NSRGY - Colgate: Great For Capital Preservation But Will It Beat The S&P 500 Index?

Summary

- Colgate owns some of the best-known oral care, personal care, household cleaning, and pet nutrition brands, has wide global distribution, and is well positioned to capitalize on growing global demand.

- Its growth and margins over the past five years have been disappointing, in part due to raw material and packaging cost increases, and a strong US dollar.

- The company lacks the scale of its large consumer product peers and could be a good acquisition target, but its premium valuation is dilutive to potential acquirers.

- While Colgate’s ~35x price-earnings multiple is quite lofty given its relatively tepid growth, I believe the prospect of being taken out by its larger peers provides support to its valuation.

- Colgate is likely to generate decent but not spectacular returns and may be more suitable for the conservative investor whose main objective is capital preservation.

Colgate-Palmolive Inc ( CL ) is one of the world's leading manufacturers and markets of oral care, personal care, household cleaning, and pet nutrition products. It owns many of the best-known brands in these categories (Figure 1) and it is likely that most SA readers are users of at least a small handful of the company’s products.

Figure 1 A selection of Colgate brands

Company presentation

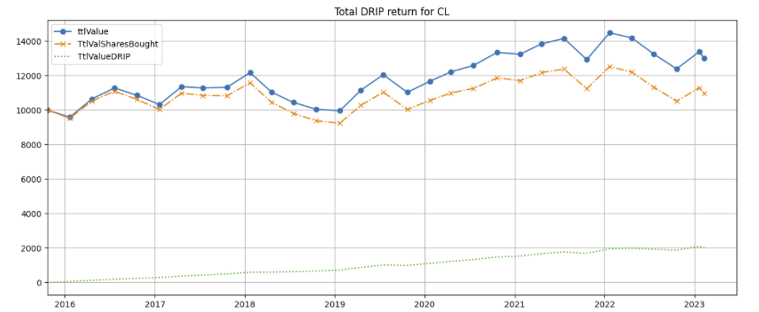

I have owned Colgate stock using a DRIP ( dividend re-investment plan ) for several years. I am disappointed by the overall results as the stock has vastly underperformed the S&P 500 index and many of its peers (Figure 2). Since 2016, the appreciation, including re-invested dividends but before taxes on the dividends received (Figure 3, dotted green line), has been a disappointing 0.3 times of invested capital (blue line).

Figure 2 Colgate stock returns

Seeking Alpha

Figure 3 DRIP returns

Created by author with public financial data

{kind=link}

In this article, I will lay out and re-examine my original investment thesis to determine whether I should continue to hold the stock in my growth-oriented portfolio.

My original investment thesis

My original investment thesis is as follows:

(1) Standards of dental hygiene and personal care in developing economies still lag the developed world; the rise of the global middle class and increasing affluence around the world will raise these standards and drive demand for dental hygiene and personal care products.

(2) As the owner of the best-known oral and personal care brands and market share leader in an oligopolistic industry, Colgate is well-positioned to capitalize on the growth of these powerful economic trends and enjoys some pricing power.

(3) Colgate’s deep penetration into households and wide global distribution is difficult to recreate and can be used to increase sales of its acquired brands.

(4) The company is well-run and consistently taking out costs, which should lead to widening margins.

(5) High returns on tangible capital

(6) The Hills Pet Nutrition segment gives investors exposure to the high-end pet food markets, which play well to the high growth theme of personification of pets.

The company’s investor relations deck available online provides additional detail.

A re-examination of each key point in my original investment thesis

(1) Standards of dental hygiene and personal care in developing economies still lag the developed world; the rise of the global middle class and increasing affluence around the world will raise these standards and drive demand for dental hygiene and personal care products.

After a sharp pullback in 2020 due to the COVID-19 pandemic, global per-capita GDP has resumed its long-term growth trend (figure 3).

Figure 4 Global per capita GDP (in current USD)

World Bank

Using Colgate’s revenue per capita as a rough proxy for market penetration (which is reasonable given the company’s leading market position in its markets, as will be discussed below), the penetration of dental hygiene and personal care products in the developed economies and Latin America are quite robust (Figure 5). However, the penetration in Africa/Eurasia and Asia Pacific are dismally low at below 10% that of North America and less than 14% that of Latin America (lines 1 and 2).

