VPN - Casino REITs: Hold'Em As Others Fold

Summary

- The lone property sector in positive-territory this year, Casino REITs have benefited from their attractive “inflation-hedging” lease structure, the rebound in Las Vegas travel demand, and broader institutional investor acceptance.

- Casino REITs remain a favorite for investors seeking inflation-hedged assets. VICI boasts inflation-linked escalators on 96% of leases while GLPI benefits from indirect inflation hedges linked to tenant performance.

- Casino REITs have been thrust into the spotlight as apparent beneficiaries of outflows at Blackstone’s non-traded REIT platform BREIT, spawning a $5.5B acquisition of two Vegas casinos by VICI.

- Balance sheet “firepower” and access to longer-term capital have become a significant competitive advantage for public REITs. VICI and GLPI appear particularly well-positioned to play offense while more-highly-levered private peers seek an exit.

- Operational execution is critical, of course, and the potential for a deeper-than-anticipated economic slowdown is an evident risk, but the impressive track record in capital deployment from these REITs justifies our willingness to “pay up” at these moderately elevated multiples.

REIT Rankings: Casino & Gaming

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on December 11th.

{kind=link}

Hoya Capital

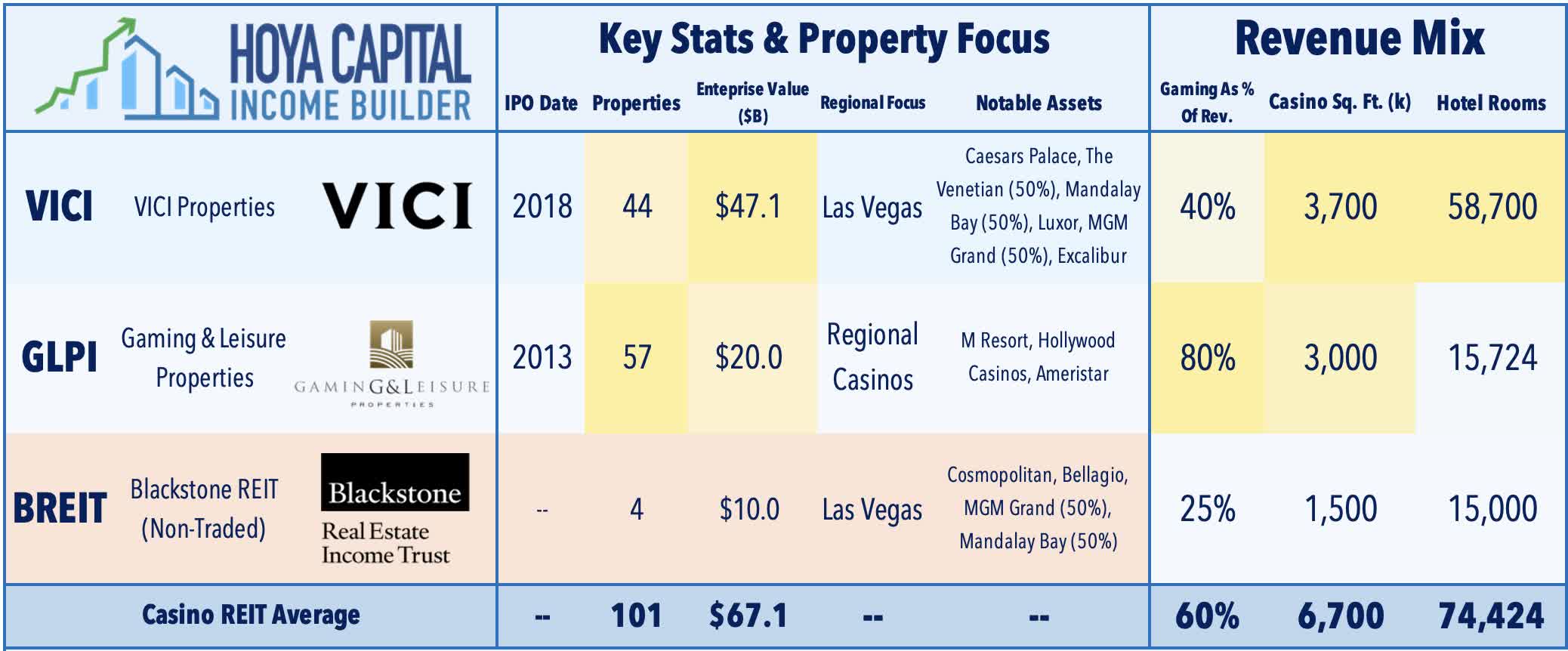

Casino REITs are the lone property sector in positive-territory this year, benefiting from their attractive “inflation-hedging” lease characteristics, significant strength in Las Vegas travel demand, and a broader institutional acceptance, which has fueled a long-awaited upward re-rating. Within the Hoya Capital Casino REIT Index, we track the two casino REITs: VICI Properties ( VICI ) - which owns a dominant share of the Las Vegas casino market following its acquisition of former REIT MGM Properties earlier this year - and G aming and Leisure Properties ( GLPI ) - which owns a portfolio of regional casinos. These two casino REITs account for $47B in market value and own 100 casinos and entertainment facilities across the United States.

