PG - Church & Dwight: Checking If The Bull-Case Is Still There (Rating Downgrade)

2023-07-06 15:46:10 ET

Summary

- Church & Dwight has historically been a steady compounding machine with a strong track record of long-term results.

- The company has a clear business model focused on executing its Evergreen Model and acquiring power brands that are leaders in their respective categories.

- After a tough 2022, the company's execution appears to be back on track, with positive signs of trend reversion, better inventory management, and strong Q1 results exceeding expectations.

- In this article, I go over my investment thesis to see what investors should do with the stock after the recent bid up in price.

Introduction

Many investors know how boring companies can often turn into exciting investments, especially over the long term, where a company's compounding power can unleash its power.

Church & Dwight ( CHD ) is one of these, as many have come to consider it a well-oiled compounding machine due to its ability to reach long-term results at a steady pace.

After a tough 2022 that affected both the company and the stock (the company seeing margin compression and its first-in-sixteen years negative TSR - total shareholder return; the stock selling-off until November from all-time highs ('ATHs') to the low $70s), Church & Dwight has once again turned to be a market-beating holding YTD.

Having recently breached the $100 a share threshold, the stock is getting near to its closing ATH price of $102 and change reached in April 2022, before the steep sell-off. Seeking Alpha is also giving an F as valuation grade , suggesting the stock is overvalued.

Since I am a shareholder, as I am preparing to read the upcoming earnings report that will be released at the end of the month, I am going over my investment thesis to see if it is time to add, to hold or to take my gains and move on. The core of my bull-thesis was the proven ability of the company to pursue steady revenue growth at high margins thanks to accurate acquisitions and a clear business model which is being executed year after year. I saw the power of a true compounder here and I decided to be part of the game for the long run.

Now, in this article, I will share my recent research to explain what I have decided to do.

An overview of the company

Church & Dwight is a very old company founded in 1846. It is the leading U.S. producer of sodium bicarbonate (baking soda), a natural product that cleans, deodorizes, leavens, and buffers. The most iconic brand of the company is the Arm & Hammer brand, whose products are in 86% of U.S. households. To show how important this brand is for the company, it is enough to know out of $5.4 billion of sales in 2022, $2 billion is Arm & Hammer.

The company's products business is split into three segments: domestic (77% of net sales), international (17% of net sales), and specialty products (6% of net sales), offering inorganic chemicals, animal nutrition, and specialty cleaners. Its product portfolio is made up of premium products for about 60% while the remaining 40% is part of the value category. This poises the company to capture demand both when consumers are trading down to value and when they are stepping up to premium.

There are two main pillars the company is made up of, as far as I understand it.

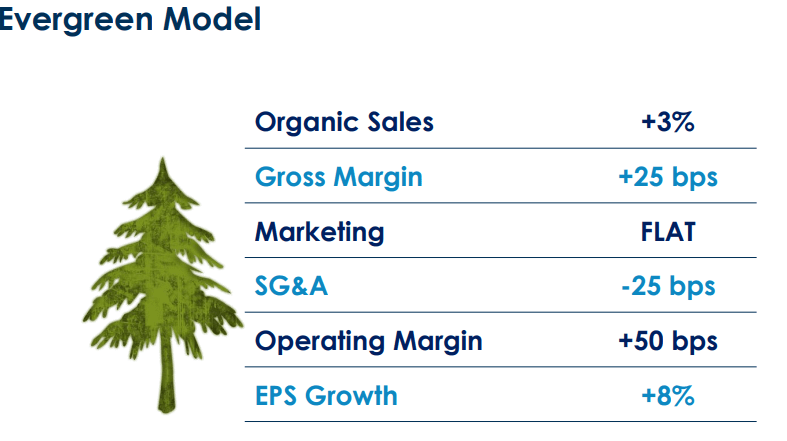

First one the company has developed what it calls "The Evergreen Model".

{kind=link}

What I like about this is that the company, year after year, is predictably focused on executing this model. It seems plain and simple, yet, it is actually challenging to keep on compounding according to these metrics in a mature and competitive industry such as consumer staples is.