Figure 5 Colgate revenue per capita as a proxy for market penetration

Created by author with public financial data

According to Colgate, a super-majority of the world’s population brush their teeth less than once a day (Figure 6). I believe the frequency will inevitably grow as the rising affluence compels people to pay more attention to their dental appearance and personal cleanliness.

Figure 6 Toothpaste growth opportunity

Company presentation

(2) As the owner of the best-known oral and personal care brands and market share leader in an oligopolistic industry, Colgate is well-positioned to capitalize on the growth of these powerful global economic growth trends and enjoys some pricing power.

Owner of the best-known brands and market share leader

Oral care is a category that is highly personal to consumers and faces minimal threat from private label manufacturers (I’d be surprised if more than a tiny handful of readers of this article have used or will switch to a private label brand to save a few dollars on a tube of toothpaste).

According to Colgate, it is the global leader in many of the categories it competes in (Figure 7).

Figure 7 Colgate market leadership

Company presentation

Based on slightly dated 2019 information (which I no reason to believe has changed significantly), the company has over 40% of the worldwide toothpaste market (Figure 8) and over 30% of the worldwide manual toothbrush market (Figure 9) by value.

Figure 8 Worldwide toothpaste share by value (2019)

Worldview 360

Figure 9 Worldwide manual toothbrush share by value (2019)

Worldview 360

The company has been a relentless marketer and innovator, creating many brand extensions and differentiated product to attract the consumers’ attention. Examples include tooth whiteners both with and without hydrogen peroxide, sunscreen UV sticks, and a Brazilian heritage toothpaste brand relaunch. (for more examples, please click here to access the company’s investor presentation )

Oligopolistic market and growth compared to competitors

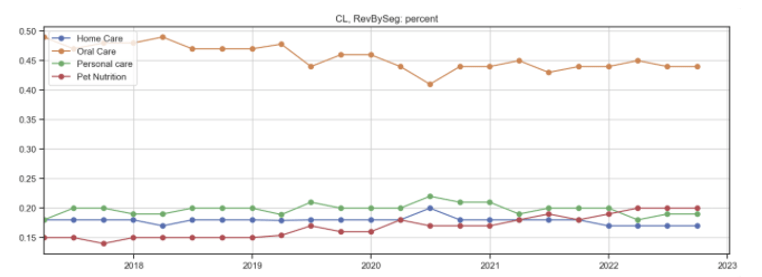

Colgate’s oral care segment is the largest at about 44% of the company’s total revenue (though it is down from almost 49% in 2018) (Figure 10, orange line), with each of the remaining three segments at below 20% of total revenue (red, green, and blue lines).

Figure 10 Colgate revenue by segment by percentage

Created by author with public financial data

{kind=link}

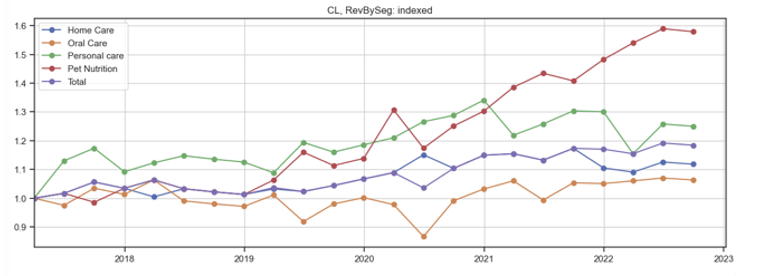

Over the last 5 years, the Oral Care and Home Care segments have grown by less than 15% in total (uncompounded) (Figure 11, blue and orange lines). Personal Care has growth in part through the acquisitions of [what] (green line), but Pet Nutrition has been the only solid grower (red line). As a result, total revenue has grown by less than 20% (purple line), which is disappointing.

Figure 11 Colgate segment growth since 2017

Created by author with public financial data

{kind=link}

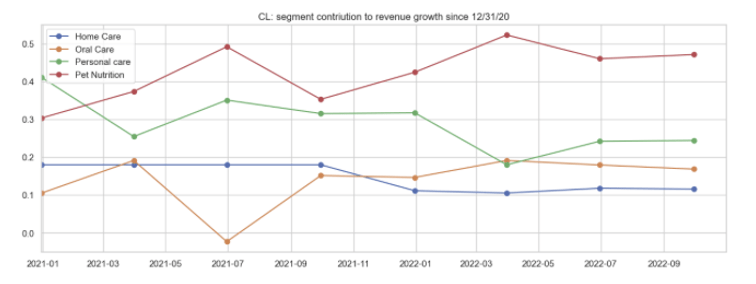

Over the last two years, Colgate’s Pet Nutrition has contributed nearly half of the company’s total revenue growth.

