CDE - Coeur Mining: Another Year Of Above-Average Share Dilution

2023-03-16 06:13:56 ET

Summary

- Coeur Mining is one of the worst-performing precious metals stocks this year, down 11% vs. a 1% gain for the Gold Miners Index.

- The underperformance isn't surprising given that CDE has hedged a large portion of output & was once again one of the worst offenders last year from a share dilution standpoint.

- Fortunately, Rochester POA 11 is nearly complete and this will translate to material growth in 2024 at lower unit costs, allowing CDE to transition back to free cash flow positive.

- However, with a track record of considerable share dilution, another high-cost year ahead and Rochester POA 11 being a 2024 story, not 2023, I continue to see CDE as an inferior way to play the sector.

The Q4/FY2022 Earnings Season for the Gold Miners Index ( GDX ) is nearing its end, and it was a disappointing year overall. While several companies delivered on production, several producers missed cost guidance. And many by a country mile, like Equinox Gold ( EQX ) and SSR Mining ( SSRM ). This was mostly because of inflationary pressures, exacerbated by lower output because of COVID-19 related exclusions, supply chain headwinds, labor tightness, and extreme weather in some jurisdictions. The result was that sector-wide all-in-sustaining costs (AISC) soared 15% to ~$1,300/oz, and on a two-year basis (FY2022 vs. FY2020), AISC margins fell over 30% to ~$500/oz.

While Coeur Mining ( CDE ) was smart to hedge last year to help it weather the storm, its costs rose considerably at several assets, and it saw another year of deeply negative free cash flow. This was, of course, related to significant capital spending at its Rochester Expansion. However, it hasn't helped that costs have increased ~65% from early estimates and while this was out of its control; the company had one of the worst track records of share dilution year-over-year despite divesting a portion of its development portfolio. So, with a track record of considerable share dilution, another high-cost year ahead and Rochester POA 11 being a 2024 story, not 2023, I continue to see CDE as an Avoid. Let's dig into its 2022 results and 2023 outlook below:

