TSLA - CHY: Upside Potential Fixed-Income Stability And Interest Rate Protection

2023-08-03 16:29:00 ET

Summary

- The high inflation rate in the U.S. is increasing the cost of living and reducing real median weekly earnings.

- People are resorting to desperate measures to cut expenses due to the rising prices of necessities like food, shelter, and energy.

- The Calamos Convertible & High Income Fund offers a 10.53% distribution yield, but investors should be cautious about the fund's ability to sustain its high yield and its premium valuation.

- The CHY closed-end fund is more heavily invested in convertible securities than many comparable funds, which improves its risk profile somewhat due to the conversion feature.

- The fund provides more capital gains potential than most fixed-income funds, but still offers the inherent protection provided by these securities.

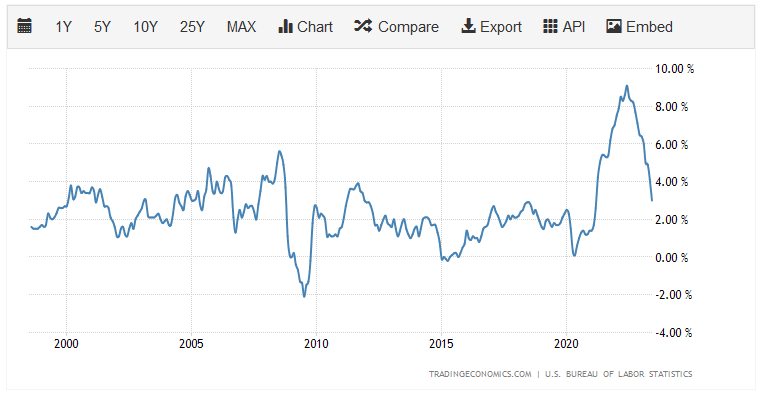

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high inflation rate and the impact that it has had on the cost of living. This is evidenced by the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average person in the United States. As we can clearly see here, over the past two years or so, this index has been increasing at the most rapid pace that it has experienced over the past twenty-five years:

{kind=link}

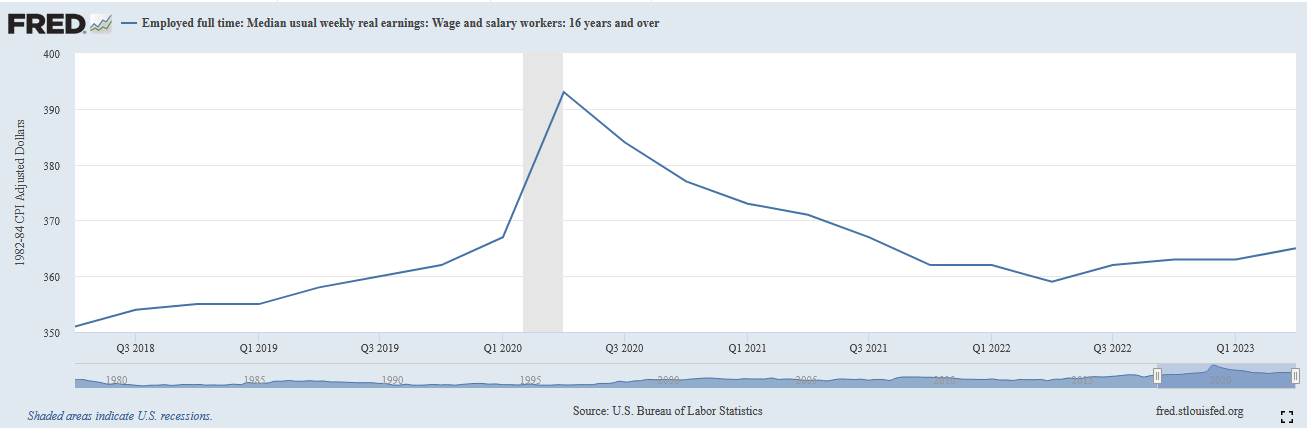

This has had a devastating effect on the average person as wages have failed to keep up with the rising price levels. As can be clearly seen here, real median usual weekly earnings have fallen quite a bit since 2020:

{kind=link}

Thus, people naturally have less money available to spend on purchasing things, which is a very real problem because inflation has been heavily concentrated around food, shelter, and energy. These are necessities that cannot be easily forgone. As such, people have been resorting to desperate measures to cut expenses wherever they can, as I illustrated in a recent blog post .

As investors, we are certainly not immune to this. After all, we require money to purchase food, pay our bills, and perhaps allow us to enjoy the occasional luxury. All of these things have become much more expensive over the past few years so naturally we need more income than we would have in the past. Fortunately, we have the ability to put our money to work for us earning an income and do not necessarily need to resort to some of the extreme measures that other people are forced to.

