CA - Centerra Gold: Oksut Delivers Above Plan In Q3

2023-11-02 13:21:15 ET

Summary

- Centerra had a monster quarter out of Oksut in Q3, but this was partially overshadowed by continued short-term challenges at Mount Milligan.

- Meanwhile, the company continued to return significant capital to shareholders, and has further room on its buyback program to continue retiring shares opportunistically.

- In this update, we'll dig into the Q3 results and if the stock is worthy of investment after a strong Q3 report.

Just over six weeks ago, I wrote on Centerra Gold ( CGAU ), noting that the stock wasn't offering enough of a margin of safety yet at US$5.10, and that the stock would need to decline to US$4.50 or lower to become attractive. Since pulling back to this low-risk buy zone, Centerra has rallied over 17%, helped by a solid Q3 report with significantly higher production, revenue, and free cash flow following the return to full production at its Oksut Mine in Turkiye. In addition, the company ramped up its share repurchases at attractive levels, buying back an additional ~$11.0 million worth of stock (1.5% of its share count year-to-date), while paying an industry-leading dividend yield. In this update, we'll dig into the Q3 results and if the stock is worthy of investment after a strong Q3 report.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

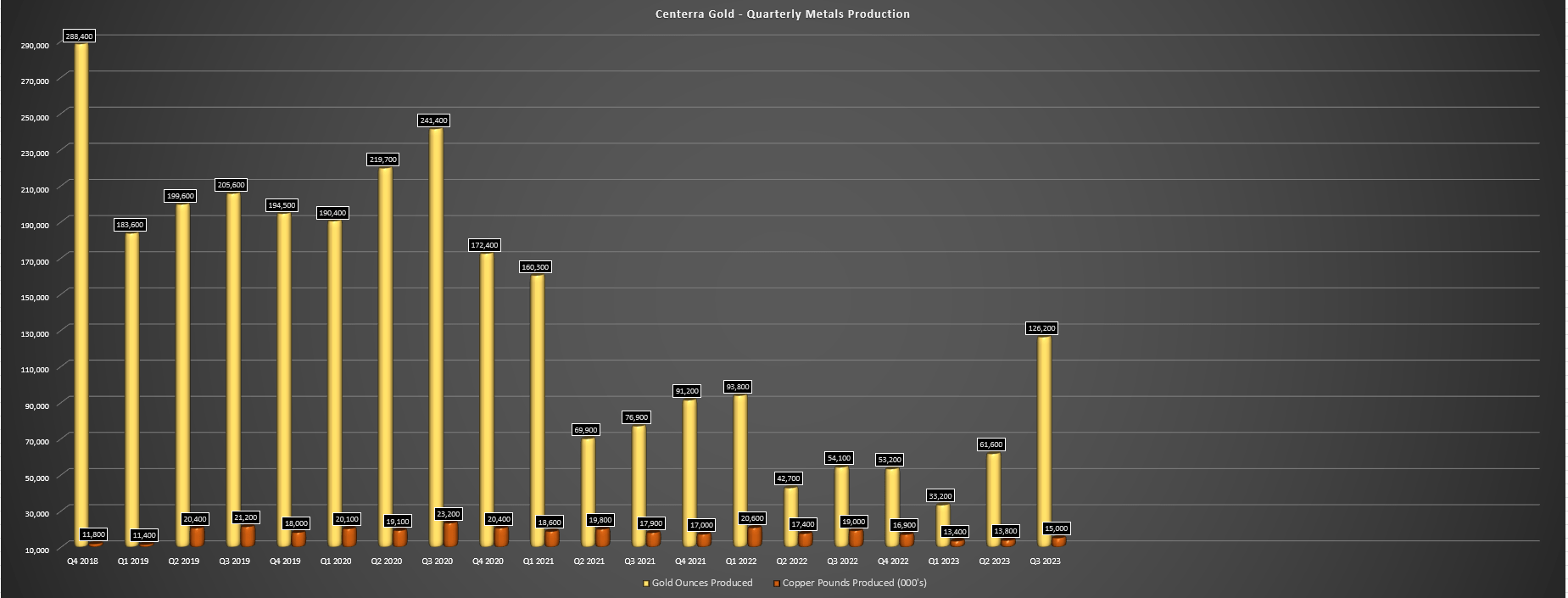

Centerra Gold ("Centerra") released its Q3 results this week, reporting quarterly production of ~126,200 ounces of gold and ~15,000 pounds of copper, translating to a 133% increase in gold production from the year-ago period. This was largely because of being up against easy year-over-year comparisons with no contribution from its Oksut Mine in Q1 2022 (suspension of gold room operations at ADR plant because of mercury being detected), and this was offset by a softer quarter from Mount Milligan which continues to work through mining the rest of the ore-waste transition zone in Phase 9 of the mine plan and the lower recoveries from blending Phase 7 (high-grade gold and low grade copper) and Phase 9 material (low grade gold and low grade copper). This negatively impacted recoveries once again in the quarter at the British Columbia Mine (elevated ratio of pyrite to chalcopyrite), translating to a softer quarter with gold production down 27% vs. Q3 2022 and copper production down over 20%.

Centerra - Consolidated Gold & Copper Production - Company Filings, Author's Chart

{kind=link}