{kind=link}

Q4 & FY2022 Production

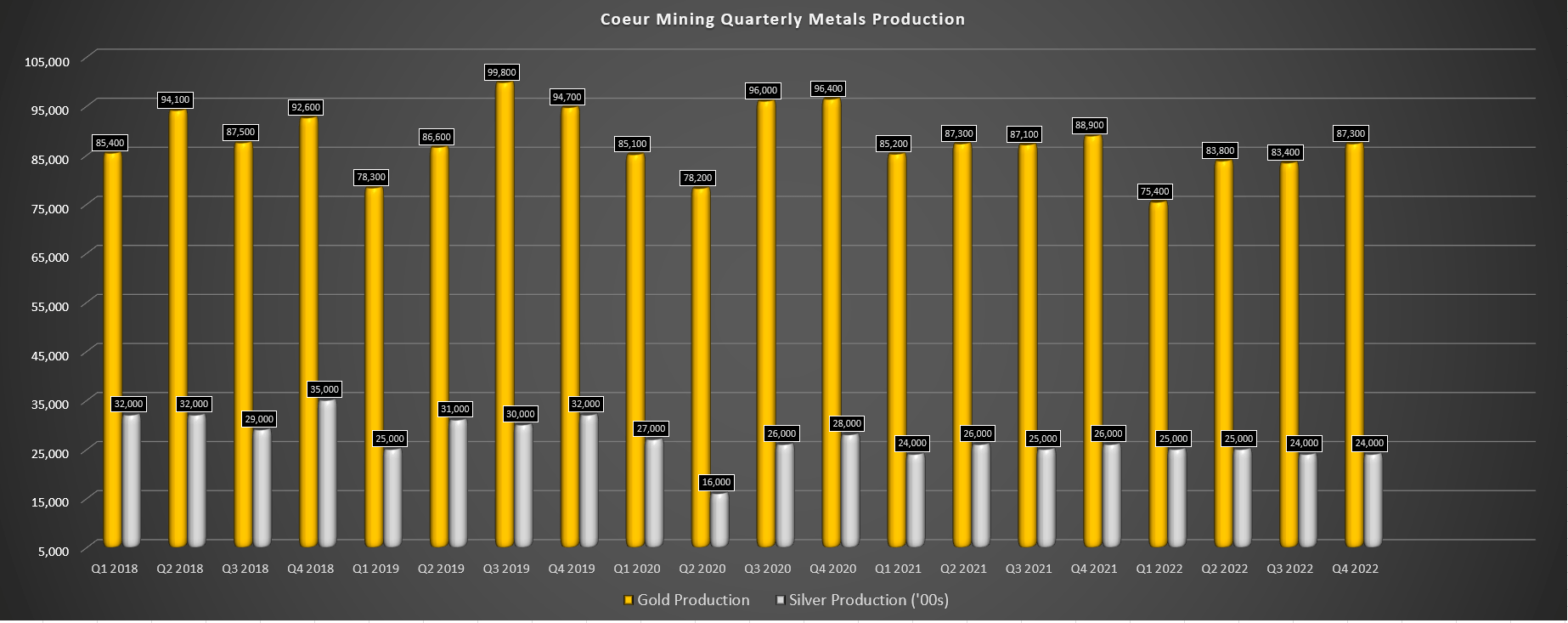

Coeur Mining released its Q4 and FY2022 results last month, reporting quarterly production of ~87,700 ounces of gold and ~2.4 million ounces of silver. This represented a 1% and 8% decline respectively on a year-over-year basis, impacted by lower production from Palmarejo (lower grades and throughput) and Kensington (lower grades). The result was that gold production came in marginally below its FY2022 guidance mid-point (~334,000 ounces) at ~330,300 ounces, and silver production also came just shy of its guidance mid-point at ~9.8 million ounces vs. a 10.0 million ounce mid-point. However, the bigger disappointment was from a cost standpoint, which we'll look at later.