{kind=link}

Hoya Capital

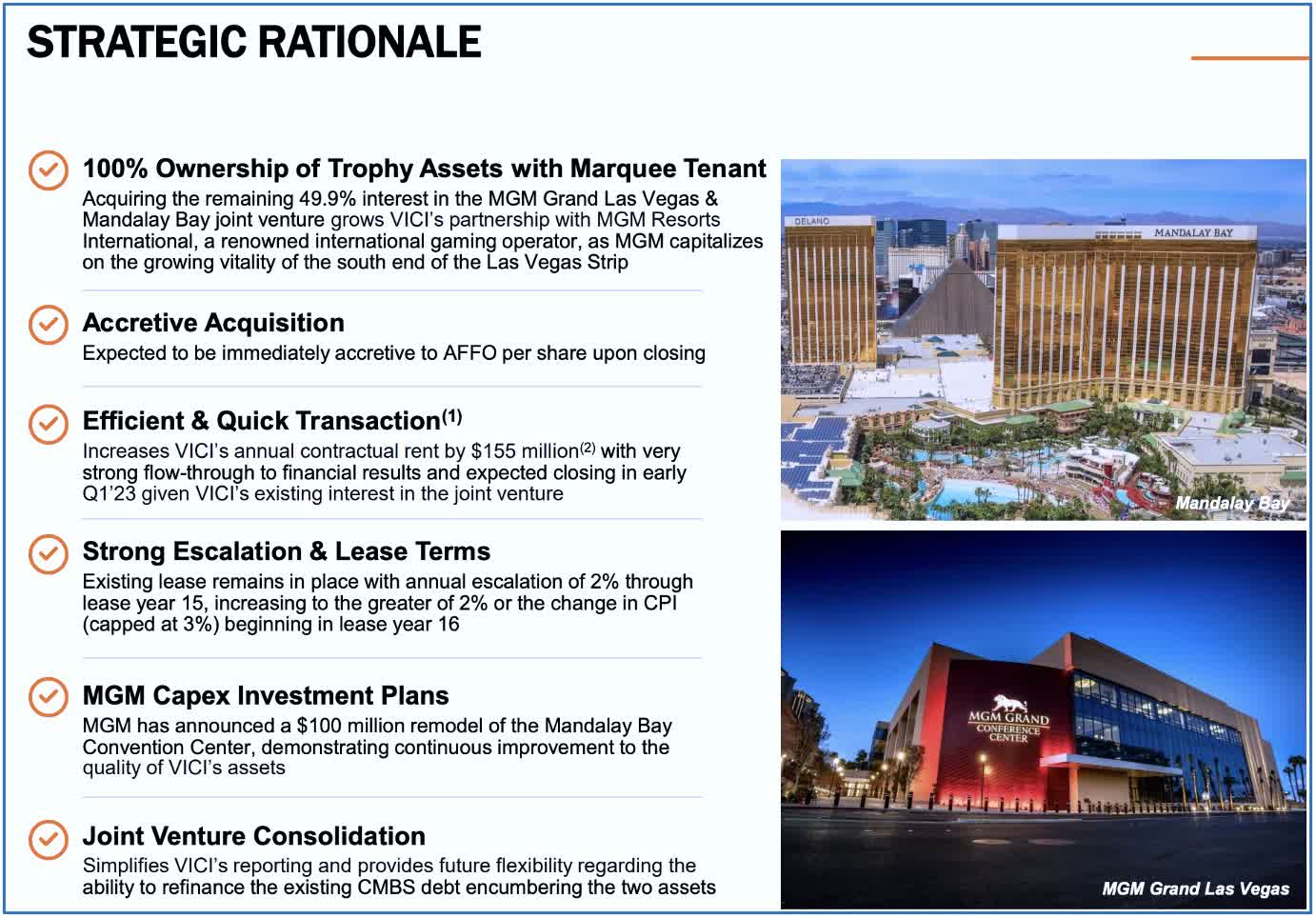

Casino REITs have recently been thrust back into the spotlight as apparent beneficiaries of much-discussed outflows at Blackstone’s ( BX ) massive non-traded REIT ("NTR") platform BREIT, which has been forced to limit investor redemptions after facing a wave of requests that exceeded its monthly and quarterly redemption thresholds. Seeking to raise capital to meet redemptions, BREIT has quickly pivoted from buyer to seller – spawning a major $5.5B deal with VICI for BREIT's 49.9% interests in the MGM Grand and Mandalay Bay. Under the terms of the $5.5B deal, in exchange for its 49.9% share in the MGM Grand Las Vegas and the Mandalay Bay Resort, Blackstone will receive $1.27B in cash while VICI will assume Blackstone's share of roughly $3B in debt. VICI - which will now own 100% of the properties - intends to fund the deal with cash on hand and proceeds from existing equity sale agreements.

{kind=link}

Hoya Capital

The transaction - which has an implied cap rate of 5.6% - is expected to be immediately accretive to VICI's AFFO/share upon closing early next year and will generate annual rent of $310M next year and escalate at a fixed 2.0% rate through 2035 and up to 3.0% thereafter. Notably, VICI Properties CEO Ed Pitoniak commented to CNBC that Blackstone approached him just a couple of weeks ago, and that the deal "came together quickly. "Transacted at favorable terms for the Casino REIT, we speculate that BREIT’s interest in the Cosmopolitan and the Bellagio could soon follow if outflows continue. We've discussed the risks of NTR space across many reports over the past half-decade and continue to watch the area for signs of stress given their typically-high leverage and sensitivity to investor fund flows - which we expect could eventually become an area that's "ripe for picking" for public REITs.

{kind=link}

Hoya Capital

Casino REITs now command a relatively dominant share of the U.S. casino real estate ownership market. These two Casino REITs have acquired over $50 billion in assets since the start of 2016 including VICI's acquisition of the real estate assets of The Venetian from Las Vegas Sands for $4 billion in cash which was the largest REIT-involved deal before VICI's acquisition of MGM Growth Properties. As we bid farewell to one REIT - MGM Properties - another player emerged onto the casino scene this year with Realty Income ( O ) - the largest net lease REIT - acquiring Encore Boston Harbor from Wynn Resorts for $1.70 billion and indicating that will be an active player in the casino business.

{kind=link}

Hoya Capital

Emerging in the mid-2010s, casino REITs had seemingly been flying under the radar over the past several years despite delivering steady and consistent outperformance and high-single-digit FFO growth fueled by this continued wave of accretive acquisitions and industry consolidation. Much like their retail-focused net lease REIT peers, external growth through acquisitions is the modus operandi of the casino REIT sector and while casino REITs now own more than a third of the total "investment-grade" casinos in the United States, recent deals and management commentary indicate that the acquisition environment remains active and should continue to provide a steady source of FFO growth for the foreseeable future given these REITs' relatively favorable cost of capital and unique competitive positioning.

