CDE - Coeur Mining: Continued Share Dilution Overshadows POA 11 Completion

2023-11-17 02:57:44 ET

Summary

- Coeur Mining's Q3 production declined year-over-year, but there was a significant improvement in October production at the Rochester mine.

- Meanwhile, its costs per silver ounce produced increased meaningfully and its per share metrics continue to lag its peers, affected by ~8% share dilution since August.

- In this update, we'll look at the Q3 results, the stock's updated per share growth outlook, and whether the poor execution finally is priced into the stock after years.

Just over 18 months ago, I wrote on Coeur Mining ( CDE ), noting that the risk of share dilution to fund its planned expansion at Rochester made CDE a name that was best to avoid at US$4.30. And while I was confident that we would see at least 15% share dilution to complete Rochester in an inflationary environment which would weigh on share-price returns, the outcome has been far worse. This is because we've seen nearly 50% share dilution (~257 million --> ~383 million shares since Q4-2022) on top of the sale of equity investments at a loss, and the sale of two development projects initially purchased in 2018 that were supposed to be a source of "high margin production".

Simultaneously, Coeur's cost profile has increased materially because of inflationary pressures, and its per share metrics continue to lag the industry with the expected growth from POA 11 being more than offset by the share dilution we've seen since project construction began. In this update, we'll look at the Q3 results, the stock's updated per share growth outlook, and whether the poor execution finally is priced into the stock after years of underperformance.