The second pillar shows part of how Church & Dwight aims at executing the evergreen model. In fact, the company fuels its growth by collecting the so-called power brands, which are all either #1 or #2 in their category. In addition, out of the 17 product categories Church & Dwight competes in, only 5 have private label exposure.

CHD 2022 Annual Report

Though some acquisitions may not have worked out as they should have (in late 2022, the company wrote off its investment in Flawless, a hair removal devices business) because of unexpected pullbacks or valuation mistakes, generally speaking, Church & Dwight has a proven track-record of hitting the nail on the head when making acquisitions. In fact, most of them turn out to be EBITDA accretive. In addition, Church & Dwight is able to acquire small brands leading a certain niche and expand their distribution all across the country, leveraging its network. At almost no cost, any acquisition immediately sees a boost in sales thanks to Church & Dwight's distribution scale.

Recent issues

In 2022, Church & Dwight failed to add yet another year to its 15-year positive streak of total shareholder return. As volumes decreased and margins compressed, the company could not help but release an EPS decline which made Mr. Farrell, the company's President and CEO, admit his disappointment. And yet, while reading the 2022 annual report and listening to the Q4 2022 earnings call, I thought the company was already leaving the black swan behind.

Execution back on track

It is impossible to think a company's growth path to move ahead smoothly without anything standing in its way. This is why I believe it is already remarkable how Church & Dwight has been able a top-performer under this point of view, delivering steadily compounding growth at a pace that seems slow, but that generates a snowball effect of large impact over the long term.

Furthermore, in the report of Q4 2022, there were signs already showing a trend reversion, also thanks to better inventory management, fewer supply chain issues, and an increased spending on marketing (which is still not being financed at pre-Covid levels). This is why I had no issue in awarding a buy rating to the company back in February. Since then the stock has returned 20% to the shareholders.

More evidence was given at the end of April, when the company released its Q1 report , with results exceeding expectation:

- Organic sales were $1.43 billion and grew 5.7% driven by product mix and pricing

- Gross Margin increased 90 bps to 43.5% thanks to productivity and pricing offsetting inflation

- Operating cash flow was $273.1 million, an increase of $120.3 million YoY

The company thus revised upwards its guidance expecting organic sales growth between 3-4% (previously 2-4%), operating profit for the year between 6-8% (previously 4-8%), and gross margin to expand by 120 bps.

Operating cash flow is now forecasted to be around $950 million (previously $925) and - who knows? - could actually cross the $1 billion threshold.

During the earnings call , we received further details that make us feel the pulse of the general economy. Consumers are still spending, but it was highlighted how the trade down to value detergent keeps on going on into 2023. And this is good news for Church & Dwight and its iconic Arm & Hammer brand which grew 9.3% versus the 3.6% of the category. It now has a 14.3% market share. This is what management said regarding this situation to profit from:

with more consumers migrating to ARM & HAMMER laundry detergent, we have the potential for a long-term benefit to the ARM & HAMMER brand similar to the last recession. In litter, the category grew 12.7%, while ARM & HAMMER litter grew 13.5%. So we gained market share in the quarter. We did see a trade down from our premium ARM & HAMMER Cat Litter to our ARM & HAMMER value litter, which is in the orange box. So consumers are staying in the ARM & HAMMER franchise .

Another highlight is the performance of the Batiste brand in the dry shampoo category. With a 20% increase in consumption, it now has a 46.2% market share.

The two most recent acquisitions, Therabreath and Hero, are also performing well. As expected, distribution of Therabreath doubled since 2021 and the results are before our eyes: 70% consumption growth, with a market share of 22.5% of the alcohol-free mouthwash. Hero grew YoY by 43.5% and gained 1.6 share points to reach a 9.1% market share in the total acne treatment category. Here, too, we see the scale-effect Church & Dwight was able to give, by expanding distribution by 50% since the October acquisition date.

