PFE - Cogent Biosciences: Multiple Inflection Points For FY23 Hold For Now

Summary

- Cogent Biosciences, Inc. is building momentum around its bezuclastinib compound.

- FY22 saw a number of positive advancements of the company's pipeline.

- The price response to these updates hasn't held into the final stages of the year, however.

- There are multiple inflection points to keep an eye out for in FY23, namely readouts from the PEAK and SUMMIT trials.

- Despite this, current broad market fundamentals command a defensive outlook to equities in our opinion; hence, we rate COGT a hold right now.

Investment Summary

Investigational cancer drugs have caught the eye of many savvy healthcare-focused investors over the last 5 years. Adding to that, clinical trial momentum has been building at pace in terms of the breakthrough's made in the segment. One case in this investment debate is Cogent Biosciences, Inc. ( COGT ), a name that continues building momentum around its bezuclastinib compound. Here I'll present our examination findings for COGT, after an extensive review of the company's primary offering and treatment market.

As a reminder, COGT is a clinical stage biotech firm dedicated to the development of targeted therapies for genetically defined illnesses. It has several investigational pathways currently in situ, searching for a medical breakthrough in these complex disease segments. This year has been a positive step for the company, with its research team working diligently to fulfil its study mandates for bezuclastinib. However, despite several positive updates, the price response has been relatively mute for COGT stock in H2 FY22', despite its ~26% YTD gain on the chart.

Net-net, we are constructive on COGT. However, in our opinion, there's still a number of hurdles the company must overcome in order to command a full-position. Hence, we rate COGT a hold.

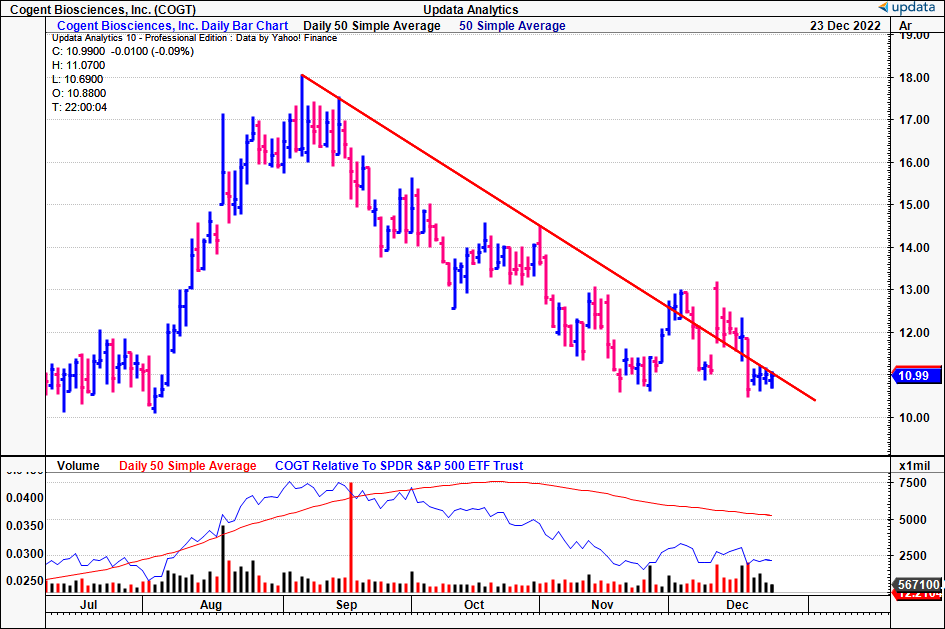

Exhibit 1. COGT daily price action, July 2022–date

{kind=link}

Catalysts to move the needle – clinical trial tailwinds

Primary conditions currently under investigation

It would be first prudent to discuss the various conditions the company is targeting with its clinical pipeline. As mentioned, COGT's foremost program is bezuclastinib, also known as CGT9486 . It targets exon 17 mutations found on the KIT receptor, itself responsible for the encoding of tyrosine kinase. Bezuclastinib is a selective tyrosine kinase inhibitor, designed to inhibit the KIT D816V mutation, as well as other KIT exon 17 mutations. For reference, an exon is a segment of DNA or RNA containing the information for a peptide sequence, whereas tyrosine kinase genes link with cellular growth factors and growth hormones.

