TSLA - Chart Industries: Big Difference

Summary

- Chart management made a financing error that dropped the stock price.

- The business of the company still appears unaffected.

- Elon Musk very much affected the business of Tesla with his public comments.

- The Chart Industries stock price has a good chance to be 50% of the offering price in the secondary offering within 18 months.

- Convertible securities outstanding will limit the upside potential of the common in the short term until they convert.

Chart Industries ( GTLS ) made a financing error that cost shareholders dearly.

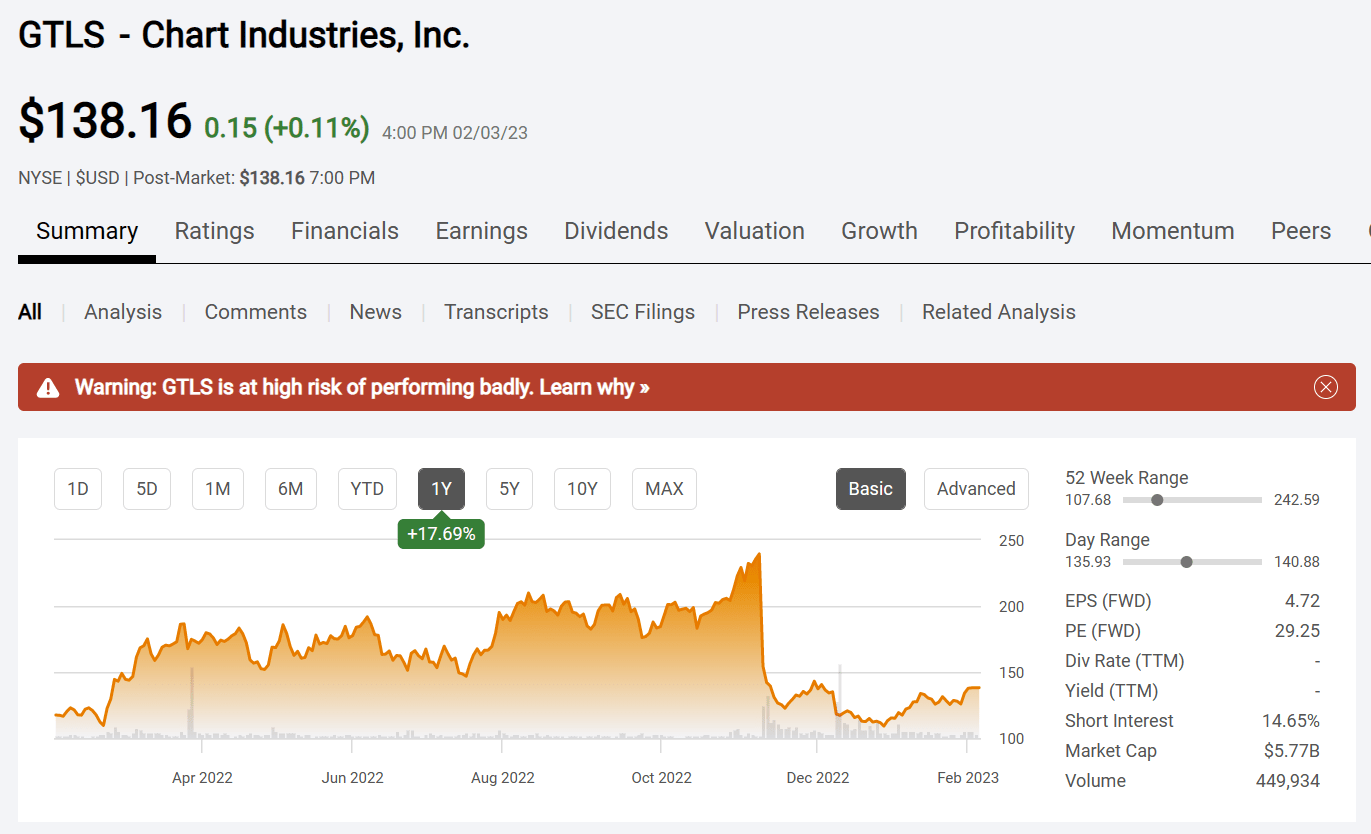

Chart Industries Common Stock Price History And Key Valuation Measures (Seeking Alpha Website February 4, 2023)

{kind=link}

The above slide obviously shows where the financing error occurred. Management realized too late that there should have been an equity component. So, the equity component was included in the financing at a later date. But the additional equity has caused some additional pricing weakness since then.

