EMR - Caterpillar: Making Itself Indispensable To Its Customers

2023-10-02 14:15:50 ET

Summary

- Caterpillar is making itself indispensable to its customers in the mining industry by providing complete solutions to decarbonization, including electrified equipment and AI optimization.

- The company has seen strong net income growth, but the share price has lagged behind. However, there is potential for strong double-digit returns in the future.

- CAT is leveraging AI and digital advancements to revolutionize its industry and improve autonomous operation, equipment utilization, and maintenance.

Investment Thesis

CAT is making itself indispensable to its customers, particularly in the mining industry, by providing complete solutions to decarbonization, which solutions include specially designed CAT equipment, including electrified trucks, hydraulic shovels, drills, large wheel loaders and dozers. This creates a fertile environment for application of AI to optimize in a digitized, electrified, autonomous operation. Continuing advancement in these areas can be expected to secure for a competitive advantage for CAT.

Caterpillar ( CAT ) grew net income at an average of around 26% over the six years to the end of 2022, with the share price lagging at a growth rate of ~17% per year. SA Premium Analysts' consensus EPS estimates indicate a flattening out of EPS growth through the end of 2024, and even negative EPS growth beyond 2024. Given the initiatives CAT is undertaking, I believe a proportion of contributing analysts might be underestimating CAT's growth potential. It is believed CAT can return strong double-digit returns, buying now and holding at least through the end of 2024. On that basis I rate CAT a Strong Buy. More detailed support for this contention is included in the additional analysis and comment section below. Firstly, I wish to explain in greater detail how CAT is going about making itself indispensable to its customers.

How Caterpillar Is Making Itself Indispensable To Its Customers:

In his recent article, " Top 10 AI Stocks To Kick Off The 4th Quarter ", Steven Cress identified Caterpillar Inc. ((CAT)) as one of several companies benefitting from the leveraging of AI in an industrial setting, rather than as a pure AI developer. Here is what Mr. Cress had to say on these companies in his article:

Staying ahead of the competition today means forging a path with digital advancements, particularly AI, for simplified, quicker, and cost-effective solutions. Where the 10 top AI stocks are centered around tech industries, other industries can leverage artificial intelligence for a competitive advantage. Highlighted earlier in the table showcasing 16 Strong Buy stocks are Caterpillar ((CAT)), Deere & Company ( DE ), and Emerson Electric ( EMR ). While non-tech, CAT, DE, and EMR have revolutionized their industries through transformative technology, complemented by underlying solid fundamentals. Where many industries, including construction, agriculture, and machinery, have made substantial investments into the ability for autonomous equipment operation through AI, improvements in their equipment designs serve as strategic business solutions, long-term safety solutions, and cost savings.

