ELV - Cigna: Do Not Miss The Moment

2023-04-06 13:21:48 ET

Summary

- The US managed care industry has strong tailwinds due to population growth, aging, and new care developments.

- The biggest risk for the industry is the introduction of the single-payer system with an estimated probability of 1-2% per election cycle.

- Cigna is currently trading significantly below its historical multiples and rather cheap on an absolute basis.

- Cigna uses its strong free cash flow primarily for buybacks and shareholders benefit from periods of stock weakness.

- The current management is effective and aligned. Since 2009 when it was installed, the stock has grown at about 19% CAGR.

The Cigna Group ( CI ) belongs to the managed care industry and together with its nationwide public peers (UnitedHealth Group ( UNH ), Aetna (a segment of CVS) ( CVS ), Humana ( HUM ), Elevance Health ( ELV ), Centene ( CNC )) is trading near the low-end of its 52-week range.

I have held CI and UNH for several years. Both have easily beaten the index and belong to my better performers even after the recent drop.

I wish I had bought them earlier!

A Big Picture

A lot of people hate managed care and the stocks of managed care companies by association. In my old article about Cigna, I tried to explain this phenomenon which triggered a heated discussion.

This is exacerbated by the industry complexity with multiple actors, conflicting interests, and many external developments (such as lawsuits and countless regulations on every level) that create buzz and seem important but impede understanding of certain basic facts.

Every year, the total cost of medical care goes up worldwide and the US is no exception. One reason for this process is higher longevity. Another is gradual population growth. Still, another is the unstoppable development of new treatments, diagnostics, and medications that mostly do not cancel the old ones. For example, MRI does not cancel X-rays, and both methods must remain available. All three reasons are objective and not caused by specific policies or bad actors.

Currently, US healthcare costs represent ~18% of GDP compared with 5% of a much smaller GDP in 1960.

Managed care is a clear beneficiary of healthcare costs increase as it pockets a certain fraction of the total costs. One may not like it but without these big health insurers, it is impossible to administer care rationally. The only threat to the industry is a single-payer system when one government-run bureaucracy replaces several private bureaucracies.

Simplistically, it is a binary situation: without the single-payer system, the managed care industry - in total and long-term - is destined to be rather successful. At-scale new entrants are quite unlikely and the existing big actors will remain toll-takers of US healthcare.

From time to time, due to strong statements from Congress members or election campaigns, various government actions on federal or state levels, and high-profile lawsuits, health insurers drop in sync. And this is the time to buy them as long as one is more or less confident that the single-payer system is not going to take over.

For it to happen, Democrats should control the executive branch and both chambers of Congress. But this is not enough. The progressive wing of the Democratic party should also prevail over the conservative wing. On a very crude level, we can assume that the chances of Democrats winning against Republicans and Progressives controlling Democratic policies are 1/2 each in presidential and congressional elections. In this case, the chances of Progressives controlling both chambers of Congress and the executive branch simultaneously are 1/64 per election cycle.

Even this is insufficient to introduce the single-payer system (or Medicare for all, M4A) as conservative Democrats may align with Republicans instead of Progressives. Despite their hate of medical insurers, doctors are also likely to be against the single-payer system and will mobilize their lobbying resources accordingly.

As a result, we estimate the chances of M4A replacing private managed care as 1-2% per election cycle at maximum. Granted, it will be a catastrophic event for the industry. However, the chances of this development are sufficiently small to justify holding health insurers in a well-diversified portfolio.

Cigna's position in the industry

Stepping down from the single-payer threat, we see a motley system of healthcare market segments and various actors interacting in a complicated way. The kernel of the system consists of medical insurance spread between Medicare, Medicaid, employer-obtained insurance, and individual (on- and off- ACA exchanges) insurance (about 9% of the population lacks coverage). Please note that managed care companies often do not underwrite medical risks directly but only administer plans insured by government, non-profit, or corporate institutions.

Managed care companies also participate in businesses adjacent to the medical insurance consisting either of care delivery assets (such as doctors' groups or pharmacies) or care facilitating assets (such as pharmacy benefit management - PBM). Often, medical insurers can direct or at least nudge patients to care delivery assets within the same company creating accretive synergies.