Rochester Mine - Company Website

{kind=link}

Q3 Production & Sales

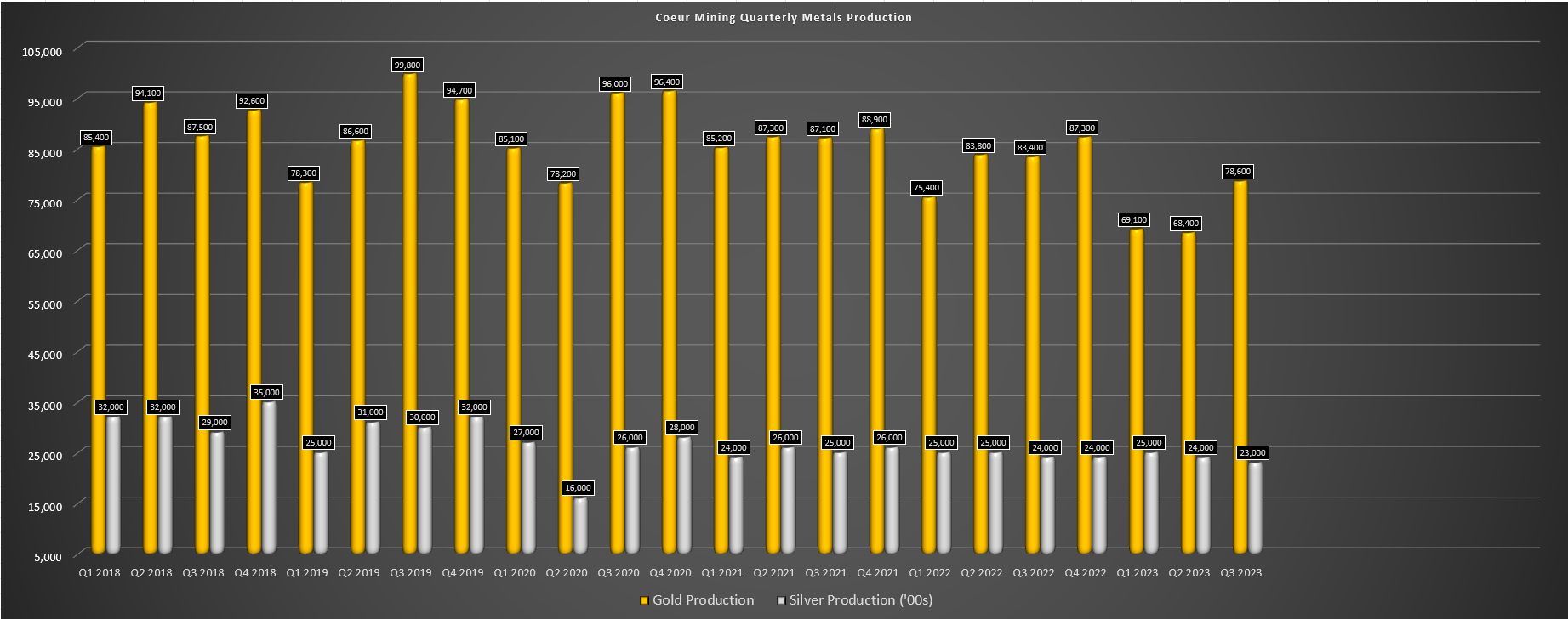

Coeur Mining ("Coeur") released its Q3 results last week, reporting quarterly production of ~78,600 ounces of gold and ~2.3 million ounces of silver, a ~5% and ~4% decline from the year-ago period. Coeur's prepared remarks lauded the sequential improvement, but production was down year-over-year despite Coeur being up against easy year-over-year comparisons (production was down 4% in the year-ago period vs. Q3 2021), and was only up sequentially because it was coming off the worst quarter in five years for gold production (~68,400 ounces). This lower production in Q3 on a year-over-year basis was attributed to the timing of production on the new leach pad at Rochester plus declining grades at Kensington (0.16 ounces per ton vs. 0.18 ounces per ton). Fortunately, this was partially offset by a better quarter from Palmarejo, and Wharf also had a decent quarter with higher grades vs. Q3 2022.

