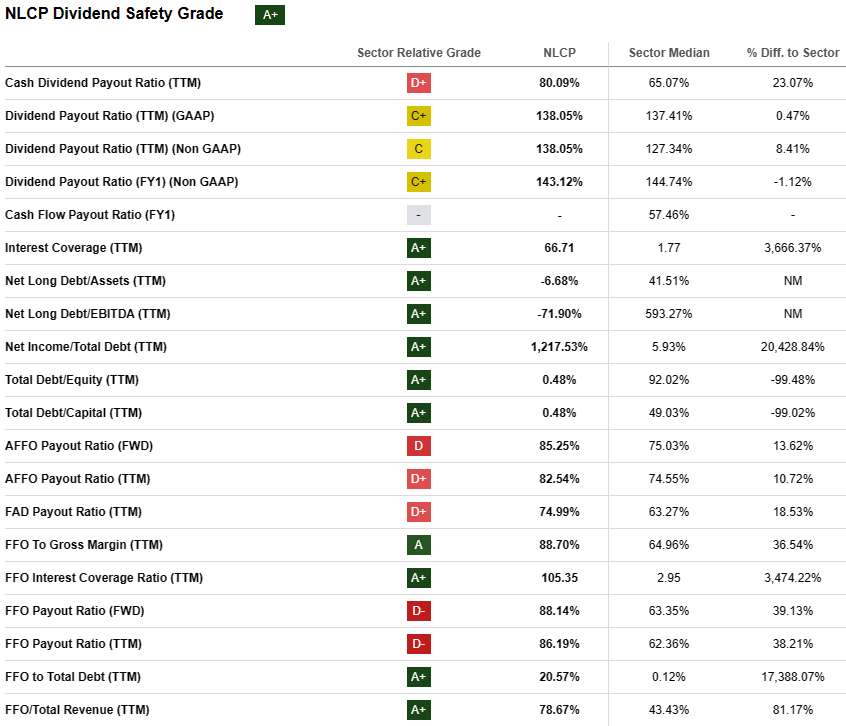

New Lake Capital Partners

As you can see, the Dividend Safety ratings take 20 data points into consideration. In the case of NLCP, 10 of the 20 data points earn a grade of A+. Almost all of them are centered around the company's favorable debt picture, and one indicates the company excels at turning revenue into FFO (funds from operations). The company is operating with a miniscule $2.0 million in debt. Debt Ratio and Debt/EBITDA are effectively zero. So despite the aggressive payout ratios, this dividend is considered very safe.

{kind=link}

Take this with a grain of salt, however. This is a volatile microcap ($0.28 billion), that has spent its two-year history searching for a bottom in share price.

