CCHBF - Coca-Cola FEMSA: Wait For A Better Entry

2023-03-24 14:56:33 ET

Summary

- Coca-Cola FEMSA, S.A.B. de C.V. has consistently maintained the strongest margin profile among its peers, usually landing between 13-15% per year.

- While the revenue growth and margin profile were both surprisingly strong, one big area of weakness for the entire category is their return on invested capital.

- To make these sugary beverages, one must invest in large plants, machinery, aluminum and glass, and a lot of labor.

Introduction

Ahhh, The Coca-Cola Company (KO), the classic American brand, known for its distinctive logo, and caramel color, and sweet taste.

Coca-Cola just feels… well, American!

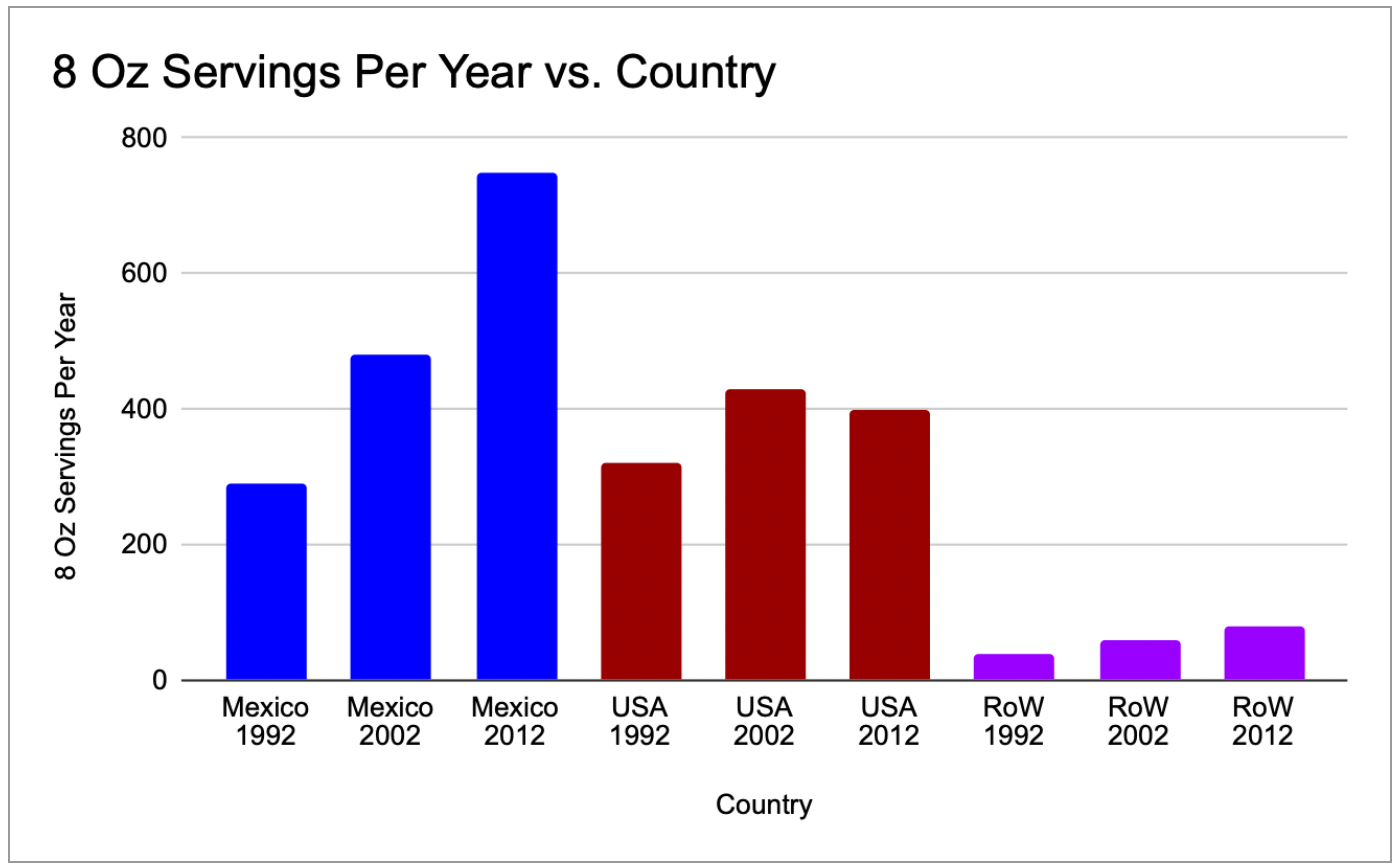

But what would you say if I told you that in terms of per capita consumption, Mexicans drink even more?!

It's true!

{kind=link}

Created by Author Using Data From Company

While American consumption of Coca-Cola has been on the decline, consumption is increasing in Latin American countries like Mexico, Chile, and Panama.

Within this article, I'd like to examine one company that is capitalizing on this trend, Coca-Cola FEMSA, S.A.B. de C.V. ( KOF ), one of the largest international bottlers of Coca-Cola serving the Latin American market (especially Mexico).

And what's more, despite the challenging macro headwinds facing much of the world, Coca-Cola FEMSA, S.A.B. de C.V., or Coke Femsa, seems to be nearly unfazed, as its stock price is up over 40% over the past 12 months while many indices like the S&P are in the red.

Talk about Alpha!

Within this article, I'll explore the business of Coca-Cola FEMSA, dig into its financial performance, and discuss where I believe shares could go from here.