Alignment between all stakeholders

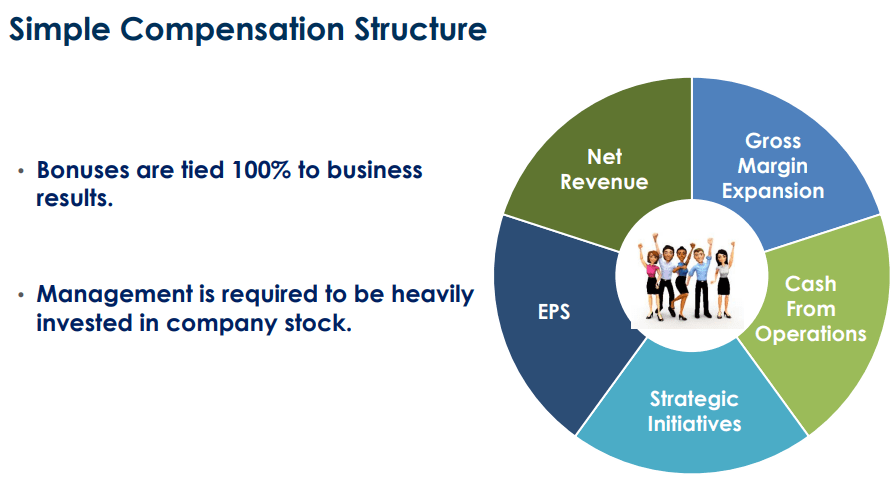

What I think investors should also know about Church & Dwight is its simple compensation structure which enables all stakeholders to be aligned. In fact, employee bonuses are tied to business results, with 20% of total bonuses linked to gross margin expansion. In addition, management is required to be invested in the stock. This reassures investors.

{kind=link}

Relevant financials

Margins

Church & Dwight used to have a gross margin above 45% before the pandemic hit. At the end of 2022, the company likely hit its low with 41.86%. Though this was not a good result, I suggest zooming out and looking around: how many companies achieve such a gross margin considering it disappointing? This gives a sense of the company's profitability. The Flawless impairment charge had a $411 negative impact on the results and brought operating margin down from 20% to 11% and the net profit margin to 7.7% versus 16%. I expect the company to have an operating margin at 21% and a net profit margin at 16% by the end of the year.

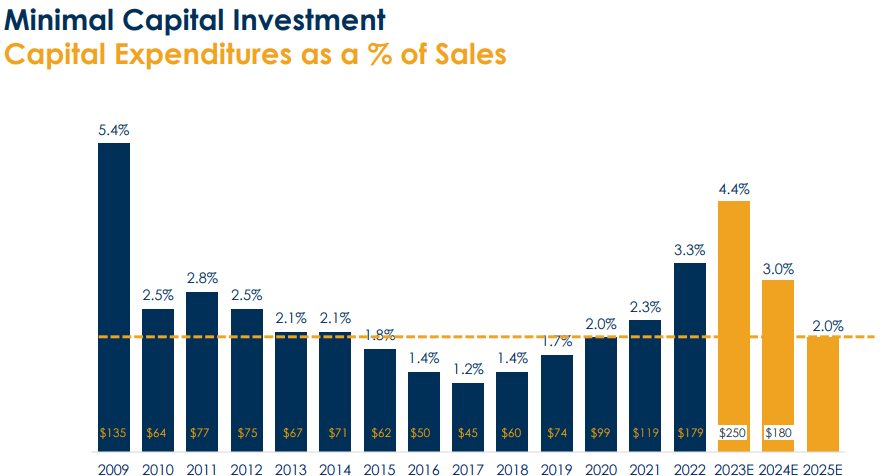

Capex

Another important aspect of the company is its low capex. Before revenues of almost $5.5 billion, capex amount only to 3.3%. As the graph below shows, it is very rare for the company to go over this threshold, since capex usually stays between 2-3%.

{kind=link}

Clearly, this eats away little cash from operating cash flow, giving room to strong cash flow generation to support new acquisitions, pay down debt, and other forms of shareholder returns.

