TSLA - CHY: This Convertible Fund Could Be Worth Picking Up If The Price Improves

2023-12-26 17:50:23 ET

Summary

- The Calamos Convertible & High Income Fund offers a 10.10% distribution yield, making it an attractive option for income-focused investors.

- The CHY closed-end fund provides exposure to convertible securities, allowing investors to potentially benefit from stock appreciation.

- The CHY fund's performance has been positive, with shares up 6.64% since the last article, although slightly lagging behind the S&P 500 Index.

- The fund appears to be fully covering its distribution, although it has been eight months since the most recent report.

- The fund is trading at an incredibly large premium, so the fund appears very expensive right now.

The Calamos Convertible & High Income Fund ( CHY ) is a closed-end fund, or CEF, that income-focused investors can employ in order to achieve their goals. The fund’s current 10.10% distribution yield stands as a testament to its success in this area, as this is a very attractive yield when we consider that the yields of most funds have declined over the past two months or so.

The fund also is one of the few options available for those investors who do not wish to sacrifice the potential upside that can be obtained from common equity investments in exchange for the higher yields of debt securities. This is due to the fact that this fund has some exposure to convertible securities, which are debt securities that can be converted into common equity in certain situations. This feature allows investors to potentially profit from a situation that causes a company’s stock to appreciate significantly from the level that it stood at when the security was first issued.

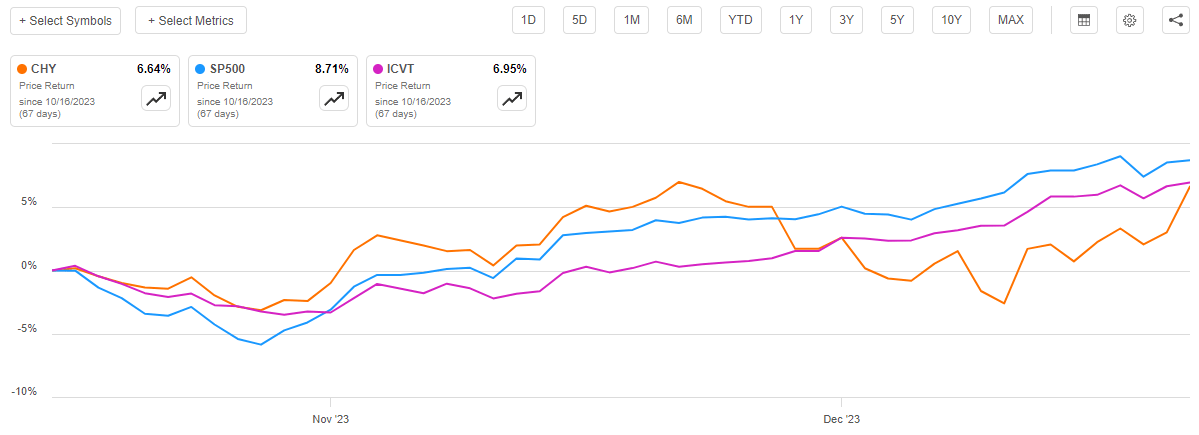

As regular readers will likely remember, we last discussed the Calamos Convertible & High Income Fund around the middle of October. That was right around the time that the overall mood in the market began to change, and investors started to bid up assets in anticipation that the Federal Reserve would cut rates over the next year. As such, we might expect that the performance of the fund has been impressive since the time that we last discussed it. This is certainly the case, as the fund’s shares are up 6.64% since the date that the prior article was published. This is, unfortunately, a bit worse than both the S&P 500 Index ( SP500 ) and the iShares Convertible Bond ETF ( ICVT ):