Coeur Mining Quarterly Metals Production - Company Filings, Author's Chart

{kind=link}

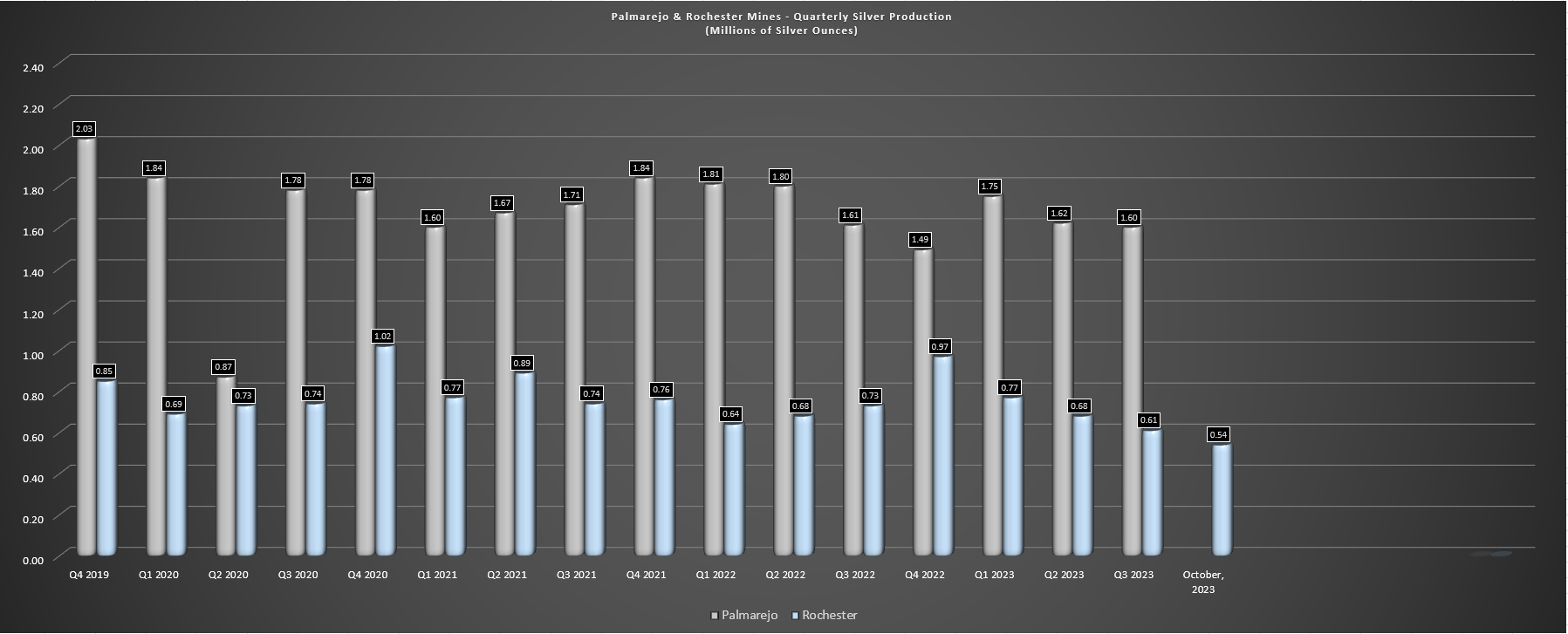

Digging into the results a little closer, Palmarejo produced ~26,900 ounces of gold (+8% year-over-year) and ~1.6 million ounces of silver (flat year-over-year) on the back of better gold grades and recovery rates, and its high compression thickener and open pit backfill project were completed ahead of schedule and under budget. This is certainly a welcome after an ~80% capex blowout at Rochester (~$400 million ---> ~$720 million). That said, adjusted costs applicable to sales were meaningfully higher for silver ($15.56/oz vs. $12.67/oz) which offset marginally lower costs for gold, and while its costs of $917/oz were low, margins remain below the industry average because of an average selling price of $1,499/oz (impact of the gold stream). The company noted that rising costs were partially related to a stronger Mexican Peso, which certainly doesn't help with 2024 expected to be a lower grade per the 2021 TR.