Generally, research long ago established that the stock price will usually reach 50% of the offering price within 18 months of the common stock price offering. Authors such as David Dreman in his latest book "Contrarian Investment Strategies: The Psychological Edge" covers this well researched issue. Since we are in a down market, that possibility certainly looms into the future. This company has much of its earnings end loaded in the past. Whether that will change with the acquisition is another matter. But a down market with relatively less significant earnings reports in the first half of the year is a good prescription for stock price weakness.

However, the company has an advantage that many more leveraged companies do not have. The company traditionally reports a backlog that takes the fiscal year (and usually then some) to fill. Therefore, cash flow generally does not decline during the fiscal year. Production can be pushed back because of delays. But the cash flow is not lost. That provides an unusual amount of uncertainty in a risky situation. More venturesome investors may want to do some due diligence on this company.

Final Financing

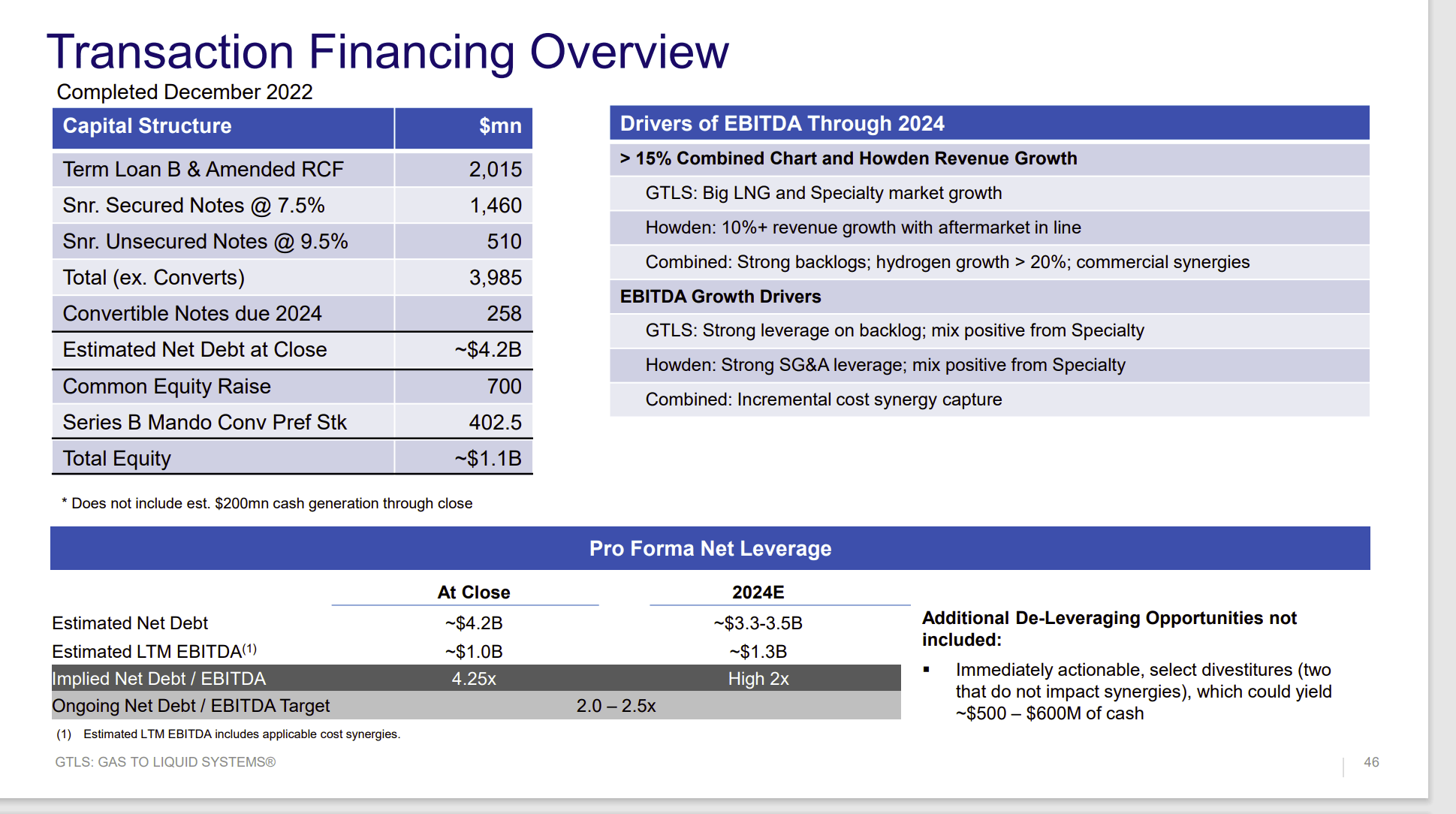

Recently management presented the final financing of the company once the merger takes place.

Chart Industries Financial Structure Guidance For Post-Merger (Chart Industries Investor Presentation January 6, 2023)

{kind=link}

Notice that managemen t has altered the financing to include the sale of some common shares as well as some convertible preferred. However, the convertible preferred does have a senior claim to the assets and therefore is about the same as debt for shareholders. Therefore, the leverage to common shareholders will be greater than the management published figures because of the convertible preferred outstanding.

Similarly, the convertible preferred, and the convertible debt represent dilution that must be overcome for common shareholders to receive benefits from the company growth after the conversion. In short, management may have set some tough challenges ahead when it comes to the common shares and simplifying the capital structure after this merger.

