YANG - China: A Lesson For Underestimating Emerging Market Risks

2023-12-27 08:45:51 ET

Summary

- Share prices of leading Chinese tech companies like Alibaba, Tencent, and Meituan are still down significantly since the clampdown began.

- In hindsight, there were already signs of exuberance and investors appeared to have underestimated the risks of investing in emerging markets.

- Investors had bought into large swaths of debt issued by highly leveraged real estate developers, believing the narrative touted by investment bankers that "these companies are backed by the government."

- The secretive nature of China's internal politics means that investors have little means of deciphering how China's new leadership would think and act.

- We see little reason to be bullish on China unless the political leadership demonstrates that it is willing to put aside its political ideologies and refocus on economic progress.

It has been three years since Chinese authorities clamped down on China's leading tech companies including Alibaba Group Holding Limited ( BABA ), Ant Financial, Tencent Holdings ( TCEHY ), Meituan ( MPNGF ), and ByteDance. Since then, the outlook for China's equity market has remained murky as investors gradually lose confidence in the economy.

With the tech clampdown holding back innovation and growth at China's leading tech companies, Western competitors were given a rare opportunity to extend their lead in cloud computing and artificial intelligence technologies. Further regulatory clampdowns in real estate combined with the draconian lock-down measures implemented during the peak of the COVID-19 pandemic, only exacerbated the selloff. With no end to the selloff in sight, foreign investors as well as Chinese billionaires have begun to shift assets elsewhere.

For investors who remained hopeful that an end to the regulatory clampdowns would eventually trigger a forceful rebound in Chinese equities, the long wait has only added to losses. Despite several occasions where senior Chinese officials have hinted that the regulatory clampdowns may be nearing an end, those promises and reassurances have amounted to nothing more than speculation.

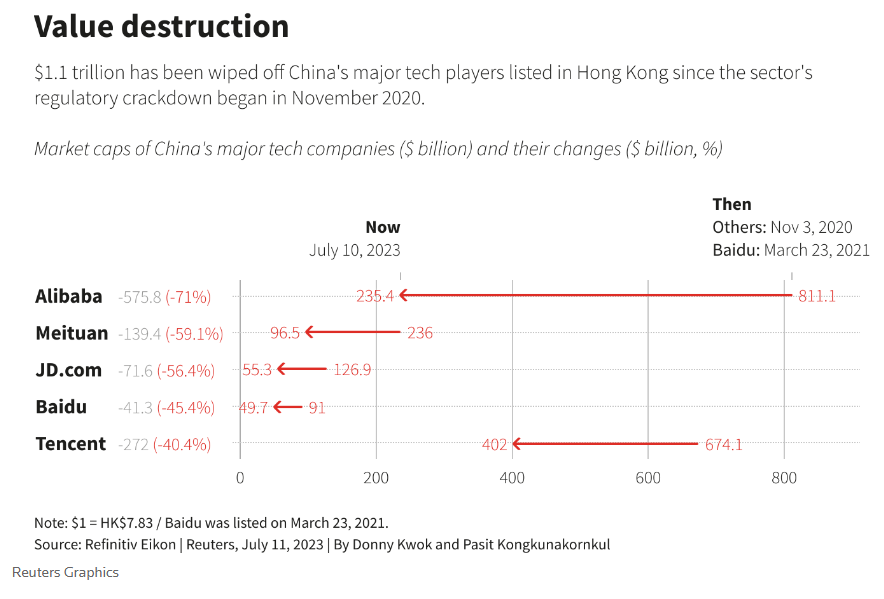

According to an article published by Reuters in July, an estimated US$1.1 trillion had already been wiped off the valuation of China's leading technology companies.