{kind=link}

Hoya Capital

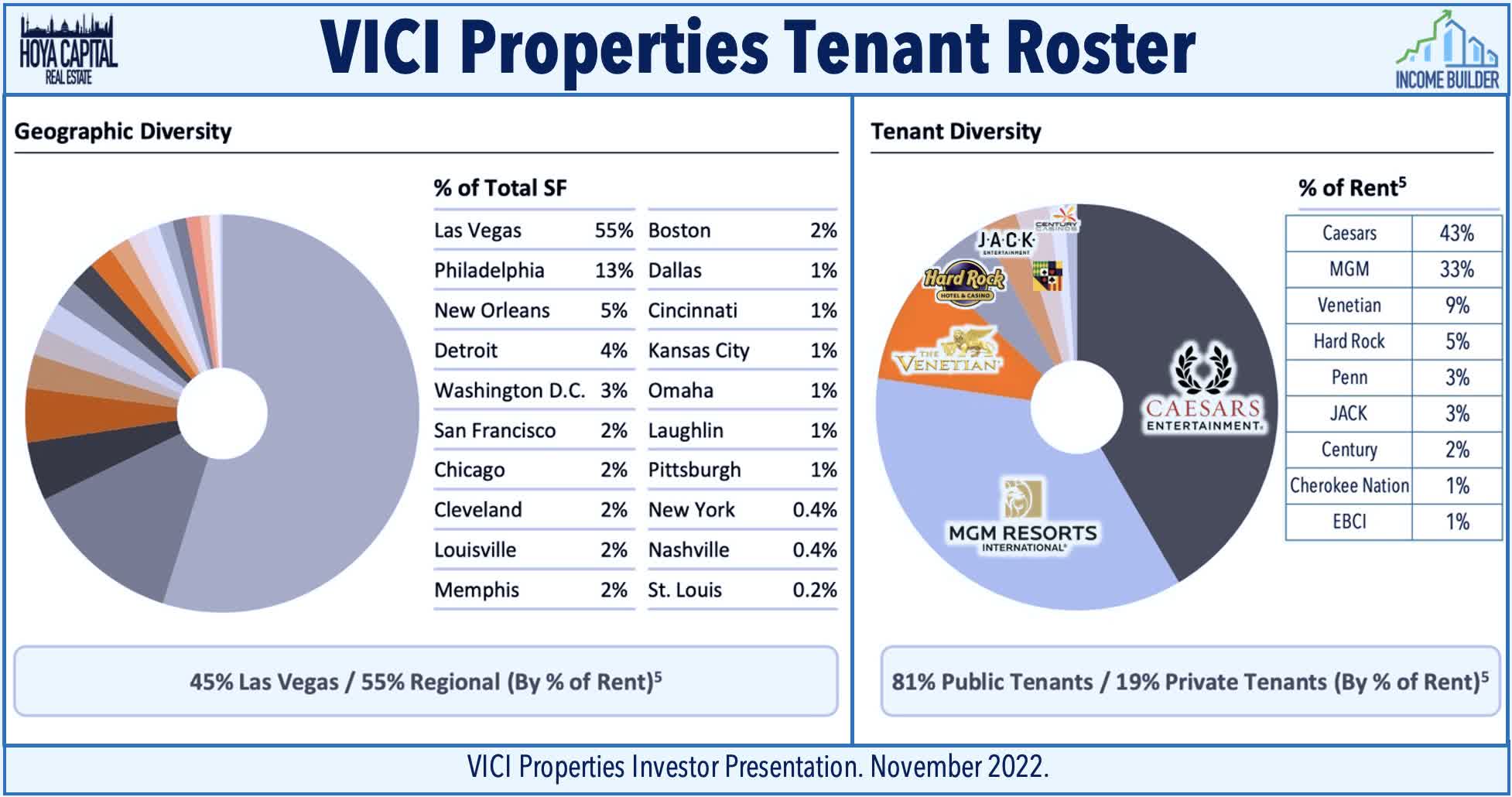

Taking a step back, VICI emerged as a "spin out" from Caesars Entertainment ( CZR ) in 2018 and has seen its market capitalization swell by 5x since its IPO. The new "King of Vegas," VICI now owns 44 properties across 15 states - a portfolio that includes 59k hotel rooms and 3 of the 5 largest hotels in the country. Its recent combination with MGP further diversifies VICI's tenant concentration and geographical scope, lowering its largest tenant exposure - Caesars - from nearly 80% at the end of 2020 to just 42% following the closing of the MGP deal and the $4B acquisition of The Venetian from Las Vegas Sands earlier this year. The MGM Growth Properties portfolio - which was initially spun out in 2016 by MGM Growth ( MGP ) owned 15 destination casinos including Mandalay Bay and the MGM Grand Las Vegas.