Coeur Mining Quarterly Silver Production - Company Filings, Author's Chart

{kind=link}

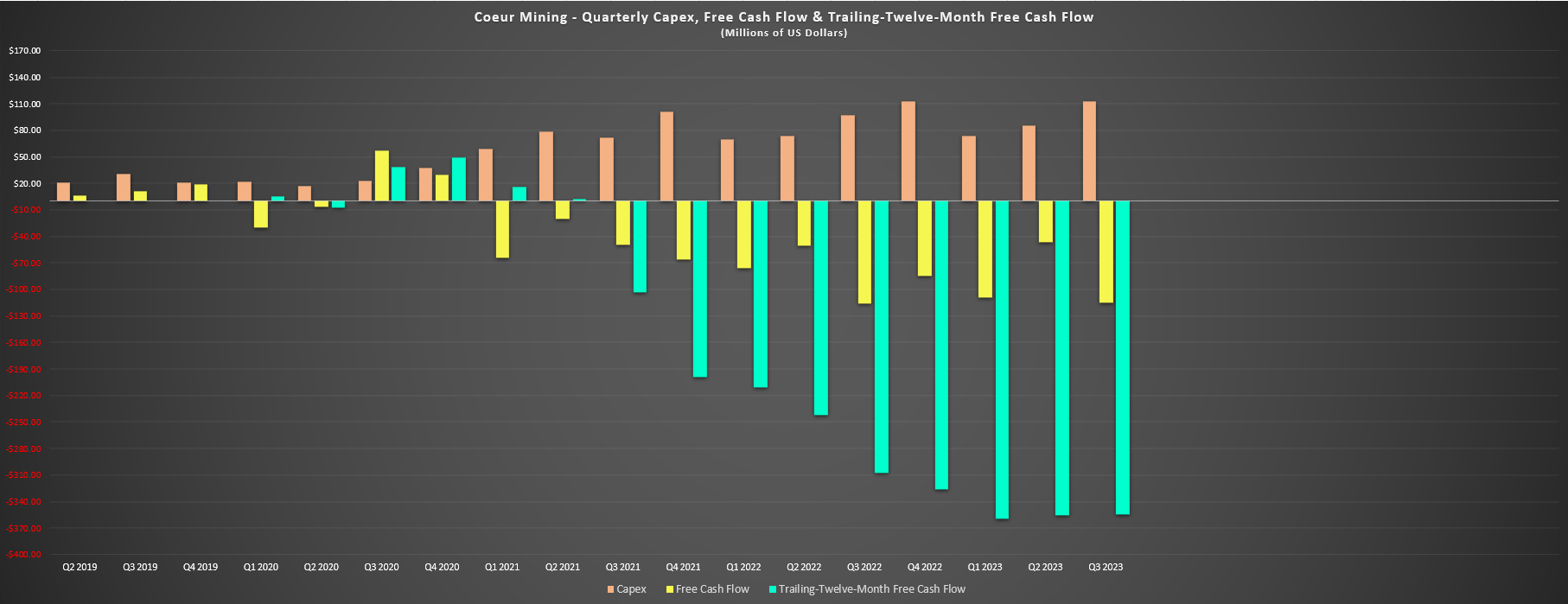

Moving over to Rochester, we can see that silver production was down year-over-year and sequentially to ~608,000 ounces, but we saw a significant improvement in production in October. In fact, October silver production at the mine was ~537,000 ounces, nearly matching all the production from Q3, while gold production was ~8,100 ounces of gold, above Q3 levels. So, with the Rochester Expansion finally complete (first production from new leach pad and process plant in September and commissioning of the new crusher corridor underway), Q4 and 2024 will see much higher production from this Tier-1 jurisdiction asset. In fact, production should increase to at 1.5 million ounces per quarter and 11,000 ounces of gold, a considerable improvement from ~608,000 ounces and ~4,500 ounces in Q3, respectively. In addition, free cash flow will flip to positive vs. trailing-twelve-month free cash outflows of ~$330 million at Rochester during this capital-intensive phase for the asset.

Coeur Mining - Quarterly Capex, Free Cash Flow & TTM Free Cash Flow - Company Filings, Author's Chart

{kind=link}

As for the company's financial results, revenue came in at $194.6 million (entirely thanks to higher metals prices) and operating cash flow improved to [-] $2.4 million vs. [-] $19.4 million last year. Meanwhile, free cash flow came in at [-] $114.7 million on higher capex, and the company ended the period with ~$460 million in net debt. This continues to leave Coeur as one of the more leveraged producers and certainly more vulnerable than names like Sandstorm Gold ( SAND ) that may also be leveraged with over $300 million in net debt. However, in SAND's case, it is protected from inflation (royalty/streaming model) and is insulated from commodity price weakness because of its business model. Hence, while Coeur may look cheap, it is certainly a riskier bet with a weak balance sheet and relatively low margins.

Costs & Updated FY2023 Guidance

Moving over to costs, Coeur reports costs applicable to sales of $17.85/oz for its silver segment, a significant increase from $14.52/oz in the year-ago period. As noted previously, this was partially related to the stronger Mexican Peso at Palmarejo and inflationary pressures sector-wide, in addition to lower metal sales. As for gold, Coeur's costs came in at a more reasonable level of $1,273/oz, down slightly from $1,318/oz in the year-ago period. However, this still translated to margins of just $515/oz on an adjusted CAS basis (~29%) due to the impact of its gold stream on its average realized selling price. And while these margins were up year-over-year and cash flow improved, the company still reported a net loss of $18.6 million and only managed to hold the line on net debt levels due to significant share dilution. In fact, the company saw its share count increase by ~8% in the period despite the benefit of near-record gold prices and in a period where other producers are aggressively buying back shares like SSR Mining ( SSRM ).

