META - CII: Covered Call Fund Helping Support Distribution In A Down Market

2023-03-26 03:42:45 ET

Summary

- CII performed relatively well through the last year despite all the volatility.

- Covered call writing contributed to a sizeable portion of the fund's distribution.

- The downside here is that investors seem to have noticed and pushed CII to a historically narrow discount.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on March 9th, 2023.

BlackRock Enhanced Capital and Income Fund ( CII ) might have a tech tilt to its portfolio, but it performed better in 2022 than the S&P 500 and Nasdaq Indexes. They paid out a large year-end special, but even despite that, the fund's NAV distribution rate isn't excessive. Thanks to its covered call strategy, that helps contribute capital gains even when equities fall. With both of those factors, the fund's current distribution looks to be sustainable in the current environment.

I've been covering several call-writing funds lately, but it's for a good reason. Not only because the new annual reports are available on a lot of the funds but also because the current environment can make these funds more appealing. They don't operate with borrowings, meaning higher interest rates aren't going to impact leverage costs. Additionally, if one expects the next year or several years to be flat or even down, these funds can continue delivering relatively better results.

Performance for CII has been quite strong since our last update . Due to a narrowing discount since then, that's also helped juice up the results.

CII Performance Since Previous Update (Seeking Alpha)

However, due to that discount narrowing, now isn't presenting as attractive as a time to consider this fund. That's despite the positive characteristics, such as a covered call strategy and sustainable monthly distribution.

The Basics

- 1-Year Z-score: -0.24

- Discount: -3.50%

- Distribution Yield: 6.98%

- Expense Ratio: 0.89%

- Leverage: N/A

- Managed Assets: $801.9 million

- Structure: Perpetual

CII has a simple objective and strategy; it "seeks to provide investors with a combination of current income and capital appreciation" by "investing in a portfolio of equity securities of the U.S. and foreign issuers." They will also "employ a strategy of writing call and put options."

This type of flexibility allows them to really invest wherever they'd like. However, the portfolio tends to overweight the large and mega-cap tech names. That is pretty standard for most straightforward equity funds.

The fund's expense ratio under 1% is rare in the closed-end fund space. While some may point out that ETFs can still charge lower expense ratios, the average expense ratio for an actively managed ETF is 0.70%. So I'd consider the expense ratio quite competitive against even ETF peers. Which, again, tends to be quite rare in the CEF space.

No leverage through borrowings on this fund means they are free from the burdens of leverage costs rapidly rising due to the Fed raising interest rates.

Performance - Positioning And Call-Writing Help CII

The call-writing strategy is slightly defensive, but they were able to provide meaningfully better results than what we saw from the major indexes. CII has a slight tech tilt, and they compare themselves against the Russell 1000 Index, where they also put up strong comparative results.

In fact, when benchmarking against the MSCI USA Call Overwrite Index, the fund was able to outperform in the last year against that too. Clearly, their positioning was also a factor for this outperformance as well as the covered calls.

{kind=link}

Like all good things, some negatives counteract the benefits that need to be considered. That is, over the longer term, these sorts of funds will tend to underperform in bull markets. With such an uncertain market at this time and expectations for a recession on the horizon, a flattish market could be something we see over the next year or even several years.

Some are suggesting that we are in for another "lost decade" for markets. In that case, a covered call fund could be one way to get at least some returns out of equities. Personally, I know I can't predict what the market will do next week or next year, so I stay diversified with a mixture of funds focusing on different strategies.

The downside here is that, like its sister fund, BlackRock Enhanced Equity Dividend Trust ( BDJ ), it would appear that investors have taken notice of their attractiveness. This has come through with the fund's flirting with premiums and historically narrow discounts. That being said, the discount has opened up a touch in the last week or so now. With the bank failures contributing to a more overall volatile period, we often see that being the case with CEFs; they go to wider discounts. Still, it is trading at a level that I would consider it more of a "hold" rather than accumulate at this time.