{kind=link}

Hoya Capital

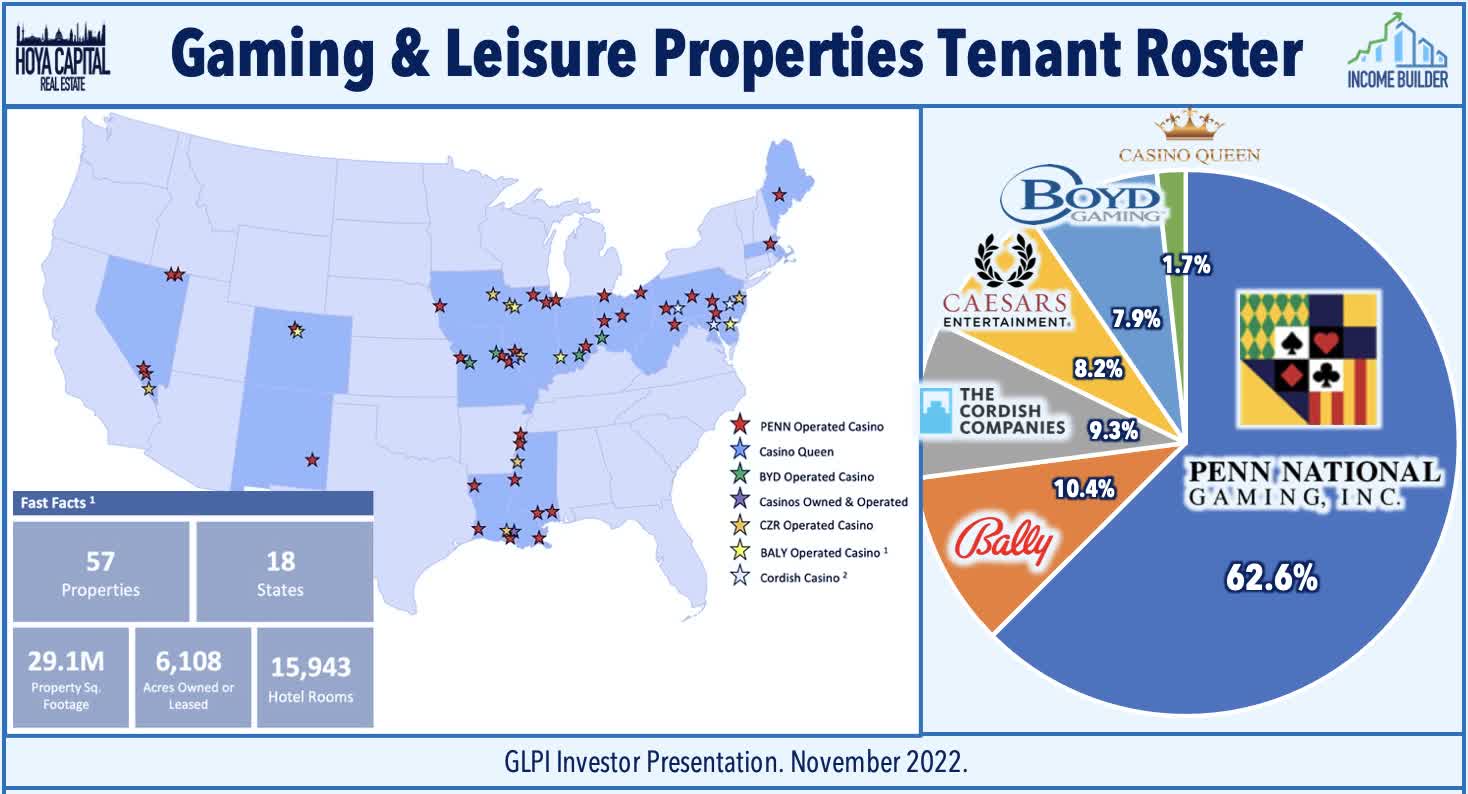

GLPI - which was spun out from Penn Entertainment ( PENN ) in 2013 - has also been an active and successful consolidator of regional casino assets, growing its market capitalization by nearly 4x since 2016. GLPI was also a bidder for MGP, but commented that the valuation "did not pencil for us" conceding that "it's a better deal for [VICI] than it would have been for us." GLPI did score a win in late 2021 with a major $1.8B acquisition of the Live! casinos in Maryland, Philadelphia, and Pittsburgh from Cordish Companies. Acquired at a 6.9% cap rate, the acquisition is GLIP's largest since 2016 and helps to diversify its tenant base further. GLPI now owns 57 properties across 18 U.S. states - primarily focused on regional casinos, which rely more heavily on gaming revenues compared to their Las Vegas peers which see a higher share of revenues from non-gaming hospitality and convention activity.

{kind=link}

Hoya Capital

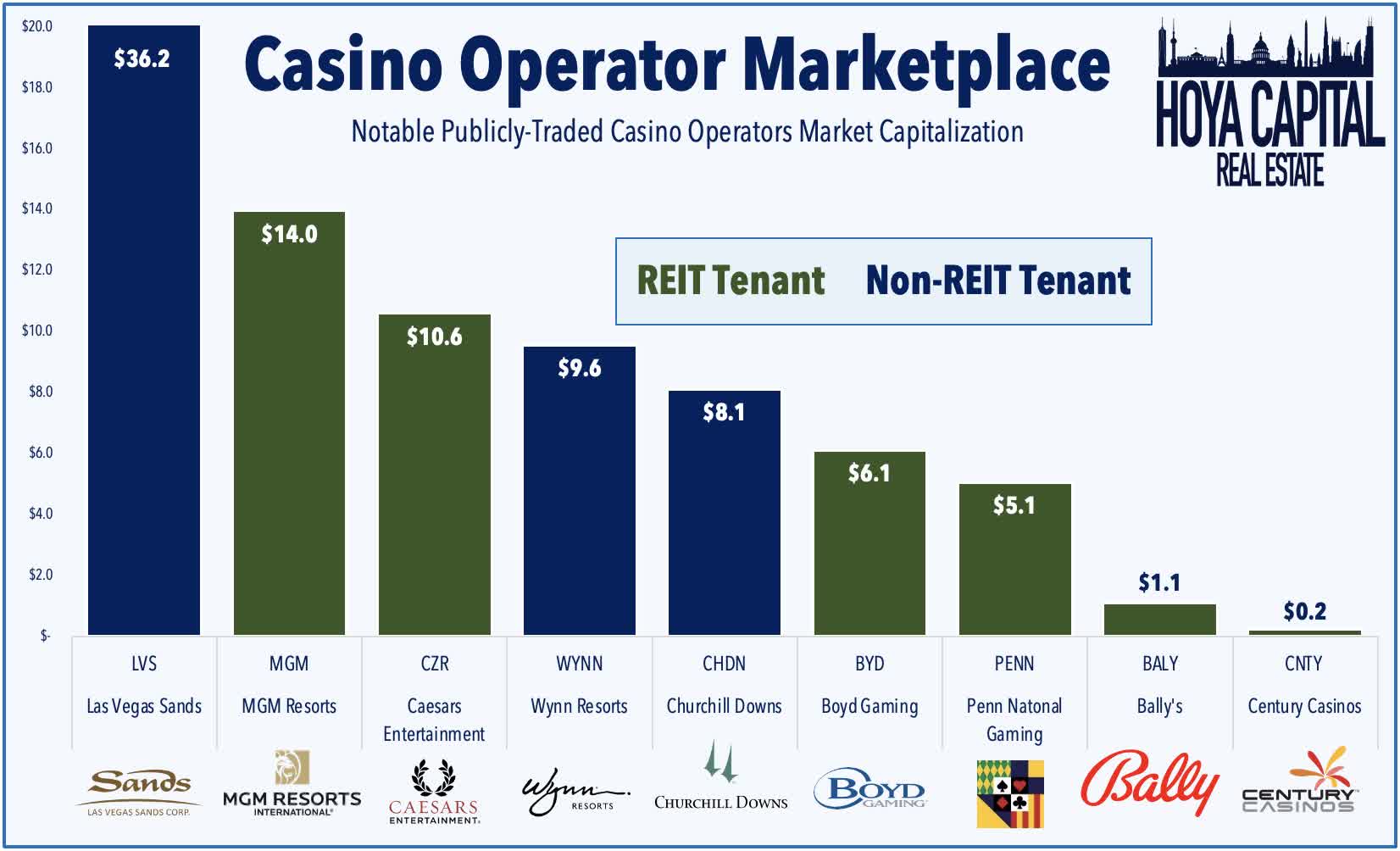

While not a publicly-traded REIT, Blackstone ( BX ) had been nearly as active in the casino space as VICI and GLPI over the past five years. In addition to its 49.9% JV stakes in the MGM Grand and Mandalay Bay which it had acquired alongside MGP in 2020, BREIT owns an 80% stake in The Cosmopolitan of Las Vegas and a 95% stake in The Bellagio while Blackstone's private equity division also owns the Aria Resort in Las Vegas. In addition to the aforementioned operators, other major casino operators include Las Vegas Sands ( LVS ), Wynn Resorts ( WYNN ), Churchill Downs ( CHDN ), Boyd Gaming ( BYD ), Bally's ( BALY ), and Century Casinos ( CNTY ) - most of which still retain ownership some or most of their real estate assets that could be potential future sale-leaseback opportunities for casino REITs. Other key publicly-traded players in the online gambling industry include DraftKings ( DKNG ), FanDuel/Flutter Entertainment ( OTCPK:PDYPY ).

