DXC - ClearBridge All Cap Value Strategy Q2 2023 Portfolio Manager Commentary

2023-07-12 08:15:00 ET

Summary

- ClearBridge is a leading global asset manager committed to active management. Research-based stock selection guides our investment approach, with our strategies reflecting the highest-conviction ideas of our portfolio managers.

- While economic and fundamental measures are sending mixed signals, odds of a recession have declined, yet the resulting market rally has not flattered value as a style. This improves the set up for the Strategy in the medium term whether we enter a downturn or not.

- Time will tell whether AI aids mega cap tech as a whole or helps to unseat them, but several market indicators point to a much harder road for their outperformance going forward.

- Our analysis continues to highlight compelling opportunities outside of mega caps, and we expect that the eventual rebound in smaller cap stocks will benefit our performance.

By Reed Cassady, Albert Grosman, & Sam Peters

Market Shows Turbulence Below the Surface

Market Update

It is difficult to recall a period with more crosscurrents impacting the global economy, different industries, consumers and financial markets than the current one. The distortions from the COVID-19 pandemic, with large swathes of the economy shut down and reopened in stuttering phases, has made understanding supply and demand versus the true trend line very difficult. Further complicating this analysis is the immense fiscal and monetary stimulus injected into the U.S. economy. It is fair to say that this indeed spurred demand as hoped, but too often into a constrained supply for goods as supply chains struggled and many services industries operated below capacity. This soaring demand against limited supply, both pandemic-related and due to persistent underinvestment in areas like housing and energy, predictably — in hindsight — combined to drive inflation to levels not seen in nearly two generations. With inflation soaring, the Federal Reserve felt compelled to hike interest rates with a ferocity reminiscent of the Volcker era. Mix in a regional bank mini crisis earlier this year, and it’s no wonder that most investors opined that a recession would soon be in the offing.

However, this much anticipated recession has yet to manifest, and recessionary fears have gradually turned into hopes of an economic soft landing. This, combined with investors’ hopes that the Fed may be approaching it rate hike conclusions and surge in the demand for mega cap AI developers helped the Russell 3000 Growth Index to surge ahead of the Russell 3000 Value Index, earning 12.47% and 4.03% respectively. Despite this challenging backdrop for value the ClearBridge All Cap Value Strategy outperformed its Russell 3000 Value Index benchmark for the second quarter by nearly 400 basis points as strong stock selection in sectors such as financials and IT helped to overcome lackluster performance in more defensive sectors, such as healthcare.

Time and again the post-pandemic era has proven to be a cycle like none other, one that eludes easy prediction and defies historical rules of thumb. For example, the 2/10 Treasury yield curve has inverted to the most negative since the early 1980s, a measure that would typically scream looming recession (Exhibit 1).

Exhibit 1: Yield Curve Reminiscent of the 1980s

| As of June 30, 2023. Source: Bloomberg |

Meanwhile, more economically-sensitive homebuilder stocks have vaulted to all-time highs, even as homebuyer affordability saw an unprecedented decline due to a doubling in mortgage rates and rapidly increasing home prices (Exhibits 2 and 3). The data suggests we have not built enough homes and there exists a multiyear supply/demand mismatch that should favor this ecosystem, while at the same time the correction in volumes and prices has proven less severe than feared. Many builders are now forecasting a return to growth in the face of affordability headwinds.

Exhibit 2: Homebuilding Stocks Move Higher…

| As of June 30, 2023. Source: Bloomberg |

Exhibit 3: …While Home Affordability Collapses

| As of June 30, 2023. Source: Bloomberg, National Association of Realtors. |

Given the strong labor market and excess savings accumulated during the pandemic, consumers are in good shape and have been better able to absorb inflationary pressures, housing and otherwise. Additionally, we are seeing the gap between headline inflation and wage growth narrow as inflationary headwinds abate, a trend which, if continued, could result in a return to real wage growth — a critical factor for our consumption-based economy.

The odds of a near-term recession have fallen, perhaps simply delaying the inevitable, but also perhaps signaling the possibility of an economic soft landing. While seemingly clear signals like yield curve inversion and the banking crisis pointed toward the most anticipated recession ever and drove the widespread shift by investors to a more defensive posture, the other shoe has yet to drop, and traditionally defensive parts of the Russell 3000 Value Index have been anything but. The consumer staples sector has returned 1.04% year to date, compared to the index’s 4.98% overall return. Health care and utilities sectors have fared even worse, returning -3.99% and -5.69%, respectively.

On its surface, the market appears to be sanguine; the S&P 500 is up +16.9% year to date in the face of recessionary fears, the CBOE Volatility Index ( VIX ) is within sight of its five-year low and high-yield and leveraged loan spreads remain relatively well contained.

"Not all is as it seems, and there is much more turbulence beneath this surface."