The future of the combined company is bright. But getting there with a regular balance sheet should be an interesting adventure. Mitigating the risk of the adventure is the long lead times combined with a high order rate. Therefore, the business is pretty much known 12 months ahead of time. That does help when you know you are going to be highly leveraged.

Another Key Difference

This situation has been compared to the ongoing Tesla ( TSLA ) saga by more than a few panicked investors. But the key difference here is that the customer base is largely intact for Chart Industries. Orders are expected to continue flowing as management has done nothing to upset the customers.

Elon Musk has upset investors with his Twitter focus . Musk has also upset Tesla customers with his Twitter antics and that has led to s ignificant order cancellations . Tesla needed a loyal customer base to overcome its low J D Power ranking of 30 out of 33. Should this situation continue to prove significant, Tesla could well be on its way to the corporate graveyard despite a decent balance sheet and a record of growth. This is a situation that needs to be turned around.

Tesla management did note record Chinese sales for the month o f January. But a record pace alone is probably not going to satisfy the market alone as this management has long guided to a 50% increase record pace. Like Chart Industries, this could be a very interesting 12 to 24 months.

The difference between the two companies is that the market has assigned a risk for the higher leveraged balance sheet of Chart Industries. But that has nothing to do with the business which is booming. But Tesla now has a business issue with the customers it sold its products to. As a result, the business is likely significantly damaged. If that is not repairable, then Tesla may well not be able to compete in the future. The situation with Tesla is therefore far more significant to long-term prospects.

The market focus on Tesla sales is only part of the issue. The long-term trend of sales and how fast customers forget some things are still very unanswered questions.