Figure 12 Colgate segment percentage contribution to total growth

Created by author with public financial data

{kind=link}

I examine each segment in greater detail:

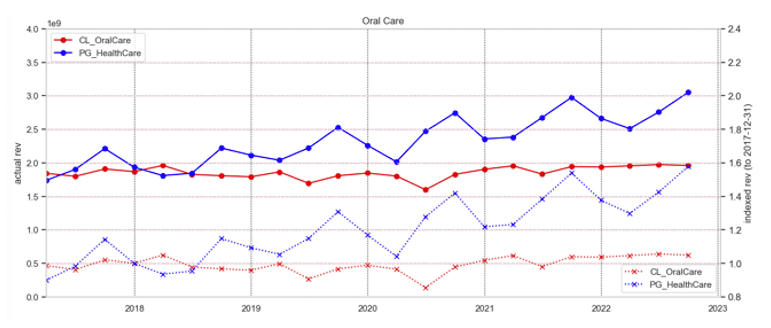

Oral care: Colgate’s Oral Care segment has hardly grown over the last 5 years (Figure 13, dotted red line, right axis), whereas Procter & Gamble’s ( PG ) healthcare segments, which includes its oral care products as well as gastro, respiratory, pain relief, supplements, and rapid diagnostics products such as Vicks, Pepto-Bismol, Metamucil) grew by 60% (dotted blue line, right axis).

Figure 13 Oral Care: Colgate vs PG

Created by author using company metrics

{kind=link}

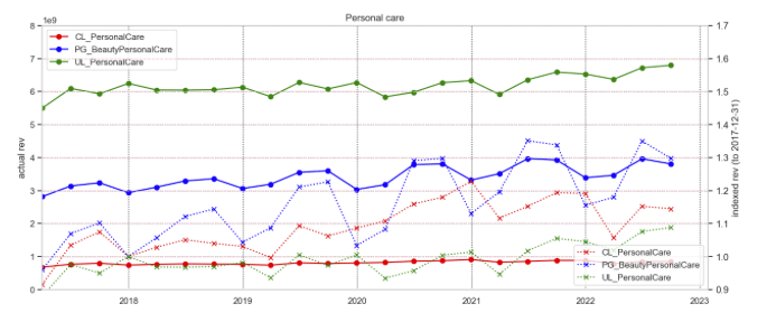

Personal Care: Colgate’s Personal Care is significantly smaller than that of its two main competitors. This segment grew about 15% over the last 5 years (Figure 13, dotted red line, right axis), whereas Procter & Gamble’s personal care segment, which includes its skin care, antiperspirant, deodorant, moisturizers, and personal cleansers) grew by 60% (blue line). Unilever’s ( UL ) personal care segment (consisting of Lux, Dove, Baseline) is far larger than (green line) but undergrew both Colgate and Procter & Gamble (dotted lines, right axis).