{kind=link}

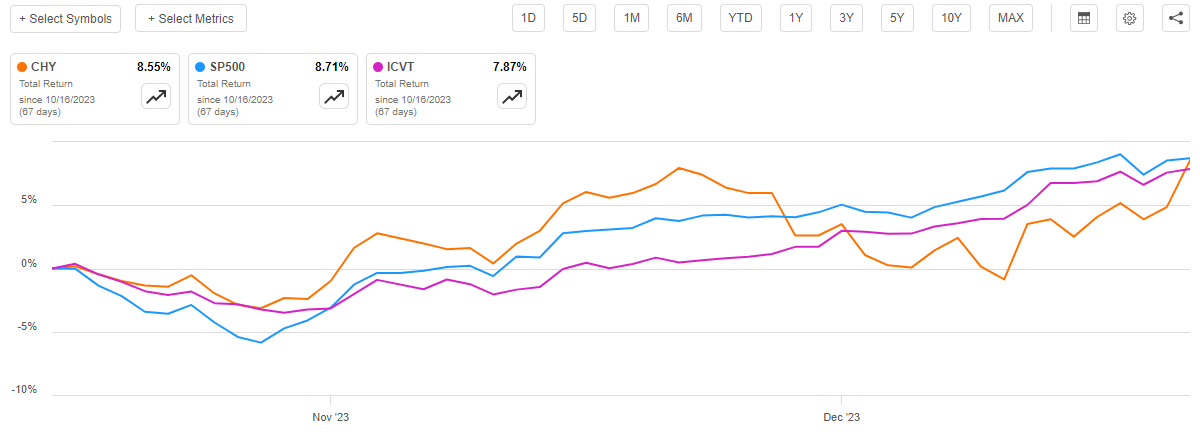

However, the Calamos Convertible & High Income Fund has a considerably higher yield than either of these indices. This is a defining characteristic of closed-end funds, as these entities typically pay out most to all of their investment profits to their shareholders. As such, looking solely at the fund’s share price performance is somewhat misleading due to the fact that the distributions received by the investors also represent an investment return to the fund’s investors. When we include the distributions that the fund paid out into its performance, it actually beat the iShares Convertible Bond ETF over the period, although it still slightly lagged behind the S&P 500 Index:

{kind=link}

This is certainly a strong enough performance to attract the attention of many investors, especially those who are looking to receive a high level of income from their assets to assist in paying bills or financing their lifestyle expenses. However, we still want to have a closer look at the fund to determine if its recent performance is justified or if it is now vulnerable to a market correction.

About The Fund

According to the fund’s website , the Calamos Convertible & High Income Fund has the primary objective of earning a very high level of total return for its investors. As regular readers can likely recall, I have criticized some fixed-income funds in the past for having total return as an objective, particularly when the fund specifically states that it is hoping to achieve its objective through capital appreciation. This one does that, as the website states:

The Fund seeks total return through capital appreciation and current income by investing in a diversified portfolio of convertible securities and high-yield corporate bonds.

A bond does not deliver long-term capital appreciation because it is both issued and redeemed at face value when it matures. Thus, there are no net capital gains over its lifetime. However, convertible bonds are an exception to this because of the convertible feature. Common stock has no maximum price that it can reach, thus it has theoretically unlimited potential. Thus, because a convertible security can be turned into common stock in certain situations, it also has no maximum upside potential. After all, the fund could always exercise this option and then either hold onto or sell the common stock to benefit from this potential for gains. The fund’s objective is therefore quite reasonable in this case.

The fund is taking advantage of its ability to invest in convertible securities. As of right now, fully 66.71% of the fund is invested in convertible securities:

Calamos

The chart of the fund’s asset allocation does not translate well to a static article, so here is the same information in table form:

| Asset Type |

| % Of Fund |

| Convertibles |

| 66.71% |

| Corporate Bonds |

| 25.36% |

| Bank Loans |

| 4.01% |

| Cash and Receivables/Payables |

| 2.19% |

| Synthetic Convertibles |

| 1.08% |

| Common Stock |

| 0.32% |

| Preferred Stock |

| 0.27% |

Presumably, the fund is not currently holding any asset-backed securities. The chart provided on the website implies that it is capable of holding them, but no weighting is currently listed. That is okay though, as the fund’s ability to hold these securities has no real impact on our thesis. The convertibles are the most important thing for our purposes, with the corporate bonds playing a secondary role. These are by far the two most heavily weighted assets in the fund, which is nice to see.

One of the problems with convertibles is that they can be difficult to obtain, but they are almost the ideal security for income-focused investors. This was especially true over most of the past fifteen years or so as it was nearly impossible to obtain decent yields from ordinary corporate bonds or even junk bonds. Granted, the yields on convertible bonds are no better than those on conventional bonds (in fact, they are usually a bit lower) but the ability to convert into common stock makes it easier to stomach fixed-income securities when interest rates are incredibly low. As such, these securities can almost be thought of as common stocks with higher yields and a senior position in the capital stack. They are more difficult to obtain than ordinary bonds though, so the fact that this fund is holding a sizable position to them is something that is very nice to see.