The Financing

The key part of the Chart Industries financing that is actually likely to prove to be very predictable is shown below :

Chart Industries Howden Acquisition Presentation Leverage Strategy November 2022 (Chart Industries Howden Acquisition Presentation November 2022)

{kind=link}

Since The Chart Industries business has relatively long lead times, the fiscal year 2023 cash flow is relatively predictable. A few small orders can be added towards the end of the fiscal year. But the production plans for fiscal year 2023 are largely known at this time.

Therefore, that debt repayment combined with planned growth for 2023 is relatively predictable. Management would likely tell you they have a significant start to 2024 as well. Orders appear to roll in about 15 to 18 months ahead of time. So, the initial deleveraging would appear to be relatively well backed up by now.

The trickier part for shareholders will be the conversion of all the convertible securities out there.

Chart Industries Financing Of Howden Acquisition (Chart Industries Presentation Of Howden Acquisition November 2022)

{kind=link}

Management is issuing some mandatory convertible preferred stock and already has c onvertibles on the balance sheet. These securities may limit the upside potential until they are gone. What has changed from that original announcement is shown earlier. The final financing has common stock replacing some of the preferred even though the JPMorgan ( JPM ) has not changed.

That means in the short-term, there is a statistical risk of downside that follows a sale of common stock combined with an upside potential limit due to the significant amount of convertible securities outstanding after the Howden acquisition is completed.