Figure 14 Personal Care: Colgate vs Procter and Unilever

Created by author using company metrics

{kind=link}

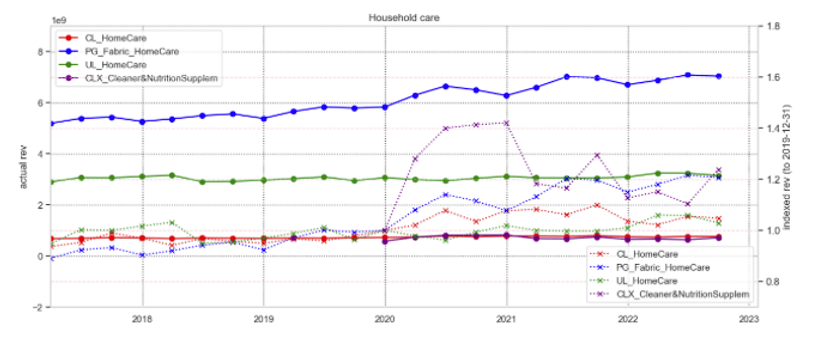

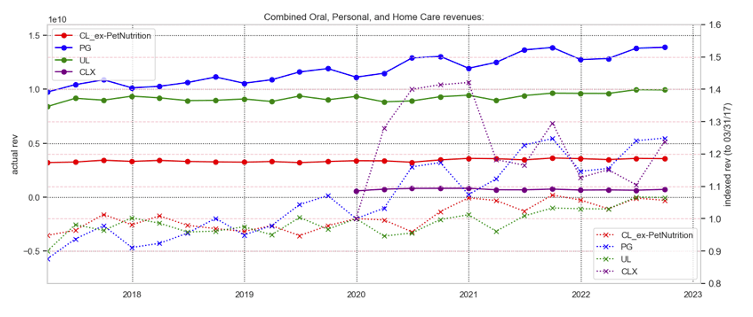

Home Care: Colgate’s Home Care segment is approximately the same size as Clorox’s ( CLX ) Cleaner and Nutrition Supplement segment which includes brand such as (Figure 15Figure 13, red and purple lines). Both are significantly smaller than the home care segments of Procter & Gamble and Unilever (red and purple vs blue and green solid lines). (Please note that P&G’s home care segment includes its laundry detergent and fabric care products, while Clorox’s Cleaner segment also includes professional cleaning products as well as professional food service and consumer vitamin supplement products).

Sales of all four companies surged during the COVID-19 outbreak due to the heightened demand for cleaners which were used to limit the spread of infection. However, while home care segments sales for Colgate and Unilever have peaked (dotted red and green lines), Procter & Gamble and Clorox have continued to grow (dotted blue and purple lines).

Figure 15 Homecare segment: Colgate vs Procter & Gamble, Unilever, and Clorox

Created by author using company metrics

{kind=link}

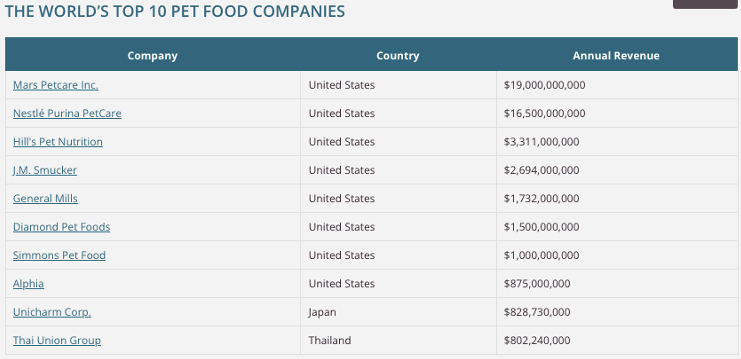

Pet Nutrition: Colgate’s Pet Nutrition segment is a distant third to Mars Petcare (privately held) and Nestle’s Purina Petcare ( NSRGF ) at just ~15% and ~20% the size of Mars and Nestle’s pet segments respectively.

It is about 10% larger than of Smucker’s ( SJM ) retail pet food segment (Figure 16) and growing at a faster rate (Figure 17, dotted red vs blue lines, right axis).

Figure 16 The top pet food companies

{kind=link}

source: Top Pet Food Companies Current Data

Figure 17 Pet food: Colgate vs Smuckers

Created by author using company metrics

Even though Colgate is a leader in oral care, its combined revenues in the oral, personal, and home care segments is significantly smaller than that of Procter & Gamble and Unilever, generating just 25% and 36% of Procter & Gamble and Unilever’s revenues respectively.

Figure 18 Combined revenues of oral, personal, and home care

Created by author using company metrics

{kind=link}

Pricing power

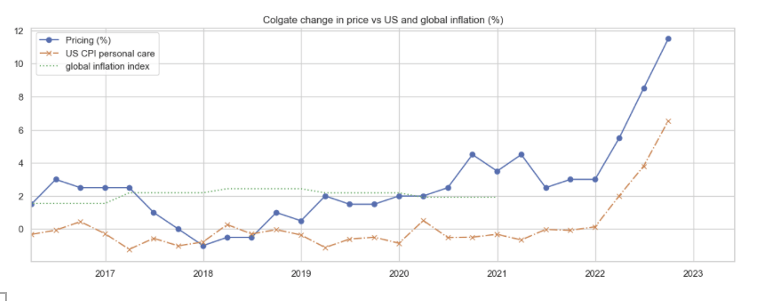

I examined Colgate’s pricing against both the US consumer price index for personal care products and global inflation index (both provided by the St. Louis Federal Reserve’s FRED) and found that Colgate was able to raise prices in excess of inflation a majority of the time (Figure 19).

