SIX - Cedar Fair: Still A FUN Way To Make Money

Summary

- Cedar Fair has done really well from a fundamental perspective lately, with sales and profits rising in response to robust results at its theme parks.

- Even so, the company has not quite kept up with the market and it is severely discounted compared to similar firms.

- Long term, the business should do well and it should be an appealing opportunity for investors to consider.

These days, the number of companies that own and operate theme parks is fairly small. And when looking at companies that specialize almost entirely in that space, the opportunities become even smaller. One company that does operate in this space though that offers some nice upside potential from here is Cedar Fair ( FUN ), a theme park operator that owns 13 different properties, including water parks and resort facilities, as well as other complementary assets. Recently, shares have risen some as the business reports robust financial performance. But I would make the case that further upside is likely warranted from here.

Making money with FUN

In early October of 2022, I wrote an article discussing whether it made sense for investors to consider a stake in Cedar Fair. In that article, I stressed that the company continues to do well from a fundamental perspective. Even so, shares were experiencing some downside pressure, likely because of concerns over the economy more broadly. This was odd because, for the most part, the firm's recovery from the COVID-19 pandemic was looking more or less complete, with spending at or near all-time highs and attendance close to where it was prior to the pandemic. Add on top of this how cheap shares were, and I felt very comfortable at that time rating the business a 'buy' to reflect my view that shares should generate performance that would exceed with the broader market could experience over that same window of time. Since then, the firm has risen, climbing by 5.1%. But to be fair, that is slightly worse than the 5.3% the general market has seen as measured by the S&P 500.

{kind=link}

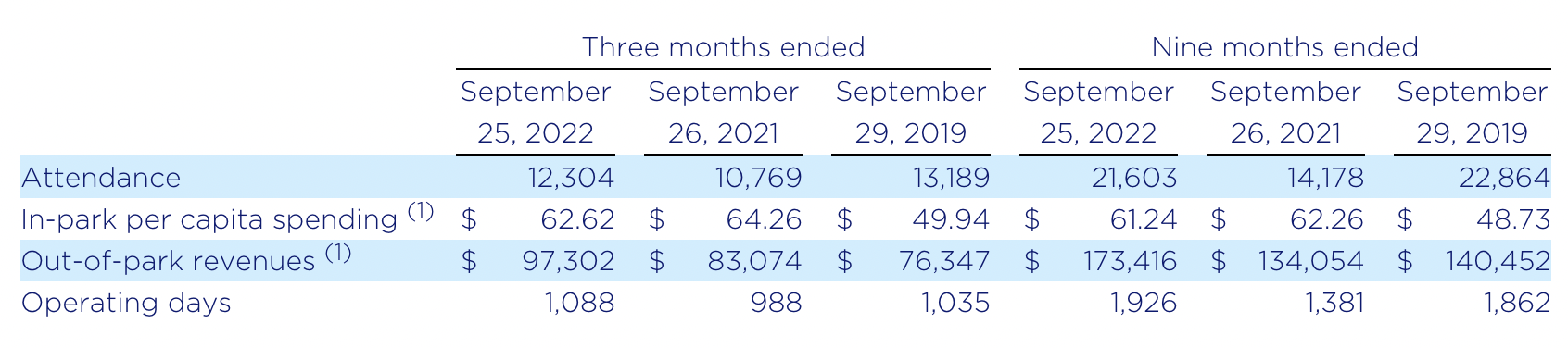

This share price appreciation has been driven largely by robust fundamental performance. To see what I mean, we need only look at data covering the third quarter of the company's 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about the business. For that quarter, sales came in at $843.1 million. That's 11.9% higher than the $753.4 million generated only one year earlier. Interestingly, this increase came at a time when in-park per capita spending actually dropped, falling from $64.26 to $62.62. The real driver then was a rise in attendance, with the number of people during the quarter totaling 12.30 million compared to the 10.77 million reported one year earlier.

{kind=link}

Given that many of the company's costs are fixed, it should come as no surprise that profitability would improve nicely as attendance or pricing increases. Net income in the third quarter totaled $333 million. That's more than double the $148 million generated the same time one year earlier. Although this was great to see, not every profitability metric was positive. Operating cash flow actually worsened year over year, dropping from $283.1 million in the third quarter of 2021 to $266.1 million the same time of 2022. Though if we adjust for changes in working capital, it would have increased modestly from $255.9 million to $257.4 million. Also on the rise was EBITDA, with the metric increasing from $333.4 million to $362 million.

