CCHBF - Coca-Cola HBC: Getting Interesting Despite The Russia Overhang

2023-09-22 10:30:00 ET

Summary

- Coca-Cola HBC is a strategic bottling partner of Coca-Cola, with a strong focus on Eastern Europe and Russia.

- The company is still making money in Russia despite geopolitical issues, but without the Coca-Cola brand.

- Coca-Cola HBC expects growth opportunities in emerging markets and mature markets like Italy, with strong mid-term growth targets.

Introduction

Coca-Cola HBC ( OTCPK:CCHBF ) ( OTCPK:CCHGY ) is a strategic bottling partner of the Coca-Cola Company ( KO ) with the exclusive rights to produce and sell Coca-Cola products in a certain geographic region. The company has always had a strong focus on Eastern Europe and Russia, and those still are the more important countries in its country portfolio.

{kind=link}

The primary listing of the company is in London where the average daily volume is almost 900,000 shares , so it clearly is the most liquid listing. Using the current GBP/EUR exchange rate, the share price is almost 25.90 EUR/share and I will use that as my reference point considering the company reports on its financial results in Euro.

You can find all relevant information here .

{kind=link}

The Russian situation isn’t holding the company’s financial performance back

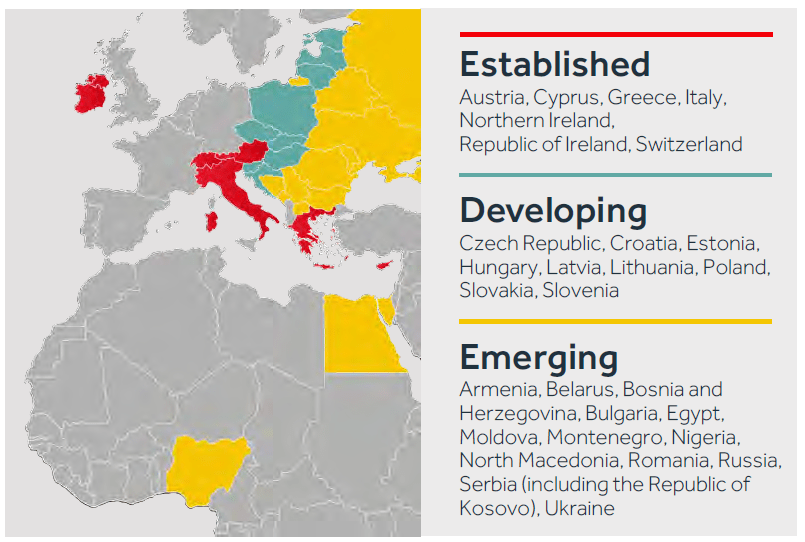

One of the main reasons to have exposure to Coca-Cola HBC is for its exposure to emerging markets. Indeed, it holds the exclusive rights for large chunks of Eastern Europe (including Poland, Czechia, Slovakia which it rightfully so classifies as developing nations), but it also offers exposure to for instance Bulgaria, Belarus and Russia, as well as Egypt and Nigeria in Africa.

I originally really liked the exposure to Russia but it goes without saying the geopolitical issues in that part of Europe have completely derailed the prospect of Russia as Coca-Cola officially left the country. Coca-Cola HBC still owns the bottling plants which are now producing the Dobry Cola , basically the domestically copied version of the real product.

This means that Coca-Cola HBC is still making money in Russia (but we will have to keep an eye on its performance and hopefully avoid nationalisations ), but it just doesn’t have Coca-Cola as powerful brand to push sales. That does have an impact on the thesis but the fallout and economic damage appears to be easier to deal with than I had initially thought. In the first half of this year, the Russian volumes decreased by a high single digit. Keep in mind though the comparable period last year only about three months of contribution from Coca-Cola products in Russia as Coca-Cola pulled the plug in March of last year.