{kind=link}

Hoya Capital

Deeper Dive into Casino REIT Sector

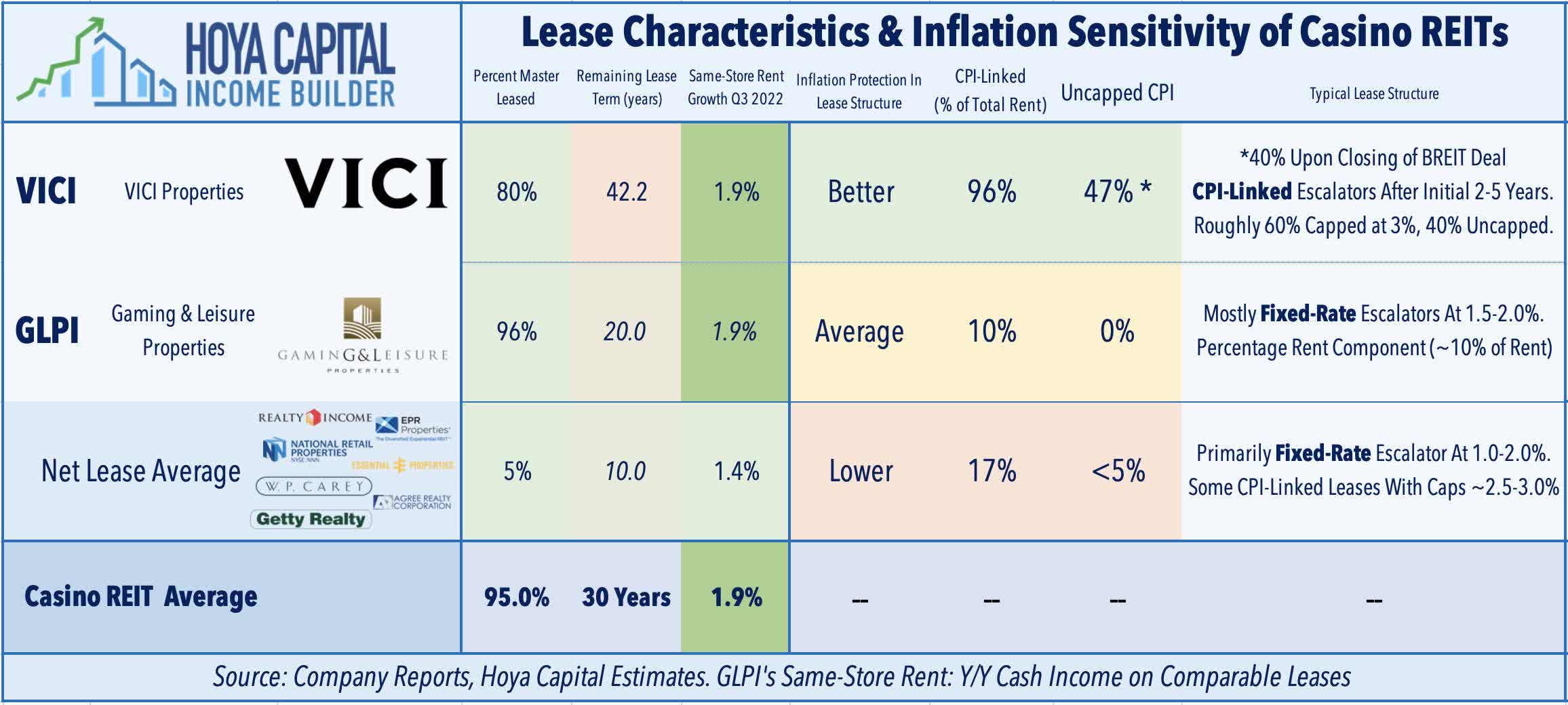

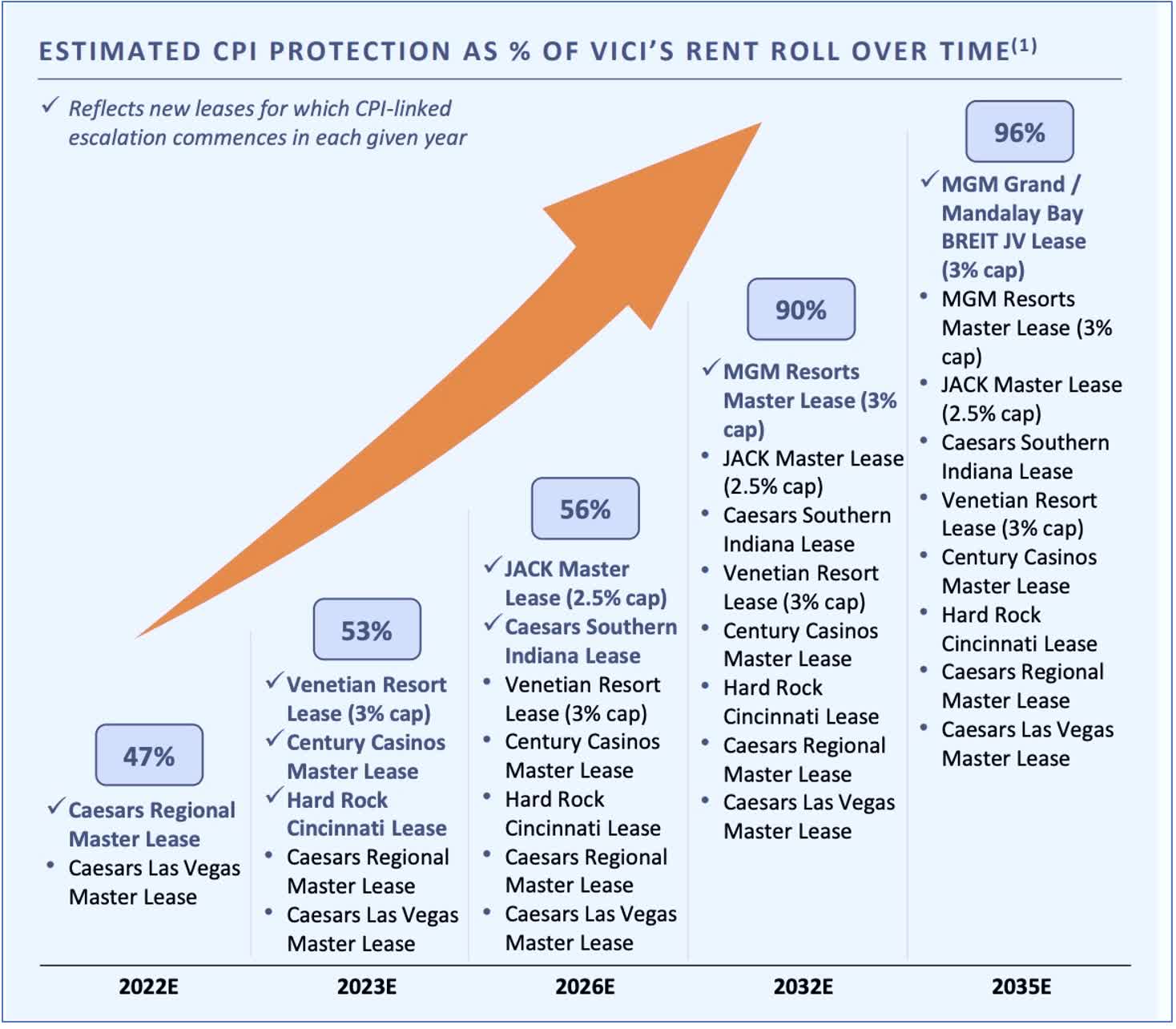

Despite their ultra-long-term triple net lease structures, casino REITs are better protected from inflation than many initially presumed. Inflation sensitivity is driven by several interacting factors including external growth potential, lease structure and term, tenant credit quality, and the cyclicality of the underlying property type. VICI boasts inflation-linked escalators on 96% of its leases – and importantly - 47% of its leases use uncapped CPI for the annual escalation formula (40% following the aforementioned deal with BREIT.) GLPI's inflation protection, by comparison, is less direct with few explicit CPI linkages - but most of its leases do include a percentage rent component – roughly 10-15% of its cash rental income – along with the 1.5%-2.0% escalator that is generally tied to rent coverage ratio thresholds - which together result in a pro-cyclical dimension to its cash flow stream.

{kind=link}

Hoya Capital

By comparison, among traditional net lease REITs, only a handful include explicit CPI linkages in their rent escalators including W.P. Carey ( WPC ) - one of our larger portfolio holdings in our REIT portfolios - which uses a significant percentage of “uncapped” CPI escalators. WPC expects same-store growth to accelerate to “closer to 4% in early 2023 resulting