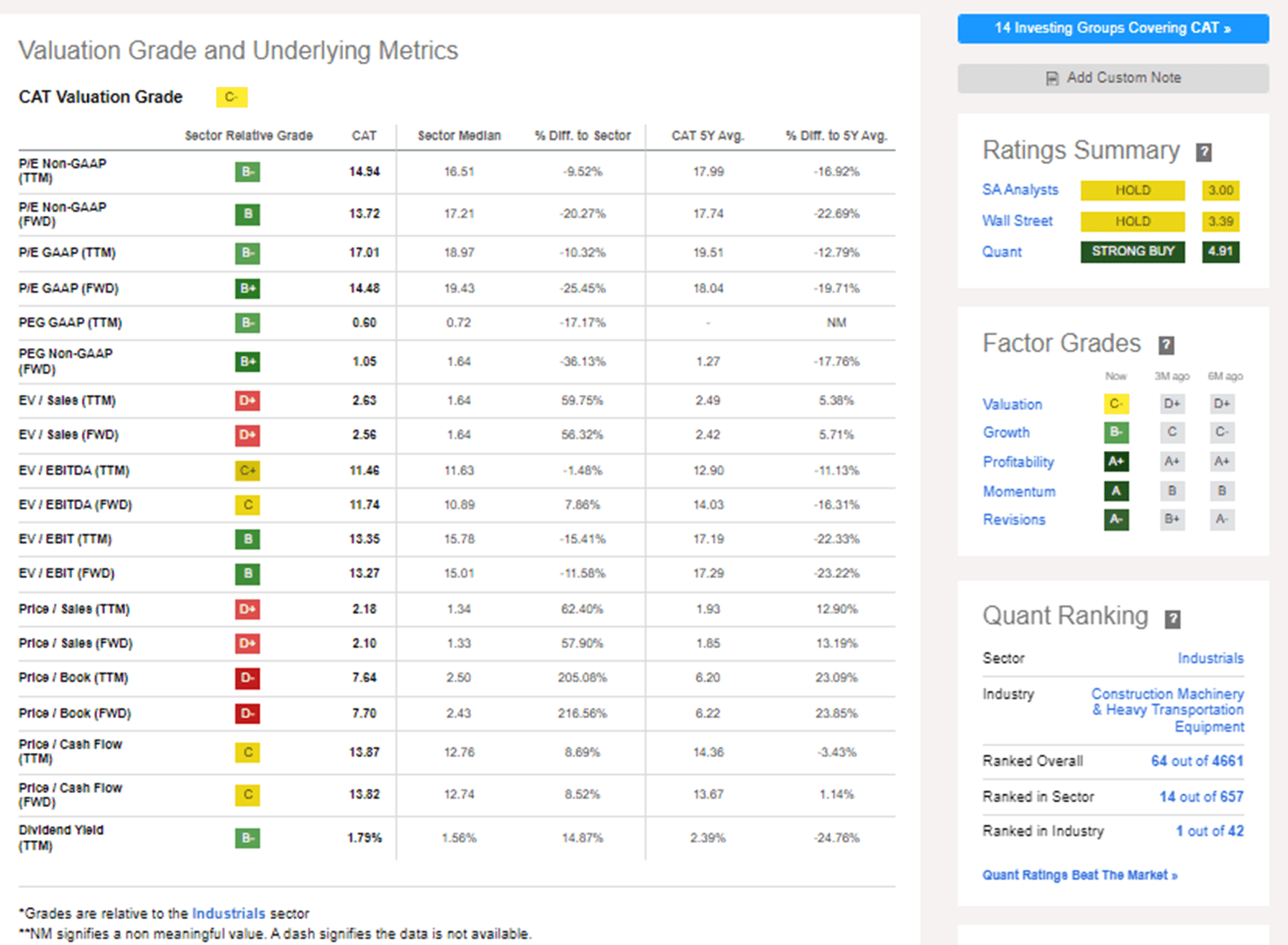

Figure 1 below shows the factor grades resulting in a QUANT Strong Buy recommendation for CAT compared to Hold ratings from Wall Street and SA Analysts.

Figure 1:

{kind=link}

The Factor Grades show a weakness for Valuation factor grade. Closer inspection shows the weakness primarily stems from poorer performance (D grades) for EV/Sales and Price/Sales and Book. However, B grades for P/E ratios and Dividend yield, indicate the shares are favorably priced compared to peers.

CAT In Strong Position To Leverage AI -

CAT is moving with the times, facilitating its customers decarbonization of their industries, particularly mining. This is not a recent initiative but activities are heating up. In the 1990s CAT established the Tucson Proving Ground .