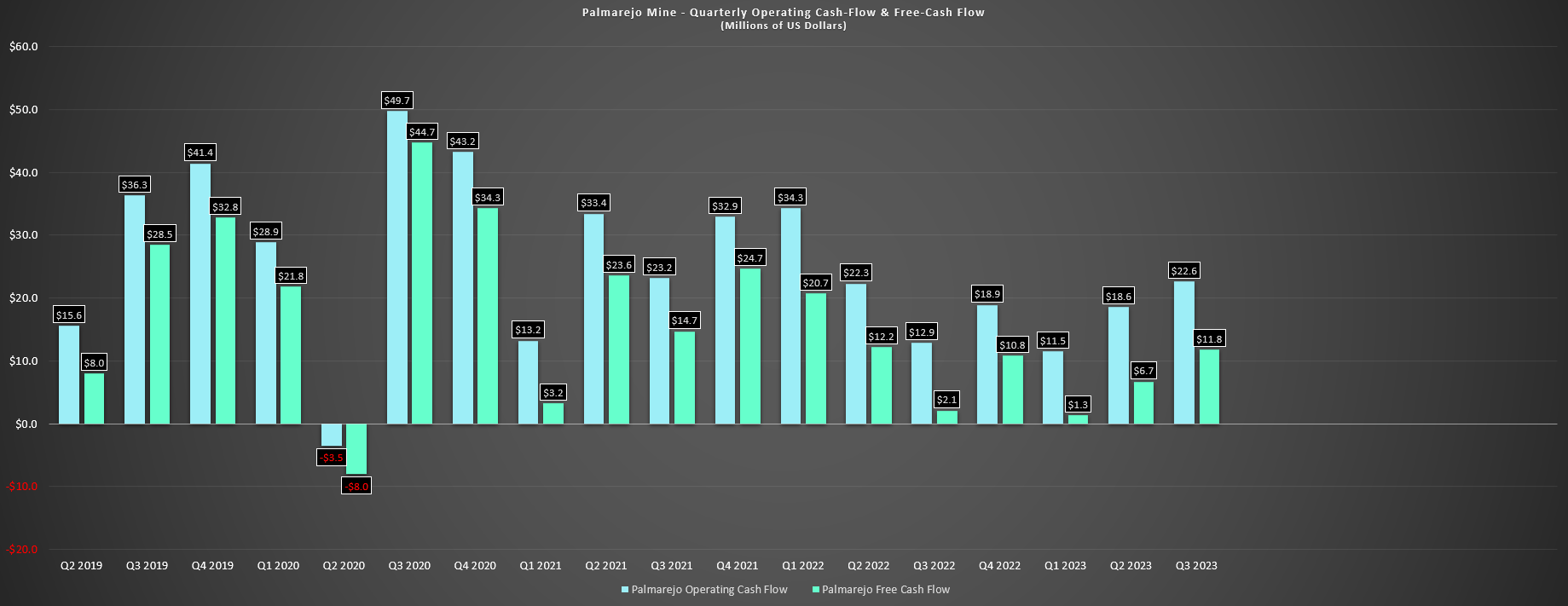

Palmarejo - Quarterly Cash Flow & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

On a positive note, Palmarejo did generate free cash flow in the period despite headwinds from a stronger Peso, and the company continues to work on building a pipeline of new targets to reduce its stream obligations by hopefully adding new reserves outside of Franco-Nevada's ( FNV ) area of interest. The other positive note of course is that Coeur's costs will improve next year with the meaningful step up in production at Rochester, suggesting that while 2023 will be another relatively low-margin year, 2024 could be much better, especially if gold prices cooperate. Let's look at the valuation below to see whether the stock is worth paying up for above $2.50 per share.