from these escalators – which will be more than double the same-store growth of the average net lease REIT. VICI applies the rental rate escalator in November using the July, August, and September CPI figures – during which CPI averaged 8.5% - and VICI’s current 2022 FFO guidance excludes any CPI impact. We expect VICI to report same-store NOI growth of at least 3% in 2023 – up significantly from the 1.9% rate reported so far in 2022 and double its historical average.

{kind=link}

Hoya Capital

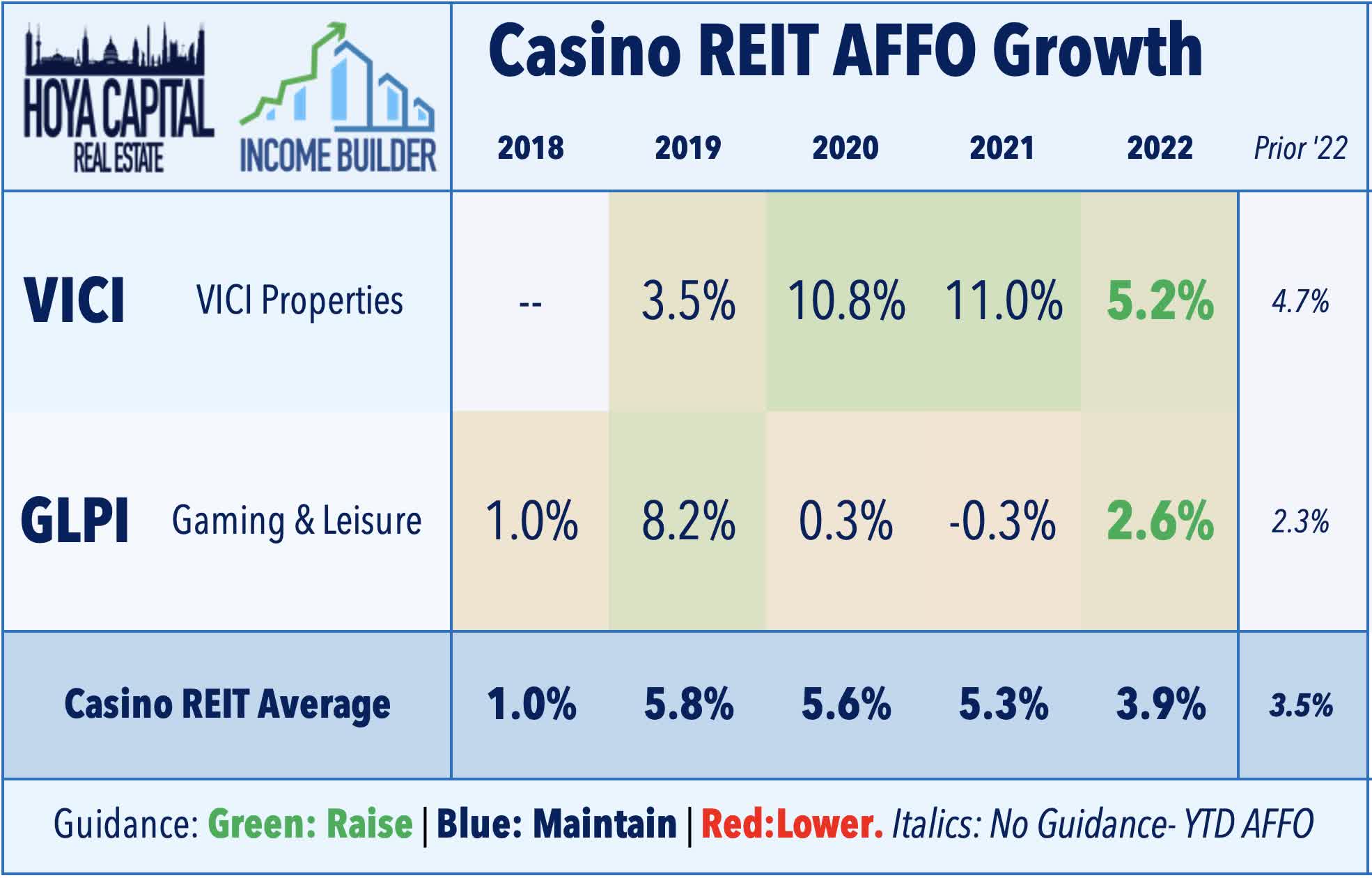

Vegas Is Back – and more popular than ever. As discussed in our REIT Earnings Recap , third-quarter results were above consensus estimates as the effects of the inflation-linked escalators began to be seen. VICI Properties ( VICI ) and Gaming and Leisure Properties ( GLPI ) each raised their full-year FFO outlook with VICI now seeing FFO growth of 5.2% - up 50 basis points from its prior guidance - while GLPI now projects FFO growth of 2.6% - up 30 basis points. Of note, despite the substantial COVID-related issues across the hospitality industry, casino REITs reported spotless rent collection throughout the pandemic and were two of less than a dozen REITs to report positive FFO growth in 2020. While VICI has recorded impressive double-digit FFO growth in each of the past two years, GLPI had stumbled a bit more than its peers during the pandemic due to the variable rent component in its leases.