Debt

The company carries some LT debt on its balance sheet, $2.6 billion to be precise. However, though interest rates are rising, the company does not have any looming long-term debt refinancings. In fact, August of 2027 is the timing of its next maturity.

With FCF expected to come slightly below $1 billion this year and an expected EBITDA of around $1.4 billion, I believe this debt is well-covered no matter how we look at it.

Valuation

Overall, I see a company in good shape which, as long as it will find new acquisitions, it should keep on growing more or less at the same pace it has been for the past 20 years.

This is a high-quality company able to win in many different niches.

However, even high-quality companies can reach such a high valuation compelling to sell.

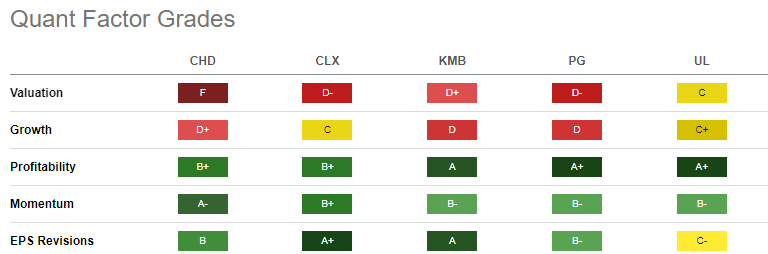

The company currently trades a fwd PE of 32.5, 58% above the sector median. This is shown by Quant Factor Grades.

{kind=link}

However, these grades reflect the poor 2022 results, highly impacted by the Flawless impairment charge. If we actually compare the growth rate among these companies, we see Church & Dwight growing well above the others with 5-yr revenue CAGR of 7.12% vs. 3.36% for Clorox ( CLX ) and 4.8% for Procter & Gamble ( PG ).

Profitability is currently given a B+, but, as we have seen above, Church & Dwight's margins are bound to increase this year as they will be back to usual levels. This will for sure lead to a better grade.

Its dividend policy, something investors carefully look at when considering stocks in the consumer staples industry, shows how Church & Dwight is more conservative in distributions, with a dividend yield of 1.1% and a payout ratio of only 34.5% (Procter & Gamble has a 2.47% yield and a payout ratio of 63.7%). Yet, the 5-year dividend CAGR of 5.60%.

Overall, the reason why Church & Dwight trades at a higher multiple is linked to its growth and its safer balance sheet.

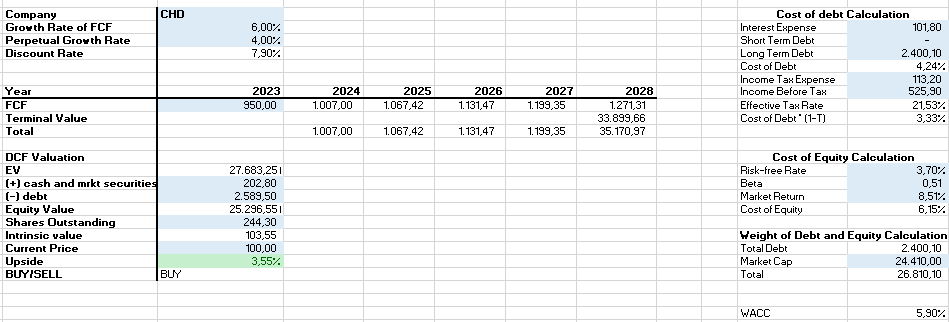

Running a discounted cash flow model, I use a discount rate of 7,90%, slightly below the market average. This is to award the company a certain premium due to its reliability.

{kind=link}

Overall, I find the company is fairly valued. I don't see any compelling reason to sell and lock in gains due to a hyper-inflated valuation, nor do I see this moment as particularly attractive as an entry point. Nonetheless, an investment like this should be considered for the very long term. Over a long period of time, the initial entry point may not be as impacting on total returns. In any case, were I not a shareholder yet, I would for sure add this stock to my watchlist and keep track of it for a while. As a shareholder, I am holding to the position, without adding other shares at the moment.

For further details see:

Church & Dwight: Checking If The Bull-Case Is Still There (Rating Downgrade)