Figure 2

{kind=link}

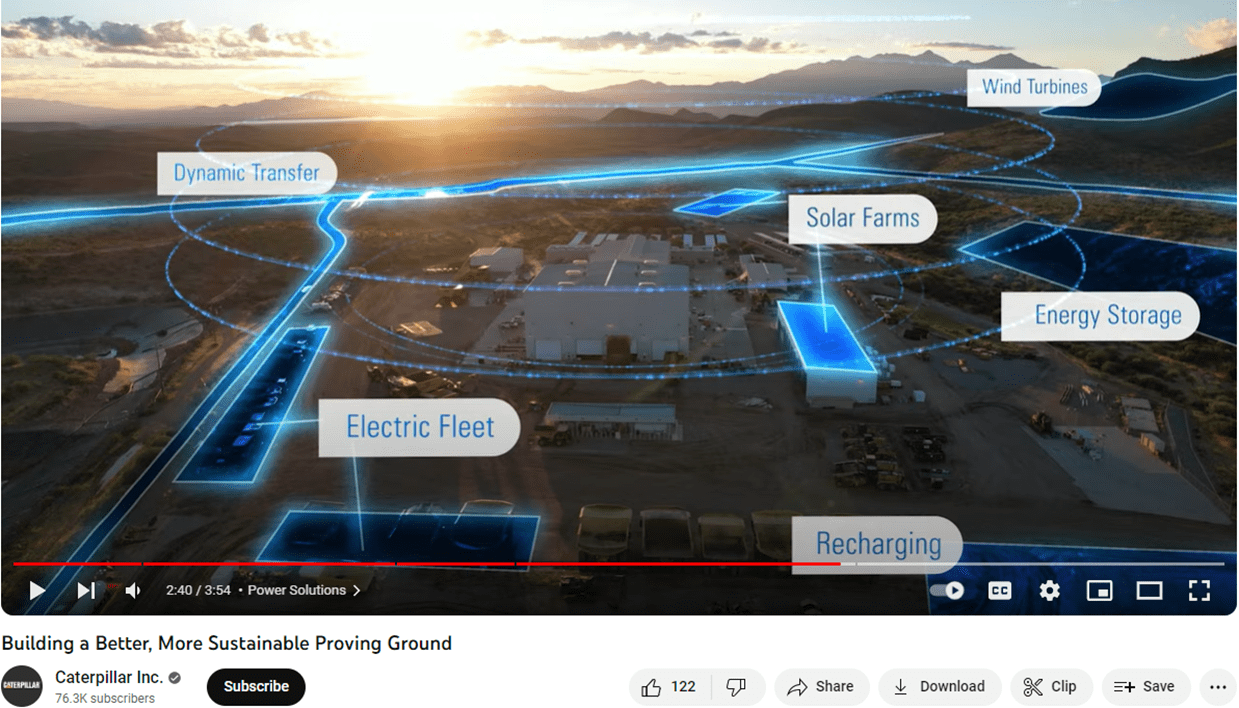

As part of the advancement of its sustainability journey, CAT is making a major investment to transform Caterpillar's premier Arizona-based testing and validation site into a state-of-the-art, fully operational mine site of the future, with all the features shown in Fig.3 below.

Figure 3:

{kind=link}

Diesel generators have been replaced by 2 MW of solar power, 3 MW of wind power, 18+ MWh of battery storage, 2 gas gen sets capable of running on natural gas, 100% hydrogen, or a blend of both. Excess energy will be used to create and store hydrogen and that hydrogen will be used for testing of FCEV powered machines, as well as generating electricity to provide greater energy resilience. To learn how to transfer energy to CAT machines and supporting facilities, the proving ground is installing infrastructure to support both stationary and mobile charging. Digital solutions are being added to orchestrate the overall power and production management ecosystem, creating the right balance for a working mine site in real-time to support CAT's growing portfolio of electric and autonomous solutions. The development area is being expanded to demonstrate the benefits of running a mine site as a complete system supported by CAT's advanced automation technology. All of the foregoing puts CAT in a strong position to leverage AI to improve autonomous operation, and to better manage equipment utilization and maintenance, including battery charging and battery life.

The Arrival Of The CAT Electric Haul Truck -

Fig. 4 below shows early learner customers in front of Caterpillar's first battery electric 793 large mining truck demonstrated at the company's Tucson Proving Ground.

Figure 4

{kind=link}

The Early Learner program launched in 2021 and focuses on accelerating the development and validation of Caterpillar's battery electric trucks at participating customers' sites. Per Caterpillar announcement in November 2022 ,

Early Learner customers came together to witness a live demonstration of Caterpillar's prototype battery truck on a seven-kilometer (4.3-mile) course. During the event, Caterpillar monitored over 1,100 data channels, gathering 110,000 data points per second, to validate simulation and engineering modeling capabilities. Fully loaded to its rated capacity, the truck achieved a top speed of 60 km/h (37.3 mph). The loaded truck traveled one kilometer (0.62 mile) up a 10% grade at 12 km/h (7.5 mph). The truck also performed a one kilometer (0.62 mile) run on a 10% downhill grade, capturing the energy that would normally be lost to heat and regenerating that energy to the battery. Upon completing the entire run, the truck maintained enough battery energy to perform additional complete cycles... The transformation of the Tucson Proving Ground allows Caterpillar to demonstrate our energy transition commitments and serve as a stronger advisor to customers as we navigate the changes together. We know it will take an integrated, site-level solution for miners to achieve their carbon-reduction goals, and we're here to help as they redefine the way they mine for generations to come...

Additional Analysis and Comment

Looking for market mispricing of stocks -

What I'm primarily looking for here are instances of market mispricing of stocks due to distortions to many of the usual statistics used for screening stocks for buy/hold/sell decisions.

I believe the answer is to compare projections, based on analysts' estimates out to the end of 2024 or later, to past performance. Summarized in Tables 1 and 2 below are the results of compiling and analyzing the data on this basis.