Digging into operations at Mount Milligan a little closer, Centerra processed ~5.61 million tonnes at 0.35 grams per tonne of gold and 0.17% copper, which was significantly lower than the 0.47 grams per tonne of gold and 0.20% copper in the year-ago period. This was related to mine sequencing with a longer time spent in the ore-transition zone than anticipated, and with Centerra noting in its Q2 results that it was mostly out of the ore-waste transition zone and that this would result in an improved production profile in H2. Given that recoveries were affected in the period yet again (63.7% gold recovery and 76.5% copper recovery) and lower grades were processed, Centerra was forced to revise guidance lower to 155,000 ounces at the mid-point vs. 165,000 ounces previously, and costs soared year-over-year to $1,150/oz related to labor and consumables inflation, higher sustaining capital, fewer ounces of gold sold, and lower by-product credits.

"At Mount Milligan, we sequenced out of the ore-waste transition zone of the mine and are on track to access higher grade copper and gold ore in the second half of the year, which should help to bolster the production profile going forward.”

- Q2 2023 Results, Company Filings

Unfortunately, Centerra shared that while it is trying to be conservative, it expects to see a continuation of the lower recoveries for gold and copper on a medium-term basis, but that it's looking at ways to increase recoveries from these much less favorable levels (Q3 recoveries were down 250 basis points on gold and 1600 basis points on copper on a year-over-year basis, and 6% and 7% year-to-date, respectively). However, while this continued headwind puts a damper on Q4 and Q1 expectations for Mount Milligan, the asset still generated positive operating cash flow, benefiting from a higher gold and copper price. And while it's been a tough year at the asset, the mine has still generated positive free cash flow this year and the company has begun a full asset optimization review to work on delivering improvements to operations.

{kind=link}

Fortunately, while Mount Milligan saw lower production, Oksut easily picked up the slack, producing ~86,700 ounces of gold and contributing to gold sales of 88,100 ounces at industry-leading costs of $582/oz. This significant increase in production was related to the restart of operations with the build-up of gold-in-carbon inventory vs. no gold production in the year-ago period (temporary suspension of processing until mercury abatement system commissioned and EIA reinstated). In fact, Centerra noted the mine exceeded its expectations during the ramp-up to full production. During the quarter, Centerra stacked ~978,000 tonnes at 1.98 grams per tonne of gold (Q3 2022: ~1.02 million tonnes at 1.96 grams per tonne of gold). And given the impressive quarter, Centerra announced an increase in guidance to 195,000 ounces at the mid-point, offsetting the 10,000 ounce drop in guidance at Mount Milligan.