At almost any moment, several external processes are occurring that may significantly affect certain segments of the managed care industry. Since these processes include various lawsuits and government acts, their outcomes and effects on the industry are difficult to predict (for example, at the time of writing, these processes include changes in Medicare Advantage payment rates, and resuming of Medicaid eligibility redeterminations after Covid).

The unique complexity and challenges of the industry make diversification quite important for the players. When we say "diversification" we mean both diversification across different types of insurance and advantageous split between insurance and non-insurance parts of the business.

In this regard, UNH is by far the biggest and best company. However, it is always expensive except for the moments when the M4A movement is particularly strong. While well diversified, Cigna is a much smaller company. However, sometimes it is trading undeservedly cheap and always generates tremendous free cash flow that is mostly returned to shareholders in the form of decent dividends and strong buybacks.

David Cordani has been Cigna's CEO since 2009. His effectiveness can be easily judged by numbers: at the end of 2009, CI was trading at $34 while at the end of 2022, it was trading at $331. It represents 19% CAGR not counting dividends which became material only in 2021. Mr. Cordani owns ~1.2M shares with a market value of more than $312M. Other officers and board members combined own half of what Mr. Cordani owns and I would like to see the latter figure higher.

The company consists of two segments - Cigna Healthcare (a medical insurer) and Evernorth Health Services which includes PBM, specialty pharmacy Accredo, and Evernorth Care - a portfolio of various health services including analytics tools, telemedicine, and provider networks. While PBM is the biggest part of Evernorth, Accredo and Evernorth Care are growing faster and arguably have better synergies with Cigna Healthcare.

In its turn, Cigna Healthcare includes US Commercial, US Government, and International Health. While US Commercial is the biggest part of Cigna Healthcare, US Government provides a major growth opportunity via increasing Medicare Advantage coverage.

Valuations

Once one understands the complex industry landscape and moving parts within the company, the numerical analysis is straightforward.

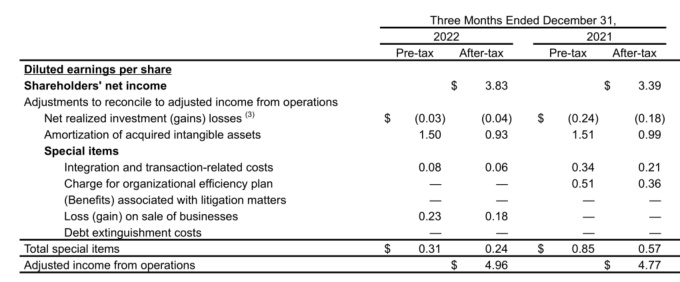

Cigna presents two main results: EPS and Adjusted EPS. Adjustments include adding back amortization of intangible assets that are on Cigna's balance sheet due to acquisitions; adding/deducting capital losses/gains associated with business dispositions; adding/deducting losses/gains of the equities within the company's investment portfolio; deducting certain special non-recurring items. I do not necessarily agree with the latter but they are sufficiently small to discuss them. All other adjustments make perfect sense. To better understand the adjustments I will present a table from Cigna's latest supplemental filings:

{kind=link}

For our purposes, adj. EPS (or adjusted income from operations in the table) is the most important metric to gauge results. I am also monitoring free cash flow per share but it closely follows adj. EPS as the company's capex is low.

Historically, CI has been trading at the average P/adj. EPS ~ 15.0 with 4.4 standard error. However, due to the various industry events and processes with unclear outcomes and effects that I described in the previous sections, at times Cigna becomes rather cheap.

For example, adj. EPS for 2022 was $23.24 and Cigna forecasts this number to be above $24.60 in 2023. Currently, CI is trading at ~$263 corresponding to P/Adj. EPS of 11.3 and 10.7 respectively. This is cheap not only relative to the company's historic valuations but also to its adj. EPS growth rate of close to 19% per year (similar to stock returns). At normal P/Adj. EPS ratio of 15, CI will be worth close to 15*24.60 = $369 in early 2024.