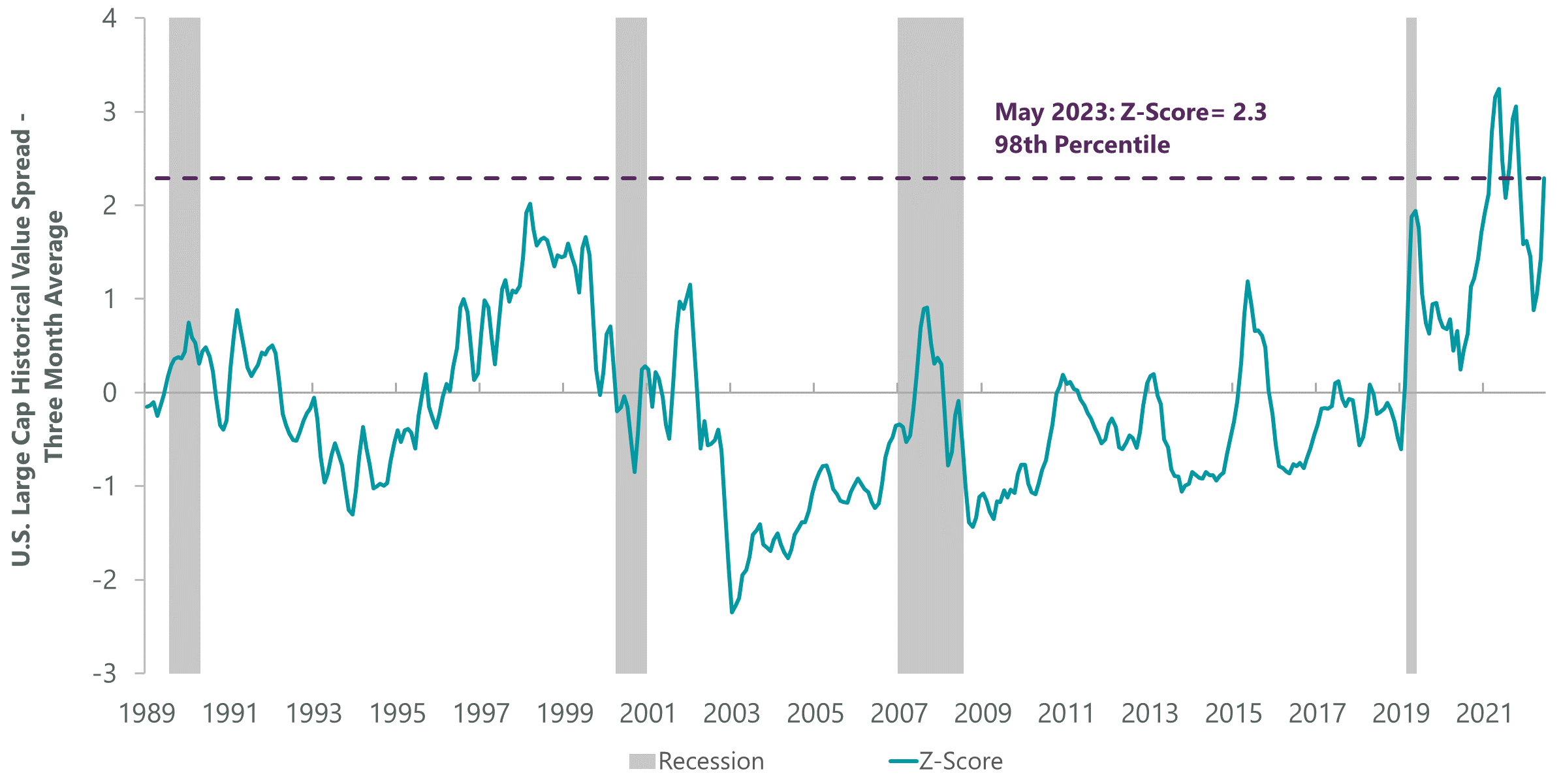

However, not all is as it seems, and there is much more turbulence beneath this seemingly placid surface. Traditionally cyclical parts of the market have found themselves left out in the cold, and value stocks appear far from staging a broad-based rebound. The rally in builder stocks belies an apathy that is more typical across most value stocks right now. Indeed, measures of valuation spreads have reverted to levels last seen during the height of the speculative growth stock mania in 2021 (Exhibit 4). Our conclusion is that the rally this year has lacked breadth and is far from an all-clear signal for the economy and future market performance.

Exhibit 4: Value Spreads Snap Back to Historic Highs

{kind=link}

| As of May 31, 2023. Source: ClearBridge Investments |

Instead, it appears that mega cap tech companies are back to being the belles of the ball, as investors piled back into many of the same winners from the pandemic peak. The furor over artificial intelligence ((AI)) and speculation that the benefits of recent breakthroughs will accrue to mega cap incumbents explains much of this, as does the perceived defensiveness of some of the business models of whichever acronym currently encompasses the group these days. Secular growth plus some degree of defensiveness just seems so obvious — a similar sentiment felt by investors who were maximally defensive earlier this year only to see such positioning meaningfully lag that market. Only time will tell whether AI ultimately flatters current tech leadership or helps unseat some of the mega cap incumbents, but we feel confident that a combination of price action to date, historic index concentration, valuation spreads near all-time highs and the underperformance of smaller companies means a continuation of their outperformance gets much, much harder from here.