Coeur Mining - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

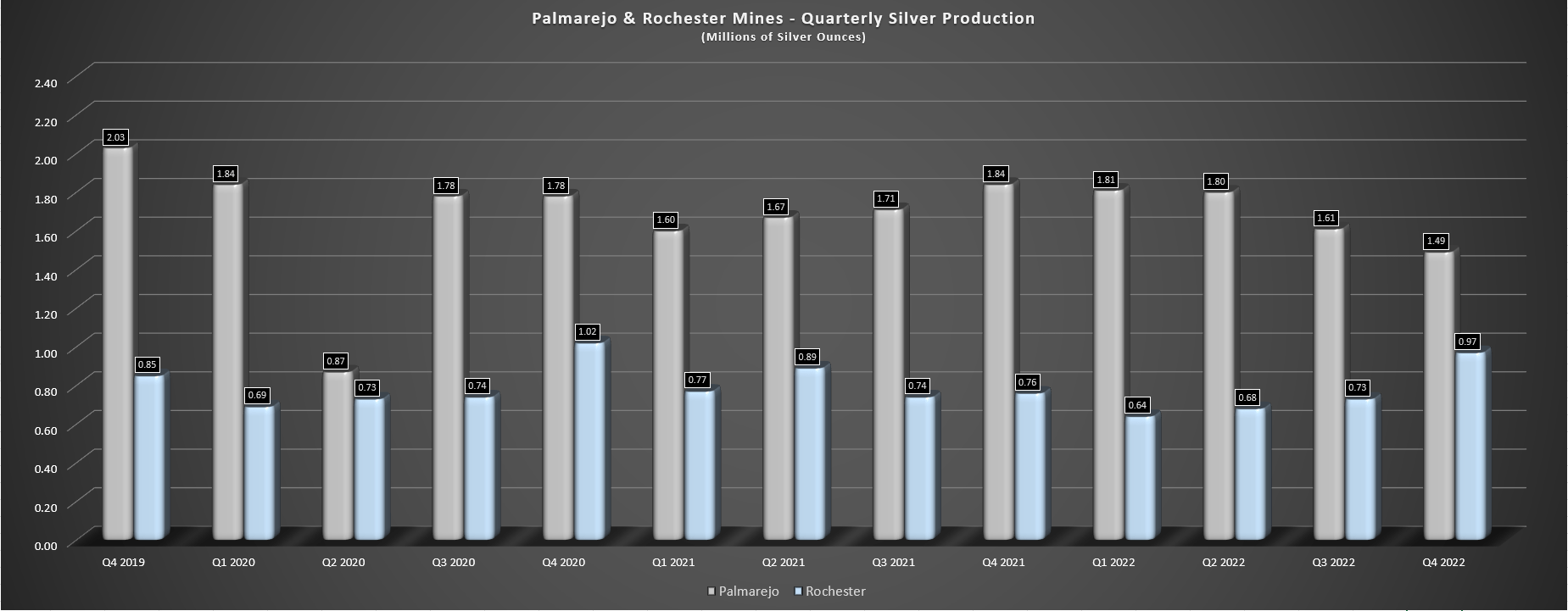

Digging into silver production first, we can see that silver production continues to trend lower at Palmarejo due to lower grades, with just ~1.49 million ounces produced in Q4 2022, the weakest quarter for the mine in the past three years outside of Q2 2020 which was impacted by COVID-19 related disruptions. Fortunately, Rochester picked up some of the slack because of higher grades in Q4, producing ~973,000 ounces of silver, a ~29% increase from the year-ago period. Although Palmarejo's silver production should be relatively flat next year based on FY2023 guidance, we will see increased production at Rochester, with guidance of 4.0 million ounces (FY2022: ~3.06 million ounces of silver), though production will be second-half weighted (POA 11 Expansion completion and commissioning).

Coeur Mining - Silver Production by Mine (Company Filings, Author's Chart)

{kind=link}

Moving over to gold production, we saw another decline in annual production at the company's flagship Palmarejo Mine, impacted by a slightly lower average grade of 0.053 ounces per ton gold and slightly lower recovery rates (92.1% vs. 92.8%). The result was that annual production declined by 2% (~106,800 ounces vs. ~109,200 ounces) despite increased tons milled, leading to higher costs at the operation when combined with inflationary pressures. As for its two gold-only operations in Alaska and South Dakota, output fell 10% at Kensington and 12% at Wharf, with both operations struggling to maintain production levels despite increased throughput (Wharf) due to lower grades. Similar to Palmarejo, this led to much higher costs and a decline in free cash flow year-over-year.