{kind=link}

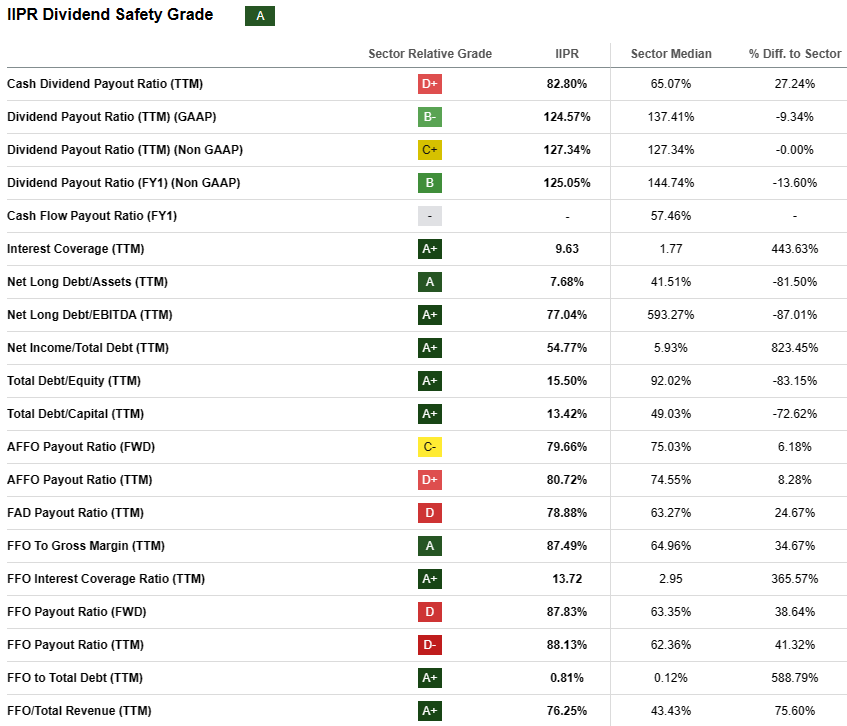

Innovative Industrial Properties

The picture for IIPR is very similar to NLCP's. Of the 20 data points, 12 grade out at B or better for IIPR. The debt picture is so favorable that the company can support aggressive payout ratios and still remain safe. IIPR's Debt Ratio is just 10%, and Debt/EBITDA stands at a microscopic 0.8. Meanwhile, FFO per share grew 8.1% for this company in 2023.

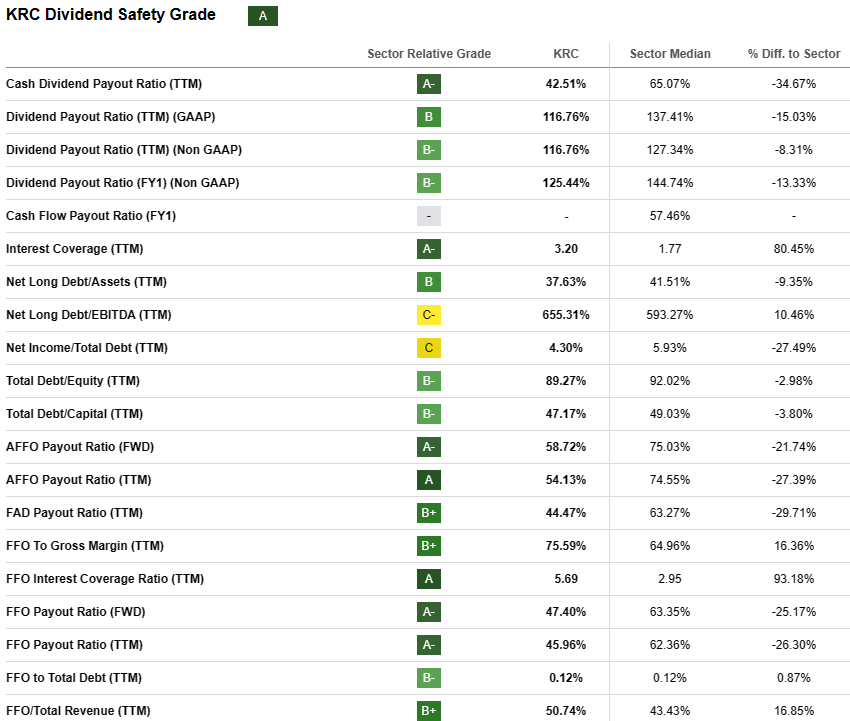

Kilroy Realty

{kind=link}

The top Office REIT on the list, Kilroy Realty has 16 of 19 data points in the B- or better range, and no data points grading at D or worse. The company manages a high yield with a conservative payout ratio of around 50%. And although KRC has significant debt ($4.9 billion), it is not problematic in comparison to the company's net income and EBITDA, when judged against other companies in its sector. Kilroy's 50% Debt Ratio is typical of Office REITs right now, and its Debt/EBITDA of 6.4 is head and shoulders above the crowd.