Strong growth supported by increasing demand in developing economies

As one of the largest Coca-Cola franchise bottlers in the world, Coca-Cola FEMSA, S.A.B. de C.V. has a vast distribution network and an extensive portfolio of brands that it can leverage. And with a per capita consumption of Coca-Cola higher in Mexico than in the U.S., and consumption growing faster, this company may have tons of upside potential.

IMF

While it has been much more volatile than developed countries like the USA, economic growth in Mexico and Latin America is still relatively strong. As these economies grow, the shared wealth expands and a growing consumer base looks for new ways to spend. One of the most accessible treats to low-income earners with growing incomes is a simple glass of Coca-Cola.

Further supporting growth in Latin America is growing American fear toward the rising power of China. Countries like Mexico are benefiting from so-called " friend-shoring " wherein countries are moving their supply chains to countries with shared (often) pro-Western values.

As international companies look to diversify supply chains away from countries perceived to be unfriendly like China, countries in Latin America stand to benefit from a possible influx of capital. Such a move, if it happens, would likely further support increased demand for consumer goods (like Coke!) in Latin America.

2022 Financial Performance

Coca-Cola FEMSA had an impressive year, with an 8.6% increase in consolidated volumes, thanks to double-digit growth in Brazil, Colombia, Argentina, and Guatemala, as well as strong performance in Mexico and Uruguay.

The company also saw a 16.4% increase in total revenues, driven by pricing initiatives, and favorable price-mix effects, alongside the aforementioned volume growth. Overall, these numbers suggest that Coca-Cola FEMSA is successfully navigating challenges in the industry and continues to grow its business both in terms of volume, and overall revenue.

Financial Performance Versus Peers

Moving on from the most recent year, let's take a look at Coca-Cola FEMSA compared to some of its other international peers.

Revenue

As you can see in the chart above, revenue at Coke Femsa has dramatically increased since the year 2000, from around $2B to over $11.3B as of this year! This coincides well with the chart from the start of this article highlighting the effect increased consumption is having on Coke Femsa's top line.

Looking at its peers, we can see that KOF is only second in size to the newly created Coca-Cola Europacific Partners ( CCEP ), which serves the European and Australian markets. Coca-Cola Consolidated ( COKE ) a U.S.-based entity, has also seen strong growth but lacks the scale that Coke Femsa has.

Margins

In addition to its relatively strong growth profile, Coke Femsa has also consistently maintained the strongest margin profile among its peers, usually landing between 13-15% per year. This may be due to the lower cost of labor in Latin American countries compared to the markets some of its other peers serve: the USA, Japan, Europe, and Australia.

Of note, Coca-Cola Consolidated has also shown improvements in growing their margins over the last few years, but, at 10.3% they are still just a bit behind Coke Femsa.

Return on Invested Capital

While the revenue growth and margin profile were both surprisingly strong, one big area of weakness for the entire category is their return on invested capital. Taking a look at the 3-year rolling average, KOF has been able to allocate its capital to earn just 6-9% per year, which is relatively average among its peers.

While Coca-Cola Consolidated has seen outsized returns on capital over the past years, its long-term track record is in a similar range to other bottlers.

Difficult Industry

Single-digit returns on invested capital suggest either poor execution or a capital-intensive industry. In the case of these bottlers, I believe it has more to do with the nature of the bottling business, which is incredibly capital-intensive. To make these sugary beverages, one must invest in large plants, machinery, aluminum and glass, and a lot of labor.

This, in my opinion, is likely why Coca-Cola decided to spin off the majority of its global bottling operations several years ago. Coca-Cola's main business clearly earns a much higher return on invested capital, and reduced exposure to bottling operations is likely a key reason why.

Risks

In my view, the largest risk facing KOF is the fact they are essentially a controlled entity by Fomento Económico Mexicano, S.A.B. de C.V. d.b.a. FEMSA ("FMX"), since they own nearly 50% of the shares and a further ~25% is owned by Coca-Cola proper. Such a low float leaves little room for retail or institutional investors to sway decision-making in any way. Depending on the company, this can either be a non-issue or a big problem. For example, if FEMSA wanted to, they could block a merger with another large bottler, even if it made financial sense. They are also exposed to several inflation-impacted inputs but, judging based on their margin profile, they have been able to push these costs onto the consumer.

Valuation and Conclusion

Given the similar margin profile between these businesses, I decided to compare them based on their price to sales. KOF comes in near the top of the pack at 1.4x sales, which is quite a bit higher than its 3-year average of 1.14x and a number of its peers as well.

At 1.4x, CCEP's price to sales is also in the premium range, but Coca-Cola HBC (Coke HBC) ( CCHGY ) and Coke Consolidated look much more reasonably priced at 1x and 0.8x sales respectively.

To conclude, Coca-Cola FEMSA has had some impressive financial performance and growth in recent years, fueled by the surging demand for Coca-Cola in developing economies. The company's ability to effectively manage costs amid inflationary pressures has resulted in an especially strong margin profile compared to its peers. However, the low returns on capital in the industry suggest a limited long-term potential for Coca-Cola FEMSA investors.

Despite its impressive track record, Coca-Cola FEMSA, S.A.B. de C.V.'s stock price is currently priced much higher than its peers, Coca-Cola Consolidated and Coca-Cola HBC, indicating that it could be overvalued.

At the end of the day, it looks like the strong margin profile and its secular growth drivers are already priced in Coca-Cola FEMSA, S.A.B. de C.V. stock.

I rate Coca-Cola FEMSA, S.A.B. de C.V. a Hold.

For further details see:

Coca-Cola FEMSA: Wait For A Better Entry