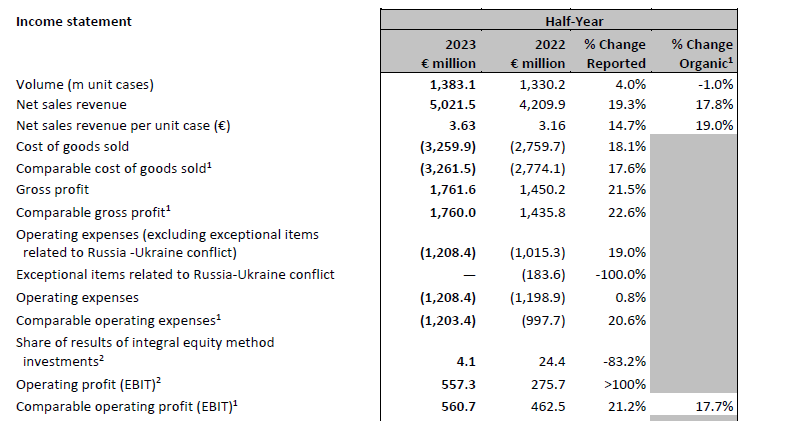

The total volume increased by about 4% on a reported basis, but decreased by 1% on an organic basis as a portion of the volume increase was related to the consolidation of the Russian assets.

Prices increased pretty sharply and this resulted in a 19.3% revenue increase on a reported basis. This means the revenue per unit case increased by about 15%, and based on the table below, it’s safe to say the percentual increase of the costs and revenue were pretty close to each other.

{kind=link}

This also resulted in a strong EBIT increase which more than doubled on a reported basis, but keep in mind the results in the first semester of last year were impacted by a 184M EUR charge related to the Russian-Ukrainian war. Fortunately Coca-Cola HBC also provided a comparable EBIT performance, but that result is equally impressive with a 21.2% increase on a reported basis and a 17.7% increase on an organic basis.

And as you can see below, the strong EBIT and relatively low net finance expense boosted the pre-tax income to 528M EUR, resulting in a net profit of 385.1M EUR.

{kind=link}

That result includes a 0.6M EUR loss attributable to non-controlling interests so the net profit attributable to the shareholders of Coca-Cola HBC was 385.7M EUR which works out to 1.05 EUR per share.

I like the Coca-Cola bottlers for their robust cash flow performance. And Coca-Cola HBC -although impacted by a war in two of the countries – still reported strong results.

As you can see below, the total operating cash flow was 495M EUR in the first semester. It probably doesn’t come as a surprise that some adjustments need to be made. First of all, the tax-related cash outflow was just 95M EUR but based on the H1 income statement, about 143M EUR was due. Secondly, there were about 29M EUR in lease payments while there was a 31M EUR cash interest payment. To be completely correct, there also was a 3.1M EUR cash settlement of derivatives but I am keeping that out of the equation for now.

{kind=link}

And the cash flow statement above also shows there was a 170M EUR working capital investment. There were also some positive adjustments: the company received 13.8M EUR in interest income. After incorporating all these elements, the adjusted operating cash flow was 571M EUR in the first half of this year. A good result.

The capex was relatively high as HBC continues to invest in expansion. The company spent 207M EUR on capex and combined with the 29M EUR in lease payments, the total investment level of 236M EUR was about 20% higher than the 198M EUR in depreciation and amortization expenses.

With 367.5M shares outstanding, the underlying free cash flow result on a per-share basis was approximately 0.91 EUR. The difference with the EPS of 1.05 EUR can mainly be explained by the difference between capex an the depreciation/amortization rhythm and a few non-cash elements that contributed to the strong net income result (the gain on disposals and the results of equity method investments).

Coca-Cola HBC hosted a capital markets day earlier this year. It hardly is a secret it is focusing on its portfolio of sparkling products which represent the vast majority of its revenue.

{kind=link}

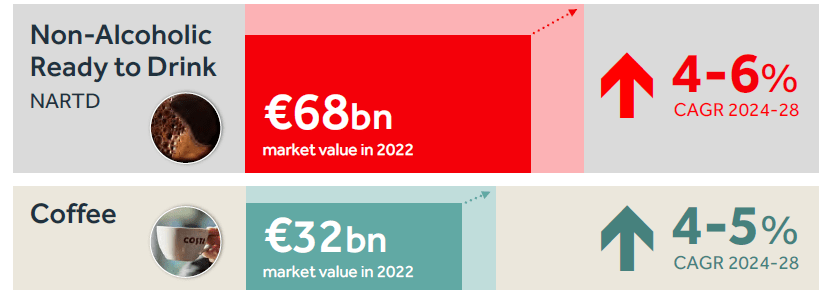

Additionally, it expects both the non-alcoholic beverage market and even the coffee market to grow by a mid single digit percentage in the next five years.