{kind=link}

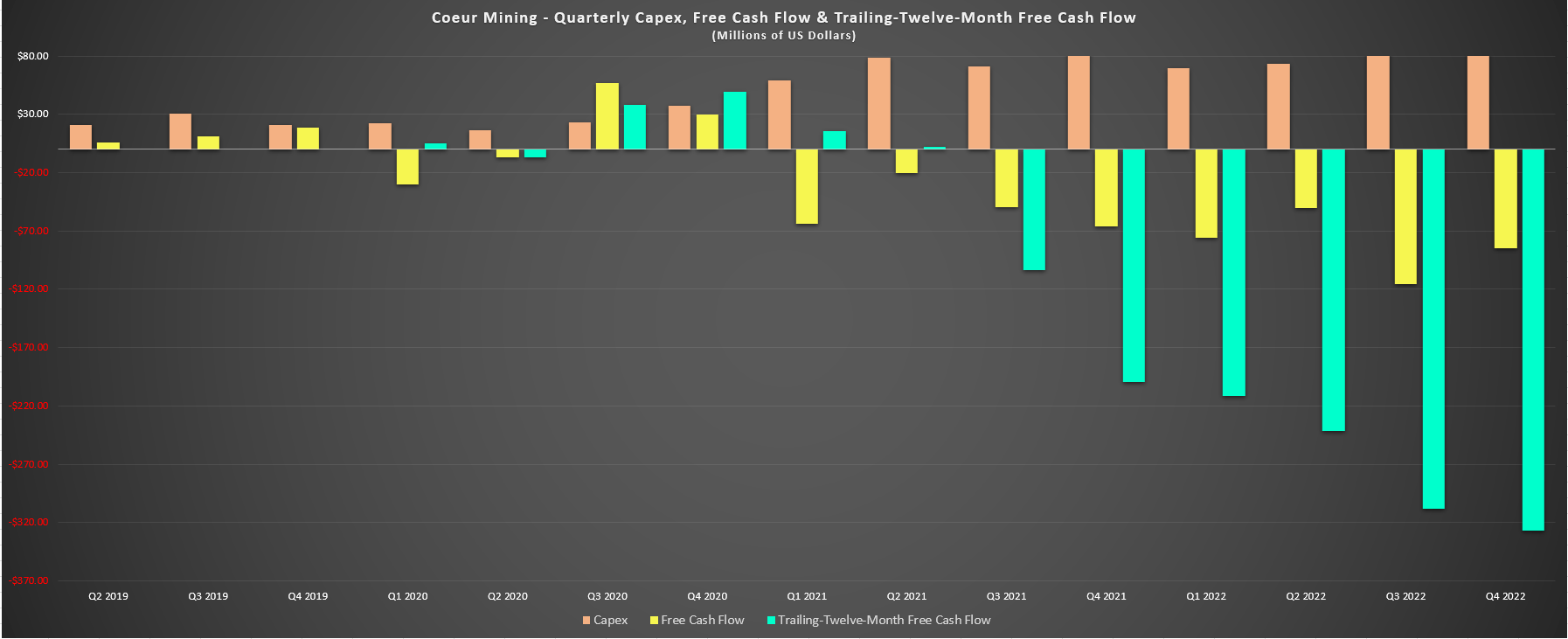

Given the sharp increase in capital expenditures (Q4: $113.1 million, FY2022: $352.4 million) due to the Rochester Expansion, lower profitability due to higher operating costs, and lower sales volumes, Coeur's saw a cash outflow of $84.5 million in Q4 2022 and $326.7 million in FY2022, a significant increase over year-ago levels ($65.9 million and $199.3 million, respectively). The result was that the company was forced to use its At-The-Market equity program twice in the year and divest its Victoria Gold shares plus its Nevada development properties to ensure sufficient liquidity to complete the Rochester Expansion. And despite these divestments and equity sales, the company still ended the year with net debt of ~$454 million, up from ~$431 million at year-end 2021.

Coeur Mining - Quarterly Capex, Free Cash Flow & Trailing Twelve Month Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Costs & Margins

Moving over to costs and margins, Coeur's adjusted costs applicable to sales [CAS] per gold ounce soared to $1,300/oz in FY2022, a 33% increase from the year-ago period. A bulk of this increase was from Palmarejo where adjusted CAS per gold ounce increased to $883/oz (FY2021: $663/oz) impacted by strength in the Mexican Peso and inflationary pressures felt sector-wide, plus the impact of lower sales volumes despite increased tons processed. Meanwhile, at Rochester, adjusted CAS per gold ounce soared to $2,269/oz vs. $1,691/oz and this was despite the benefit of higher sales volumes. On a silver basis, the results weren't much prettier, with adjusted CAS per silver ounce increasing to $25.74/oz (FY2021: $23.57/oz). The result was that the Nevada mine reported operating cash flow of (-) $48.0 million, a further decline from FY2021 levels.

{kind=link}

Given the significant increase in costs at its top two operations with higher costs at its other two operations as well and only a slight increase in gold prices due to favorable hedging, FY2022 CAS margins per ounce slid 35% to $436/oz on a consolidated basis. Meanwhile, silver CAS margins per ounce were demolished, sliding from $9.36/oz to just $4.77/oz with the bulk of this impact from weaker average realized silver prices ($21.77/oz vs. $25.66/oz). While it's positive to see that metals prices are sitting above 2022 average prices currently, Coeur has guided for much higher costs year-over-year at Kensington and Palmarejo and relatively flat costs at Wharf, suggesting we'll see further margin compression year-over-year if metals prices don't continue to cooperate and remain at favorable prices.

As noted in its prepared remarks, Coeur Mining has hedged ~180,000 ounces of gold at $1,961/oz and ~2.3 million ounces of silver at $24.50/oz, providing it some protection against downside volatility in metals prices, but also capping its upside.