The KIT D816V mutation is also the driving force behind systemic mastocytosis ("SM"), a severe disease caused by uncontrolled proliferation of mast cells, in the overwhelming majority of cases. If you weren't aware, mast cells are key players in our immune systems, involved in the inflammatory response to invading pathogens. They excrete lysosomes, which are responsible for the breakdown of the harmful bacteria invading the body's cells. Alas, SM is a condition characterized by an extensive list of symptoms, ranging from abdominal pain, diarrhea, gastroesophageal reflux, to shortness of breath.

These same exon 17 mutations are also found in patients suffering from advanced gastrointestinal stromal tumors ("GIST"), a cancer type reliant on oncogenic KIT signaling. Therefore, as a highly selective and potent KIT inhibitor, bezuclastinib aims to provide a novel treatment option for these patient groups as well.

Recent clinical developments

It's also worth noting that COGT is also pushing to develop a suite of targeted therapies initially targeting FGFR2 and ErbB2, two genes involved in cell division and neuron development respectively. For example, it is investigating the development of bezuclastinib for patients with advanced systemic mastocytosis ("ADVSM") in its APEX clinical pipeline . Here, it will be competing with Blueprint Medicines' ( BPMC ) Ayvakit , also indicated in GIST.

Recently, COGT announced positive clinical data from its Phase 2 APEX trial. Specifically, it noted an 89% overall response rate ("ORR") in tyrosine kinase inhibitor-therapy naïve patients, and a 73% ORR in patients after 27-week follow-up [n=28]. Meanwhile it is performing the same investigational studies for bezuclastinib for non-advanced systemic mastocytosis ("Non-ADVSM") in the Phase 2 SUMMIT trial.

This is an interesting hypothesis for COGT, as the vast majority of ADVSM and Non-ADVSM patients have a KIT D816V mutation as well. Unlike SM, where life expectancy isn't generally impacted, ADVSM patients have a greatly reduced lifespan, with a median survival of less than 3.5 years. For patients with Non-ADVSM, there are no approved therapies available, and, while their lifespan is also not impacted by the disease, these patients suffer from a poor quality of life and desperately need new treatment options. Hence, there is a demand for a medical breakthrough in this broad segment.

PEAK 3 momentum an additional catalyst

Based on data from the PEAK trial's lead-in study, Cogent has initiated the randomized portion of the study using a 600 mg dose of a new formulation of bezuclastinib, which demonstrated clinical exposure equivalent to the 1,000 mg original formulation in the company's GIST Phase 1/2 clinical trial.

This will form the underlying dosage for the Phase 3 PEAK clinical tria l. The Phase 3 trial is a multi-part study that will enroll around 426 patients. The first part will consist of two evaluations, including:

- Confirming the dose of the updated formulation of bezuclastinib; and

- Evaluating drug-to-drug interactions between bezuclastinib and Pfizer's ( PFE ) sunitinib [brand name, Sutent].

With respect to the second part:

- It will enroll ~388 patients who are intolerant to, or who have failed prior treatment with imatinib [brand name Glivec, also a tyrosine kinase inhibitor]; and

- Investigate the efficacy of bezuclastinib plus sunitinib, versus sunitinib alone. Patients are set to be randomized in a 1:1 manner.

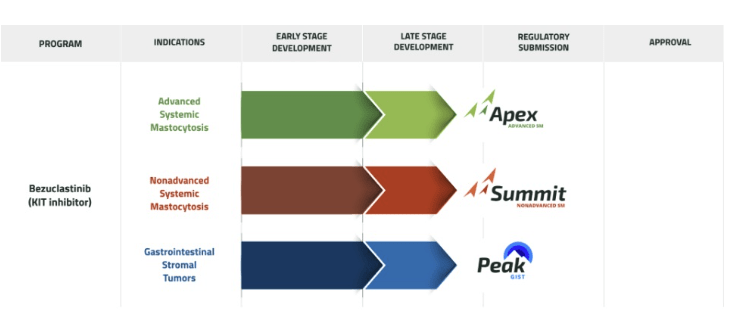

Investors can expect readouts from the PEAK and SUMMIT trials in H1 and H2 FY23' respectively, and so these would be key inflection points to watch out for. You can see COGT's full clinical pipeline in the image below.