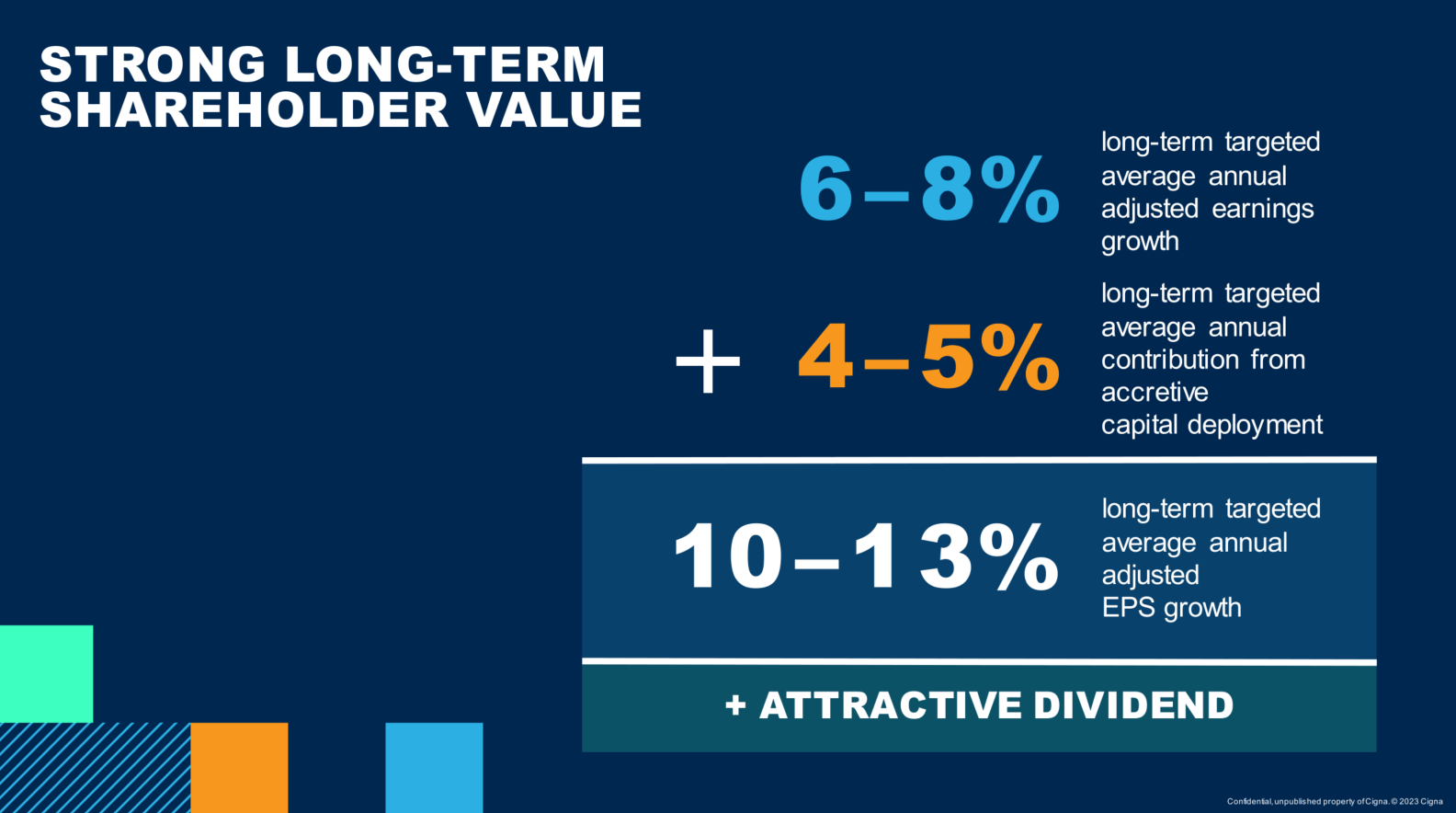

Cigna's forecast is quite modest compared to its historic results:

{kind=link}

The 4-5% growth on the slide reflects mostly buybacks. Adding a 2% dividend produces 12-15% forecasted annual returns. No matter whether one is based on the company's forecast or its historic results, the current valuations are low and the industry's long-term tailwinds remain unabated.

I have already mentioned that Cigna repurchases plenty of its stock. In 2019, Cigna acquired Express Scripts issuing shares for payment. It was a transformational deal as Express Scripts became the platform for creating Evernorth. At the end of 2019, Cigna had ~380M shares. This number now is only ~300M. During several years, the company has repurchased almost a quarter of its shares and does not stop here. This activity becomes particularly accretive when CI is trading weakly as it is now.