Portfolio Positioning

This myriad of factors and crosscurrents are all germane in considering our portfolio positioning. History strongly suggests that current valuation spreads will help drive outperformance of value as a factor and the Strategy over the medium term. Our bottom-up analysis also continues to show more opportunity outside of the mega caps, resulting in the Strategy having a smaller average market cap than our index, and we expect that the eventual reversion higher in smaller cap stocks will benefit our performance. For example, we added a new position in Marvell Technology ( MRVL ), a networking and storage semiconductor company in the 5G, data center and automotive ethernet end markets. In addition to being seen as one of the main beneficiaries of future AI-related data center buildouts, we believe the company’s crucial supplier position at the nexus of high-growth technology sectors leaves it exceptionally well-positioned to be a long-term compounder for the portfolio, and this potential is not reflected in its current valuation.

Our analysis indicates that traditionally defensive sectors continue to be overvalued, particularly considering the alternative of owning cash that yields 5%+ with no valuation risk and the prospect for greater yields if the Fed continues to tighten. Given these risks, we are deliberately holding more cash that we intend to deploy into high-return opportunities if market stress emerges.

We continue to diligently adhere to our investment process and methodology and have populated the portfolio with companies with either exceptional balance sheet strength or resilient P&Ls, or in many cases both, which will allow them to emerge stronger if any cyclical weakness materializes. Within this framework, we continue to look for companies whose unique business models add diversification and differentiated drivers to the portfolio while also helping to manage portfolio volatility.

New purchase Clean Harbors ( CLH ) fits the bill across all these attributes. The environmental and industrial services company specializes in transporting, treating and disposing of hazardous waste through its waste treatment and disposal facilities. Due to the high regulatory burden of entering the hazardous waste disposal industry, the company has been able to establish itself as the industry leader, while industry consolidation is helping it achieve strong pricing power. The company’s strong free cash flow generation and idiosyncratic growth opportunities add to the resiliency of the portfolio against major market disruptions.

Ultimately, our positioning balances the need to lean into the value opportunity medium term against the risks present to the market near term.

Outlook

As we continue to push into this unique market cycle, we are reminded of the importance of remaining both humble and vigilant due to how quickly the winds can change direction. While we have been pleasantly surprised with how well the economy has held up, the Fed’s need to continue interest rate hikes only further raises the odds of something else breaking, either within the traditional banking system or (more realistically) outside of it. The lagged impact of higher interest rates continues to suggest elevated odds of a recession and warrants caution on the margin. As a result, we will continue to adhere to our rigorous investment process and to manage according to our philosophy of seeking attractive long-term returns over a full market cycle.

Portfolio Highlights

The ClearBridge All Cap Value Strategy outperformed its Russell 3000 Value Index during the second quarter. On an absolute basis, the Strategy had positive contributions from 10 of the 11 sectors in which it was invested during the quarter. The leading contributors were the financials, IT and industrials sectors, while the health care sector was the sole detractor.

On a relative basis, overall stock selection effects contributed to outperformance while sector allocation effects detracted. Specifically, stock selection in the financials, IT, energy, communication services, industrials, materials and utilities sectors and an underweight to the consumer staples sector benefited returns. Conversely, stock selection in the health care sector, an underweight to the communication services sector and an overweight to the energy sector detracted from performance.

On an individual stock basis, the biggest contributors to absolute returns in the quarter were Meta Platforms ( META ), Oracle ( ORCL ), Marvell Technology, [[EQT]] and Vulcan Materials ( VMC ). The largest detractors from absolute returns were AbbVie ( ABBV ), [[AES]], Pfizer ( PFE ), CVS Health ( CVS ) and Gilead Sciences ( GILD ).

In addition to the transactions listed above, we initiated positions in Block ( SQ ) in the financials sector, Airbnb ( ABNB ) in the consumer discretionary sector and Canadian Pacific Kansas City ( CP ) in the industrials sector. We exited positions in Cisco Systems ( CSCO ) and DXC Technology ( DXC ) in the IT sector, Unilever ( UL ) in the consumer staples sector and Gray Television ( GTN ) in the communication services sector.

Reed Cassady, CFA, Director, Portfolio Manager

Albert Grosman, Managing Director, Portfolio Manager

Sam Peters, CFA, Managing Director, Portfolio Manager

| Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. Performance source: Internal. Benchmark source: Standard & Poor's. Copyright © 2023 ClearBridge Investments, LLC |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

ClearBridge All Cap Value Strategy Q2 2023 Portfolio Manager Commentary