{kind=link}

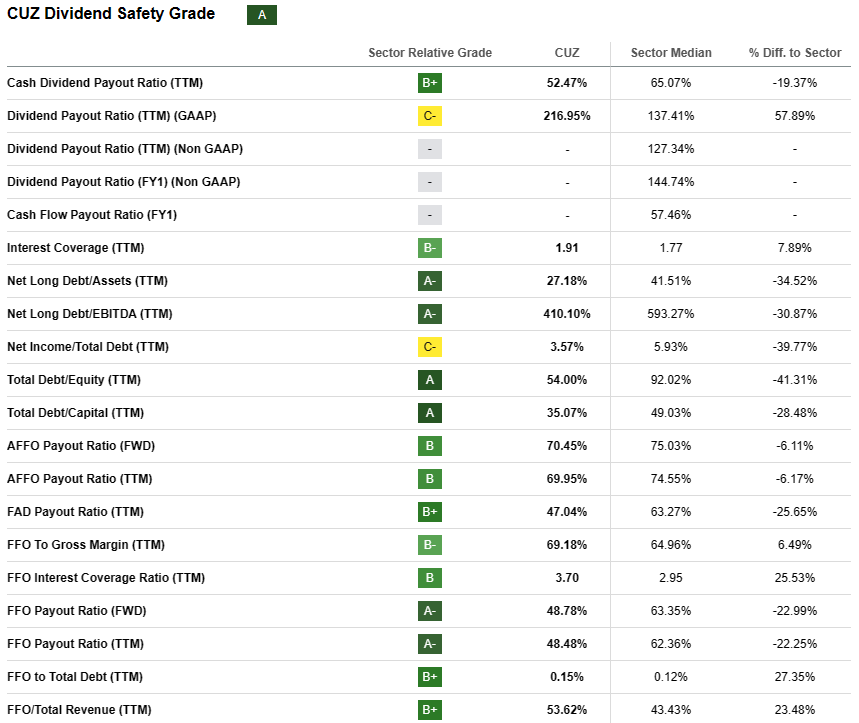

Cousins Properties

Fellow Office REIT Cousins Properties has 15 data points in the A to B- range, out of 17 that apply, and no data points grading at D or worse. This company's Debt Ratio of 38% and Debt/EBITDA of 4.8 are exceptional for an Office REIT, and its FFO has been very stable over the past 6 years, in spite of the pandemic. Thus, the flow of revenue appears more than adequate to maintain the conservative payout ratios.