{kind=link}

Hoya Capital

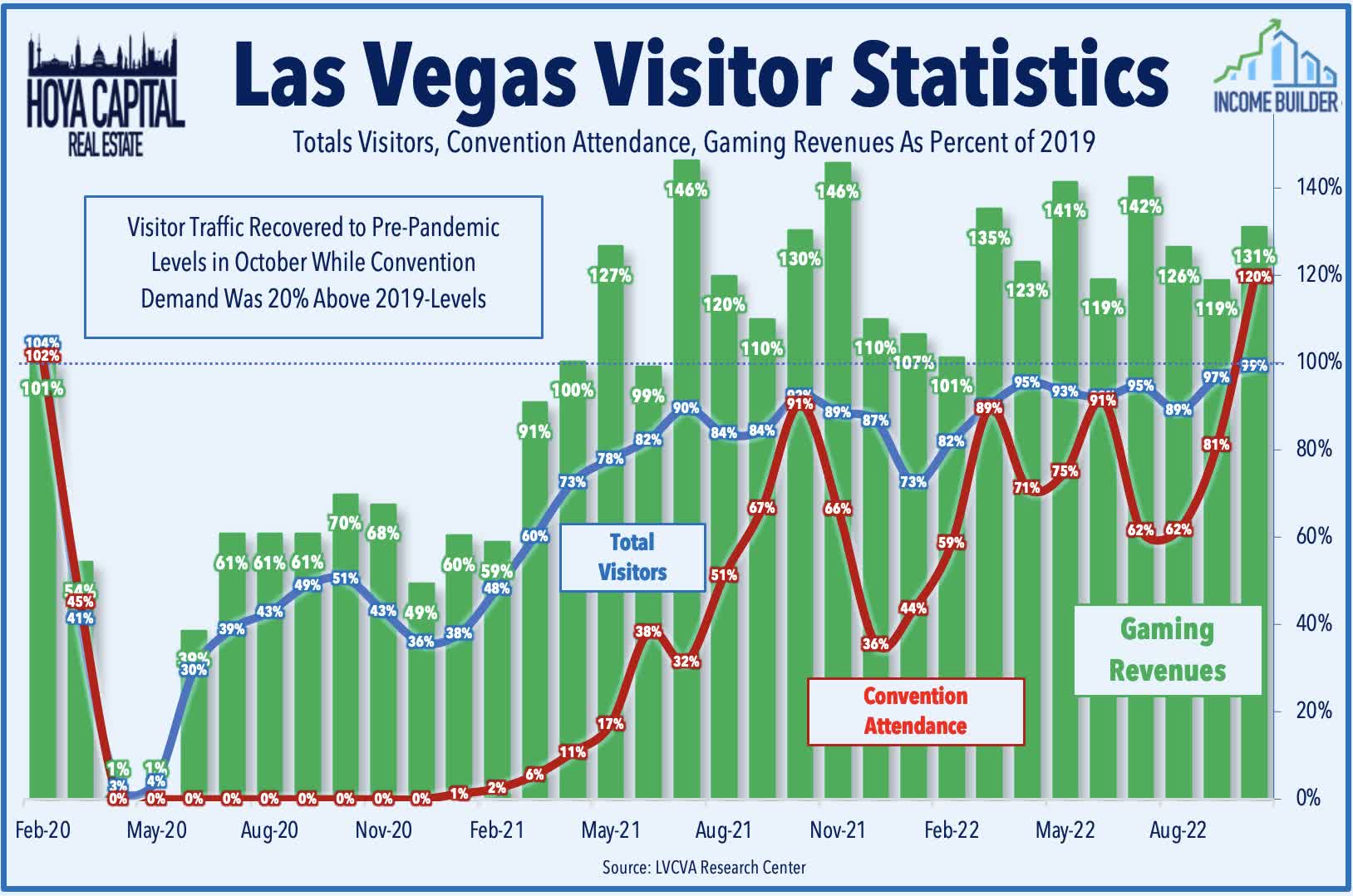

Las Vegas has been a notable outperformer among domestic travel destinations throughout the pandemic and this relative strength has continued despite signs of emerging softness in leisure-oriented travel demand in recent months. The Las Vegas Convention and Visitor Authority reported last month that total visitor traffic to Las Vegas returned to pre-pandemic record-highs in October, defying a broader moderation in occupancy levels seen across most other major markets since late Summer. Critically, convention attendance exceeded pre-pandemic levels in October for the first time last month while Vegas hotels recorded total revenues that were 50% above October 2019 levels. Regional casinos recorded Gross Gaming Revenues that were 14% above 2019-levels while Vegas casinos recorded GGRs that were 31% higher than 2019 – gains that have importantly come alongside – not in spite of - the growing popularity of iGaming and sports betting.

{kind=link}

Hoya Capital

Casino REIT Performance & Fundamentals

Casino REITs were slammed during the early onset of the outbreak amid the stifling economic lockdown that forced the majority of properties across the country to close temporarily, but mounted a furious comeback in the back half of 2020 and ended the year as one of the best-performing REIT sectors and continued that strong performance in 2021 and into 2022. Casino REITs are now the single-best-performing property sectors this year, higher by 11.1% this year compared to the 26.0% decline from the broad-based Vanguard Real Estate ETF ( VNQ ) and the 17.2% decline from the S&P 500 ( SPY ).

{kind=link}

Hoya Capital

As we've projected for the past several years, casino REITs have indeed benefited from an upward "re-rating" from investors as the sector has matured and as the business model - and economic "moat" around these REITs - has become better understood. As noted above, Casino REITs are now trading at multiples that are actually slightly above their similarly-sized net lease REIT peers with a Price/FFO multiple of roughly 17x. Critically, unlike their hotel REIT peers which have been among the worst-performing REIT sectors since the start of the pandemic, casino REITs' ultra long-term (15-50 year) triple-net master lease structure leaves most of the financial and operational risk - both on the upside and the downside - to their tenants. As a result, casino REITs have delivered some of the strongest 5-year returns in the REIT sector.

