CDE - Coeur Mining: A Light At The End Of The Tunnel

2023-10-03 11:14:26 ET

Summary

- Coeur Mining has experienced significant share dilution and lifeless returns for shareholders since 2020.

- This can be attributed to a massive capex blowout at Rochester, and the result is a weaker development pipeline, the sale of strategic investments, and significant dilution.

- Fortunately, there's finally a light at the end of the tunnel with the Rochester Expansion nearing the finish line.

- In this update, we'll look at the valuation after this ~80% correction, whether CDE stock is offering a margin of safety, and if the stock is finally investable.

Roughly three years ago, I wrote on Coeur Mining ( CDE ), noting that there was no way to justify chasing the stock above US$10.00 and that its 40% rally in one month was not the time to be greedy, specifically stating:

"In fact, if Coeur Mining heads above $11.70 in Q1 due to improved sentiment among the silver miners, I would view this as an opportunity to book profits. This is because the stock would trade at over 17x FY2021 annual EPS, a lofty price to pay for a miner with a mediocre long-term track record, evidenced by several years of net losses per share and a massive write-down on Silvertip. Given the risk of share dilution to buttress the balance sheet to help fund the Rochester Expansion combined with industry-lagging margins, I believe there are far better places to park one's money in this sector."

- Coeur Mining Update, Valuation No Longer Attractive, December 27th, 2020

The stock would peak during the silver squeeze at $12.60 above my $11.70 sell target and has dropped over 80% since, with the violent correction not being surprising when factoring in the near 50% share dilution in the period. And while I previously noted that the company had a mediocre track record, we've seen a massive downgrade to this title, with a poor track record being generous with above-average share dilution at multi-year lows, losses on equity investments, and this significant share dilution being despite selling off multiple assets to help fund POA 11 (Sterling, Crown, La Preciosa). And while inflation is partially to blame for the messy situation, the ~80% over-budget Rochester Expansion is above the industry average.

Although this certainly doesn't inspire confidence, there's finally a light at the end of the tunnel here, with Coeur announcing initial production from its Rochester Expansion, with production from the new Stage VI leach pad, and commercial production at the Merrill-Crowe plant expected in early 2024. Meanwhile, construction of the three-stage crushing circuit is nearly complete. Assuming all continues to go to plan and no more capex blowouts are reported, the company has less than $60 million in additional spending to project completion, and the much-awaited benefit will be a doubling of its production profile at this Tier-1 jurisdiction asset to 7.5+ million ounces of silver and ~65,000 ounces of silver in FY2025 based on company estimates. Let's take a closer look below:

Rochester Operations - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

A Light At The End Of The Tunnel

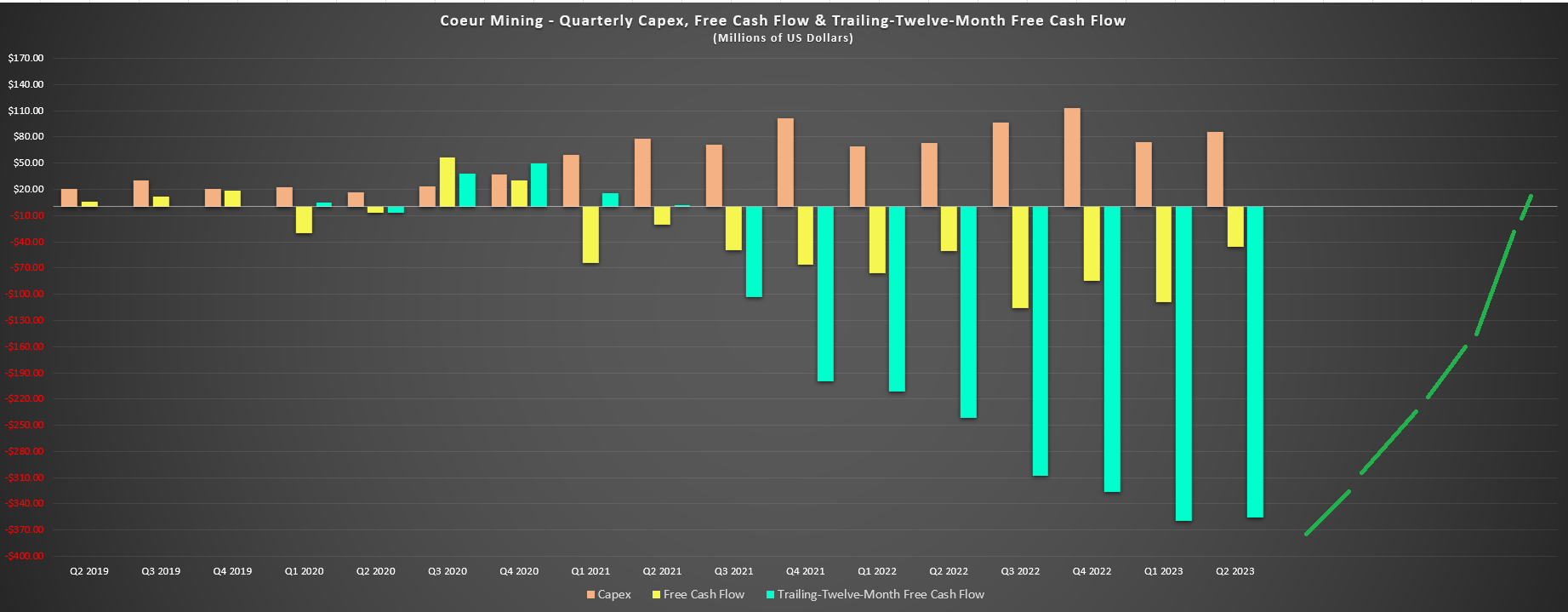

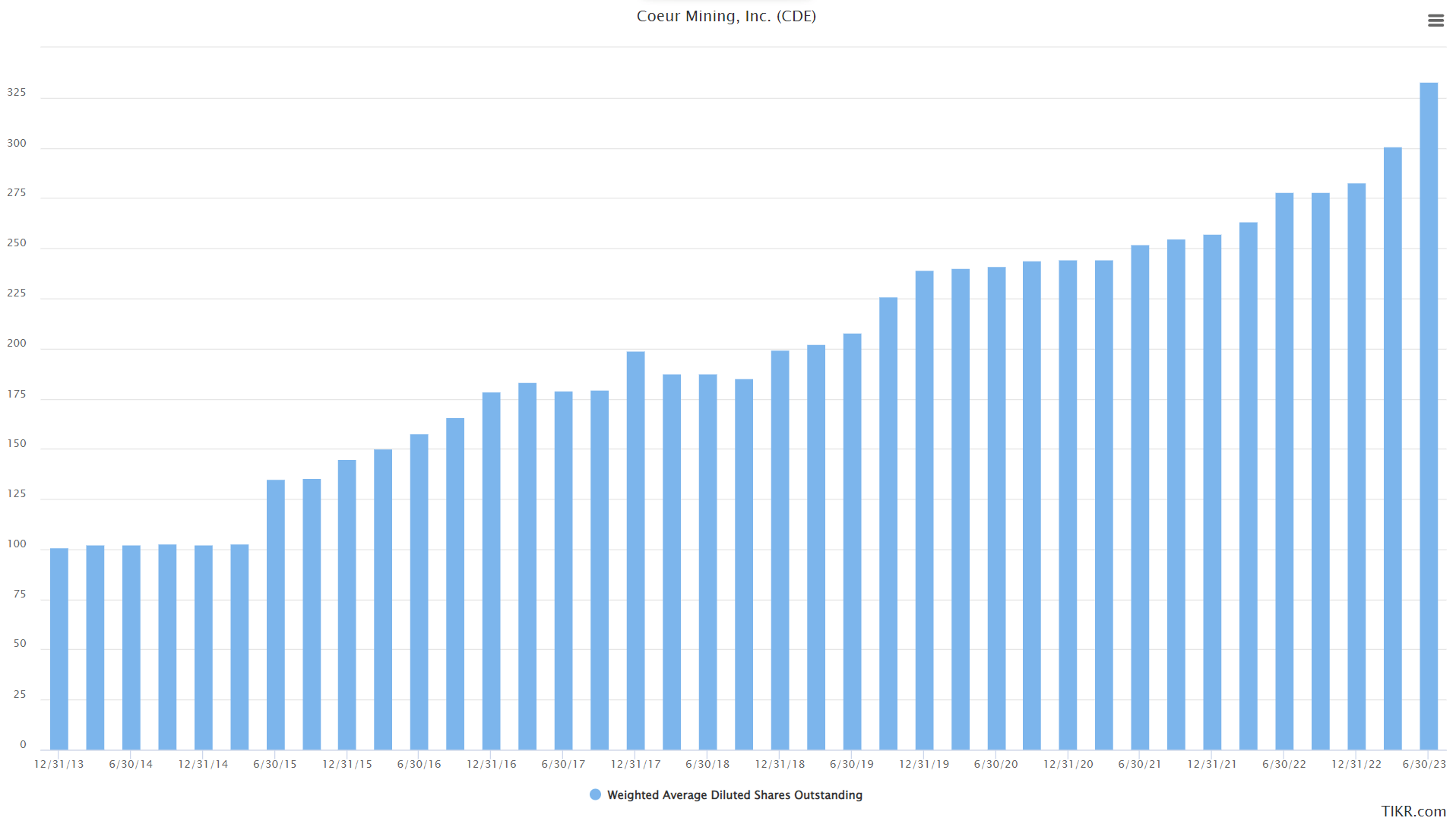

Investing in Coeur over the past few years has not been for the faint-hearted, with investors getting wind of an additional ~32.9 million shares sold at $3.04 earlier this year at multi-year lows, translating to ~10% share dilution. More share dilution was announced shortly after Coeur's ATM sales of ~$100 million related to a flow-through financing, and this dilution was on top of double-digit share dilution in 2022, and despite all of this dilution, Coeur still sports one of the weakest balance sheets, with ~$60 million in cash and ~$420 million in net debt. However, as noted, the Rochester Expansion, which has been a massive drain on its cash position is just months away from completion, setting Coeur up to generate positive free cash flow again by Q2 2024 if metals prices can cooperate. And with cash outflows like we've seen, this will certainly be a welcome development for shareholders getting used to staring at red ink.

Quarterly Capex, Free Cash Flow & TTM Free Cash Flow - Company Filings, Author's Chart