{kind=link}

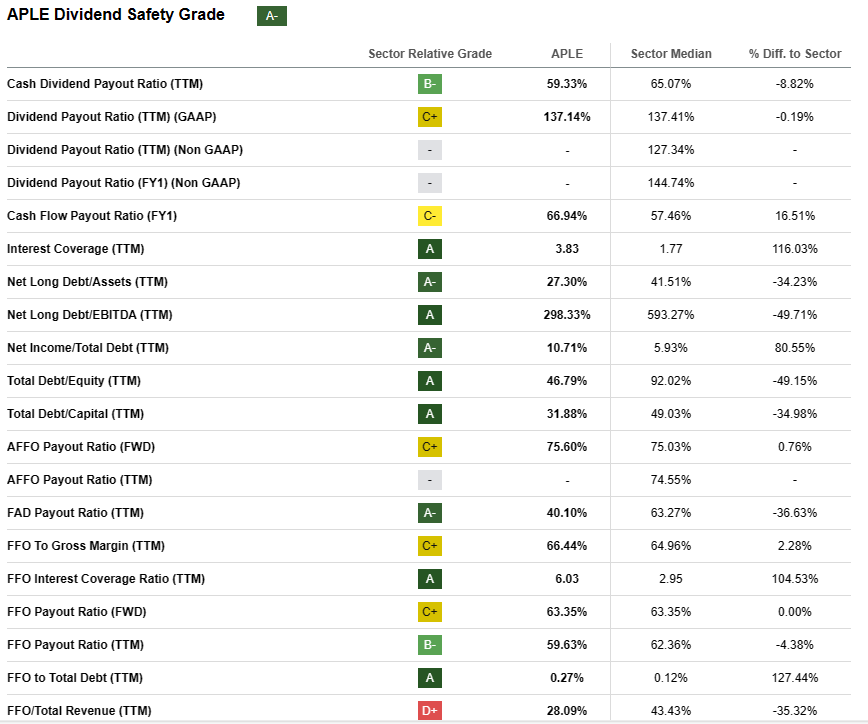

Apple Hospitality

Apple Hospitality is another company whose debt picture is so favorable, and whose revenues are so predictably steady, that it can afford modest payout ratios without danger to the dividend. This company's Debt Ratio is a mere 29%, with a Debt/EBITDA ratio of 3.5, indicating robust ability to pay off their debt with their earnings. Eleven of the 17 data points grade out at B- or better, and none come in at D or worse.

{kind=link}

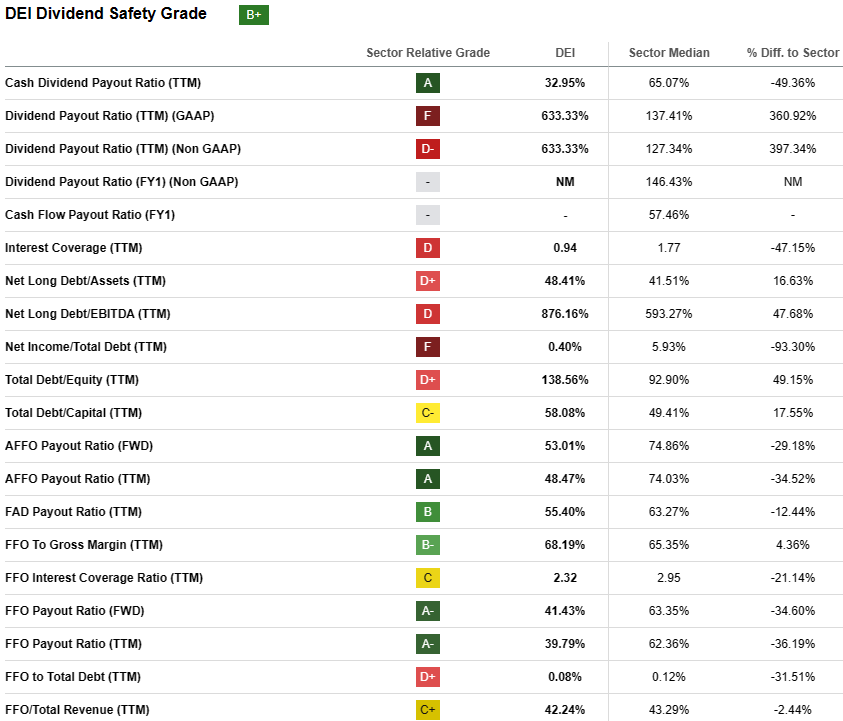

Douglas Emmett

Fellow Office REIT DEI has some significant areas of concern in income/debt ratios, but 7 of the 18 data points are in the A to B- range. The company's Debt Ratio is 55% and Debt/EBITDA stands at 8.2, but while high, these ratios are typical of the Office REIT sector. Meanwhile, the company's FFO dropped about (-10)% this year, and the decline is expected to continue. So the favorable Dividend Safety grade of B+ for DEI is almost entirely a function of the conservative payout ratios.

