CRNC - Cerence: Fade The Ambitious New Mid-Term Targets

Summary

- Cerence latest FY23 guidance update falls short of expectations.

- The mid-term growth outlook is compelling, but rests on unproven new markets.

- With the stock still fairly pricey for a loss-making tech name, I see more risk than reward here.

Cerence ( CRNC ), which primarily operates in the in-car voice-enabled digital assistant space, has come a long way since it was spun out from Nuance (NUAN) in 2019. As highlighted at its investor day , the company is bullish on the mid-term, setting an ~26% YoY price per unit ((PPU)) growth target through FY24. Management also sees ample addressable market opportunities beyond autos in transportation and non-transportation adjacencies. It's hard to fault ambition, but a governance overhang is warranted following a string of management departures (CEO, CFO, and General Counsel) in recent months. Given the previously issued FY24 financial guidance had also been withdrawn on account of the previous management setting unrealistic targets, I am hesitant to underwrite the updated numbers at this juncture. In the meantime, CRNC remains on track for more GAAP losses heading into FY23 and bears an elevated debt load (thanks to the debt-funded dividend paid to NUAN post-spinoff). At >3x fwd EV/Revenue, I see more risk than reward here.

FY23 Guidance Update Falls Short

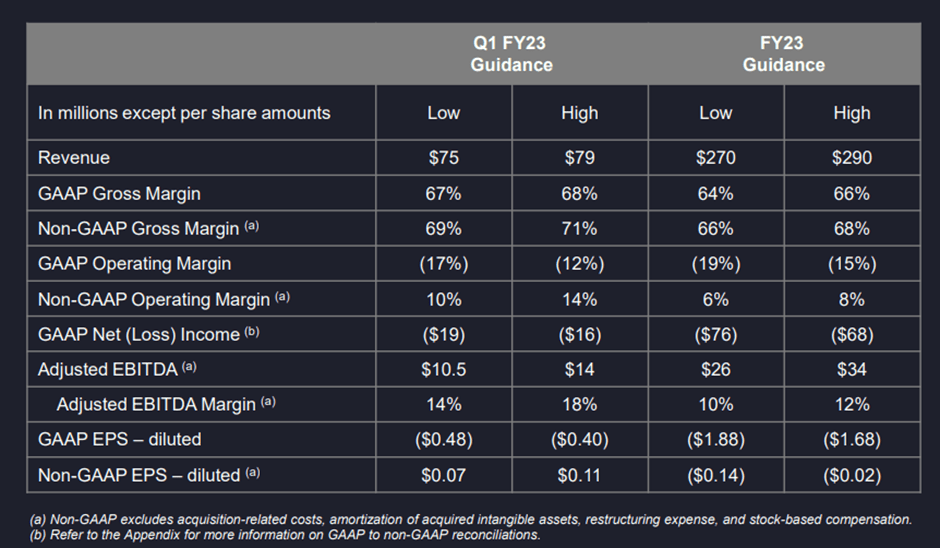

While CRNC's Q1 2023 guidance range came in ahead of consensus on the top and bottom lines, the FY23 guide missed across the board. To recap, the company has guided to a revenue range of $270m to $290m for the year (implying a 12-18% YoY decline) based on global production running ~3% below IHS estimates. FY23 adj EBITDA (excluding stock-based compensation) guidance also disappointed at $26m to $34m, while operating EPS (excluding stock-based compensation) is guided to be in the red within a -$0.02 to -$0.14 range.

{kind=link}

The key driver of the FY23 disappointment was a shift in the company's contract policy - per management, no fixed contracts will be signed from Q4 2022 onwards, as it looks to cap the annual fixed contract contribution within a ~$40m/year range. While this policy does help address license inventory issues, it will create a near-term P&L headwind, as CRNC only sees a kick-start in growth from FY24. Yet, the potential to build a more predictable income stream over the mid to long run is appealing. Execution will be key here; in particular, the company's progress toward balancing the proportion of sell-in and consumption of fixed contracts (targeted to be equal by FY25) will be worth monitoring.

Capitalizing on New and Existing Addressable Market Opportunities

Over the mid-to-long term, the CRNC story primarily rests on its exposure to the secular growth in software content in vehicles, including 'connected cars' and AI-related in-cabin applications. Building on its leadership in in-car voice-enabled digital assistants, management has defined an ambitious new 'Destination Next' strategy, outlining the path from Cerence Voice and Assistant to more advanced features like Cerence Co-Pilot and Cerence Companion. The ambition is commendable, but given these solutions represent a significant step forward from current conversational AI technology, the execution could be challenging, particularly with new CEO Ortmanns barely one year into the role.