{kind=link}

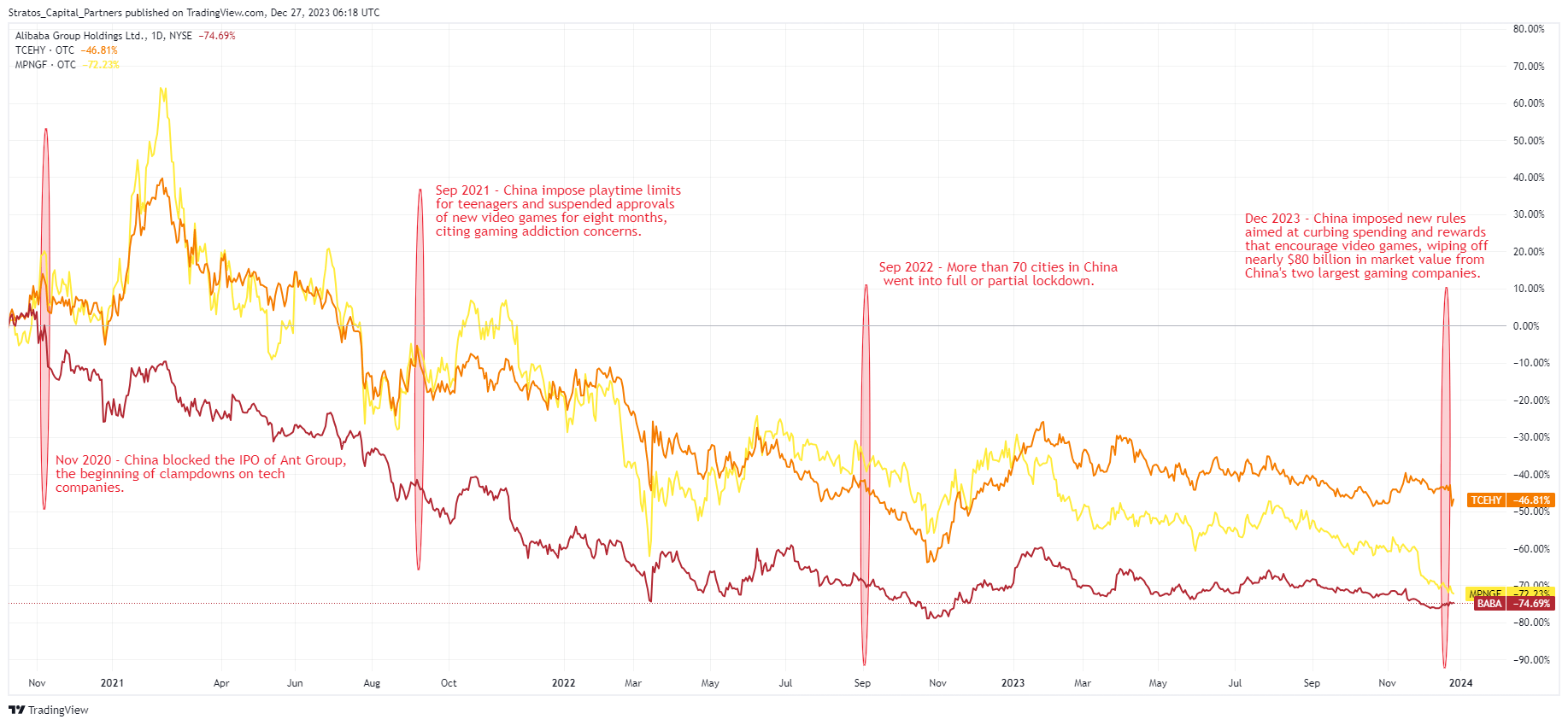

Since then, the share prices of these tech companies have only continued to fall. As the accompanying chart shows, share prices of Alibaba, Tencent, and Meituan are still down -50% to -70% since China initiated a clampdown on tech companies in late 2020.

{kind=link}

These staggering losses have raised important questions as to why investors were completely blindsided by the Chinese Communist Party's ((CCP)) actions. How even professional portfolio managers and institutional investors have underestimated the risks in the chase for higher returns.

Some investors may blame the CCP for failing to consider the economic consequences of interfering in the tech and real estate sectors. Others may blame the Biden administration for adding insult to injury by tightening export controls on advanced semiconductor chips in a bid to block China from acquiring advanced chips.