{kind=link}

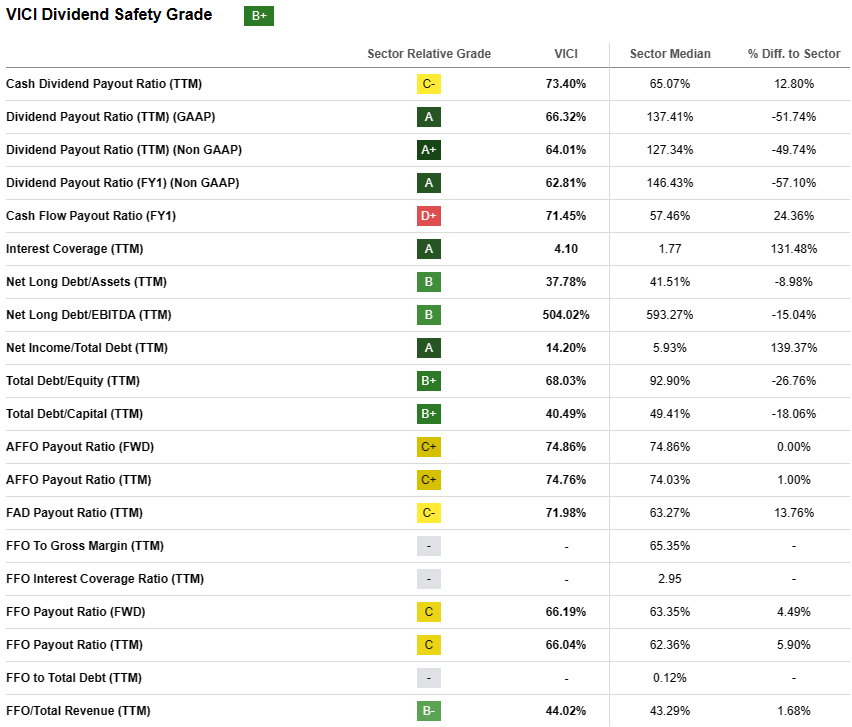

VICI Properties

Casino REIT VICI Properties has 10 data points that grade out at B- or better, of the 17 that apply. Although its payout ratios are modestly aggressive, its debt picture and steady revenues leave little cause for worry. VICI's Debt Ratio of 30% and Debt/EBITDA of 5.7 are both excellent, and its 26.7% growth in FFO per share in 2023 is impressive.

{kind=link}

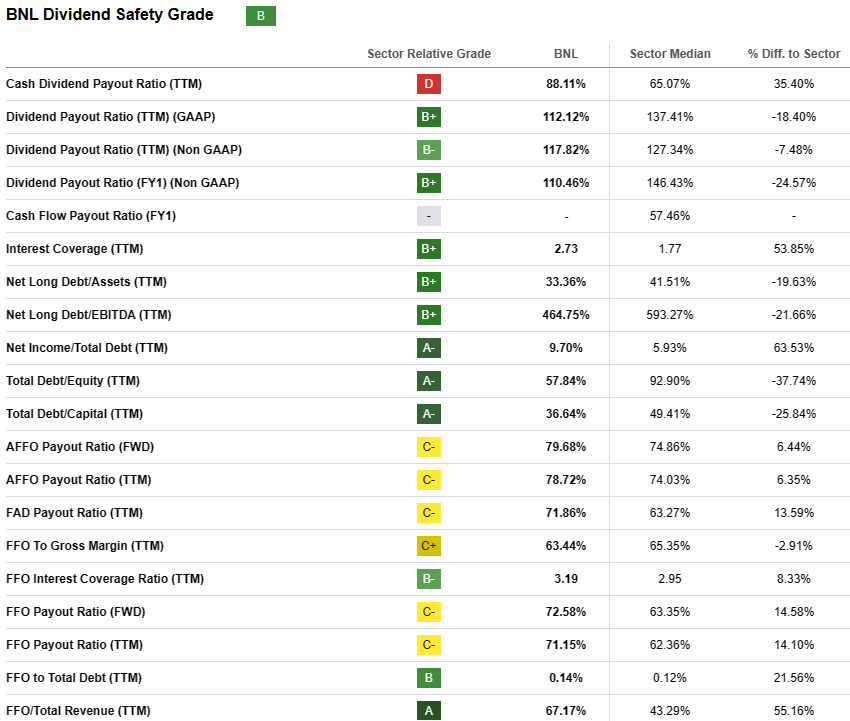

Broadstone Net Lease

Broadstone Net Lease, the first triple-net company to make the list, has 13 data points grading out at B- or better, out of the 19 applicable. Although the payout ratios are a bit more aggressive than the companies listed above, they are still conservative compared to other Net Lease REITs. Meanwhile, the debt and revenue pictures are so favorable that there is little worry about the dividend. The Debt Ratio is a mediocre 39%, but the Debt/EBITDA is excellent, at 4.9. This company's revenues have been remarkably steady since the pandemic.