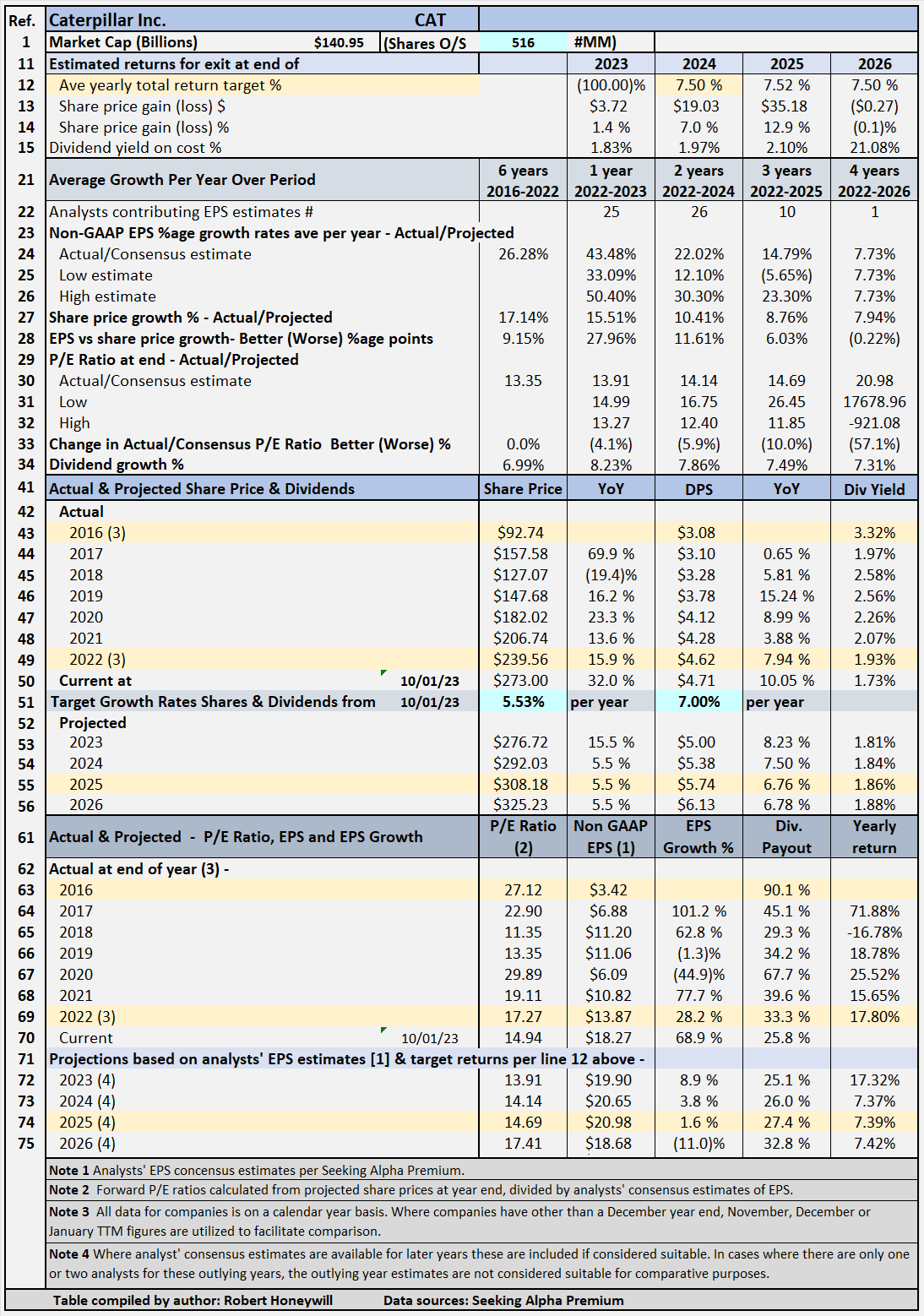

Table 1 - Detailed Financial History And Projections

{kind=link}

Table 1 shows CAT non-GAAP EPS has grown from $3.42 for 2016 to $13.87 for 2022, an average yearly growth rate of 26.3% for the six years 2016 to 2022. Despite this, CAT's stock price grew at a much lower 17.1% per year, from $92.74 at the end of 2016 to $239.56 at the end of 2022. This is primarily due to a decrease in the P/E multiple from 27.12 at the end of 2016 to 17.27 at the end of 2022. The share price growth has been supported by a dividend per share average yearly growth rate of 7% per year from $3.08 at end of 2016 to $4.62 at end of 2022. This dividend growth rate of 7% per year is well below the EPS growth rate of 26.3%, and has resulted in a decrease in the dividend payout ratio from 90% for 2016 to ~20% at end of 2022.