As CII is near its 10-year high valuation mark, being patient could be an appropriate course of action. On the other hand, for those who already hold a position, we aren't so grossly overvalued that I think we need to stampede for the exits.

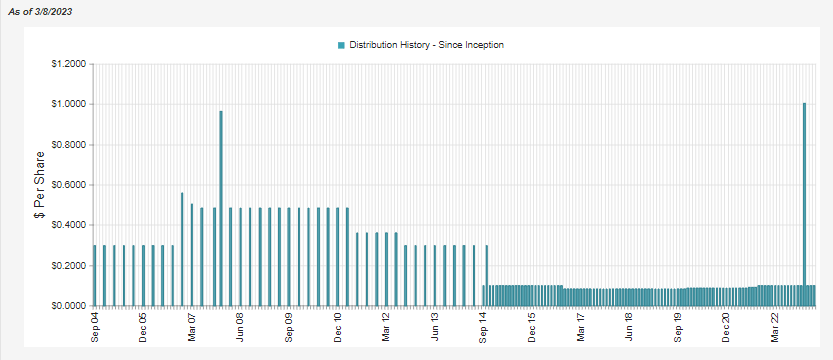

Distribution - Currently Steady And Sustainable

The fund had paid a quarterly distribution and cut it several times after the GFC. They then cut again around 2016 by a bit, but they have since raised the distribution.

{kind=link}

Given the NAV distribution rate of 6.73%, I think we are looking at a fairly sustainable level. That even includes the outsized year-end special of $0.90637 they paid at the end of last year. That was nearly doubling the annualized $1.194 the fund pays out now. Specials are great, but that's a lot of assets being paid out at one time that can sometimes impact the future earnings potential of the fund.

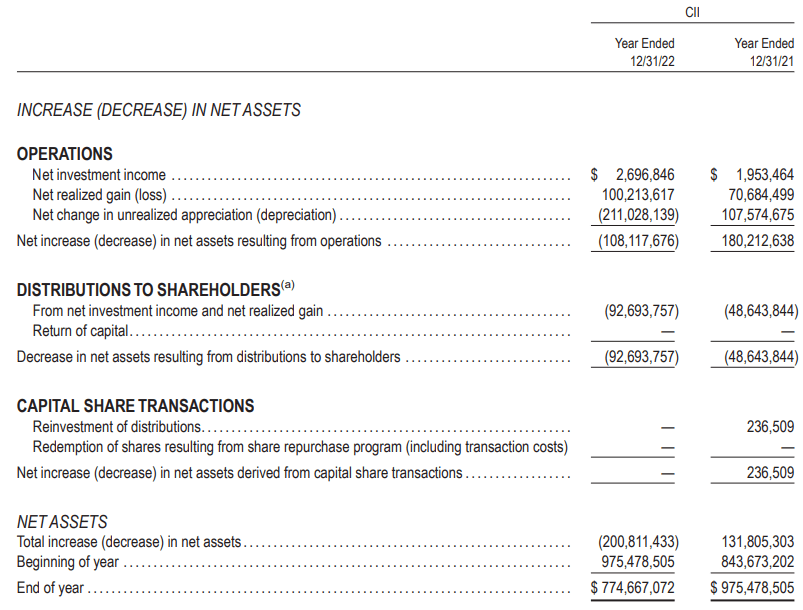

Naturally, with the distribution almost doubling, the distributions paid out to investors in the 2022 year were also doubled. They had to pay out the large year-end special due to realizing significant capital gains throughout the year. Even the realized gains they brought in last year were well in excess of the distribution amount paid out.

{kind=link}

Still, we can see that net investment income covers very little of the distribution. On a per-share basis, they reported an NII of $0.06 for 2022. Although not large on an absolute basis, on a relative basis, that was quite the jump from last year's $0.04. Of course, that's still well short of covering the fund's distribution through income.

While the largest contributor to the fund's realized gains in the past year were underlying investments, a quarter of the gains came via covered call option premiums. Those are capital gains that can be generated even in a down market, as we had in 2022.