{kind=link}

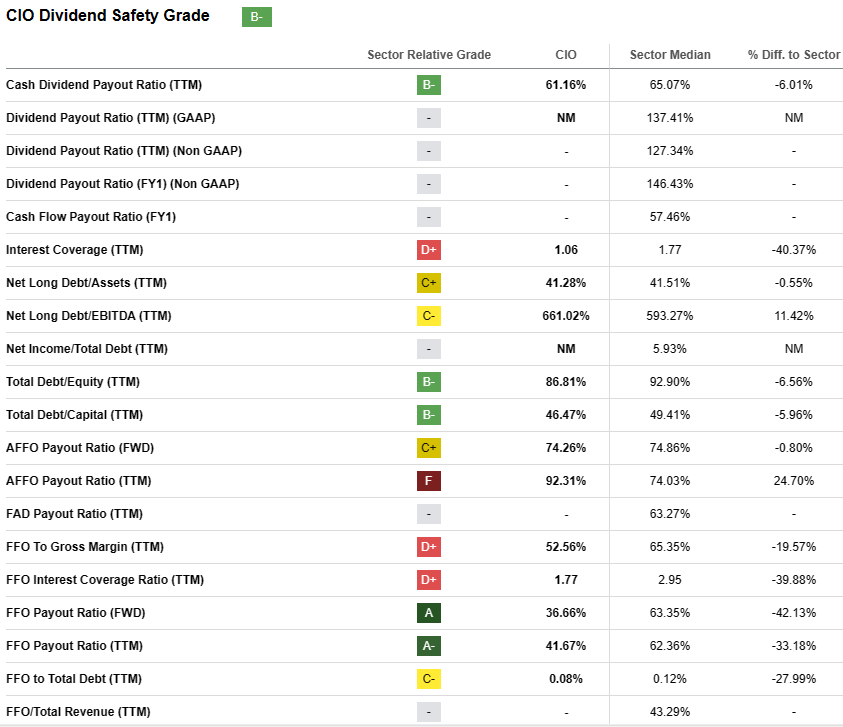

City Office

CIO is a micro-cap ($0.21 billion), so data points are a little sketchier, and there are some interest coverage issues, but the payout ratios are conservative, and the debt/capital and debt/equity pictures are quite good. CIO's Debt Ratio of 60% and Debt/EBITDA of 7.8 are typical of Office REITs at the moment. A note of caution: this is a small, volatile company, whose FFO dived by (-14.0)% in 2023, with more slippage expected next year.