{kind=link}

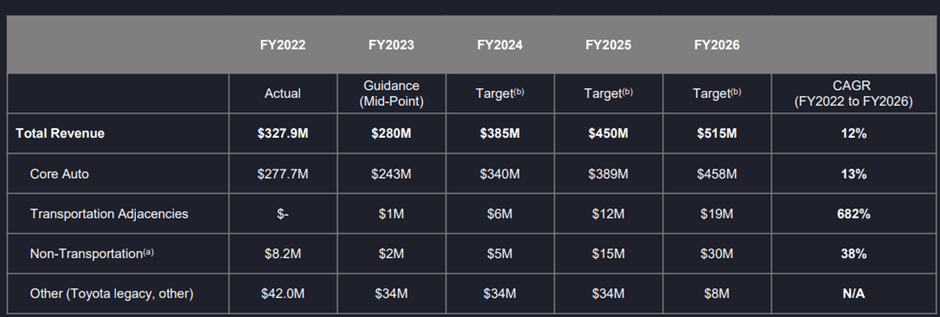

While the core auto segment still makes up the vast majority of the CNRC revenue base, the company sees opportunities to expand organically into transportation and non-transportation adjacencies. On the transport side, this includes two-wheelers, trucks, and RVs, while non-transportation is mainly licensing-related. The growth targets seem a tad ambitious, though. Not only do they rely on contributions from undeveloped products like Cerence Co-Pilot and Cerence Companion, but the triple-digit % CAGR target (albeit off a low base) for the transportation adjacency seems like too high a bar. The 38% CAGR non-transportation revenue is perhaps more realistic, though any licensing opportunities will depend on field of use restrictions with former parentco NUAN being freed up after expiry.

{kind=link}

Unveiling the Updated Mid-Term Financial Targets

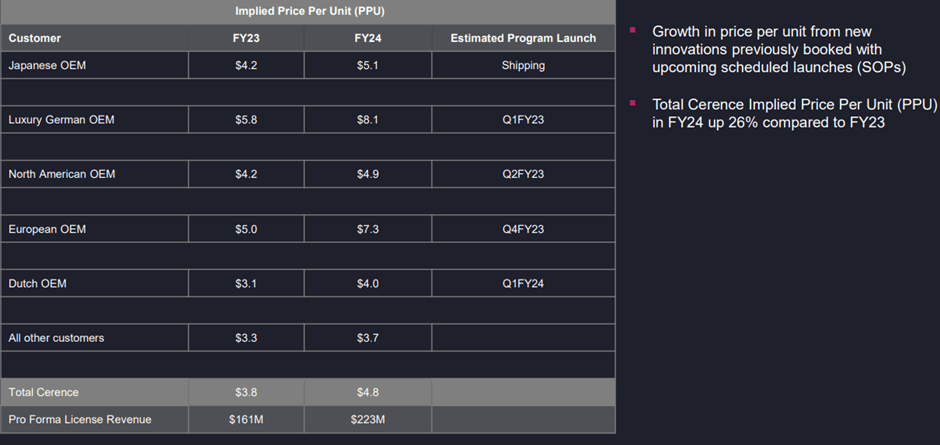

The company also introduced new mid-term financial targets at its investor day, calling for a moderation in PPU or content per vehicle as it moves from Co-Pilot to Companion and introduces these new/updated features. Still, the total implied PPU is guided to be up 26% YoY in FY24, as the company sees the 'Companion' product going live soon. With its backlog already covering ~95% of its FY23 plan and ~75% of its FY24 target, the new PPU growth target is optimistic but not unrealistic, in my view.

{kind=link}

The more conservative approach represents a welcome change from the company's prior track record on the guidance front. Recall that the recent departures of its CEO, CFO, and General Counsel saw the previously issued mid-term financial guidance withdrawn due to unrealistic growth targets. Still, the new mid-term growth outlook rests on new end markets that are largely unproven, and getting there will depend on execution and competition (note tech giants like Google (GOOG) ( GOOGL ) and Microsoft ( MSFT ) have offerings that, to some degree, compete with CRNC).

Fade the Ambitious New Mid-Term Targets

Overall, there was a lot to like from this year's investor event, given the upbeat PPU growth outlook into FY24, as well as the incremental addressable market opportunities beyond the core auto business. Still, it will take time for the new CRNC management team to regain credibility, having been forced to retract the FY24 financial guidance issued in August last year due to the unrealistic growth targets. Getting back on track following the senior management turnover in recent months is also a risk. Pending tangible results from new management, the stock will likely be weighed down by a governance overhang. Over the near-term, key metrics to monitor include CRNC's progress toward regaining GAAP profitability and de-levering the balance sheet.

For further details see:

Cerence: Fade The Ambitious New Mid-Term Targets