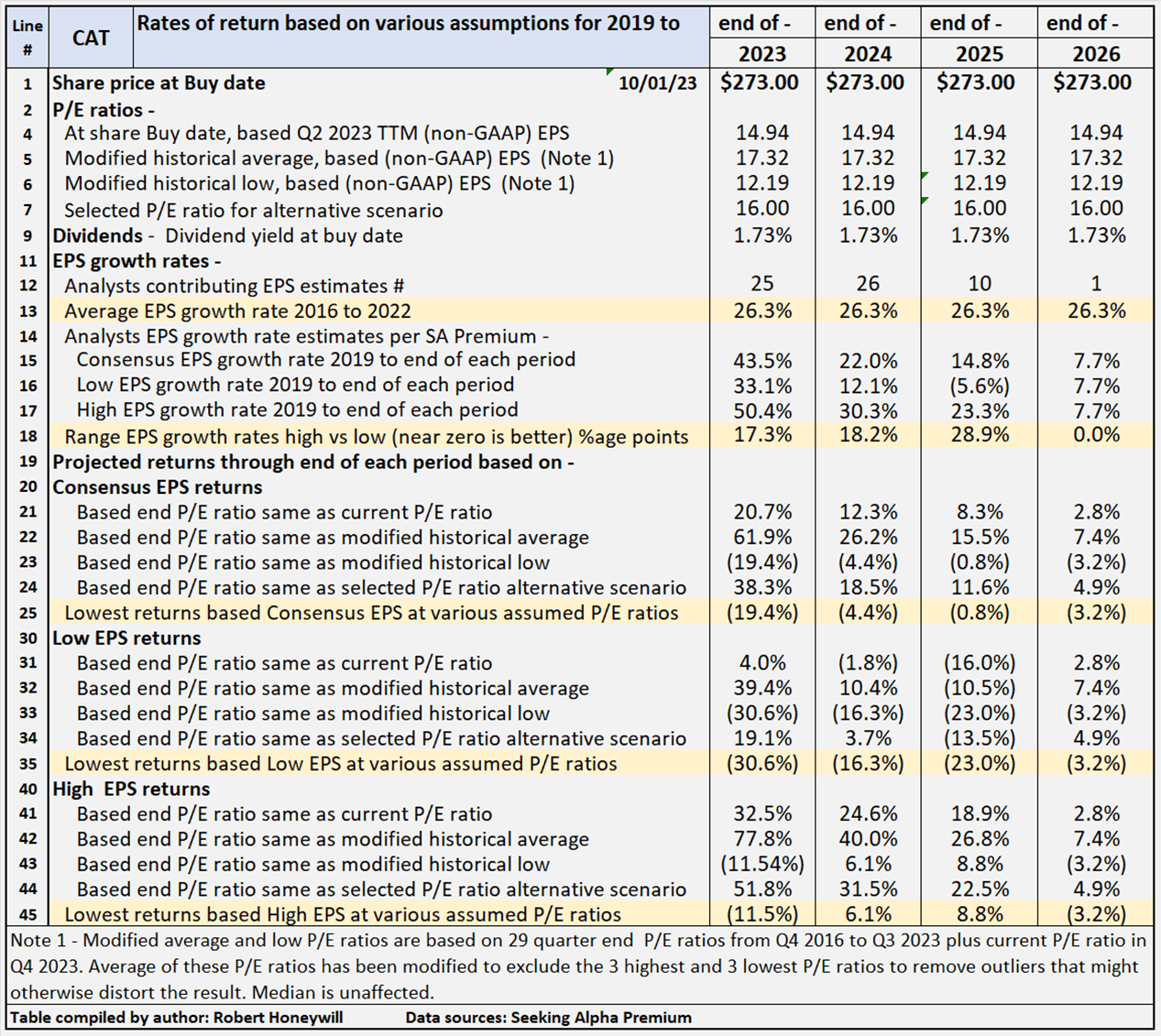

Table 2 below provides scenarios projecting potential returns based on select historical P/E ratios and analysts' consensus, low, and high EPS estimates per Seeking Alpha Premium through the end of 2024.

Table 2 - Summary of relevant projections CAT

{kind=link}

Table 2 provides comparative data for buying at a share price at the beginning of October, 2023 and holding through the end of years 2023 through 2025. There's a total of nine valuation scenarios for each year, comprised of three EPS estimates (SA Premium analysts' consensus, low and high) across three different P/E ratio estimates, based on historical data. Table 2 shows potential returns from an investment in shares of the company at a range of historical and assumed P/E ratio levels. This analysis, from hereon, assumes an investor buying CAT shares today would be prepared to hold through the end of 2024, if necessary, to achieve their return objectives. Comments on contents of Table 2, for the period to 2024 column follow.

Consensus, low, and high EPS estimates

All EPS estimates are based on analysts' consensus, low and high estimates per SA Premium. This is designed to provide a range of valuation estimates ranging from low to most likely, to high based on analysts' assessments. I could generate my own estimates, but these would likely fall within the same range and would not add to the value of the exercise. This is particularly so in respect of well-established businesses such as CAT. I believe the "low" estimates should be considered important. It's prudent to manage risk by knowing the potential worst-case scenarios from whatever cause.