{kind=link}

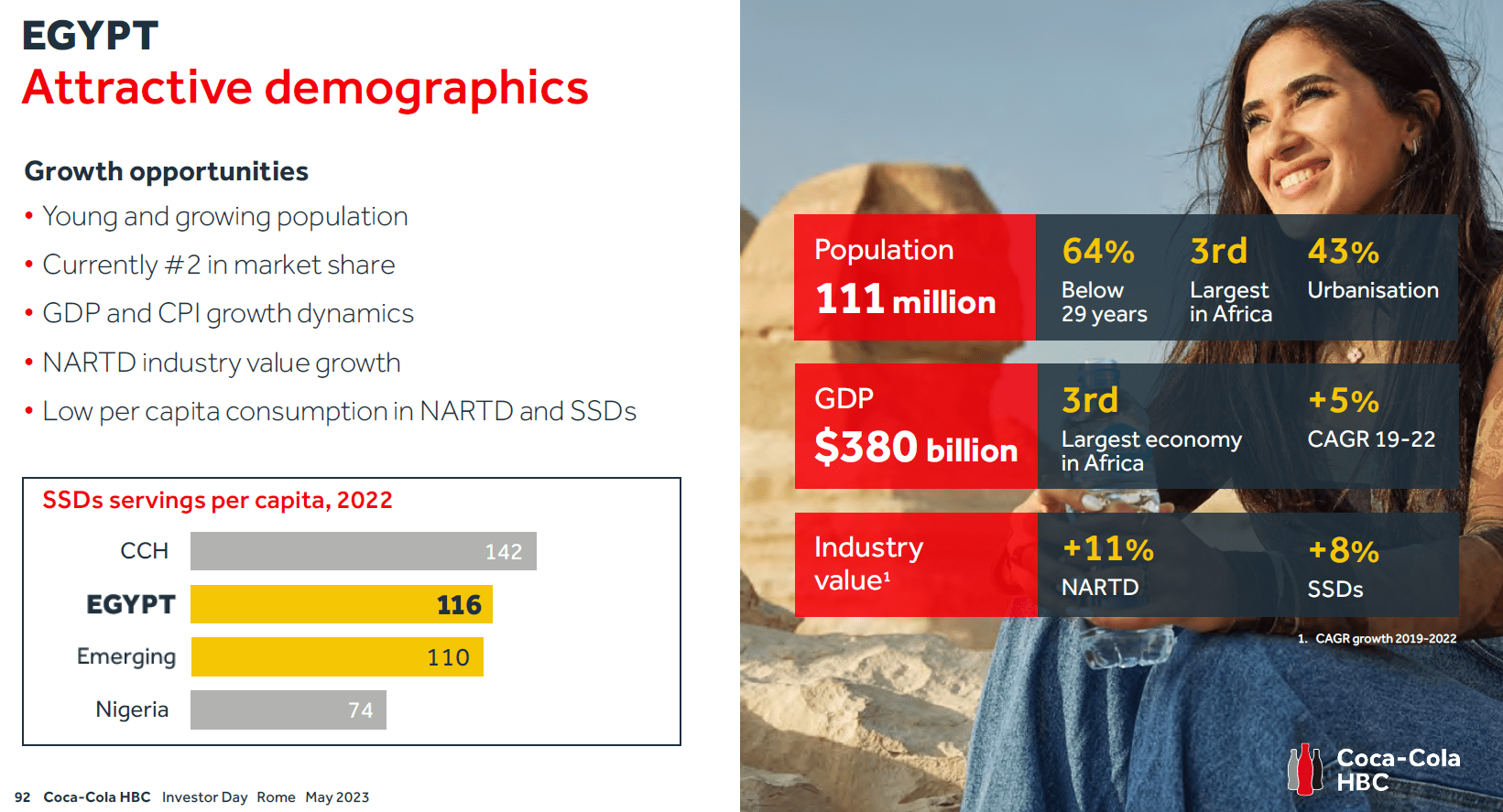

Additionally, the recent acquisition of the Egypt concession could also be a strong driver for the company. After all, it is a very young country and Coca-Cola HBC is counting on the population growth and GDP per capita growth to grow the business there.