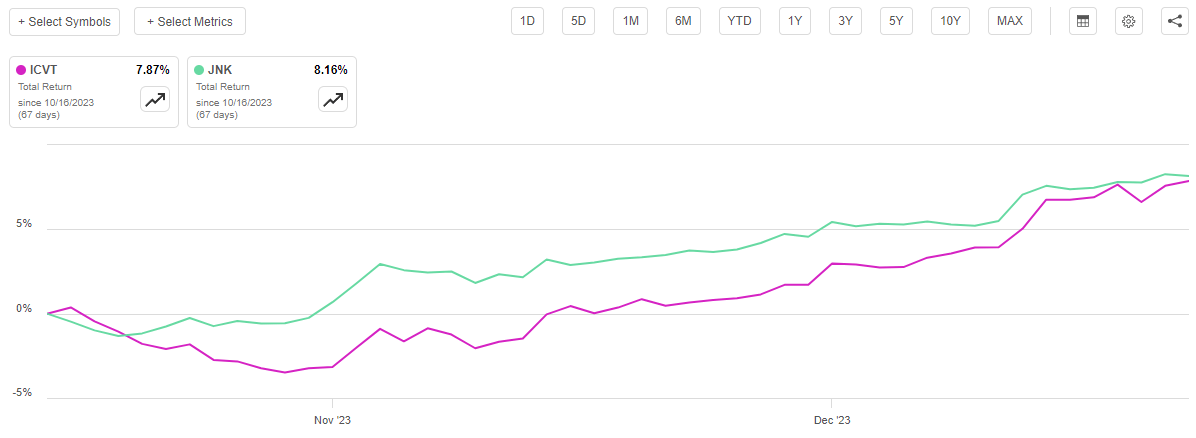

The fund’s allocation to convertible securities is a lot higher than the last time that we discussed it. At the time of the previous article, the fund’s convertible allocation was only 63.74% of its assets. The increase was probably caused by caused by the fund actively increasing its allocation to convertibles. As we can see here, junk bonds have outperformed convertibles since the time that the previous article was published:

{kind=link}

As such, it does not seem likely that the fund’s increased allocation to convertible securities was caused by these securities outperforming the rest of the portfolio. However, the fund only has a 36.00% annual turnover, so it is clearly not doing an excessive amount of trading activity to change its portfolio around very much. That is, after all, a lower turnover than most equity closed-end funds but it is slightly higher than many other fixed-income funds possess.

There might be some reasons for the fund to shift its allocation towards convertible securities. As I noted in a previous article , convertible securities are frequently issued by companies that have difficulty obtaining financing at a reasonable price. This may be due to the fact that they are start-ups with little or no revenue or are in an industry that is distressed. For example, Tesla ( TSLA ) issued these companies in its early days. Wells Fargo ( WFC ) also issued them during the financial crisis back in 2008 and 2009. The ability to convert these securities into equity can be the carrot that induces investors to purchase the convertible securities. After all, a start-up that enjoys success can deliver enormous capital gains to its stockholders. A company that is experiencing short-term problems (like a bank during the financial crisis) could accomplish the same feat when the problems are resolved. These securities were also popular during the post-pandemic bubble when there was an absurd amount of money flying around for a home and a lot of people were starting up companies or engaging in other risky activities that could have potentially high capital gains if successful. Convertible securities allowed investors to obtain some sort of yield when interest rates were at zero while still benefiting from the potential capital gains.

There are some signs that investors are once again moving money into riskier activities. According to a recent article on Marketplace.org:

Stocks rallied pretty much across the board for big profitable companies, and for the smaller, not-so profitable ones too. Other risky assets – cryptocurrency, for example – have been on the rise as well.

It’s not exactly the meme stock, SPAC, NFT mania of early 2021, but recently, some investors have been buying more stock in certain kinds of companies.

“Technology companies that don’t earn any money. They are profitless,” said Ross Mayfield, an investment strategy analyst at RW Baird.

That is exactly the kind of environment that could be beneficial for convertible securities. After all, if investors are willing to drive up the stock prices of riskier companies that tend to issue these securities, then the conversion feature becomes more valuable. As such, the fund’s managers could be making a smart decision by increasing the exposure to convertible securities. Of course, this is all dependent on the economy achieving a “soft landing,” and there is no guarantee that this will be the case.