Overall, Coeur did a decent job of coming near meeting its guidance in FY2022 but the bar was set pretty low and margins declined considerably year-over-year despite delivering into its guidance range. Worse, in regards to things Coeur can control, it was one of the worst offenders yet again from a share dilution standpoint sector-wide, with it currently having ~296 million shares, up from ~255 million shares in the same period last year. Importantly, this continues a long streak of above-average share dilution, so this isn't a one-off while the company works to complete a major capital project. In fact, Coeur has seen a double-digit compound annual growth rate in its share count since 2012, explaining its terrible share price performance in the period with production per share held dropping like a stone. Let's look at the stock's valuation following the recent decline:

{kind=link}

Valuation

Based on ~296 million shares and a share price of US$3.10, Coeur trades at a market cap of $887 million and an enterprise value of ~$1.34 billion. This might appear to be a cheap valuation for a company producing over 450,000 gold-equivalent ounces (GEOs) from mostly Tier-1 jurisdictions, but as noted earlier, Coeur is one of the higher-cost producers sector-wide, and costs continue to rise at its lower-cost Palmarejo Mine as grades steadily decline at the asset. The hope is that the Rochester POA 11 Expansion will pull consolidated unit costs lower while providing material growth in output, but at least for the time being, this is a producer with a track record of serially diluting shareholders with a cost profile that leaves much to be desired.