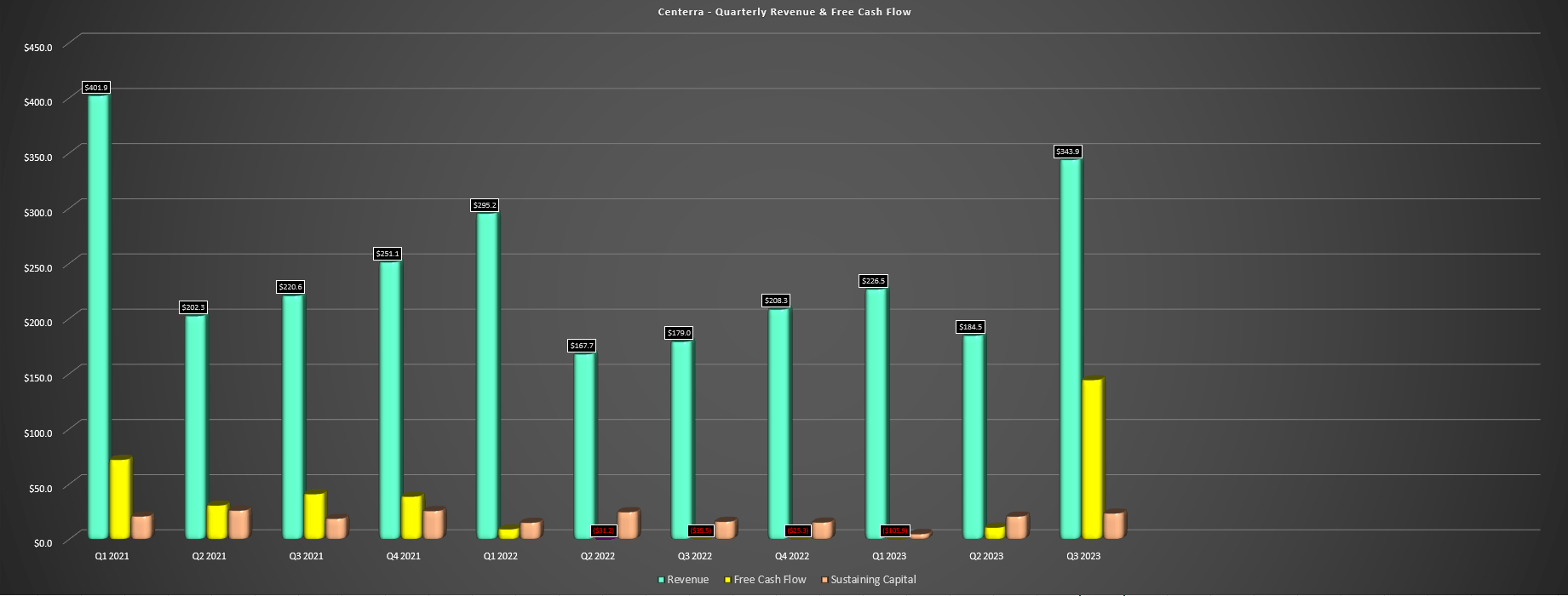

Centerra - Quarterly Revenue, Sustaining Capital & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Given the significantly higher gold production and sales combined with higher gold and molybdenum prices (~2.7 million pounds sold at $24.08/lb at its MBU), Centerra had its best quarter in years from a revenue standpoint (since Kumtor nationalization), reporting sales of $343.9 million and operating cash flow of $166.6 million. And with what should be a better year at Mount Milligan and a full year of production from Oksut (210,000+ ounces) in FY2024, we should see another strong year for the company on deck, especially if Centerra can get its metallurgical challenges at Mount Milligan sorted out early in 2024. And with ~$490 million in cash (~$140 million in free cash flow generated in Q3), $25 million due in December from Orion Mine Finance (deferred payments for Greenstone purchase) and ~$900 million in liquidity, Centerra is certainly in a favorable position if it were to choose to take advantage of the depressed valuations to add another development/producing asset.

Besides $25 million payable by year-end by Orion, Centerra will also receive:

1. ~11,111 ounces of refined gold (or the cash equivalent) or a combination of refined gold and a cash equivalent of the shortfall ounces within 30 days of 250,000 cumulative ounces being produced at Greenstone

2. 11,111 ounces of refined gold (or the cash equivalent) or a combination of refined gold and a cash equivalent of the shortfall ounces within 30 days of 500,000 cumulative ounces being produced at Greenstone

3. 11,111 ounces of refined gold (or the cash equivalent) or a combination of refined gold and a cash equivalent of the shortfall ounces within 30 days of 700,000 cumulative ounces being produced at Greenstone