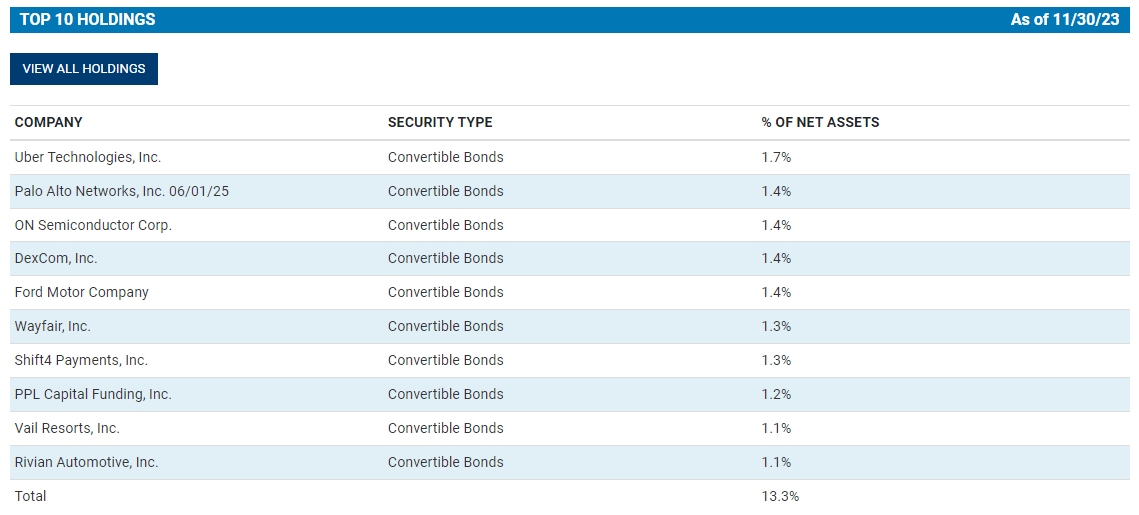

The fact that convertible securities are frequently issued by start-ups and other financially challenged companies is something that might be concerning to some investors. After all, many income-focused investors are retirees or other individuals who do not really want to gamble or risk losing their money. Fortunately, most of the largest positions in this fund are companies that are established and are probably not excessively risky. Here are the largest positions in the fund right now:

{kind=link}

Admittedly, a few of these companies are not the safest things available in the market. UBER Technologies ( UBER ), for example, has had difficulty generating a profit on any sort of consistent basis. We can see this quite simply by looking at the company’s annual net income over the past decade:

{kind=link}

I am still reasonably confident that most people reading this would be more comfortable lending money to a company like UBER than they would to some tiny start-up that nobody has ever heard of.

Rivian Automotive ( RIVN ) is another company in the portfolio that could be riskier than might be desired by more risk-averse investors. This concern could be amplified by the fact that we have seen a few high-profile bankruptcies among electric mobility companies recently. Lordstown Motors ( RIDEQ ) declared bankruptcy back in June and Bird filed for bankruptcy last week. Bird is admittedly not an electric car manufacturer, but that does not mean that its filing will be ignored by investors in the electric vehicle industry. For its part, Rivian has also had some problems this year and Tesla’s Elon Musk even predicted that Rivian will go bankrupt. However, Rivian only accounts for 1.1% of the fund’s portfolio so bankruptcy would not have a huge impact on the fund’s investors. In addition, the fund’s holdings are debt securities, so they still enjoy a certain amount of protection that the common stockholders do not. As such, this position is probably not worth worrying about and it could still deliver a substantial amount of upside if Rivian recovers and becomes successful.

Leverage

As is the case with most closed-end funds, the Calamos Convertible & High Income Fund employs leverage as a method of boosting the effective yield and total return that it receives from the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase convertible securities and high-yield bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

It is important to note though that this strategy is not as effective today with interest rates at 6% as it was two years ago when interest rates were at 0%. This is because the higher borrowing costs have greatly reduced the difference between the rate at which the fund borrows and the yield that it can get from the assets in the portfolio.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive amount of risk. I do not generally like to see a fund’s assets exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Calamos Convertible & High Income Fund has leveraged assets comprising 37.19% of its portfolio. This is a much lower level of leverage than the 39.32% that the fund had the last time that we discussed it. This is a very good sign, as it indicates that the fund has not been increasing its leverage as the market has improved.