{kind=link}

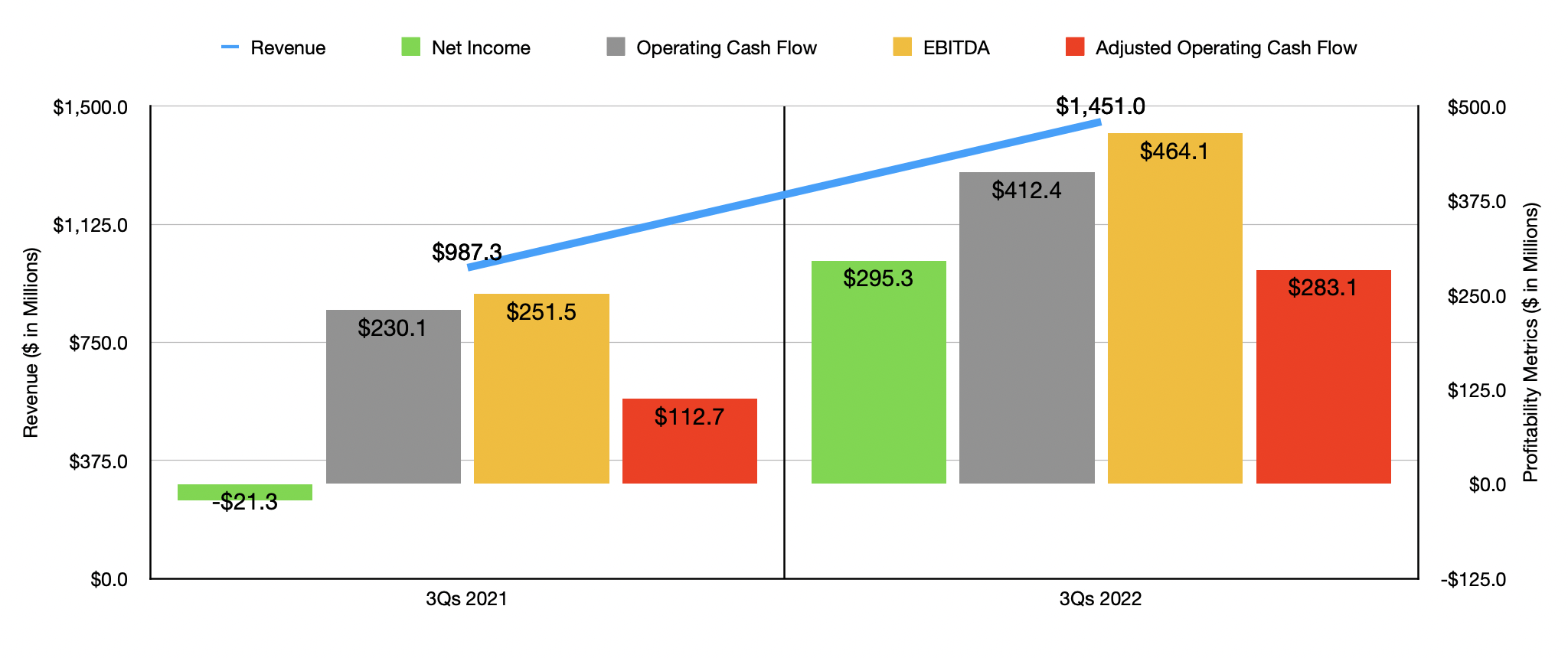

To be very clear, the third quarter of 2022 was not the only positive quarter for the enterprise. For the first nine months of the fiscal year, sales of $1.45 billion dwarfed the $987.3 million reported one year earlier. A surge in attendance from 14.18 million to 21.60 million more than offset a decline in in-park per capita spending from $62.26 to $61.24. The rise in revenue naturally brought with it improved profitability as well. The company went from generating a net loss of $21.3 million to generating a profit of $295.3 million. Operating cash flow jumped from $230.1 million to $412.4 million, while the adjusted figure for this more than doubled from $112.7 million to $283.1 million. Also rising nicely was EBITDA. Year over year, that metric grew from $251.5 million to $464.1 million.

In the absence of real guidance from management, I simply decided to annualize results experienced so far for the 2022 fiscal year. Assuming that current trends hold, the company should generate adjusted operating cash flow of $393.1 million. This should translate to EBITDA of somewhere around $599 million. Using these numbers, the company is trading at a forward price to adjusted operating cash flow multiple of 5.9. By comparison, the number using data from 2021 when the firm was still recovering from the pandemic is 14.8. The forward EV to EBITDA multiple for the company, meanwhile, should be around 7.2. That stacks up favorably against the 13.3 reading that we get using data from the year before.

{kind=link}

As part of my analysis, I decided to compare Cedar Fair to the two other firms that represent comparable pure-play theme park operators. These would be Six Flags Entertainment ( SIX ) and SeaWorld Entertainment ( SEAS ). On a price to operating cash flow basis, these companies are trading at multiples of 8.9 and 7.1, respectively. Using, instead, the EV to EBITDA approach, these multiples would be 10.6 and 8.3, respectively. In both scenarios, Cedar Fair was the cheapest of the group, though not by a great deal. If we were to assume that the company would warrant upside to bring its trading multiple in line with the cheaper of its two peers, then that would imply upside potential of 20.3% using the price to operating cash flow approach. Using, instead, the EV to EBITDA approach, that upside would be 28.1%.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Cedar Fair |

| 5.9 |

| 7.2 |

| Six Flags Entertainment |

| 8.9 |

| 10.6 |

| SeaWorld Entertainment |

| 7.1 |

| 8.3 |

Takeaway

Based on the data provided, I must say that I continue to be impressed by Cedar Fair from a fundamental perspective. Although the company has not performed exactly as I would have anticipated, robust sales, profits, and cash flows have helped to push the stock up on an absolute basis. So long as fundamental performance does not worsen from here, shares do also look cheap on an absolute basis and relative to similar firms. Because of these factors, I do still think it makes sense to consider the company a 'buy' at this time.

For further details see:

Cedar Fair: Still A FUN Way To Make Money