Figure 19 Relationship between Colgate price increase and inflation indices

Created by author using company metrics and FRED data

{kind=link}

Source: St. Louis Federal Reserve FRED -- CUUR0000SEGB and FPCPITOTLZGWLD

An examination of the data of historical price changes and the relationship between pricing changes and volume shows that: [A] Colgate lowers prices infrequently, and [B] there is a negative relationship between pricing and volume (Figure20).

Figure 20 Relationship between changes in pricing and volume

Created by author using company metrics

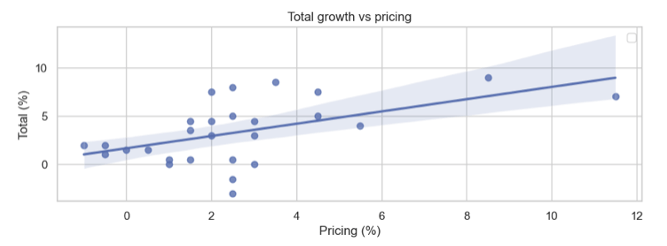

A regression analysis also shows the company’s price increases have generally resulted in increased revenue (Figure 21).

Figure 21 Relationship between changes in pricing and revenue

Created by author using company metrics

{kind=link}

(3) Colgate’s deep penetration into households and wide global distribution is difficult to recreate and can be used to increase sales of its acquired brands.

Colgate noted in its investor presentation that it has greater household penetration than any other brand (Figure 22), and theoretically, is able to leverage its widespread channels to expand distribution of the acquired brands and products. Colgate has entered the premium skin care with the acquisitions of Filorga (estimated sales of $200 million) for $1.69 billion in 2019 and professional skin care businesses EltaMD and PCA Skin (estimated sales of $100 million) for ca. $730 million in 2017. However, they have yet to grow to a scale that requires the creation of a separate reporting segment.

Figure 22 Colgate's household penetration

Company presentation

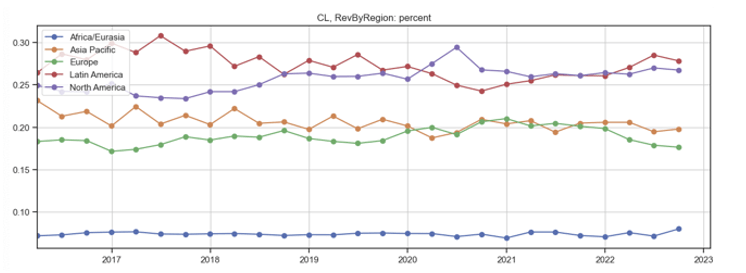

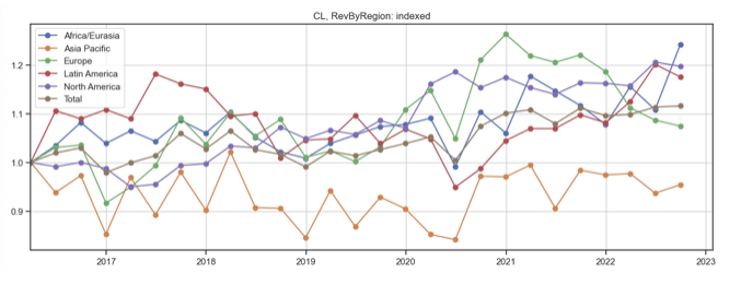

Globally, Colgate has a broadly diversified geographical distribution and derives the most of its revenues from Latin America and North America (Figure 23, purple and red lines), both of which are growing faster than Europe and Asia Pacific (Figure 24, purple and red vs green and orange lines). Africa/Eurasia has also grown rapidly but accounts for approximately 5% of revenues is unlikely to move the needle for the near future. However, none of the regions apart from Africa/Eurasia has grown more than 20% (uncompounded) over the last five years.