As we can see here, the fund’s net asset value is up 8.90% since the last time that we discussed it:

{kind=link}

This is the reason why the fund’s leverage has decreased over the period. Basically, the portfolio has gotten bigger, but the fund’s leverage stayed the same. This naturally means that the borrowed money is a smaller percentage of the overall portfolio.

It is a very good sign that the fund has been keeping its leverage stable as the value of its assets increases. If the fund did otherwise, it would represent a risk to investors since it could blow up the fund in the event of a market correction. This fund is not doing that, but it does still have a bit higher leverage than we really want to see. With that said funds that invest in debt securities like this one can usually carry a higher level of leverage than equity closed-end funds because the assets are less volatile. There are plenty of other debt funds with similar levels of leverage to this one, so it is not ridiculously out of line with its peers. When all of this is considered, the fund’s leverage appears to be acceptable, but we definitely do not want it to borrow any more money.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Calamos Convertible & High Income Fund is to provide its investors with a high level of total return. In order to accomplish this objective, the fund invests its assets primarily in convertible securities and junk bonds. These instruments primarily provide their total return in the form of direct payments to the investors, although convertible securities can also deliver capital gains if they are converted into common stock. In today’s environment, the yields on most debt securities are quite attractive so this should provide the fund with a reasonable level of income as a percentage of its portfolio size. This fund takes things a step further by borrowing money and using that money to purchase more bonds. This provides it with a higher level of income than it could achieve solely by relying on its equity capital. The fund adds any capital gains that it manages to realize to this pool of money and then pays it out to its shareholders, net of its own expenses. We can expect that this business model would give the fund a fairly high yield.

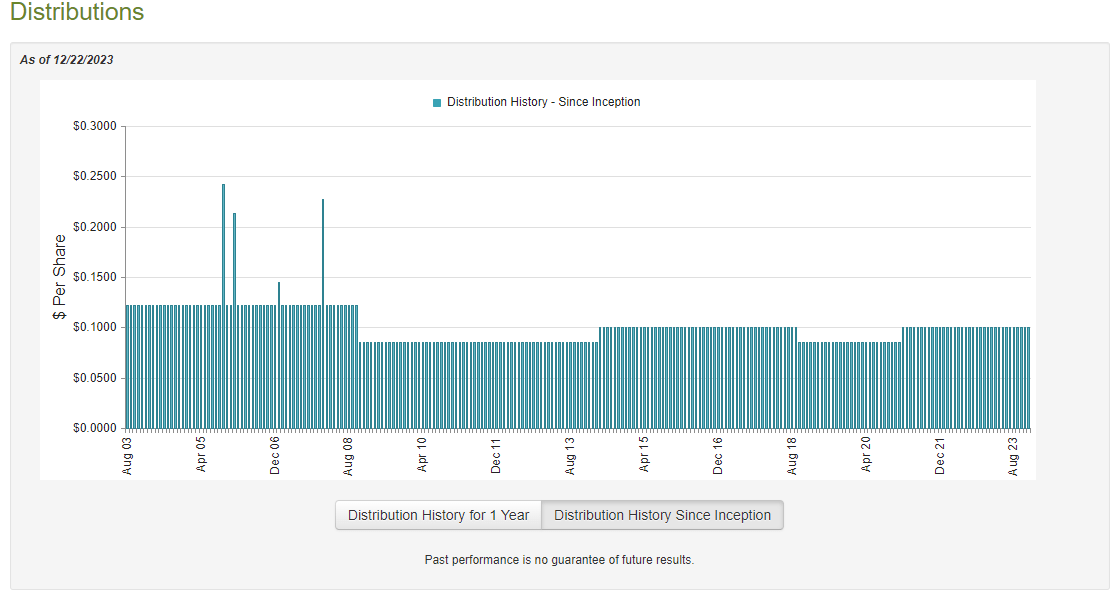

This is certainly the case, as the Calamos Convertible & High Income Fund pays a monthly distribution of $0.10 per share ($1.20 per share annually), which gives it a 10.10% yield at the current price. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years:

{kind=link}

As we can see here, the fund has had to change its distribution quite a few times over its lifetime. However, this is one of the few debt funds that did not cut the payout following the sharp reversion of monetary policy in 2022. That event caused most funds that are heavily invested in fixed-rate debt or equities to take substantial losses. In fact, about the only funds that did not take losses during that year are the ones that invested heavily in floating-rate securities. As we saw earlier, this fund does not have significant exposure to those securities. The fact that this one did not have to cut the payout like other convertible funds, such as the Virtus ones, is something that we should investigate. This might be a sign that the fund is paying out more than it has been able to earn from its investments, which is destructive to net asset value and not sustainable over any sort of extended period.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, this report will not include any information about the fund’s performance over the past eight months. This is quite disappointing, as the market has been quite volatile over the intervening period, and this could have had a very significant impact on its portfolio. For example, the risk-on trade was pretty strong throughout the first half of this year but reversed in mid-July. It reversed again around mid-October and the market started gaining traction as long-term interest rates dropped. The fund almost certainly had some opportunity to earn trading profits during both of the periods of strength, but likely took losses over the summer while long-term interest rates were rising, and both bond and stock prices were falling. This report will not include any information about the fund’s performance during any of these periods.

During the six-month period, the Calamos Convertible & High Income Fund received $16,723,953 in interest and $3,203,958 in dividends from the investments in its portfolio. However, some of this interest was considered to be amortization of principal so it is not considered to be investment income for tax or accounting purposes. As such, the fund reported a total investment income of $14,850,520 over the period. This was not enough to cover its expenses, and the fund reported a net investment loss of $1,500,710 during the period. At first glance, this is likely to be concerning as the fund obviously did not have sufficient net investment income to cover any distributions. This is a problem for a debt fund, as we normally like funds that invest primarily in debt securities to be able to completely cover their distributions out of net investment income. Obviously, there is no chance that this one managed to accomplish that due to its expenses exceeding its investment income.

However, there are other methods through which the fund can obtain money to offset the net investment loss and cover its distributions. For example, it might have been able to accomplish this task through the realization of gains from the conversion of some of its securities into common stock with embedded gains. The fund also might have been able to exploit the appreciation in bond prices that comes with declining long-term interest rates.

Fortunately, the fund did enjoy a certain amount of success in this area during the period. It reported net realized gains of $54,719,793 that were partially offset by $31,303,100 net unrealized losses. Technically, that was not enough to fully cover the $45,482,406 that the fund paid out in distributions, but this does not tell the whole story because the only reason that the fund failed to fully cover the distribution is because of the unrealized capital losses. As everyone reading this is well aware, unrealized losses can be erased the moment the market turns favorable again. The fund’s net realized gains were sufficient to cover the distribution and the net investment loss. That is the most important thing and the fund’s financial performance was acceptable during the period.

The fund has apparently continued to deliver an acceptable performance since the end date of the most recent financial report. As we can see here, the fund’s net asset value per share is up 2.57% since May 1, 2023:

{kind=link}

This strongly suggests that the fund has been able to fully cover all of the distributions that it has paid out since the close of the period. As such, it does not appear that the distributions are destructive to its net asset value right now. We probably do not have to worry about a near-term distribution cut.

Valuation

As of December 22, 2023 (the most recent date for which data is available as of the time of writing), the Calamos Convertible & High Income Fund has a net asset value of $10.77 per share, but the shares currently trade for $11.88 each. That gives the fund’s shares a 10.31% premium on net asset value at the current price. This is a better price than the 11.63% premium that the shares have had on average over the past month, but that is still an enormous premium to pay for any fund. This premium is perhaps the biggest problem with this fund, as it weakens what would otherwise be a very strong thesis.

Conclusion

In conclusion, convertible securities can be very good holdings for income-focused investors as they provide a respectable level of income and capital gains potential. The capital gains potential is far better than we would ordinarily have by investing in fixed-income securities. This fund appears to be one of the better funds that focuses on these securities, but that comes at a price as it trades at an enormous premium to net asset value. This premium is large enough to remove any interest in the fund by more value-oriented investors, which is unsurprising.

Calamos Convertible & High Income Fund does still boast a reasonably attractive yield that appears to be fully covered, though. There are certainly some risks here, including the fact that the market may be disappointed if the Federal Reserve does not cut interest rates sufficiently next year, but this fund may be worth picking up if it ever trades at a more reasonable price.

For further details see:

CHY: This Convertible Fund Could Be Worth Picking Up If The Price Improves