{kind=link}

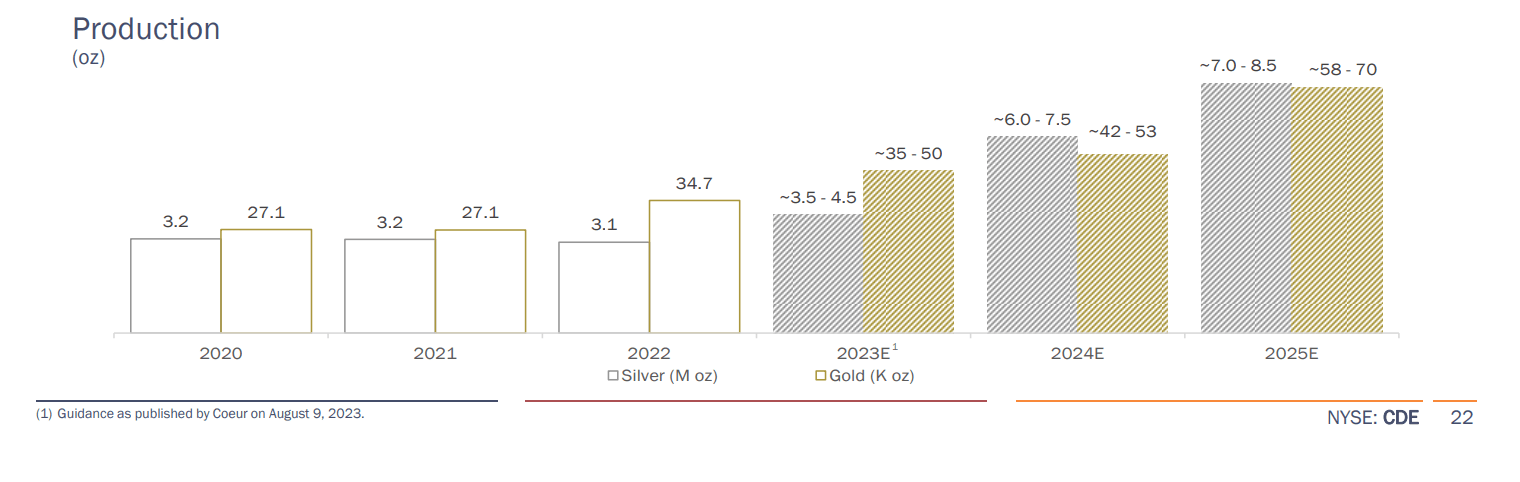

As the chart below shows, the Rochester Mine will go from the company's least significant mine with considerable free cash outflows during its expansion to its largest (adjusting for stream impact at Palmarejo), producing over 160,000 gold-equivalent ounces [GEOs] per annum based on 2025 estimates and an 80 to 1 gold/silver ratio. This should allow Coeur to generate at least $50 million in free cash flow next year after debt repayments, a significant improvement from free cash outflows of ~$155 million year-to-date and $300+ million on a trailing-twelve-month basis. In addition, the steady ramp up in production will help Coeur's rapidly declining production per share metrics, with little to show for its ~50% share dilution since Q3 2019 given that production has declined in the period (lower grades at Palmarejo, Silvertip taken offline). Most importantly, though, the company will be able to attack its debt load, which stood at ~$470 million at the end of Q2, a hefty figure for a company generating less than $85 million in EBITDA in the past four quarters combined.

Rochester - Historical Production & Forward Estimates - Company Presentation

{kind=link}

To summarize, while there's been no way to justify holding shares in Coeur over the past two years since construction began, that setup is finally getting ready to turn with limited risk of further cost increases (over 90% of capital has been spent), and the company is getting ready to enjoy the fruits of this labor.