One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed in the financial media and many investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would like to have in order to make an informed investment decision. This is a shame because these funds offer certain advantages over ordinary open-ended and exchange-traded funds. In particular, they have the ability to employ certain strategies that boost their yields well beyond those of any of the underlying assets.

In this article, we will discuss the Calamos Convertible & High Income Fund ( CHY ), which is one closed-end fund that can be used by investors that are actively seeking an income. This fund currently boasts a 10.53% distribution yield, which is easily enough to attract the eye of anyone that is seeking to receive a high level of income. Unfortunately, any time that a fund manages to achieve a distribution yield that high, it could be a sign that the market expects that the fund will soon have to cut its payout. As such, this is something that we will want to pay special attention to over the course of this article.

Let us investigate and see if the Calamos Convertible & High Income Fund could be a worthy addition to your portfolio today.

About The Fund

According to the fund's webpage , the Calamos Convertible & High Income Fund has the objective of providing its investors with a high level of total return. This is a bit surprising when we consider the name of the fund. After all, the name of the fund sounds like this is a closed-end fund that invests in a combination of convertible bonds and junk bonds. That is the case, but the fund shows a marked preference for convertible securities. As of the time of writing, 66.96% of the fund's assets are invested in convertible securities. This is clearly shown here:

Calamos

The convertible securities add a bit of a twist here, and explain the preference for total return. A convertible bond is simply a bond that can be converted into equity in the issuing company after certain conditions are met. Thus, it basically provides both the safety and income potential of a bond combined with the upside potential of common stock. These securities are frequently issued by start-ups or similar companies that do not have the cash flow to obtain regular debt financing but may have the potential for substantial returns a few years down the road.

For example, Tesla ( TSLA ) issued securities like this back in its early days. I do not need to state how well investors in the common stock of that company have done over the past ten years or so. The fact that the fund is primarily invested in these securities explains the focus on total return as opposed to the current income that we would ordinarily see with a debt fund.

It is also worth mentioning that the Calamos Convertible & High Income Fund is one of the few funds in the market that is weighted towards convertible securities. Many of the other closed-end funds that invest in these securities, such as the Advent Convertible & Income Fund ( AVK ), only have around 30% of their total assets invested in convertibles. Thus, someone who has a real desire to include these securities in their portfolio may prefer the Calamos Convertible & High Income Fund over some of its closed-end fund peers.

As just mentioned, convertible securities are frequently issued by start-up companies that have limited cash flow and so might not be able to obtain debt financing at a reasonable cost. There are few sectors that are more well-known for being start-ups than technology. As might be expected then, the largest individual sector held in the portfolio of the Calamos Convertible & Income Fund is the technology sector. We can see this quite clearly here:

Calamos

Interestingly, this is less than the allocation to technology in the broader market. As of the time of writing, the S&P 500 Index (SP500) has a 28.27% weighting to the information technology. This is actually rather nice to see, since technology is more than double the allocation of the sector largest sector in the market (healthcare), so this fund actually appears to be more diversified than the S&P 500 Index. This fund is actually slightly overweighted to healthcare than the S&P 500 Index, which could actually be a good thing. As is the case with technology start-ups, healthcare start-ups have the potential to be incredibly profitable if they are successful. That is especially true when we consider the aging population in the United States, Europe, and Japan. The fact that this fund is slightly overweighted to this sector could thus provide the fund with considerable upside following the conversion of a convertible bond to common equity.

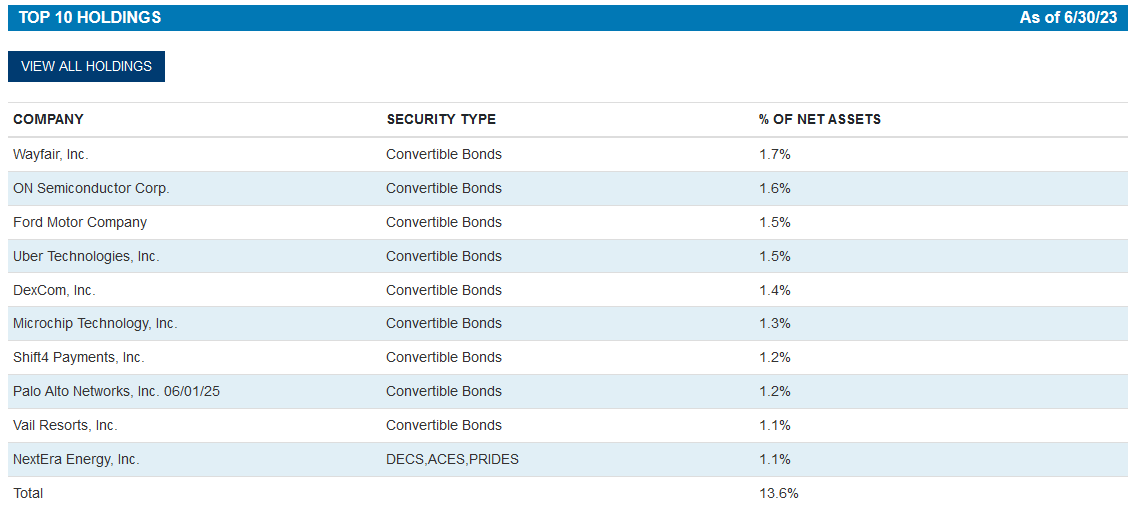

As might be expected, the companies that comprise the largest positions of this fund are going to be somewhat different than we would normally see in a fund whose top two sector allocations are technology and healthcare. Here they are:

{kind=link}

We actually do see quite a few companies on this list that are relatively young. For example, online marketplace Wayfair ( W ) was founded in 2002, and Uber Technologies ( UBER ) is certainly a fairly young company as it only had its initial public offering in 2019. In fact, of the companies on this list, only Ford Motor Company ( F ) and NextEra Energy ( NEE ) are more than thirty years old. Ford has had some debt problems in the past, so it is unsurprising that it ended up issuing convertible bonds. The only company on here that is surprising as a convertible bond issuer is NextEra Energy, as that company actually has a fairly low net debt-to-equity ratio and enjoys the stable cash flows that are characteristic of any utility company.

As regular readers on the topic of closed-end funds are likely well aware, I do not typically like to see any single position in a fund account for more than 5% of the fund's total assets. That is because this is approximately the level at which a given asset begins to expose the fund as a whole to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any company possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio then this risk will not be completely eliminated. As such, the concern is that some event will occur that causes the price of a given asset to decline when the market does not. In such an event, an asset that accounts for too much of a given portfolio could end up dragging the entire fund down with it.

As we can see above, though, that does not appear to be a risk that we need to worry about here as there is no individual asset that accounts for such an outsized proportion of the fund. As such, we should not really need to worry about idiosyncratic risk with this fund. It appears to be sufficiently diversified to protect us against unique risks to any individual company.

Leverage

In the introduction to this article, I stated that closed-end funds like the Calamos Convertible & High Income Fund have the ability to employ certain strategies that allow them to boost their yields well beyond that of any of the underlying assets in the portfolio. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase convertible securities and high-yield bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

t is important to note, though, that this strategy is not as effective today with interest rates at 6% as it was eighteen months ago when interest rates were 0%. This is because the higher borrowing costs have greatly reduced the difference between the rate that the fund borrows and the yield that it can get from the assets in the portfolio.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

Unfortunately, this fund fails that requirement as its levered assets comprise 36.97% of the portfolio today. This is probably okay, considering that bonds tend to be less volatile than stocks, allowing funds that invest primarily in debt securities to carry somewhat higher leverage than common equity funds. However, it is still important to keep the fund's leverage in mind as this fund will be somewhat more volatile in the market than a similar fund that does not employ leverage.