Costs & Margins

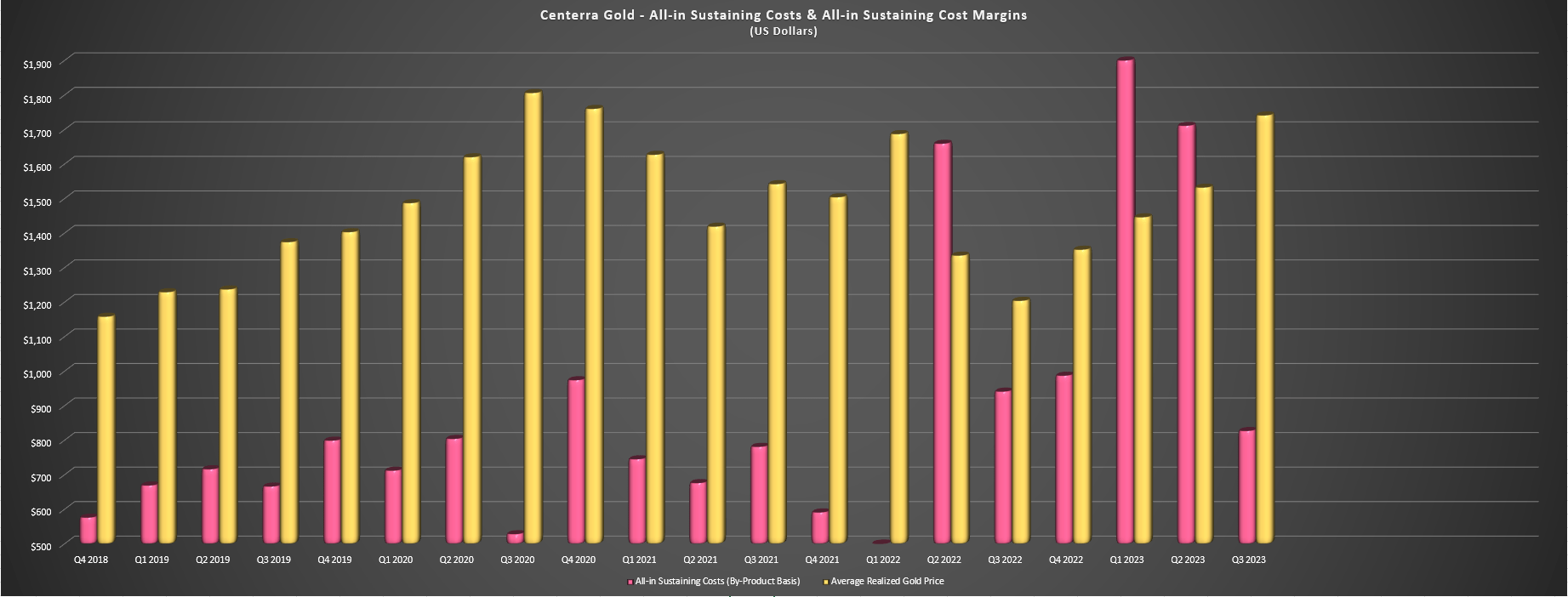

Moving over to costs and margins, Mount Milligan's costs increased sharply in Q3 as noted earlier (fewer copper pounds sold, fewer gold ounces sold, general inflation and 20% higher sustaining capital), with all-in sustaining costs coming in at $1,150/oz (+87% year-over-year). This resulted in the asset reporting AISC margins of $210/oz (Q3 2022: $589/oz) despite the higher gold price and has resulted in a significant decline in free cash flow generation year-to-date. However, as noted, the restart at Oksut more than offset the weaker performance at its flagship asset, with Centerra's consolidated AISC coming in at $827/oz on a by-product basis, down 12% year-over-year. The result? Industry-leading AISC margins of $914/oz, a material improvement from $263/oz with a lower average realized gold price (only contribution coming from an asset with gold stream impact), and a lower commodity price in general.