Alternative P/E ratios utilized in scenarios

- The actual P/E ratios at share buy date based on actual non-GAAP EPS for TTM Q2-2023.

- A modified average P/E ratio of 17.32 based on 29 quarter-end P/E ratios from Q4 2016 to Q3 2023 plus current P/E ratio at beginning of Q4-2023. The average of these P/E ratios has been modified to exclude the three highest and three lowest P/E ratios to remove outliers that might otherwise distort the result.

- A modified low average P/E ratio of 12.19 based on 29 quarter-end P/E ratios from Q4 2016 to Q3 2023 plus current P/E ratio at beginning of Q4-2023. The average of these P/E ratios has been modified to exclude the three highest and three lowest P/E ratios to remove outliers that might otherwise distort the result.

- A median P/E ratio is calculated using the same data set used for calculating the modified average P/E ratio. Of course, the median is the same whether or not the three highest and lowest P/E ratios are excluded. In the case of CAT I have chosen to use an assumed P/E ratio of 16.0 in place of the historical median of 17.27 (similar to the average). I have done this to provide an idea of the impact on returns of the multiple settling between the present level and the historical average. The selected P/E multiple of 16.0 is also below the sector median per Fig. 1 above.

Reliability of EPS estimates (line 18)

Line 18 shows the range between high and low EPS estimates. The wider the range, the greater disagreement there is between the most optimistic and the most pessimistic analysts, which tends to suggest greater uncertainty in the estimates. There are 26 analysts covering CAT through the end of 2024. In my experience, a range of 18.2 percentage points difference in EPS growth estimates among analysts is high, suggesting a degree of uncertainty, and thus lesser reliability of the estimates.

Projected returns (lines 19 to 45)

Lines 25, 35 and 45 show, at a range of historical P/E ratio levels, CAT is conservatively indicated to show returns between negative (16.3)% and positive 6.1% average per year through the end of 2024. The negative (16.3)% return is based on analysts' low EPS estimates and the positive 6.1% on their high EPS estimates, with a (4.4)% negative return based on consensus estimates. Those are the lowest of the returns under the consensus, low and high EPS scenarios, and assume a P/E ratio of 12.19 in 2024. At the high end of the projected returns for CAT, the indicative returns range from 10.4% to 40.0%, with consensus 26.2%. These returns assume a P/E ratio of 17.12 in 2024, based on the current P/E ratio of 14.94 increasing to 16.0 by end of 2024, around halfway between the current P/E multiple of 14.94 and the historical average of 17.12.