We think the real reason behind these losses was much more fundamental. Investors have become greedy and complacent after witnessing China's rapid rise over the years, and have underestimated the risks associated with investing in emerging markets.

Underestimating Political Risks In Emerging Markets

There are many reasons why some institutional investors and portfolio managers choose to invest in emerging markets. One reason is that emerging markets are countries that are going through rapid economic development and therefore experiencing a phase of elevated economic growth. Thus it is not unusual to see sustained real GDP growth of well above 6% in emerging markets. Companies therefore also enjoy greater potential for growth in emerging markets than in mature developed markets.

Another reason is that investors understand there is a risk premium embedded in emerging market assets. Therefore, investing in emerging markets potentially generates higher returns for equity portfolios long term. Although it is not possible to directly observe this risk premium in real time, many studies have shown that such premiums do exist and can be harvested over time just like any other factors including value, quality, liquidity, or size.

The real problem, however, is that investing in emerging markets seems like a good strategy only during normal economic and political environments.

Because emerging markets tend to have less reliable economic systems and institutions, investing is fraud with hidden risks. In the event of an economic crisis, emerging markets often lack effective policies and robust institutions needed to respond adequately. Just like how many emerging markets have experienced debilitating currency devaluations and capital flight in the past. Capital flight is particularly common and unique to emerging markets because developed country currencies are often viewed as safe haven currencies in times of crisis. Thus capital flight often exacerbates an economic crisis in emerging markets, resulting in a loss of confidence in the local currency and credit markets freezing up.

Furthermore, political upheavals are also more common in emerging markets, where existing economic policies are constantly at risk of being modified or scrapped entirely with political change. This adds to the uncertainties of doing business and investing in emerging markets.

China's Risk Premium

In the case of China, with its authoritarian single-party political system, the government holds absolute power and can enact sweeping economic policies in very little time. One key advantage of such authoritarian political systems is that policies can be executed decisively when needed.

However, the tradeoff is that free markets are unable to function effectively when the government chooses to intervene excessively, often distorting economic incentives and disrupting the workings of a healthy capitalist system. When China clamped down on its leading technology companies and real estate, it demonstrated how the prospects of investing in the economy could change so quickly and drastically.

In hindsight, there were already signs of exuberance. Investors had bought into large swaths of debt issued by highly leveraged real estate developers, believing the narrative touted by investment bankers that "these companies are backed by the government" or "the government will never allow these companies to default." Investors were too happy to ignore the risk premium embedded in the high yield offered by Chinese bonds and believed that higher returns were possible with little risk.

To a certain extent, many investors believed that the CCP would continue to pursue economic growth over its political interests. Afterall, that was exactly why China's economy has performed so well since its accession into the World Trade Organization in 2001. China's focus on economic growth and improving the economic welfare of its citizens seems to be the only logical way forward. But economic logic means very little to political leaders in single-party states like China. Securing power is a top priority, economics can wait.

The secretive nature of China's internal politics also means that investors have little means of deciphering how China's new leadership would think and act. And sure enough, President Xi Jinping would later surprise the world by directing the country's focus towards "common prosperity" and "national security" in a bid to secure the CCP's power. Ambitious private enterprises were warned not to put profits before duty to citizens. The state media repeatedly echoed Xi Jinping's warning that "Houses are built to be inhabited, not for speculation."

What can investors possibly expect from an economy where corporate profits are frowned upon and where real estate is viewed more like a consumable than an investment?

China's economy currently remains in a state of stagnation. And we see little reason to be bullish on China unless the political leadership demonstrates that it is willing to put aside its political ideologies and refocus on economic progress. That would be a massive hurdle for Xi Jinping, however, as pivoting on previous policies would be an admission of failure and risks political in-fighting within the CCP. But failing to do more to stimulate the economy means China is likely to continue to be stuck in its stagnating economic state.

For further details see:

China: A Lesson For Underestimating Emerging Market Risks