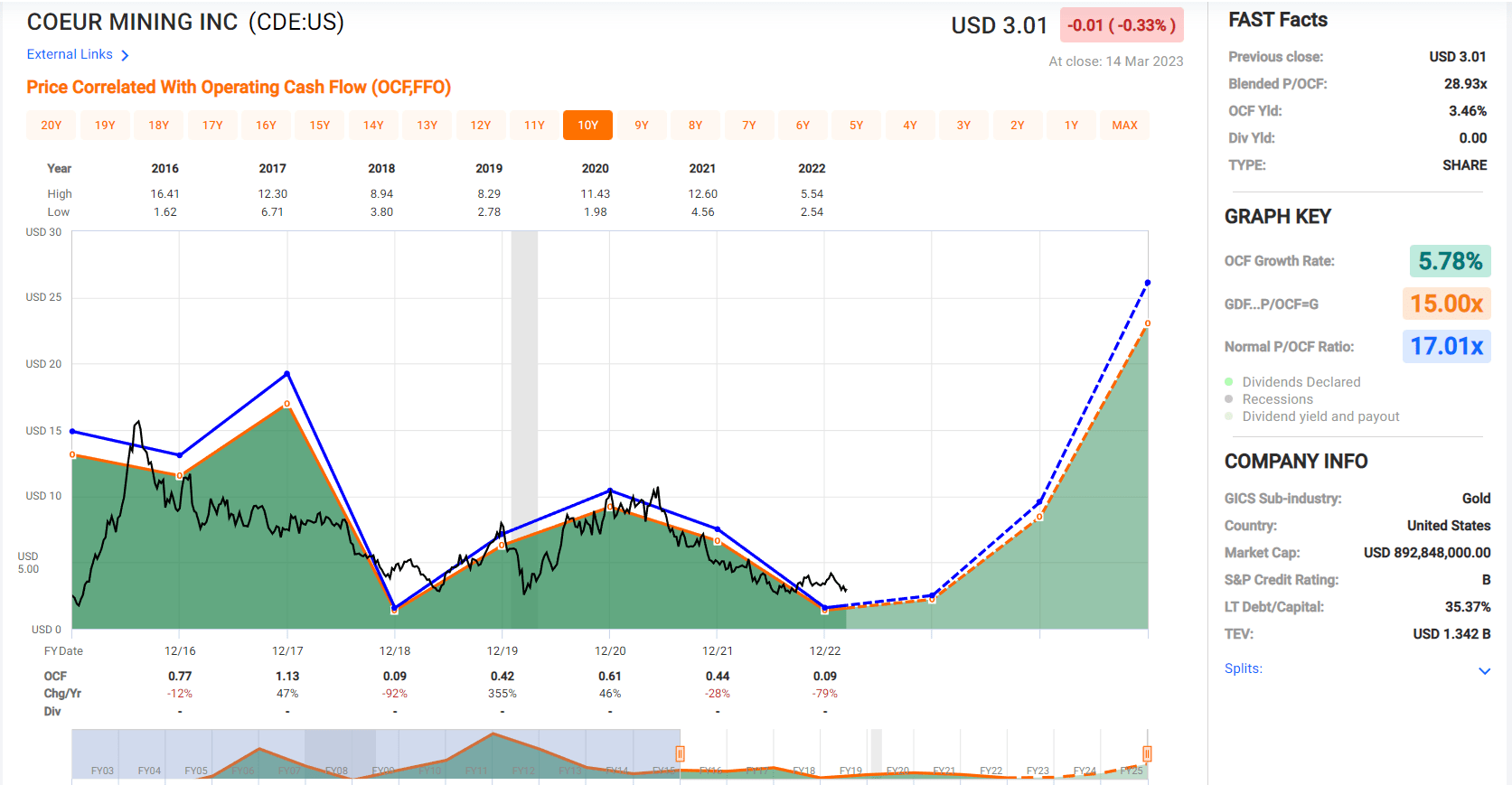

Coeur Mining - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

If one looks at Coeur's historical cash flow multiple (13.7), they might conclude that Coeur is undervalued, but I would disagree. Not only is this historical multiple rich for any producer in the sector, it's a very rich multiple for a high-cost producer like Coeur. Using what I believe to be a more reasonable multiple of 6.0 to reflect industry-lagging margins and conservative FY2024 cash flow per share estimates of $0.52, I see a fair value for Coeur of $3.12. If we add $160 million in value ($0.54) to its Silvertip Project (British Columbia), this translates to a fair value of $3.62. After measuring from the current share price of $3.10, this points to a 17% upside from current levels.

I have used FY2024 cash flow per share estimates to give the company the benefit of its Rochester POA 11 Expansion, which won't be truly reflected in its FY2023 results.

Although this upside case might look attractive, I am looking for a minimum 40% discount to fair value when buying small-cap producers, and certainly those that seeing consistently rising share counts with inferior track records of generating value for shareholders. In Coeur's case, we saw another year of ~15% share dilution (two At-The-Market ATM offerings at a price of $4.53 and $3.39, respectively) and this dilution was despite also disposing of non-core assets to AngloGold Ashanti ( AU ) and taking a loss on Victoria Gold ( VITFF ) acquired from Orion in 2021 as a strategic investment which came at the expense of share dilution at the time (~12.7 million CDE shares).

The only positive was that at least it used expensive shares of its own stock to acquire the Victoria Gold shares that it sold at a loss.

After applying this 40% discount required to start new positions in small-cap producers to what I believe to be a fair value of $3.62 for Coeur Mining, I would need a minimum share price of US$2.17 to become interested in CDE stock where there would at least be a margin of safety. Obviously, there is no guarantee that the stock drops this low, but I want to be compensated accordingly if I'm going to invest in a high-risk, high-reward name. The same is true of First Majestic ( AG ), which I have warned against owning since $16.00 when others were pounding the table to go long, and it's now fallen more than many might have expected when it briefly traded above $20.00 in 2021. So, at current prices, I continue to see CDE as an Avoid in favor of higher-quality names elsewhere.

First Majestic Silver Article - February, 2021 (Seeking Alpha Premium)

{kind=link}

Summary

Coeur Mining had a satisfactory year operationally in 2022 and was one of the few companies with the foresight to hedge which helped it to weather the storm better than some of its other high-cost peers, and certainly better than smaller names that shut down entirely like Pure Gold ( LRTNF ) and Great Panther ( GPLDF ). That said, 2023 will be another high-cost year, and Coeur will benefit less than its peers from gold/silver price upside given the significant hedging it's done to ensure sufficient liquidity for the nearly completed Rochester Expansion. Obviously, the Rochester Expansion is a key catalyst that will transition CDE back to free cash flow positive, but this is a 2024 catalyst.

The other issue with owning CDE is that while I see a lower likelihood of share dilution this year, this is a team that continues to dilute each year even with metals prices up considerably from 2019 levels. The result is that it has one of the worst track records of production growth per share sector-wide and I see no point in owning a producer with declining production per share as you are effectively losing leverage to the metal price. In these cases, it's better to own the metal itself. To summarize, I continue to see CDE as an inferior way to play the sector, but if the stock were to dip below $2.20, this would represent an attractive entry from a swing-trading standpoint.

For further details see:

Coeur Mining: Another Year Of Above-Average Share Dilution