Recent Developments

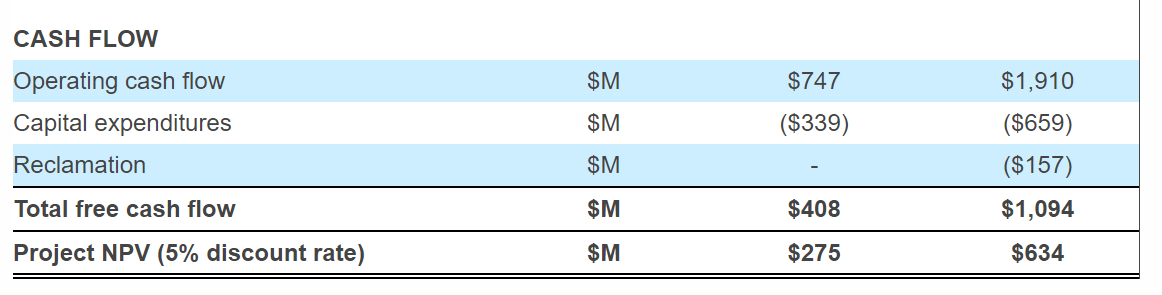

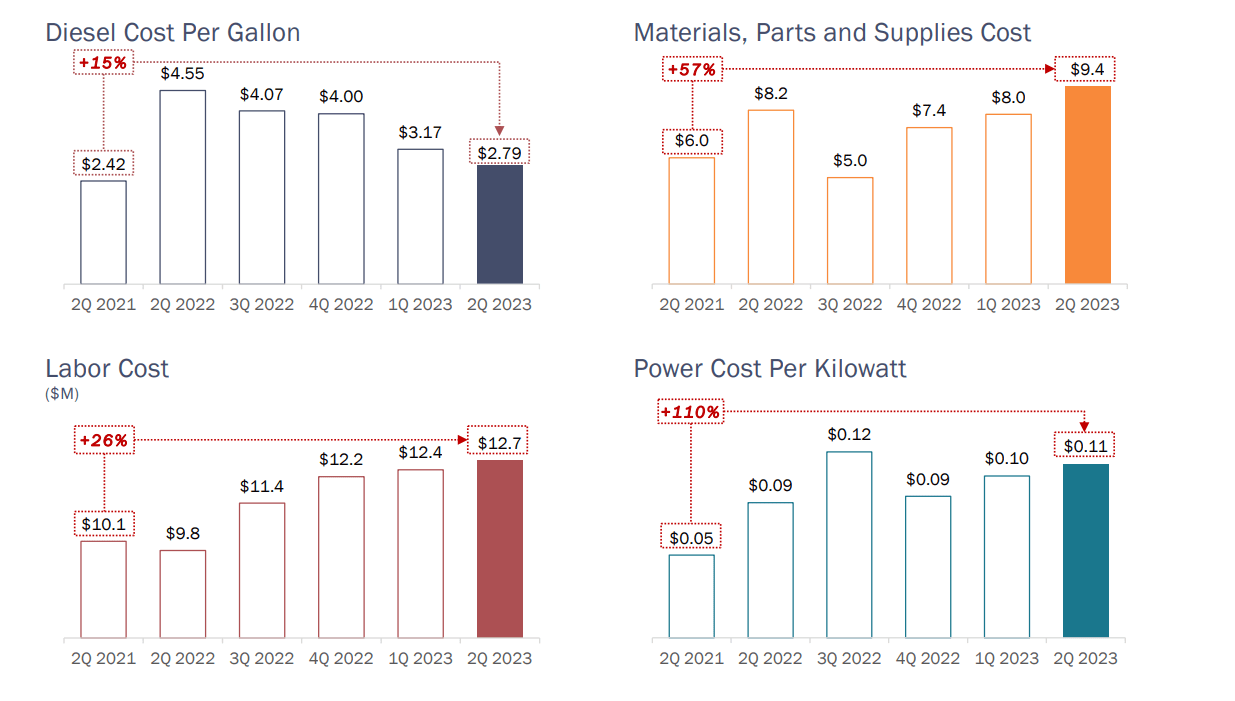

Unfortunately, while getting the Rochester Expansion online is positive news, the numbers look very different to how they did in 2020 when Coeur announced its Rochester Expansion. This is because gold and silver prices have made little upside progress from Q3 2020, but we've seen over 30% inflation sector-wide, making the estimates of average annual free cash flow of $104 million at Rochester quite stale. Meanwhile, the after-tax IRR of 31% is a distant memory, with capex on the project nearly doubling to ~$730 million, cutting down its estimated After-Tax NPV (5%) of $634 million at Rochester even if we use higher gold and silver prices of $1,800/oz and $21.00/oz vs. previous estimates of $1,544/oz and $19.45/oz, respectively. And while diesel prices have eased from peak levels in 2022, they're back on the rise since Q2 and there's been minimal relief for power, labor, and consumables costs.

Rochester Expansion 2020 Assumptions - Company Website

{kind=link}

As the chart below shows, diesel costs are up over 20% since Q2 2021 when adjusting for more recent costs per gallon, materials, parties and supplies costs are up nearly 60%, and power costs are up over 100%. Meanwhile, a massive component of costs, labor, has risen 26% and there's no reason to believe these costs will ease given that we continue to see mild to moderate levels of labor tightness in prolific mining jurisdictions like Nevada, Ontario/Quebec, and Western Australia depending on the mine. Hence, while Rochester will generate positive free cash flow, the recent drop in gold and silver prices combined with significantly higher operating costs has soured the outlook vs. what investors might have expected as of Q4 2020 from an IRR, After-Tax NPV (5%) and annual free cash flow generation standpoint.