Valuation

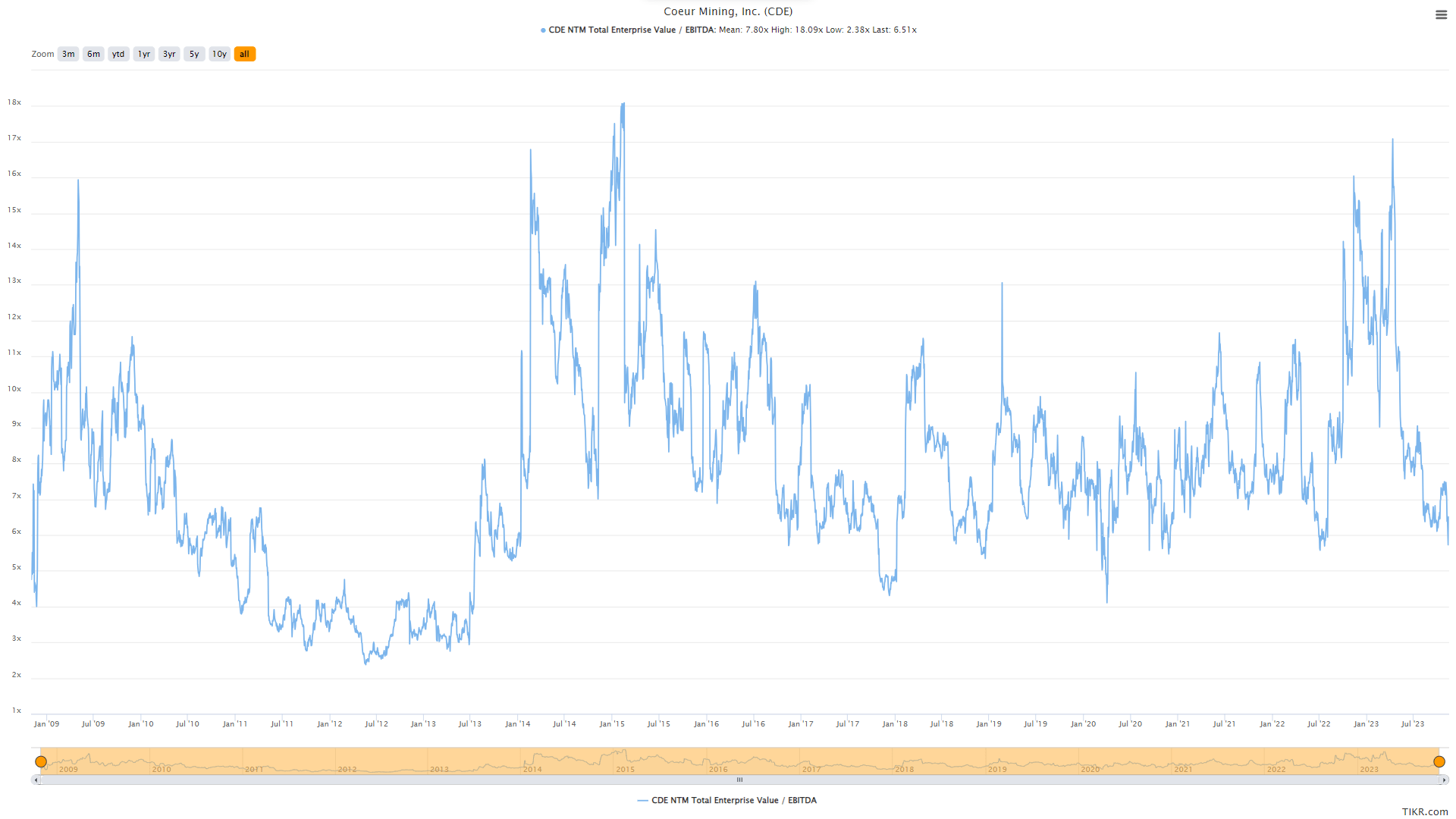

Based on ~384 million fully diluted shares and a share price of US$2.53, Coeur trades at a market cap of ~$970 million and an enterprise value of ~$1.43 billion. This leaves the company trading at a discount vs. many of its peers with silver exposure at just 0.66x P/NAV vs. an estimated net asset value of ~$1.46 billion. Meanwhile, the stock also trades at a reasonable valuation from a forward EV/EBITDA standpoint, below its 10-year average EV/EBITDA multiple of ~7.8x. That said, and as I've argued in past updates, Coeur is a value trap. The reason is that it consistently sits atop the leaderboard for share dilution among its peers, diluting shareholders by nearly 300% since 2013 and ~100% since 2018 during a 60% rise in the gold price and with the benefit of a silver squeeze (when it would have been a wise time to raise significant capital through its ATM or a bought deal vs. selling at progressively lower prices as it has over the past 30 months). Meanwhile, its portfolio is mediocre, even if concentrated in better jurisdictions, with the best asset encumbered by a massive gold stream, and its cost profile is well above the gold producer average (bulk of Coeur's revenue comes from gold).

CDE NTM EV/EBITDA Multiple - TIKR.com

{kind=link}

Some investors might argue that this share dilution is all in the past and that taking a rear-view mirror approach towards Coeur could be a mistake. However, I would strongly disagree with this view, given that the same management is in place that contributed to industry-leading share dilution and questionable allocation of capital (outbidding a peer for La Preciosa which was sold at a massive loss, acquiring Silvertip, where it took a ~$250 million impairment, a strategic equity investment during a period of elevated capex only to sell at a loss). In addition, while the share dilution might finally be in the rear-view mirror, this doesn't mean that there isn't permanent damage from this dilution to the company's per share metrics. And as the chart below shows, unless Coeur plans on buying back over 100 million shares despite it being one of the more leveraged producers (over 4.0x net debt to EBITDA), the company will maintain one of the worst trends for production growth per share sector-wide.