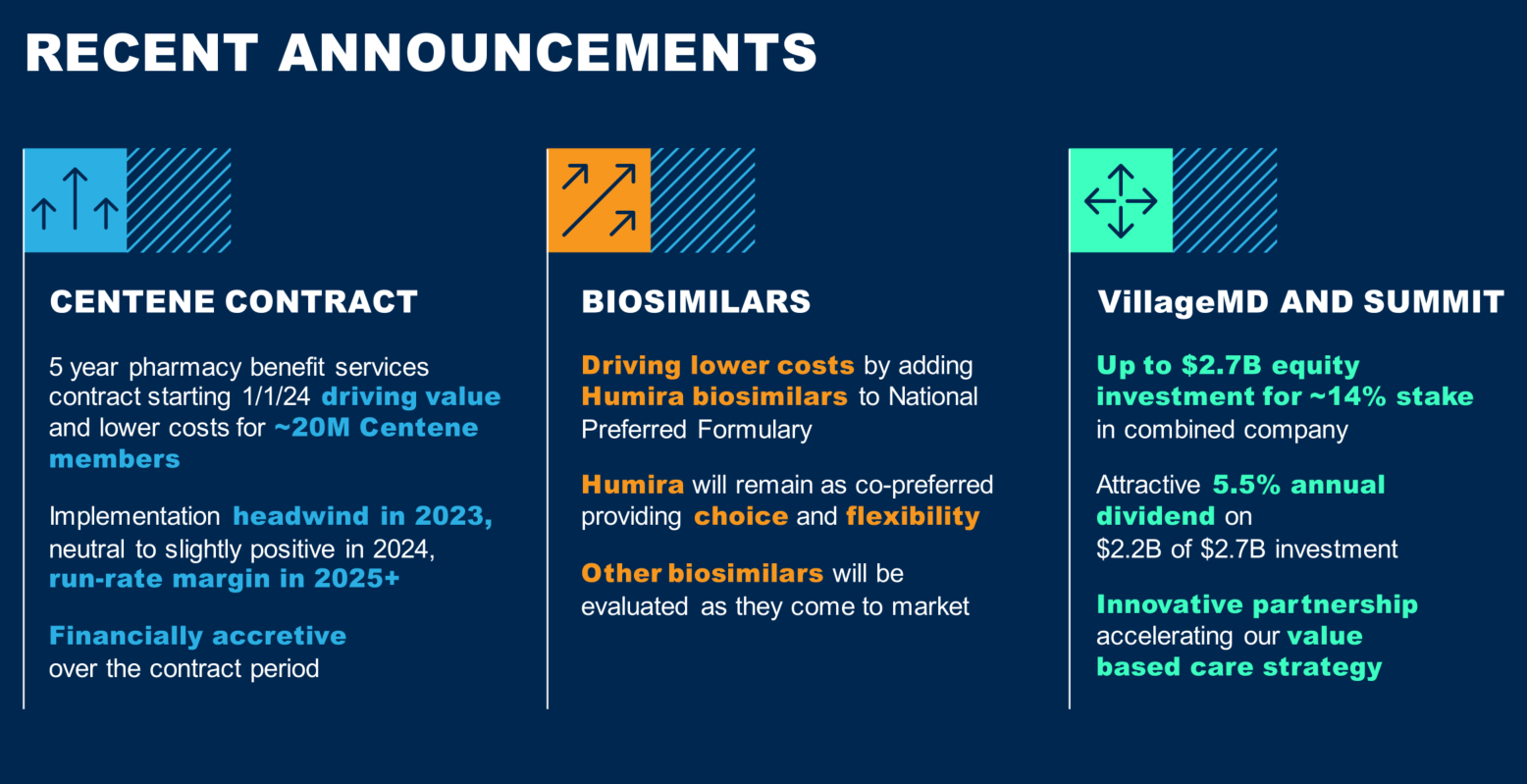

The immediate future seems rather bright too. Some of the recent developments are illustrated on the following slide:

{kind=link}

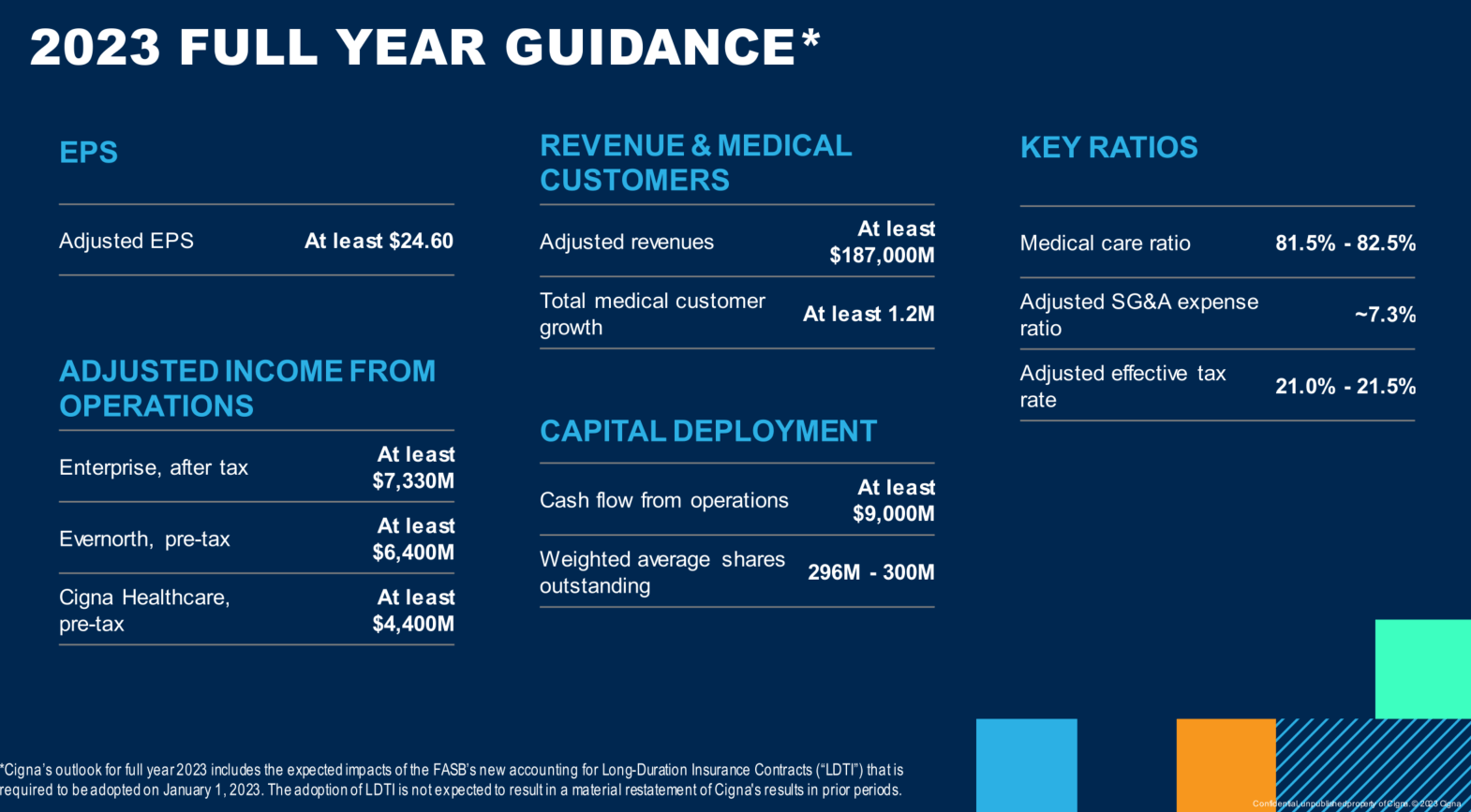

Below is the company's full 2023 forecast:

{kind=link}

Besides buybacks, the company has several other financial levers to play with. The two most obvious are the reduction of the SG&A expense ratio via cost management and scaling up and increasing synergies between Cigna Healthcare and Evernorth. Every year, Cigna tends to increase the number of its medical customers and will try to direct some of them toward Evernorth's services.

Conclusion

If one is comfortable with the single-payer risk, Cigna is likely to become a good investment. Investors in Cigna should be prepared to tolerate and use its volatility. The last time Cigna was trading that cheap was about 1.5 years ago and the period of weakness lasted close to half a year. The stock has been in decline since the end of 2022 and the period of weakness may or may not be over. It only partially depends on the company's results. Due to never-stopping buybacks, such weakness is the most profitable development for investors. I am always looking forward to these periods of weakness and use them to add shares.

For further details see:

Cigna: Do Not Miss The Moment