Figure 23 Colgate percentage revenues from each region

Created by author using company metrics

{kind=link}

Figure 24 Revenue growth by region, indexed to 1Q 2016

Created by author using company metrics

{kind=link}

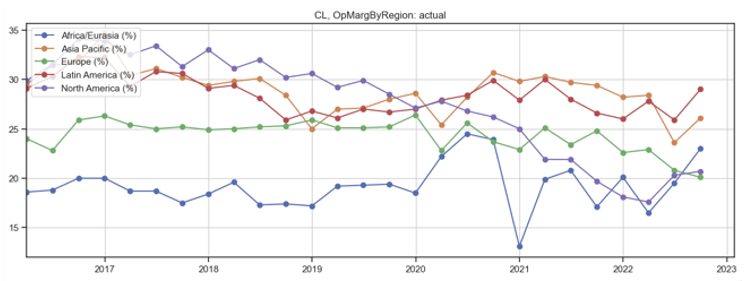

Margins in North America, Colgate’s second largest region, have declined by over 1000 basis points over time (purple line) due to increased advertising, higher overhead expenses, and charges related to the company’s Growth and Efficiency program; this was accompanied by raw material and packaging material cost increases, followed by plant closures, and supply chain issues after the COVID-19 outbreak which caused the company to incur additional air freight and transportation charges to fulfil customer orders. The aforementioned Growth and Efficiency program--initiated in 2012 and expanded in 2014-15 – that was expected to “ensure sustained solid worldwide growth in unit volume, organic sales, operating profit and earnings per share”, does not appear to have delivered on its objectives as of 2022.

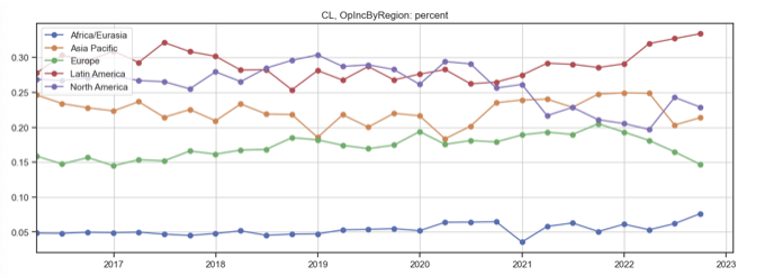

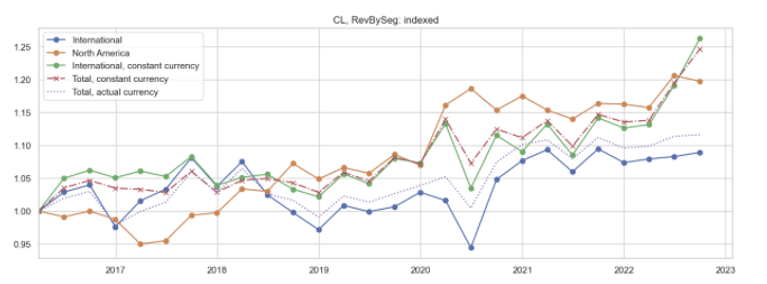

Operating Margins are highest and have held up in Latin America and Asia Pacific (Figure 25, red and orange lines) despite the strengthening US Dollar (see Figure 32 below). As a result, Latin America generates about one-third of overall operating income (Figure 26, redline), and Asia Pacific generates almost as much operating income as North America (orange and purple lines) on just 70% of the sales.

However, North American margins appear to have bottomed out in early 2022, and non-US dollar denominated operating income should expand if/when the US Dollar exchange rate regresses to its longer-term mean. As such, there is potentially room for a reversal.

Figure 25 Operating margins by region

Created by author using company metrics

{kind=link}

Figure 26 Operating income by region

Created by author using company metrics

{kind=link}

Comparison of revenue by region vs major competitors

Colgate’s North American and international revenue is just about 12% and 26% that of Procter & Gamble’s US and international revenue respectively, and about 36% and 16% that of Unilever’s Americas and international revenue respectively (Figure 27).

In an industry where manufacturing, marketing, and research & development economies of scale matters, Colgate’s revenue is far smaller than both Procter & Gamble and Unilever.

Figure 27 Revenues by region vs competitors

Created by author using public data

(4) The company is well-run and consistently taking out costs, which should lead to widening margins.

In its investor presentations, Colgate discusses cost savings from the ongoing initiatives it has implemented over the years (Figure 28).