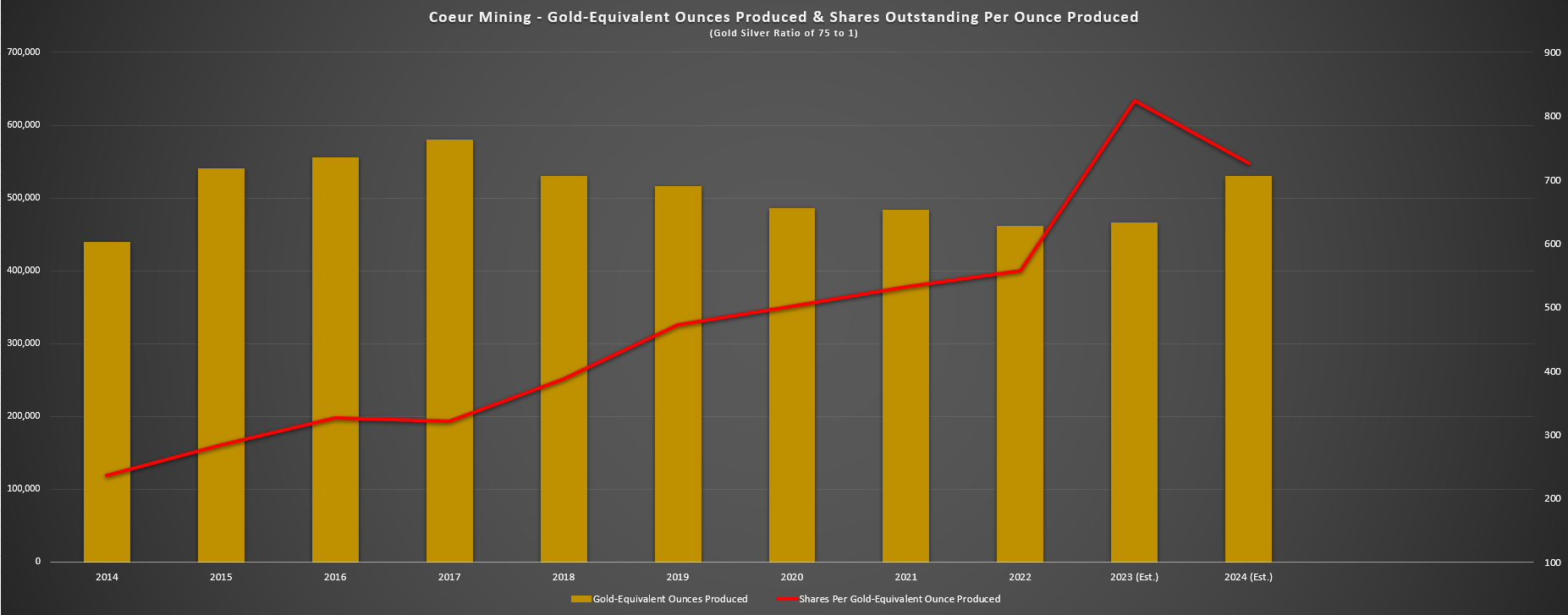

We highlight the latter point in the below chart, showing that investors in Coeur during 2014 previously needed to hold just ~250 shares to get exposure to each ounce of gold-equivalent production. As of this quarter, that figure has risen to nearly 800, meaning that investors have got massive negative leverage to metals prices with their exposure to production down over 60% in the period given that production is actually down while the share count is up ~150% and this is despite selling off projects recently (Sterling/Crown, La Preciosa) which should have reduced the rate of share dilution. In the same period, the best producers like Agnico Eagle ( AEM ) have meaningfully grown production, reserves, cash flow, and dividends per share. And as I've noted in past updates, there is no reason to invest in a producer that cannot at least hold the line on per share metrics.

Coeur Mining - Annual GEOs Produced, Shares Outstanding Per GEO Produced & Forward Estimates - Company Filings, Author's Chart & Estimates Coeur Mining Shares Outstanding - FASTGraphs.com

{kind=link}

{kind=link}

Plus, even if we include expected growth from Rochester POA 11 in 2024/2025 when GEO production increases to ~540,000, production per share will still be down meaningfully since it approved the project. This means that while Coeur may see higher revenue, cash flow, and a longer mine life, there's no benefit to patient shareholders as it's been diluted away. Finally, for teams that have made multiple questionable moves in the past, it's hard to rule out further destruction of value going forward, meaning that higher metals prices may not help as much as hoped if it leads to another dilutive acquisition. Hence, I would much prefer to own producers that are being aggressive in the current environment in the lower portion of the cycle with a proven track record vs. betting on a "fair" business at a "wonderful" price, which Buffett has consistently warned against.