{kind=link}

Hoya Capital

Deeper Dive Into Casino REIT Sector

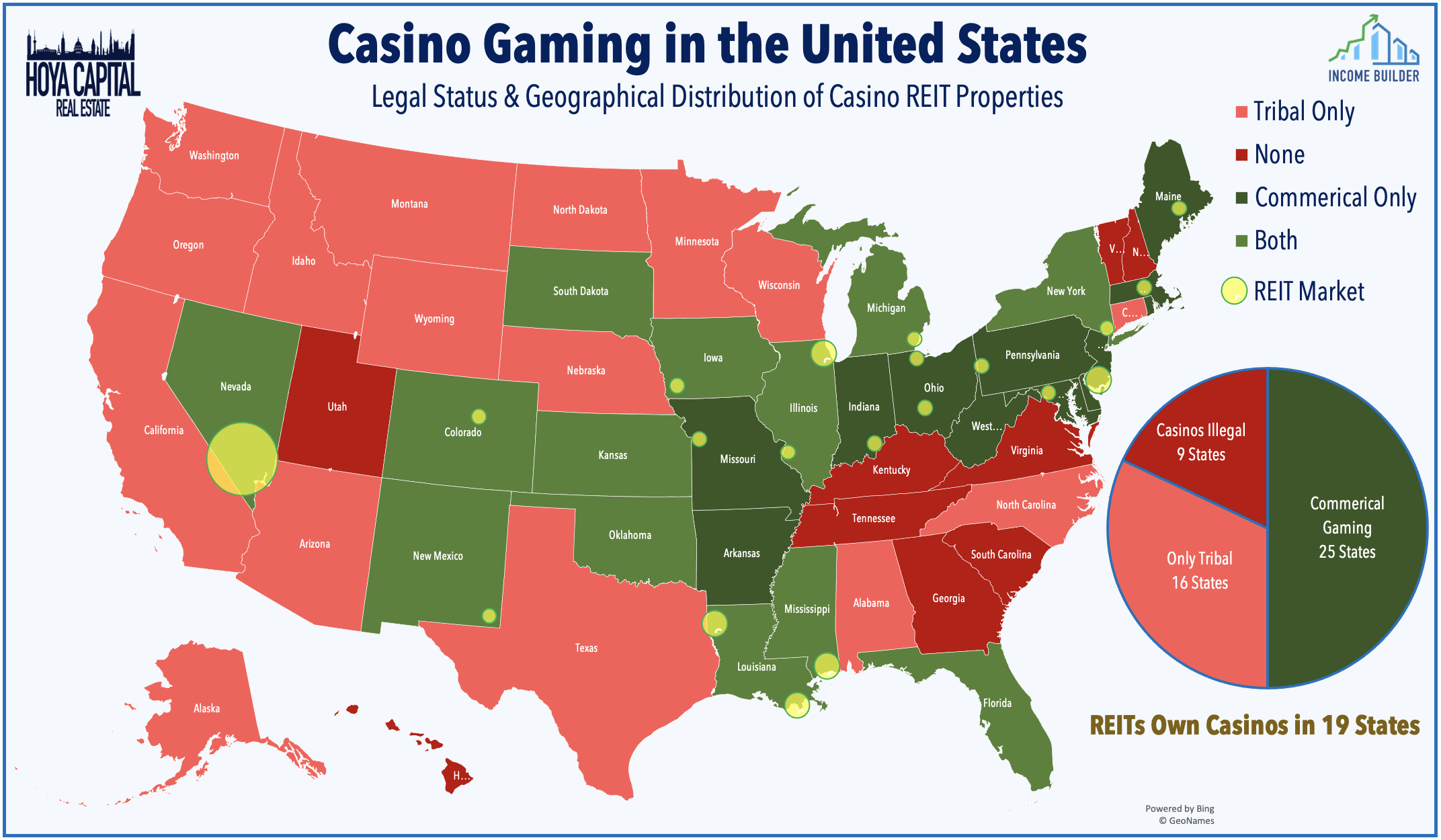

"Headquartered" in Las Vegas, gambling is one of the most highly regulated industries in the United States. Until the 1980s, commercial casinos were prohibited outside of "The Strip," leaving the lucrative gaming business to Native American tribes, who were largely exempt from state prohibitions. The last forty years have seen a wave of legalization of commercial casinos as states increasingly realized the "tax goldmine" they were sitting on. Tax revenue from gaming, for instance, represents nearly a quarter of state tax revenues collected by Pennsylvania. Twenty-five states now permit commercial casinos and these three REITs own properties in nineteen of these states.

{kind=link}

Hoya Capital

Blending some of the better attributes from each of the net lease, hotel, and healthcare REIT sectors, casino REITs emerged in a fashion similar to many lodging REITs as "spinoffs" designed to separate the capital-intensive real estate business from the operationally-intensive property management business. Casino REITs now own 100 of the roughly 250-300 "investment grade" commercial casinos in the United States, one of the highest concentrations of REIT ownership within any property sector. We've long viewed casino REITs as a compelling "under the radar" alternative to other seemingly "cheap" sectors facing stiffer secular headwinds. Like their net lease peers, casino REITs are some of the most operationally efficient property sectors, operating with Adjusted NOI margins of nearly 90%, leaving most of the financial risk and capital expenditure responsibilities to their tenants.

{kind=link}

Hoya Capital

Takeaway: Hold'Em As Others Fold

Casino REITs - the lone property sector in the green this year - have benefited from their “inflation-hedging” lease structure, notable strength in Las Vegas travel demand, and broader institutional investor acceptance. Casino REITs have recently been thrust into the spotlight as apparent beneficiaries of issues at Blackstone’s non-traded REIT platform BREIT, spawning a $5.5B acquisition of two Vegas casinos by VICI. A theme that we see across many REIT sectors, balance sheet “firepower” and access to longer-term capital have become a significant competitive advantage for public REITs. VICI and GLPI appear particularly well-positioned to play offense while more-highly-levered private peers seek an exit. Operational execution is critical, of course, and the potential for a deeper-than-anticipated economic slowdown is an evident risk, but the impressive track record in capital deployment from these REITs justifies our willingness to “pay up” at these moderately elevated multiples.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Casino REITs: Hold'Em As Others Fold