Centerra Gold - AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

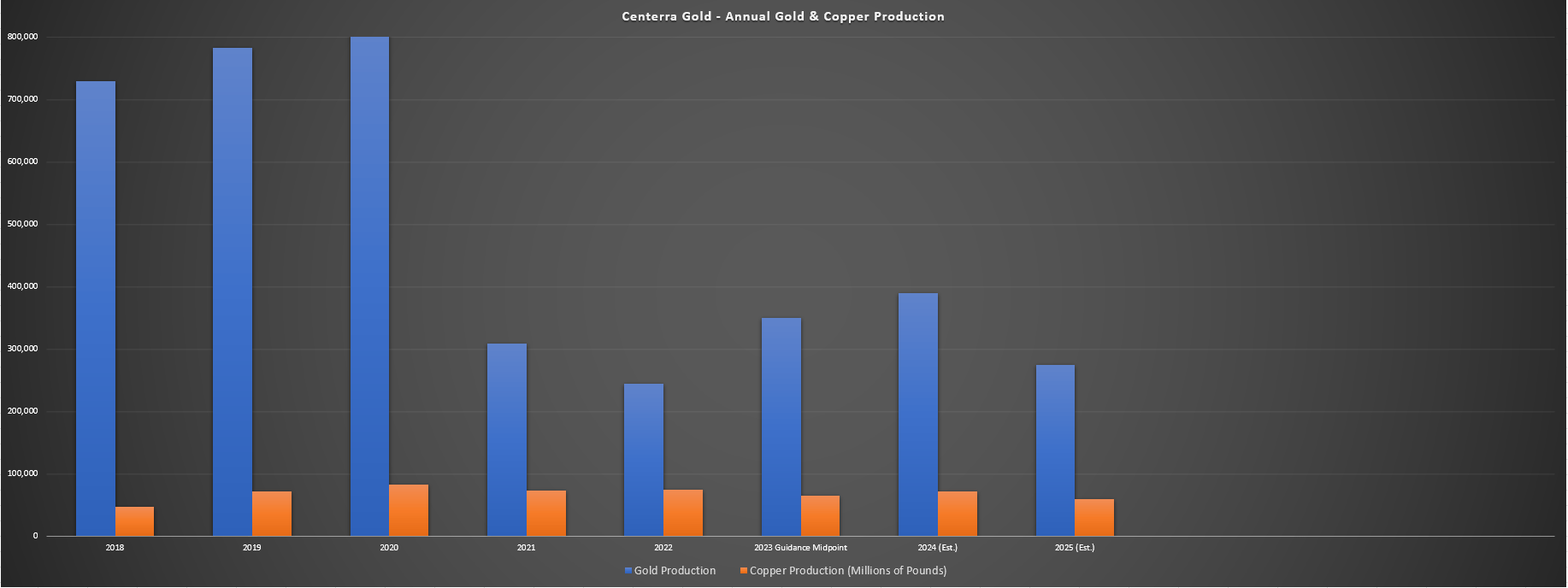

Based on the solid performance in Q3 from Oksut, Centerra has maintained its FY2023 AISC guidance of $1,025/oz at the mid-point, which would make Centerra one of the top-12 lowest cost gold producers this year among the 60+ producers I track (assuming it can come in within its guidance range). That said, the unfortunate part about Centerra Gold is that its cash cow Oksut is expected to see a production cliff in 2025, with output set to decline by over 40% from ~210,000 ounces in FY2024 to barely 135,000 ounces in 2025 and just ~120,000 ounces in 2026. Meanwhile, production is expected to wind down by early 2029, meaning that the company will have to either bring Goldfield online, look at restarting its Thompson Creek Mine, or look at M&A to maintain its gold-equivalent ounce production profile and attractive margin profile post-2025. And given that I'm not sure a restart at Thompson Creek will help the stock's multiple and the fact that we'll see a meaningful increase in costs plus sharply declining production post-2025 without M&A, I'm less inclined to chase the stock above US$5.65 even if it is very reasonably valued.

Centerra - Annual Gold/Copper Production & Forward Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

{kind=link}

Summary

Centerra had an exceptional quarter at Oksut after a return to normal operations even if this was offset by another challenging quarter at Mount Milligan, this looks largely priced into the stock at a market cap of ~$1.25 billion. Plus, Centerra continues to be more active on its buyback program than most of its peers and has additional room to continue opportunistically buying back its shares. And while 2023 has been a solid year, 2024 should be even better with a full year of production out of Oksut and hopefully a return to more normal recoveries by Q2 2024 at Mount Milligan. That said, while Centerra is cheap, it's in the uniquely negative position of seeing peak production next year with no clear way to plug this gap outside of molybdenum which could translate to a lower multiple for the stock or Goldfield, but which could take until 2028 to bring online.

Based on what I believe to be a fair value of US$7.60 and a required 40% discount to fair value, Centerra's ideal buy zone comes in at US$4.60 or lower, suggesting that the stock is well outside of its low-risk buy zone after its recent rally. And while the stock could continue to rally, I see far more attractive bets elsewhere in the sector. To summarize, I think Centerra is more of a trading vehicle until there's a concrete way to smooth out the production cliff, and I see restarting Thompson Creek as a less appealing option with volatile molybdenum prices and the potential for multiple compression as base metals names typically trade at lower multiples than gold-focused names. Therefore, I would view any rallies above US$6.12 before year-end as profit-taking opportunities.

For further details see:

Centerra Gold: Oksut Delivers Above Plan In Q3