Rochester Cost Increases - Company Presentation

{kind=link}

Unfortunately, Rochester isn't the only jurisdiction to see labor and cost inflation, with the company's other mines in the United States also suffering from inflationary pressures which not only affect margins but could affect cut-off grades, creating a greater hurdle to adding reserves. And in Mexico, Palmarejo is not getting any help from the strength in the Mexican Peso, which has cooled to 17.6 to 1 (USD/MXN) vs. 20/1.0 last year, but is still much stronger and affecting costs for Mexican miners. And with the Palmarejo Mine already saddled with a ~50% gold stream at a price of $800/oz that was agreed upon in 2014, the combination of inflationary pressures and a stronger Mexican Peso are not ideal for the company's #2 asset post-Rochester Expansion. Hence, although the outlook for Rochester and overall free cash flow has improved, I'm less optimistic about reserve growth and margins at its other assets, which could see rising cut-off grades and pinched margins, especially if metals prices can't rebound by early next year when Coeur's hedges roll off.

Valuation

Based on ~357 million fully diluted shares and a share price of US$2.10, Coeur Mining trades at a market cap of ~$750 million and an enterprise value of ~$1.16 billion, making it one of the lowest capitalization producers among its peer group of 350,000+ producers in Tier-1 jurisdictions. That said, and as I have consistently highlighted in past updates, there has been absolutely zero reason to own the stock given that it was impossible to pin down a correct valuation for Coeur when more shares were going out the door each quarter (consistent dilution). Meanwhile, the company's operating portfolio has left much to be desired, with a low grade operation at Rochester, short mine lives at its high-grade assets, and a significant gold stream in a jurisdiction on what's arguably its best asset, Palmarejo. Not helping matters is that investment attractiveness for Mexican assets like Palmarejo has declined somewhat following several negative developments this year in Mexico (Penasquito strike, changes to mining laws ).

Coeur Mining - Weighted Average Share Count - TIKR.com

{kind=link}

Unfortunately, this inferior operating portfolio and track record of consistent share dilution has made it nearly impossible to justify an investment in Coeur. However, on the positive side, the massively over-budget Rochester Expansion is finally complete. This means that we should see a halt to the regular share dilution investors have experienced. Simultaneously, this operation will significantly increase Coeur's company-wide production, with Coeur set to benefit from an incremental ~40,000 ounces of gold and ~4.0+ million ounces of silver post-expansion, translating to an additional ~$150 million in annual revenue even at conservative metals prices. And while this pivot back to positive free cash flow won't benefit shareholders as it will go to taking care of the company's heavy debt load, investors can at least breathe a sigh of relief that the cash burn and share dilution is in the rear-view mirror and the hedges that weighed on revenue generation will roll off at year-end.

So, what's a fair value for the stock?

Given Coeur's track record of consistent share dilution and its weaker operating portfolio relative to some of its peers, I think a discounted multiple to its peer group is appropriate, and I would argue that a generous multiple is 10.0x forward free cash flow. If we multiply this figure by estimates of ~$150 million in FY2025, this translates to a fair value for Coeur of $1.5 billion. After subtracting ~$360 million in net debt and dividing by 368 million shares (assumes minor share dilution over the next two years), Coeur's fair value comes in at US$3.10 per share. This points to a 48% upside to fair value (2-year target price), which is a decent upside case if one is hoping to get leverage to gold/silver prices. However, I am looking for a minimum 40% discount to fair value when starting new positions in small-cap producers given their higher risk. If we apply this required discount, Coeur's ideal buy zone comes in at $1.85 or lower, suggesting the stock has still not entered a buy zone after its violent correction.

Summary

It's been a tough few years for Coeur Mining and an even tougher stretch for investors in the stock. The only silver lining is that this lifeless performance might serve as a painful lesson that owning sector laggards with poor track records in a cyclical sector is one of the worst strategies one can employ. That said, pessimism on the stock is the worst I've seen it in years and the worst appears to be behind Coeur from a share dilution standpoint. Plus, while the balance sheet leaves a lot to be desired, there's a light at the end of the tunnel when it comes to de-leveraging. So, if I wanted to own CDE, I see the stock as a Speculative Buy at $1.85 from a swing-trading standpoint. However, with a handful of higher-quality names also on the sale rack, I remain focused elsewhere, and this is not a stock I would consider owning outside of a very brief swing trade given the industry-lagging per share metrics.

For further details see:

Coeur Mining: A Light At The End Of The Tunnel