{kind=link}

Taking the NII generated plus the options written capital gains isn't enough to cover the distribution entirely. However, it does cover a fair portion of the payout to investors in a given year should they be able to generate the same in the following year. That should help keep the current distribution stable for the foreseeable future.

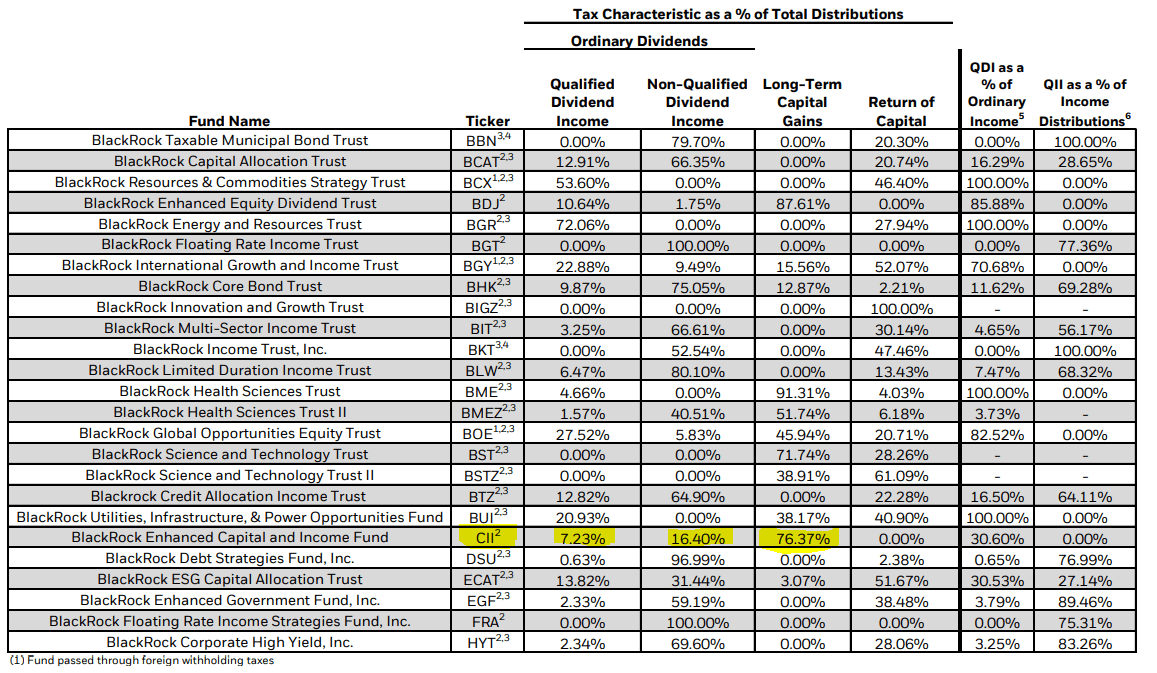

For tax purposes, in 2022 , the largest distribution characterization was assigned as long-term capital gains.

{kind=link}

While that probably appears to make sense given the sizeable year-end long-term capital gain paid out, this is generally the case anyway. As we saw above, income generation in the fund is fairly minimal, and most coverage will come through capital gains. This was also reflected in 2021's tax classifications , where nearly 96% of the fund's distribution was characterized as long-term capital gains.

CII's Portfolio

The fund managers here aren't overly aggressive with buying and selling but aren't sitting around, either. With the covered calls, they are actively managing those positions too. The portfolio turnover rate of the prior year was 32%, up from 27% in 2021 but down from 46% in 2020.

The fund's portfolio comprises primarily U.S.-based companies, representing 93.29% of the portfolio at the end of February 2023. The portfolio is dominated by large/mega-cap positions, as mentioned above. The average market cap for the underlying holdings comes to a monstrous $409.952 billion.