We'd also point investors to Needham's recent buy rating on COGT , premised on the company's PEAK and SUMMIT trial momentum. Analysts at the firm project $1.3Bn in sales for bezuclastinib in 2030, with the view it can outperform BPMC's Ayvakit. Note, it also forecasted $1.2Bn for Ayvakit sales in 2030.

Exhibit 2. COGT clinical pipeline, showing Apex, SUMMIT and PEAK trials for bezuclastinib

{kind=link}

COGT liquidity

Being a clinical stage biotech, it's quintessential to examine the company's liquidity and access to capital. Back in May, the company filed a shelf-registration authorizing it to sell up to $300mm of equity and debt [either as standalone or in combination]. Moreover, in June, COGT finalized its public offering of ~17.9mm shares at $8.25 per share, where it raised a net total of c.$162mm.

It's also worth highlighting that the company has ~606,000 warrants on issue and ~81,000 shares of series A preferred stock outstanding. The latter is convertible into 20.26mm shares of common stock, and this should be factored into the investment debate going forward.

Following measures taken throughout the year, COGT left the third quarter with $140.5mm in cash and $148.5mm in marketable securities. Up to September 30 2022, it had burnt $89.2mm in cash from operations [Exhibit 3]. This is coupled with a $153.1mm outflow for the purchase of additional fixed property, plant and equipment. Despite the $79mm net cash burn for the 3 months, management believe the cash runway is sufficient to last until FY25.

Exhibit 3. COGT consolidated cash flows, Q3 FY22

Data: COGT Q3 FY22 10-Q, pp. 25, see: "Liquidity and Capital Resources"

Valuation

We'd note to investors that COGT trades at ~3.4x book value, a range it has held tight across the last 2 years [Exhibit 4]. Note, this is above the S&P 500's price/book ratio of ~1.07x, raising an interesting debate on value creation vs. relative value.

On the one hand, it could be argued that a multiple 3.4x is evidence of management's value creation above its book value of equity. Whereas it could also be argued this is pricey, considering the company's pre-revenue status.

