CRNC - Cerence: Revolutionizing The Road With AI Assistants

2023-06-22 17:23:12 ET

Summary

- Cerence has both positive and negative aspects, with signs of a turning quarter and future growth potential.

- The stock is not attractively priced, and there is a high level of optimism regarding fiscal 2024 profitability.

- While revenue growth rates are expected to improve, concerns remain about profitability and the decision to raise capital through convertible debt.

- Therefore, I'm neutral on this stock.

Investment Thesis

Cerence Inc. ( CRNC ) has both good and bad aspects. The good element is that the business is evidently turning a quarter and pointing to one more challenging quarter ahead before its growth rates start to improve.

The bad news is that I simply don't find its stock attractively priced. Not only is the stock not particularly cheap. But I also find that there's a lot of hope priced into fiscal 2024 seeing a significant jump in profitability.

And if that's the case, why is Cerence seeking to raise more capital via convertible debt?

The Cerence Story

Cerence Inc. builds virtual assistants for the automobile industry. Their solutions enable conversational interactions between vehicles and drivers. They are a leading provider of AI-powered assistants and innovations for connected and autonomous vehicles, offering a popular software platform for building automotive virtual assistants.

They deliver solutions on a white-label basis, allowing their customers to fully customize the virtual assistants with unique branded personalities. Cerence's platform uses speech recognition, so drivers can interact with virtual assistants.

At its core, Cerence's value proposition is that cars are becoming increasingly autonomous, hence drivers demand hands-free access to virtual assistants. At least that's the underlying narrative. The underlying reality is slightly more mixed.