{kind=link}

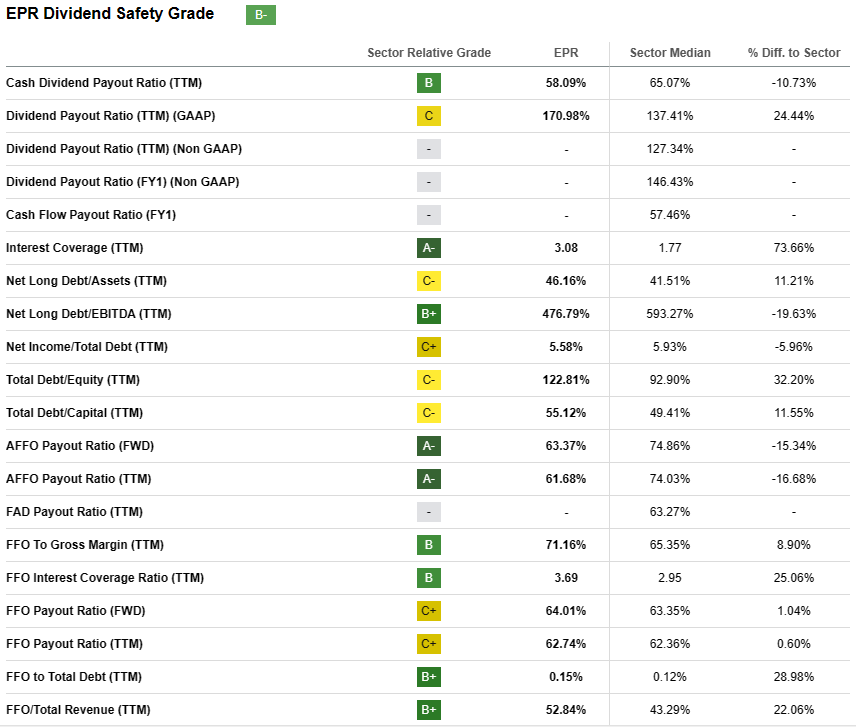

EPR Properties

Triple Net Lease REIT EPR has no data points grading out at D+ or worse, and 9 of the 15 applicable data points grade out at B or better. Payout ratios and debt are moderate, and revenues are healthy. EPR's Debt Ratio of 50% is a bit high, but its Debt/EBITDA of 6.1 is low, indicating a strong chance to earn its way out of its liabilities. FFO per share jumped by 10% in 2023.

{kind=link}

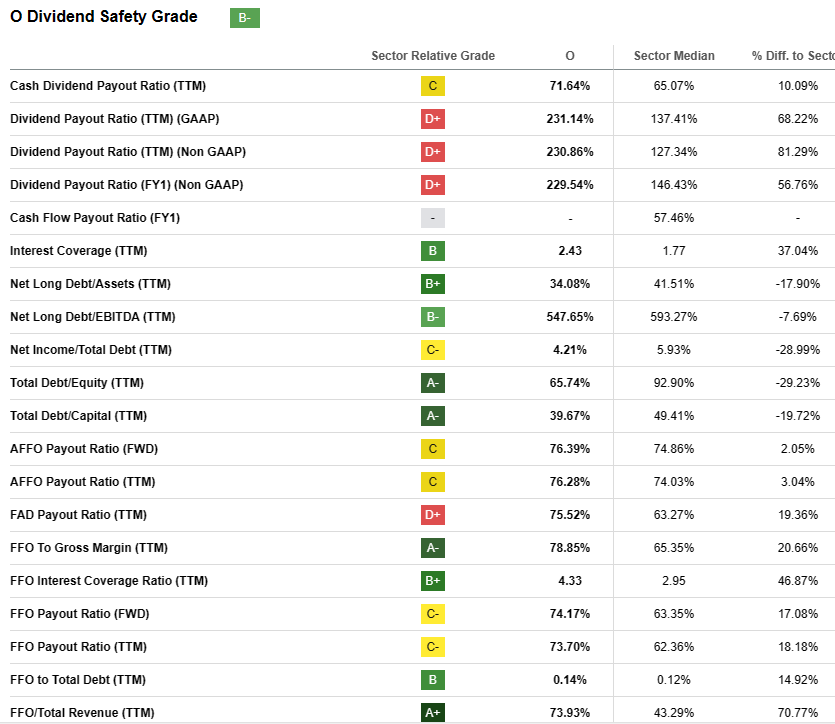

Realty Income

Last but not least, venerable Realty Income's payout ratios are generous, but the debt picture and revenue picture are so healthy that it appears the company can afford its largesse toward the investor. Debt ratio for O is healthy at 31%, and Debt/EBITDA is solid at 6.1 (and excellent for a Net Lease REIT). FFO per share has risen steadily over the past 6 years, right through the pandemic.

{kind=link}

Bottom Line

The companies on this list are not necessarily all Buys. Dividend Safety is only one factor of many, to consider when investing. It is more than possible for any or all of these companies to lose more in share price than they pay in dividends, as we have all seen with so many REITs over the past 2 years. However, the rare combination of high yield and great safety these companies offer, make them excellent candidates for a closer look.

For further details see:

Cash COWs: 11 High-Yield REITS With Very Safe Dividends