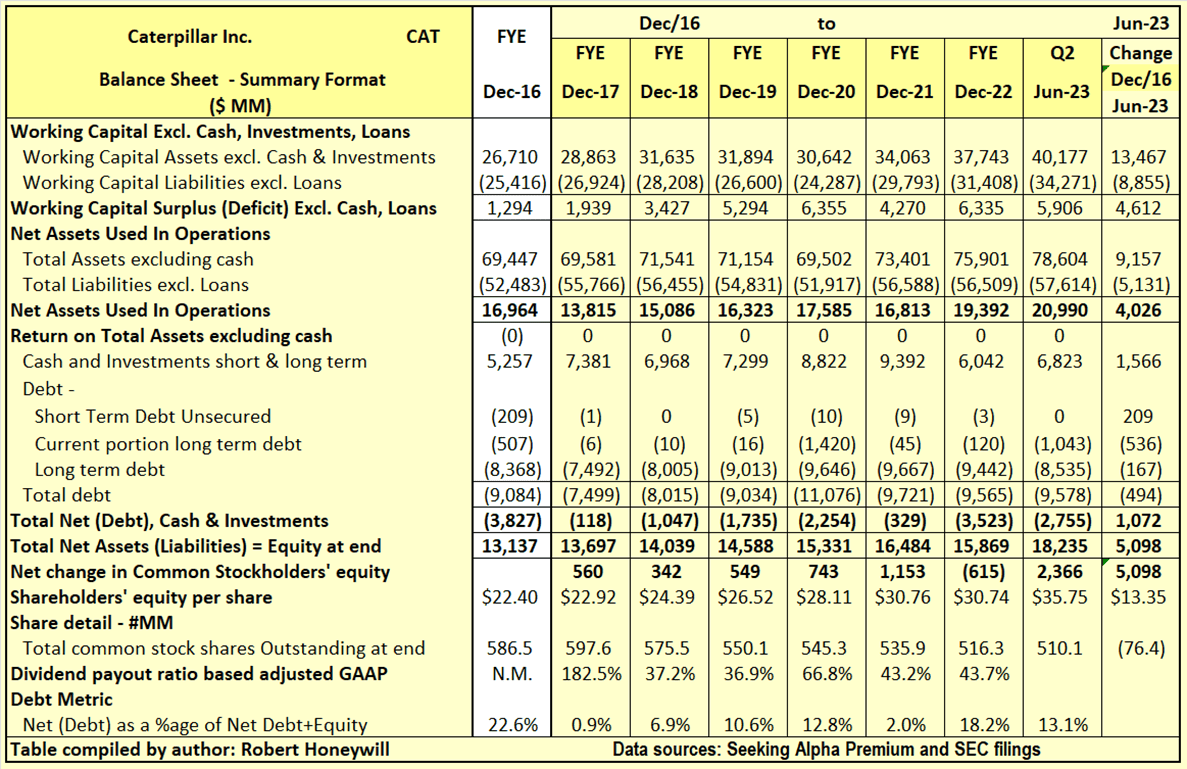

Checking CAT's "Equity Bucket"

Table 3.1 Caterpillar Balance Sheet - Summary Format

Seeking Alpha Premium and SEC filings

{kind=link}

Over the 6.5 years from the end of 2016 through the end of Q2-2023, CAT has increased shareholders' equity by $5,098 million. This increase in equity was used to increase Net Assets Used In Operations by $4,026 million, and reduce debt net of cash by $1,072 million. Net debt as a percentage of net debt plus equity decreased from 22.6% at end of 2016 to 13.1% at end of Q2-2023, due to the use of increased equity to increase investment in the business and reduce net debt. Outstanding shares decreased by 76.4 million from 586.5 million to 510.1 million, due to share repurchases offset in part by share issues for employee compensation. The $5,098 million increase in shareholders' equity over the last 6.5 years is analyzed in Table 3.2 below.

