CHWY - Chewy: Long-Term Growth Potential Intact With Enlarged TAM

2024-01-05 09:47:36 ET

Summary

- I still see CHWY as an attractive long-term investment despite weak active customer performance.

- The company's plans to open veterinary clinics in 2024 enable it to fully address the $47 billion pet health TAM.

- Autoship, which allows customers to auto-purchase products at predetermined intervals, is a strong growth driver for Chewy.

Summary

Following my coverage of Chewy, Inc. (CHWY), which I recommended a buy rating due to my belief that there were still multiple positive aspects of CHWY business that deserved credit despite the weak active customer performance. This post is to provide an update on my thoughts on the business and stock after reviewing Investor Day. I continue to see CHWY as an attractive long-term position given the enlarged TAM and long-term growth potential. However, I am now more conservative in my assumptions, as the active customer metric has not shown any strength yet. I also reiterate my point that investment positions should be small at this stage.

Investment thesis

For reference, I will touch on the 3Q23 results briefly so readers can understand why the share price reacted negatively post-earnings, followed by a surge (which I believe was due to the positive message sent during the Investor Day). Regarding the results for 3Q23, I must admit that the revenue performance was less than satisfactory. The sequential decline in Active Customers resulted in revenue falling short of management's guidance. CHWY is still stuck in the weak part of the cycle where macro weakness continues to weigh on the industry broadly, with pet household adoptions declining by 16% y/y. Adopting a pet is, after all, a discretionary expense. As I mentioned before, the market is heavily focused on how the Active Customer metric trends. As such, the disappointing performance and management expectation that Active Customers will only turn when macro stabilizes (which is not anytime soon) caused the negative share price action.

{kind=link}

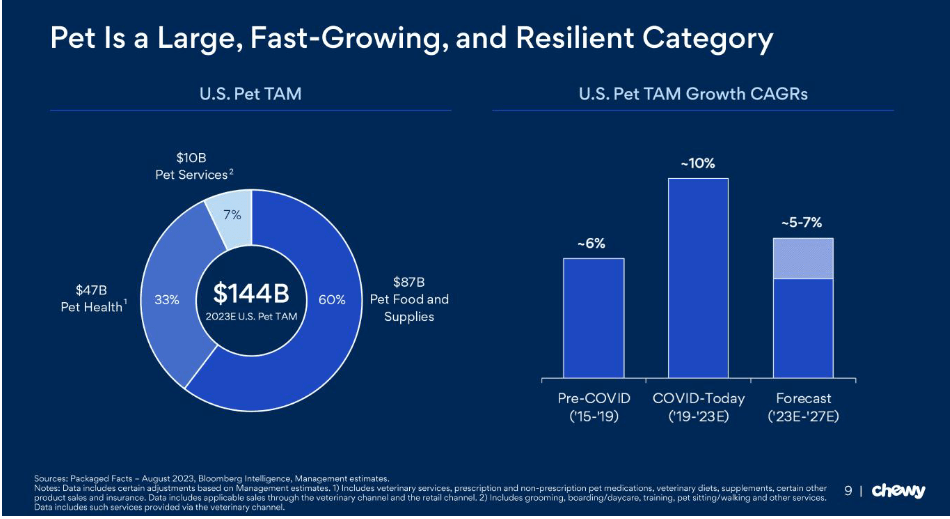

Boiling it down, I believe the issue that investors are concerned with is whether CHWY will be able to continue growing, and management gave a very positive answer during Investor Day. Management revealed plans to open four to eight veterinary clinics in 2024 as part of their health offering expansion during the presentation. This is an important step in unlocking the full $47 billion pet health TAM (CHWY currently addresses $22 billion of the $47 billion). At maturity, a well-performing clinic can expect to earn $2 million in revenue and have an EBITDA margin of 20%, according to management. While this seems to contribute very little to FY24 performance (8 * $2 million is only $16 million), I think the bigger implication here is that it provides another avenue of revenue stream for CHWY. On top of the clinic-driven revenue, it opens doors for CHWY to increase its wallet share and drive adoption of its current offerings. Examples include suggesting a pet food product, insurance, and telemedicine. By my math, in terms of units, the addressable size is easily more than 10 thousand ($25 billion / $2 million revenue). Clearly, there is a lot of opportunity for CHWY to capture here.

I also think that the vet clinic will bode well for CHWY Health. For context, CHWY Health revenue has grown at about 37% CAGR (from FY18 to FY22), reaching around $3.1 billion in revenue. The business-to-consumer (B2C) offerings of CHWY (such as pharmaceuticals, nutritional supplements, and OTC medications) were the primary growth engines. This business unit is a lot more profitable as well as having a much higher gross margin (10 points higher than CHWY retail), primarily due to compounded medications being more profitable than core pharmacy sales. With CHWY entering the vet clinic space, I believe it will provide a more wholesome healthcare service to pets, and pet owners that are more skeptical will likely be more open to adopting CHWY online services (they could first visit the clinic to see whether CHWY is trustworthy before adopting online). In other words, I see this offline channel expansion as another customer acquisition channel for CHWY. Therefore, I am positive that CHWY Health can grow. Note that only 20% of CHWY customers have purchased from CHWY Pharmacy, so there is also a penetration growth theme ongoing.

Besides long-term growth drivers and TAM expansion, I think management gave a timely update on how effective the Autoship product has been. I continue to view Autoship as a strong growth driver because it provides a steady flow of predictable, sticky, and repeating revenue while also letting customers auto-purchase products at predetermined intervals. Customers are more loyal as a result of this convenience, and Autoship penetration has been on the rise in recent years; Autoship customers now make up 75% of CHWY's total net sales.

Valuation

Own calculation

As active customers continue to remain weak, I think it is right to adjust my growth assumptions in the near term. I based FY23 revenue growth on management guidance and assumed the same 10% growth rate for FY24 as the macro conditions are unlikely to turn super bullish in the near term. That said, I do want to highlight that the economy is definitely in better shape than a few quarters ago, as inflation has tapered and the Fed is not targeting more hikes (in fact, their intention is to cut rates). There is definitely room for CHWY to outperform my expectations. Nonetheless, a conservative approach is warranted as the CHWY active customer metric was weak. One major change to my model is that I revised my valuation multiple down from 2x to 1x. Given how the share price has reacted to CHWY 3Q23 performance and the Investor Day presentation, I think the market is unlikely to rerate the stock back to 2x just based on guidance and narrative. CHWY will need to show actual performance before the market will be convinced. Benchmarking how Rover Group ( ROVR ) valuation multiple recovered back to its historical average (valuation hit a low in 2H22), the path was gradual (and not a sharp jump), and I assume the same path for CHWY valuation.

Risk

My revenue projections might be way off if CHWY's active customer base continues to deteriorate more than I expected. This could be due to excessive churn or gross additions worsening as the macro environment continues to show no sign of further improvements.

Conclusion

In conclusion, I reiterate my buy rating for CHWY given the enlarged TAM and long-term growth potential despite near-term challenges with the active customer metric. I thought the Investor Day was really positive as it gave an update on management expansion plans into the $47 billion pet health TAM, leveraging veterinary clinics to broaden revenue streams and enhance CHWY's healthcare offerings. I believe this strategic move complements CHWY Health's impressive growth trajectory, particularly in B2C offerings. Autoship's efficacy in driving predictable and loyal revenue remains a robust growth driver.

For further details see:

Chewy: Long-Term Growth Potential Intact With Enlarged TAM