For some perspective, BDJ's portfolio had an average market cap of $102.6 billion for its underlying holdings, and that would be considered skewed to the large-cap side. Of course, these fluctuations change, and when tech had a massive run-up in 2020 and 2021, they were pushed to some fairly elevated levels in terms of their market cap.

Anything over $10 billion is considered large-cap, so holding some of the stocks in the $1 trillion+ club can be outliers to skew the average higher.

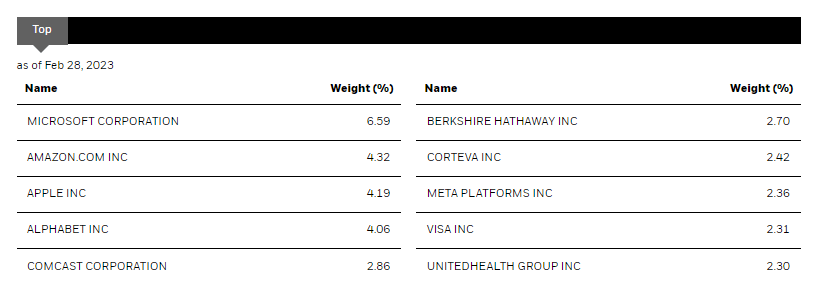

With that, the top ten holdings here will all be names that most people would recognize if they are investors or not. These are also relatively regular names, with most appearing in our last update as well.

{kind=link}

With the mega-cap tech names fully represented here in Microsoft ( MSFT ), Amazon ( AMZN ), Apple ( AAPL ) and Alphabet ( GOOG ), it isn't a surprise that we see the sector weightings tilt towards the tech sector.

We even have Meta Platforms ( META ) make their way as a top holding but at a relatively smaller weighting. Notably, META was not a top ten position in the fall of 2022 for CII. While it was a position then, it was a smaller one. They bumped up the share count meaningfully from 84,339 to 107,439. That being said, during that time, shares of META had also performed well. It would appear they picked up some shares at the right time.

Ycharts

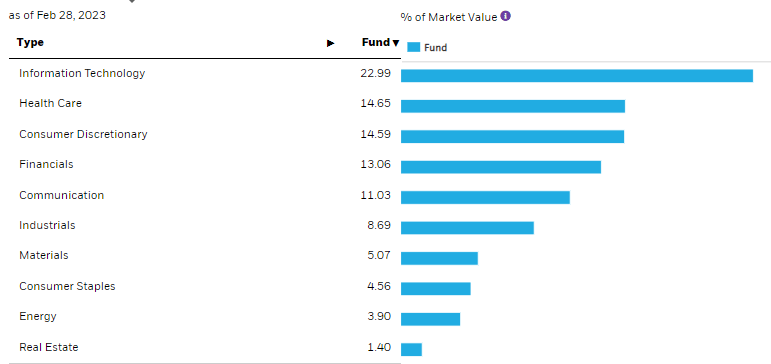

Besides the tech sector being slightly overweight relative to the other sectors represented, one of the benefits I think this fund provides is being fairly diversified.

{kind=link}

Since our last update, the weightings in terms of sectors haven't changed too much. After tech, the sector allocations are fairly grouped up with similar weightings. Therefore, even though we've seen consumer discretionary leapfrogged by healthcare exposure as the second largest weighting now, it wasn't by a commanding weighting change. Consumer discretionary exposure slipped from 14.92% weighting to 14.59%. For healthcare, the weighting went up to 14.65% from 13.50%. These are fairly small weighting changes that can be done through normal fluctuations in the market over time.

Conclusion

CII performed well in 2022 with a volatile market. That would be thanks to the fund's covered call strategy and portfolio positioning. While the performance wasn't positive, it was well ahead of the broader indexes and beat out its benchmarks. A covered call fund and one as diversified as CII could be attractive in the coming year or even years if one thinks we are in for a flattish or continued bumpy ride in the market. However, the downside here is that CII's discount has become quite shallow. A dollar-cost average or having some patience here for a larger discount could pay off.

For further details see:

CII: Covered Call Fund, Helping Support Distribution In A Down Market