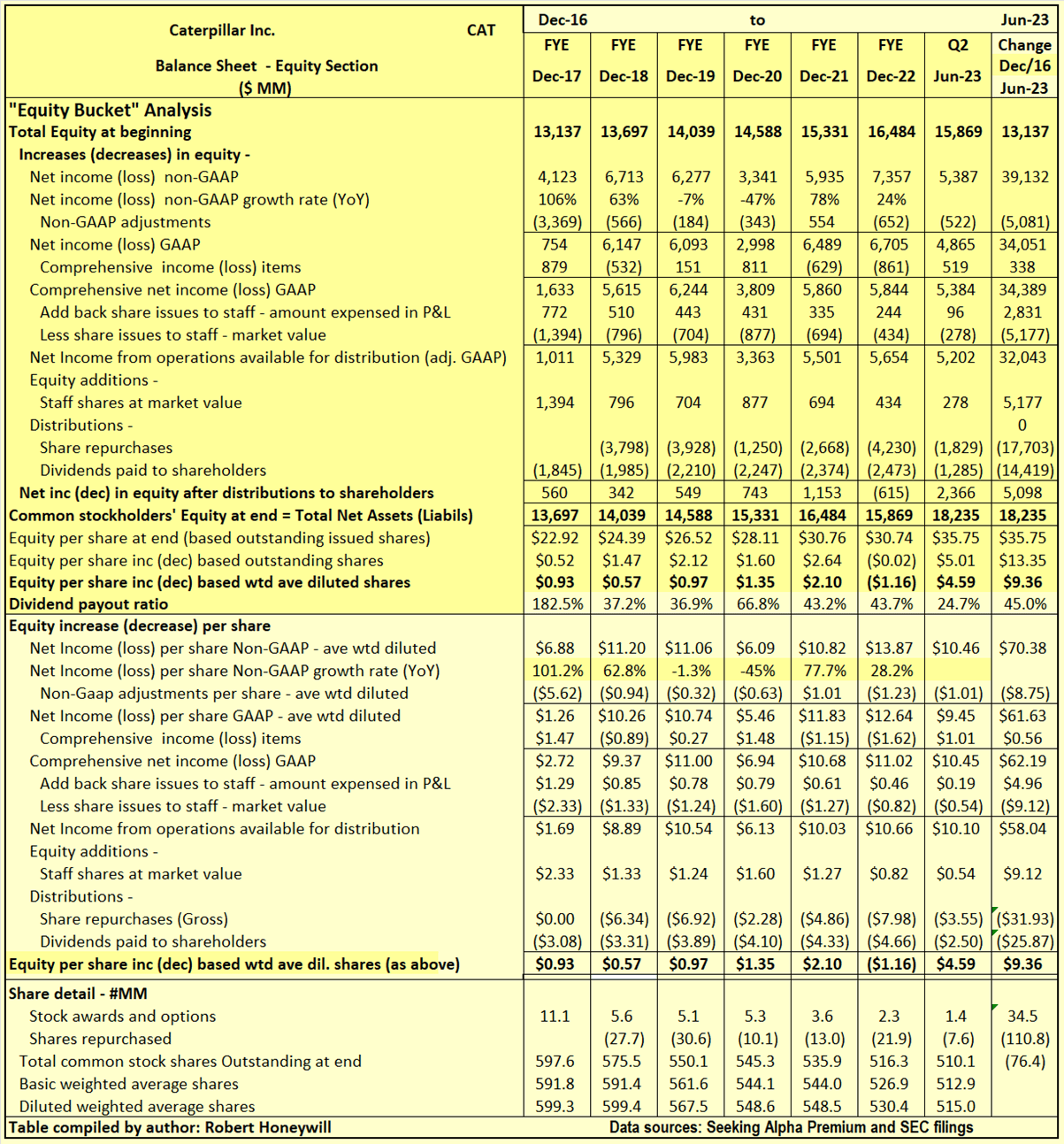

Table 3.2 Caterpillar Balance Sheet - Equity Section

Seeking Alpha Premium and SEC filings

{kind=link}

I often find companies report earnings that should flow into and increase shareholders' equity. But often the increase in shareholders' equity does not materialize. Also, there can be distributions out of equity that do not benefit shareholders. Hence, the term "leaky equity bucket." This is happening to some extent with CAT in relation to share compensation.

Explanatory comments on Table 4.2 for the period end FY-2016 to end Q3-2022

- Reported net income (non-GAAP) over the 6.5-year period totals to $39,132 million, equivalent to diluted net income per share of $70.38.

- Taking into account non-GAAP adjustments, GAAP net income over the 6.5 years is $5,081 million lower (EPS lower by $8.75) at $34,051 million.

- Other comprehensive income is positive at $338 million (EPS effect $0.56).

- Amount taken up in equity to account for 34.5 million shares issued to staff over the 6.5 years is $2,831 million. This compares to an estimated market value of $5,177 million at the time of issue of these shares. The effect is a reduction of $2,346 million (EPS effect $4.16) compared to reported net income. This is greater than 5% of reported GAAP and non-GAAP net income over the period, and thus is a material difference.

- Taking the above-mentioned items into account, we find, over the 6.5-year period, the reported non-GAAP EPS of $70.38 ($39,132 million) is reduced to $58.04 ($32,043 million), added to funds from operations available for distribution to shareholders.

- Dividends of $14,419 million were adequately covered by this $32,043 million generated from operations, resulting in a net increase of $17,624 million in equity.

- This net $17,624 million increase in equity from operations, together with the $5,177 million capital raised through share issues to staff, enabled repurchase of 110.8 million shares at a cost of $17,703 million. This left a net increase in shareholders' funds of $5,098 million per Table 3.1 above.

Summary and Conclusions

The level of gains earned by longer-term shareholders of CAT over the last several years have been limited by multiple contraction offsetting the impact of strong EPS growth. The current multiple is below the long-term average and some multiple expansion could contribute to strong share price through end of 2024. The prospect of share price growth is dimmed to some extent by fairly flat growth reflected in SA Premium analysts' consensus EPS estimates. The consensus EPS estimates are apparently being dragged down by a significant number of analysts projecting low or negative EPS growth rates beyond the end of 2023. This seems counter-intuitive given the aggressive steps CAT is taking to be an integral part of the decarbonization efforts of the mining industry, and other industries utilizing CAT equipment. These are industries undergoing massive transformation in the way they manage and operate major equipment, of the likes supplied by CAT. It is hard to see how this will not benefit CAT and its top and bottom lines. I believe it is reasonable to discount to some extent the analysts' low EPS estimates, as reflected in Tables above. On that basis, at a relatively conservative forward P/E ratio of 16.0, strong double-digit returns are indicated as a likely outcome from buying at the current price and holding through end of 2024. Also, CAT's strong cash flow generation should easily allow for increasing dividends at least at the historical growth rate of 7% average per year. The balance sheet analysis above indicates considerable strength with low debt levels, allowing CAT to continue to invest in facilities to support its customers in their decarbonization efforts, with flow on benefits to CAT. CAT is rated a Strong Buy.

For further details see:

Caterpillar: Making Itself Indispensable To Its Customers