So, where would CDE become worthy of buying?

Using what I believe to be a generous multiple of 9x free cash flow given the track record here and even using 2-year forward estimates to be generous (FY2025) of ~$175 million, I see a fair value for the stock of ~$1.32 billion. If we divide this figure by ~392 million fully diluted shares and add expected net debt, this translates to a fair value of US$3.35. Although this translates to a 37% upside from current levels, I am looking for a minimum 40% discount to fair value to justify entering new positions in small-cap cyclical stocks, and ideally closer to 50% for sector laggards. Hence, even if we use the low end of this required discount, CDE's ideal buy zones comes in at US$2.02 or lower, suggesting the stock is now well outside of its low-risk buy zone after its recent rally.

Summary

Coeur Mining had a better Q3 sequentially, and while we did not see the fruits of multiple years of growth capex at Rochester in the quarter, we saw a significant tick higher in production in October, and we should see production of at least 530,000 GEOs in 2024. However, while production was in line with my expectations, I did not expect to see another half-year period with high single digit share dilution (share count grew from ~353 million to ~383 million shares from August to November), and this put a further dent in already underwhelming per share metrics. Hence, with CDE remaining a serial diluter with a low probability of being acquired because of a mediocre portfolio, I continue to see the stock as un-investable, and one of the least attractive ways to get exposure to precious metals. That said, if the stock were to decline below US$2.02 before February, I would view this as an opportunity to go long from a swing-trading standpoint.

For further details see:

Coeur Mining: Continued Share Dilution Overshadows POA 11 Completion