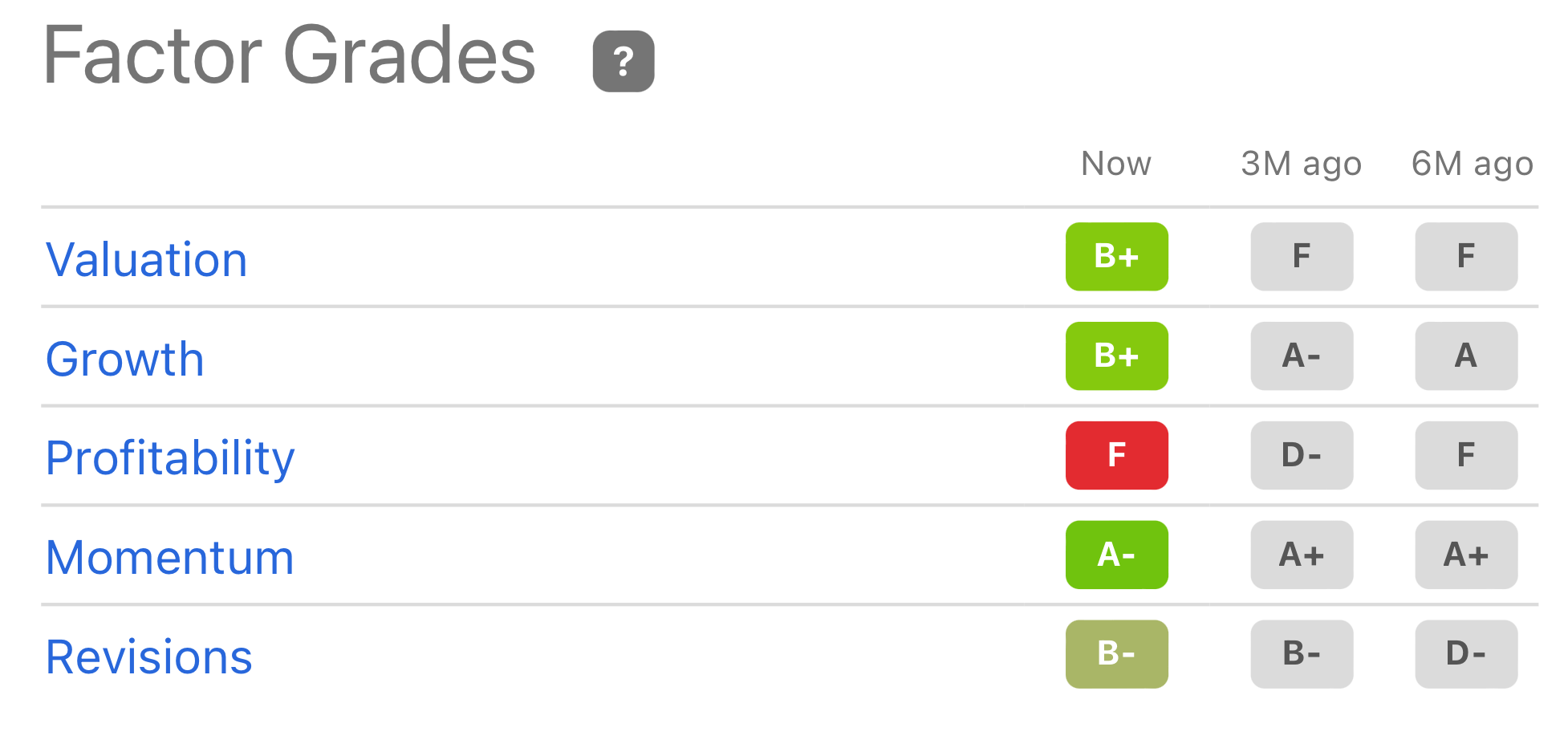

Checking Seeking Alpha's factor grading system to provide an objective answer, we can see the stock is rated highly in terms of valuation [Exhibit 5]. In fact, it is rated highly across all metrics, bar the obvious, being profitability. This adds a bullish weight to the COGT risk/reward calculus in our opinion, and advocates us rating it a sell.

Exhibit 4. COGT price to book value ratio versus the S&P 500 P/B ratio

{kind=link}

Exhibit 5. Quantitative factor grading rates COGT highly, adding a heavy bullish tilt to the investment debate, and balancing the downside

{kind=link}

Finally, turning to technically derived price targets, we see the stock has multiple downside objectives pointing to a range of $7.50–$8.60. In combination with the above, the blend of positive and negative valuation inputs helps us arrive at a neutral position on COGT. Further data around its PEAK, Apex and SUMMIT trials may be needed in order to warrant a strong buy rating in our opinion.

Exhibit 6. Downside targets to $8.60, $7.50, balancing the upside factors discussed

Data: Updata

In short

Cogent Biosciences, Inc. is building continued momentum around its bezuclastinib pipeline, and has made substantial ground in reaching the phase 3 portion of its PEAK study. In 2023, there are notable inflection points that investors should be taking close notice of. In our opinion, positive readouts from its PEAK and SUMMIT trials are worthy of COGT re-rating to the upside [due in H1 and H2 FY23, respectively]. However, at this point in time, we'd like more evidence of the trials' successes/failures in order to commit to a full position. Nonetheless, we are constructive on this name, and are waiting patiently on the sidelines for the above-mentioned data. Net-net, we rate Cogent Biosciences, Inc. a hold.

For further details see:

Cogent Biosciences: Multiple Inflection Points For FY23, Hold For Now