Figure 28 Cost savings initiatives

Company presentation

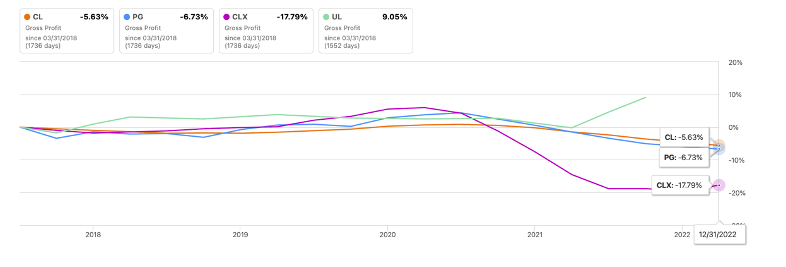

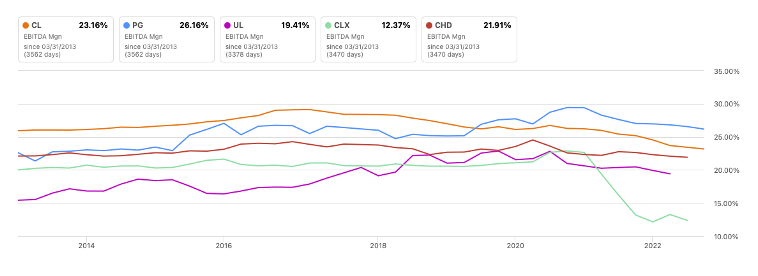

However, its gross and EBITDA margins have declined and are at the lowest level in the last five years (Figure 29 and Figure 30), which may be due to the following causes: [A] cost savings have been passed onto its customers, or [B] the strong USD has caused non-US dollar denominated gross margins to be compressed in dollar terms (this will be discussed in key financials below).

Figure 29 Gross margin

{kind=link}

Figure 30 EBITDA margins

{kind=link}

(5) High returns on tangible capital

Colgate's EBITDA return on tangible capital (i.e., EBITDA/(current assets + net PPE - current liabilities) has averaged over 100% over the last five years. However, as noted above, its organic growth has been relatively tepid.

(6) The Hills Pet Nutrition segment gives investors exposure to the high-end pet food markets, which play well to the high growth theme of personification of pets.

Based on the analyses in Figure 16 and Figure 17 above, this thesis point appears to be holding true.

Key financials

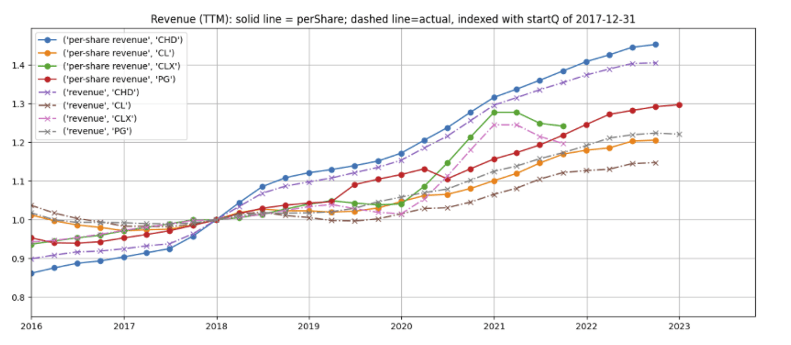

Colgate’s revenue and per-share revenue growth has lagged its peers Procter & Gamble, Clorox, and Church & Dwight ( CHD ).

Figure 31 Colgate revenue and per-share revenue vs peers

Created by author using company metrics

{kind=link}

Foreign currency adjustment

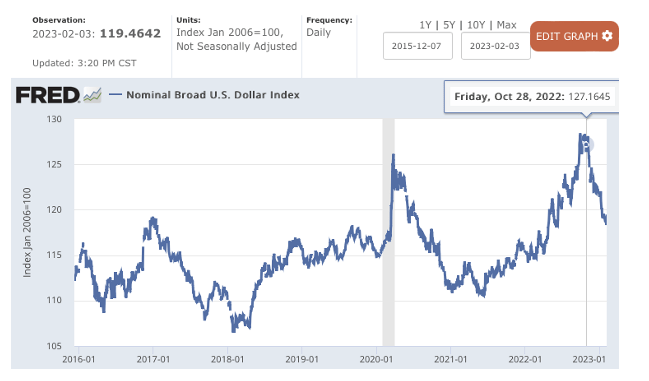

I note that Colgate’s and its peers’ revenues have been negatively impacted by the strong US Dollar as measured by the nominal broad US Dollar index (Figure 32).