{kind=link}

But Coca-Cola HBC also sees plenty of growth opportunities in what we would perhaps already consider a mature market, like Italy. Interestingly, the total consumption in Italy is about 15% lower than in Greece and about 40% lower than in Spain, so Coca-Cola HBC is expecting to see Italy catch up to the other Mediterranean countries. One of the investments the company is focusing on is the addition of three new filling lines in the country. Those should be operational by 2025 and will boost the capacity by almost 20% (compared to the 2022 production capacity).

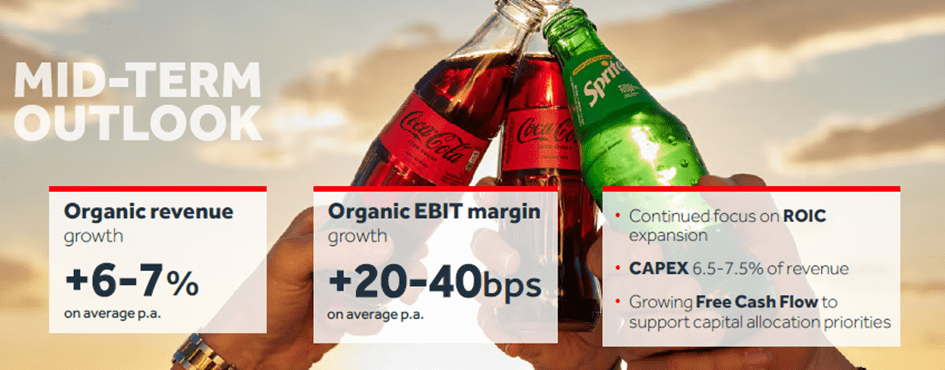

This translates into pretty strong mid-term growth targets. As you can see below, the company anticipates a 6-7% annual organic revenue growth while its EBIT margin should increase by 20-40 bps per year as well. With an EBIT level of 930M EUR in FY 2022 and an additional acceleration this year, those targets could be pretty impressive.

{kind=link}

If we would assume a FY 2023 EBIT of 1.02B EUR (which represents the lower end of the company’s guidance for 2023 ) and increase the revenue by 6% per year, the EBIT will reach 1.29B EUR by 2027. And that excludes any margin expansion. Assuming a 20 bps per year margin expansion (again the lower end of the official mid-term guidance) the EBIT could increase by an additional 106M EUR to 1.4B EUR.

Even if we would deduct 130M EUR in net interest expenses assuming a cost of debt of 4.5% and a return of 1.8% on the cash pile, the pre-tax income would be 1.27B EUR. After applying the normal tax rate of approximately 27%, the net income would be 927M EUR or 2.52 EUR per share. And assuming the payout ratio of 40-50% remains unchanged, this would imply a dividend of 1-1.25 EUR per share from 2027 on. Coca-Cola HBC’s website mentions a 10% dividend withholding tax rate which would be good considering the stock has a Swiss ISIN-code and the standard Swiss dividend withholding tax is 35%. As I currently do not own any shares of Coca-Cola HBC, I have no first-hand information on the applicable foreign dividend withholding tax rate.

Investment thesis

I like the bottlers associated with Coca-Cola as there are very few brand names with such a wide brand recognition and reputation. The markets HBC is focusing on are still growing and the recent entry into Egypt likely is a good move as HBC will be able to leverage its expertise in this new market.

Just like most other Coca-Cola related bottlers, Coca-Cola HBC isn’t cheap. The stock is currently trading at approximately 13-14 times earnings and at an EV/EBITDA multiple of less than 8 (and decreasing pretty fast based on the projected growth profile). That being said, the strong brand reputation and the exclusive rights to produce, market and distribute Coca-Cola related products are quite valuable and if the revenue can indeed increase by 6% per year for the next few years, the EBIT result will grow tremendously and the stock is trading at only 10-11 times the anticipated earnings for 2027.

And that makes Coca-Cola HBC worth considering. The current value is not outrageously high and there is a clear and credible growth trajectory to execute on in the next few years.

For further details see:

Coca-Cola HBC: Getting Interesting Despite The Russia Overhang