Distribution Analysis

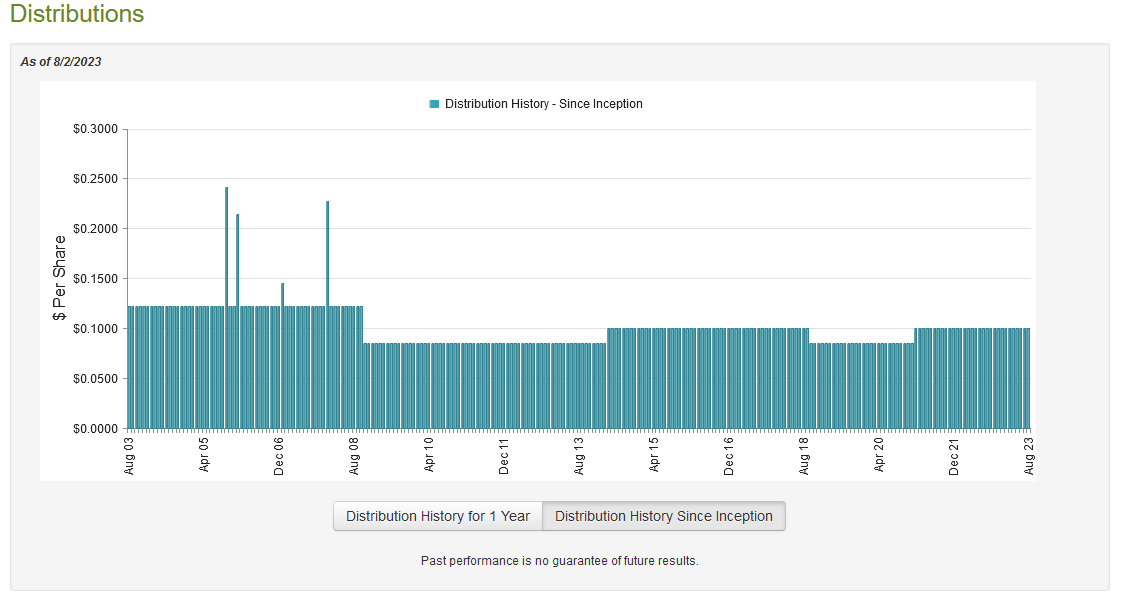

As stated earlier in this article, the primary objective of the Calamos Convertible & High Income Fund is to provide its investors with a high level of total return. However, in order to achieve this objective, the fund invests primarily in convertible debt and high-yield bonds, which both deliver their returns primarily through direct payments to the investors. This fund collects those payments, applies a layer of leverage to boost the effective yield of the portfolio, and then pays its investment returns out to its shareholders. As such, we can assume that this fund should have a very high yield itself. This is certainly the case as the Calamos Convertible & High Income Fund pays a monthly distribution of $0.10 per share ($1.20 per share annually), which gives it a 10.53% yield at the current price. The fund has been more consistent about its distribution over time than we might expect, but it has still exhibited some variation:

{kind=link}

The fund has generally been more resistant to changes in interest rates than many other fixed-income funds. This is somewhat explainable by the fact that the majority of this fund's assets are invested in convertible securities. Convertible securities are not as affected by interest rates as ordinary bonds due to the conversion feature. Due to this feature, a convertible security might rise in price alongside the issuing company's common stock during bull markets regardless of interest rate movements.

However, it is still somewhat surprising that the fund has been able to maintain the consistency that it has since stocks have generally moved inversely to interest rates ever since the financial crisis fifteen years ago. Thus, we should investigate the fund's ability to cover its distribution in order to determine how sustainable it is likely to be. After all, we do not want to be the victims of a distribution cut since that would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we do have a fairly recent document that we can consult for that purpose. The fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, it should give us a pretty good idea of how well the fund navigated the intense market turbulence last year as well as the partial recovery that we experienced during the first few months of this year.

During the six-month period, the Calamos Convertible & High Income Fund received $16,723,953 in interest and $3,203,958 in dividends from the securities in its portfolio. However, some of this money was considered to be a payment on amortizing debt and not investment income. Thus, the fund only reported total investment income of $14,850,520 over the period. The fund paid its expenses out of this amount, which left it with a negative $1,500,710 available for shareholders. Obviously, this is nowhere near to enough to pay any distributions but the fund still paid out $45,482,406 in distributions over the period.

At first glance, this is likely to be concerning as the fund clearly failed to cover its distributions out of net investment income. This is concerning for a fixed-income fund as we usually like these securities to cover their distributions out of net investment income.

However, the fund does have other methods that can be employed to obtain the money that it needs to cover the distributions. For example, it might have been able to generate some capital gains that can be paid out. It did have modest success at accomplishing this, as the fund reported net realized gains of $54,719,793 during the period but these were partially offset by $31,303,100 net unrealized losses. Overall, the fund's assets declined by $19,732,392 over the period after accounting for all inflows and outflows. This is disappointing, but the net realized gains were actually enough to cover the distributions and the net investment loss with quite a bit of money left over. As such, this distribution could be sustainable depending on how well the fund's portfolio manages to perform going forward.

I will admit that I am much less concerned about this fund than I have been about other fixed-income funds over the past twelve months. Income-focused investors will probably be reasonably happy with this fund.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Calamos Convertible & High Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of August 2, 2023 (the most recent date for which data is available as of the time of writing), the Calamos Convertible & High Income Fund has a net asset value of $10.87 per share but the shares current trade for $11.36 each. This gives the fund's shares a 4.51% premium to the net asset value. This is higher than the 3.60% premium that the shares have possessed on average over the past month.

I will admit, too, that I do not like to buy any fund at a premium to net asset value. As such, it may make sense to wait and see if this fund can be obtained at a more reasonable price before purchasing shares.

Conclusion

In conclusion, the Calamos Convertible & High Income Fund could offer a way to gain exposure to the upside potential of common equities while still enjoying the safety of fixed-income securities. This is due to the fact that convertible securities in general are designed to deliver investors the best of both worlds. The fund should also enjoy a certain amount of insulation against interest-rate risk due to the convertible feature present on the majority of the assets in the fund's portfolio. This is a good thing, because there is a fairly high probability that the Federal Reserve will raise rates again before the end of this year.

The Calamos Convertible & High Income Fund does boast a suitably high yield, but it appears capable of sustaining it, which is also much better than a lot of other fixed-income funds. The big problem here is that the fund trades at a fairly high price relative to the actual intrinsic value of its shares, so anyone paying today is paying more than the liquidation value. This is not a desirable situation, but it is definitely worth buying the fund's shares if they ever switch over to a discount.

For further details see:

CHY: Upside Potential, Fixed-Income Stability, And Interest Rate Protection