Figure 32 Nominal broad US Dollar index (using FRED DTWEXBGS)

{kind=link}

After adjusting the Colgate’s international revenues using the nominal broad US Dollar index, revenues grew by about 25% over the last 6 years (Figure 33, red-dashed line), suggesting that the strong US dollar has played a part in holding back the company’s US-denominated growth numbers. I would be first to acknowledge that this is far from a precise adjustment, but it is directionally correct and the best I can do given the limited performance metrics and data provided by the company.

Figure 33 Colgate's "constant currency"-adjusted revenues

Created by author using company metrics

{kind=link}

Valuation

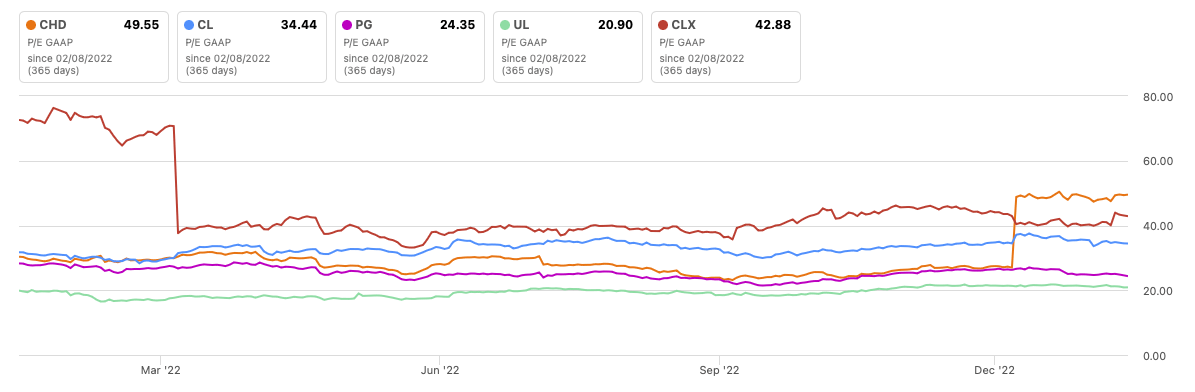

Colgate’s stock trades at a price-earnings multiple of around 34.9x, which is not cheap for slow grower, and a premium to Procter & Gamble and Unilever (Figure 34). However, Colgate’s smaller size and market capitalization makes it a potential acquisition target to the consumer product giants, the prospect of which provides support to its premium valuation.

Figure 34 Colgate valuation vs peers

Created by author using public financials and stock data

{kind=link}

Concerns

Oral care, personal care, household cleaning products, and pet food are viewed as daily necessities with relatively low price points and consumers will continue to purchase them in both good and tough economic times as well as through pandemics. As such, the business risk of Colgate is quite low.

My two key concerns are:

(1) A combination of the slow growth and high valuation could cause the stock to deliver sub-par returns for an extended period of time.

(2) Colgate’s substantially lower combined revenues in oral, personal, and home care products compared to industry giants Procter & Gamble and Unilever could keep it at a disadvantage in being able to exploit economies of scale.

There were rumors of talks in 2007 of Unilever acquiring Colgate , but then-CEO Ian Cook asserted to analysts that “there are absolutely no conversations with Unilever”. I believe the likelihood of an acquisition is low as long as Colgate’s valuation remains higher than its peers’ (Figure 34) as the transaction would be dilutive to a potential acquirer. However, the prospect of an acquirer swooping in if Colgate’s stock price falls likely provides some support for Colgate’s valuation.

Conversely, Colgate could potentially be an acquirer for small competitors such as Clorox or Church & Dwight but the valuations of both are substantially higher than Colgate's and will be dilutive.

Summary

Colgate is a leading producer of the best-known oral care, personal care, household cleaning, and pet nutrition brands, has wide global distribution, and is well positioned to capitalize on growing demand due to the rising global middle class.

Its growth and margins over the past five years have been disappointing even though pricing has kept up with inflation in part due to raw material and packaging cost increases, supply chain issues, and a strong US dollar.

The company lacks the scale of its large consumer product peers such as Procter & Gamble or Unilever and could be a good acquisition target, but its premium valuation is dilutive for potential acquirers.

While Colgate’s ~35x price-earnings multiple is quite lofty given its relatively tepid growth, I believe the prospect of being taken out by its larger peers provides support to its valuation.

Colgate is likely to generate decent but not spectacular returns and may be more suitable for the conservative investor whose main objective is capital preservation.

For further details see:

Colgate: Great For Capital Preservation But Will It Beat The S&P 500 Index?