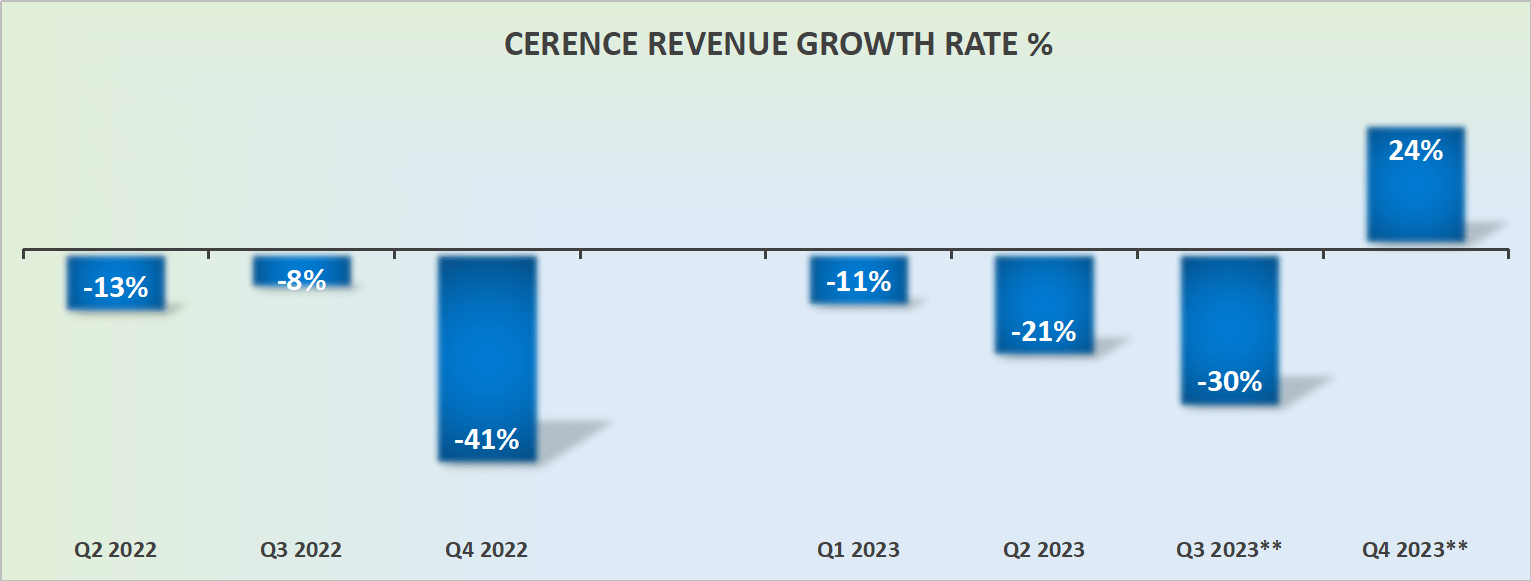

Revenue Growth Rates Set to Improve

{kind=link}

The bull case here is that once we get past fiscal Q3 2023, then Q4 2023, and in particular fiscal 2024, should see Cerence on a path towards solid and sustainable growth rates.

That being said, the skeptic in me is quick to remark that this is natural, given that fiscal 2023, particularly the first 3 quarters have been so remarkably unremarkable.

What's more, anyone that follows Cerence closely is undoubtedly aware that its license business is the crown jewel of this investment case. With this context in mind, this is what management stated last month :

[...] the license business remains strong and is indicating slow improvement from the issues that have plagued auto production over the last few years.

In conclusion, the outlook appears to entertain the idea that Cerence's prospects should be stabilizing. And that's clearly an attractive aspect to consider, but now let me get to why I'm not particularly bullish on Cerence's stock.

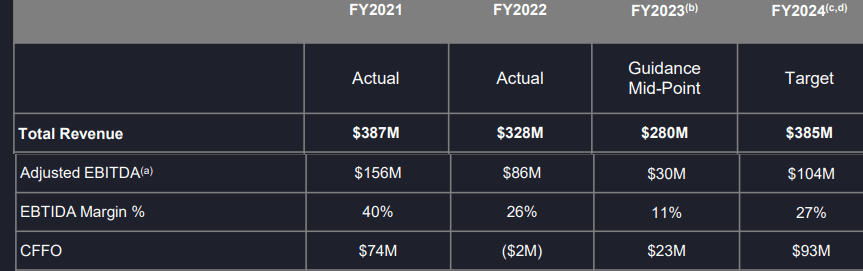

Profitability Profile Points to a Dramatic Jump in Profitability

{kind=link}

There are two main reasons why I'm unsure about Cerence's prospects. Firstly, including its full fiscal 2023 guidance, Cerence's adjusted EBITDA figures are not that impressive.

At approximately $35 million of EBITDA being guided for at the high end, that hardly supports its valuation of more than $1 billion of market cap.

But on top of that, the second consideration is that there's a lot riding on Cerence's EBITDA profitability dramatically improving in fiscal 2024.

As you can see above, Cerence is guiding for more than a triple in EBITDA growth next fiscal year.

And to further complicate matters, Cerence's fiscal 2022 bookings ended the year at $648 million. While its bookings for the first half of fiscal 2023 point to $263 million. Meaning that if we annualize this booking number and add some extra growth on top, even then, I don't believe we'll cross higher than $610 million.

Meaning that its bookings, a leading indicator of revenue growth rates will be lower this year than in 2022. These facts hardly describe a growth company.

And while it's not a thesis breaker, but rather, just another consideration, after its convertibles capital raise, the business will be left with approximately $360 million of net debt.

Secondly, allow me to put forward this consideration. If Cerence is expected to see its profitability so significantly ramp up over the next several quarters, why is the company raising funds via convertibles?

The Bottom Line

Cerence Inc. presents a mixed picture.

On the positive side, Cerence is showing signs of improvement with a challenging quarter ahead before expecting growth rates to pick up.

However, Cerence Inc. stock doesn't appear attractively priced, and there seems to be an optimistic outlook for fiscal 2024 profitability. This raises questions about why Cerence is seeking additional capital through convertible debt.

While the revenue growth rates are expected to improve after a lackluster fiscal 2023, concerns remain about the company's profitability profile and the need for significant growth in fiscal 2024.

The company's debt situation and the decision to raise funds through convertibles further add to the uncertainties surrounding Cerence's prospects.

On balance, I'm neutral about Cerence Inc. stock.

For further details see:

Cerence: Revolutionizing The Road With AI Assistants