The Business

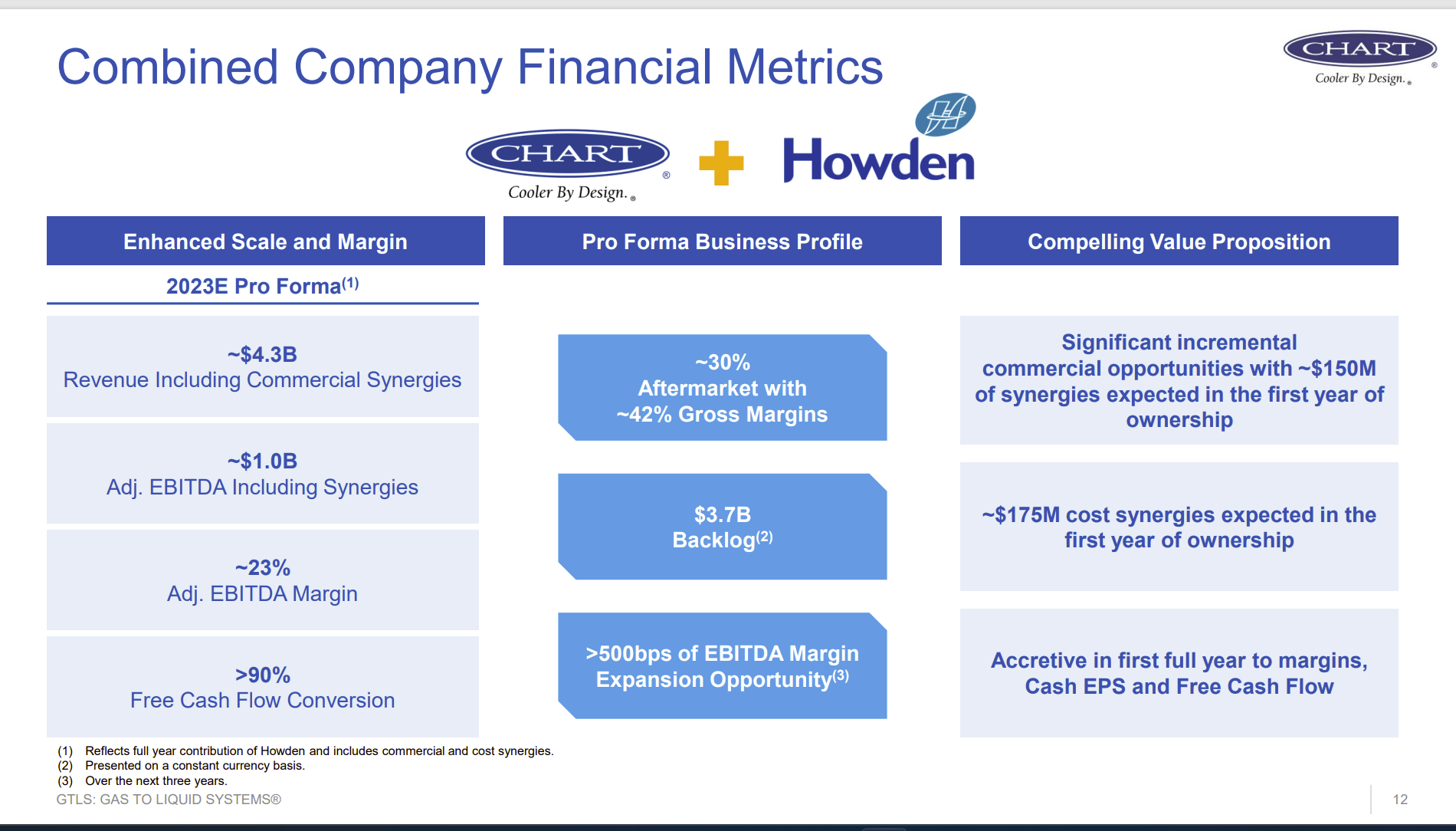

Howden brings a significant backlog to combine with the Chart backlog that ensures a booming business at least for the time being.

Chart Industries Post Acquisition Outlook Including Howden (Chart Industries Howden Acquisition Presentation November 2022)

{kind=link}

Chart will usually "keep everybody in place" when it makes an acquisition. That definitely minimizes the risk of an acquisition going south (especially a big acquisition like this one). Generally, the benefits accrue from the combined sales efforts of the newly combined company and sales force. This is demonstrated in the slide below:

Chart Industry Presentation Of Howden Acquisition Sales Benefits (Chart Industry Howden Acquisition Presentation November 2022)

{kind=link}

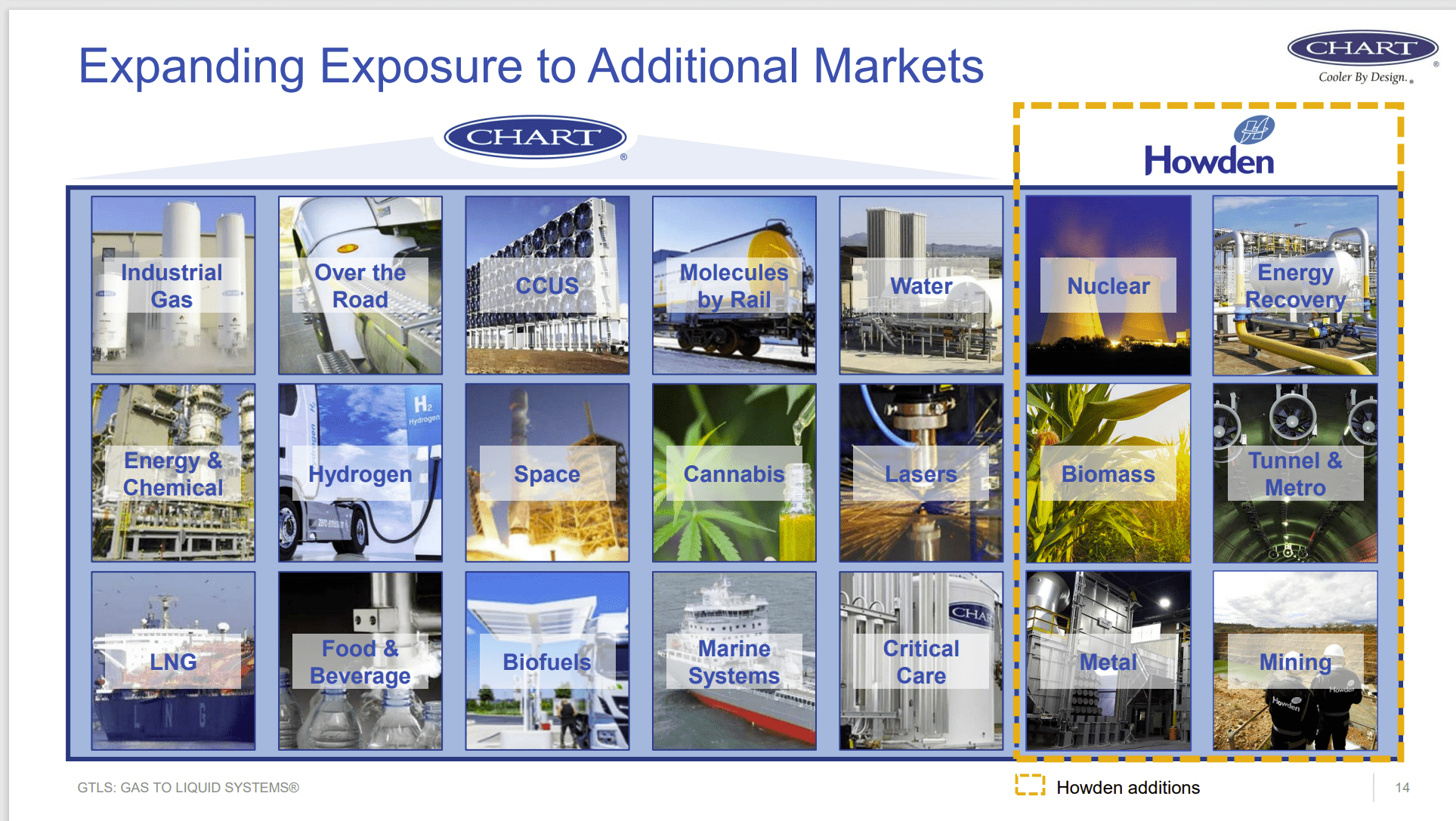

The company gains exposure in some very fast-growing markets as well as some more established markets. Management hopes that with the balance between the various markets that the company can continue to grow even if a market or two declines.

The common denominator for all the industries is the handling of gas of some form. With Chart, the technology rarely changes much. But products for each market are generally acquired rather than developed. This has proven to be a profitable strategy in the past with a lot of smaller acquisitions.

Note that the latest January presentation goes into far more detail on all of this for any interested investors.

The Future

The sale of some common shares has added some safety to the deal and reduced the financial leverage a little bit. The situation could have been handled much better with an initial announcement of an equity offering to finance the deal. The cost of not putting in the initial common equity in the financing plans is that the preferred will convert at a far lower stock price than would have likely been the case.

It does appear that management is counting on at least some convertible (either preferred or debt) converting in the first year of the combined company's existence. The reasonableness of that assumption is up to the investor to decide. In any event, there will be some decent EBITDA growth if this merger goes through like the others in the long history of Chart Industry mergers.

There is a fair amount of various convertibles outstanding after the acquisition that may "put a lid" on share price appreciation in the short term. So, investors may want to see the stock price action of the newly combined company before they "jump in". The financial leverage definitely makes this a risky situation as the preferred will count the same as debt for common shareholders and raise the financial leverage considerably above the target leverage noted in the presentation.

Still, this business is very predictable and it's booming. Management has done its best to diversify away from the large oil and gas projects that were the "bread and butter" of this company way back when it was founded. The one good thing about this combination is that it takes a giant step away from the oil and gas industry.

Management can restore market confidence by getting the capital structure simplified as soon as possible. It will take some time. But venturesome investors who do not mind the risk factors may want to consider this security once the current pricing weakness ends. The markets the company sells to are by and large very good growth markets that bode well for the future.

Disclaimer: I am not an investment advisor and this is not a recommendation to buy or sell a security. Investors are recommended to read all of the company's filings and press releases as well as do their own research to determine if the company fits their own investment objectives and risk portfolios

For further details see:

Chart Industries: Big Difference