WAL - Commerce Bancshares: Deterioration Continues

2024-01-12 02:54:59 ET

Summary

- Commerce Bancshares' stock has outperformed the market but has shown weak performance compared to other players in the banking sector.

- CBSH has experienced a decline in deposits and an increase in uninsured deposit exposure, indicating weakness in its metrics.

- Debt levels remain elevated, but cash on hand has grown. The bank has also reduced its securities holdings and has a significant portion of its loan portfolio in mortgage-backed securities.

- Shares are pricey as well, meaning that there are better prospects to be had on the market today.

Back in July of 2023, when the banking crisis was still relatively fresh on everybody's minds, I found myself wondering what kind of prospects, if any, Commerce Bancshares ( CBSH ) might offer investors. At that time, there was a tremendous amount of uncertainty in the banking sector. And in that article , I concluded that, even though the firm was trading near the low point that it fell to in response to the collapse of some institutions in the banking sector, it was not an ideal prospect for investors. This was in spite of the fact that the company's financial track record leading up to that point was quite solid. But weakness on the deposit side, high amounts of uninsured deposit exposure, and a rather lofty share price compared to other players in the space led me to rate it a 'hold'. Now since then, shares have outperformed the broader market, rising by 6.7% compared to the 3% seen by the S&P 500. However, given how much upside many other players in the market have seen over the same window of time, this is a rather weak showing. And frankly, given what we have seen on the fundamental side, I am surprised the stock is up as much as it is.

This picture isn't looking pretty

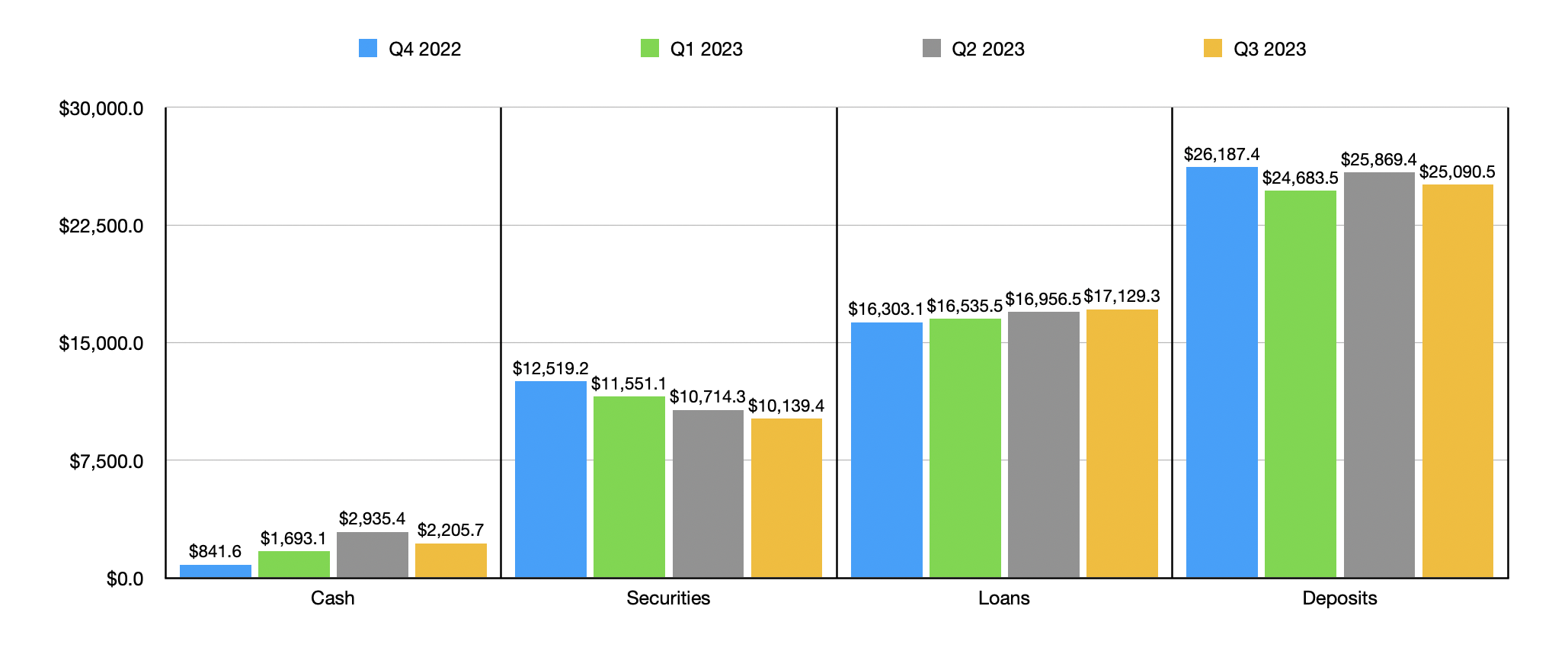

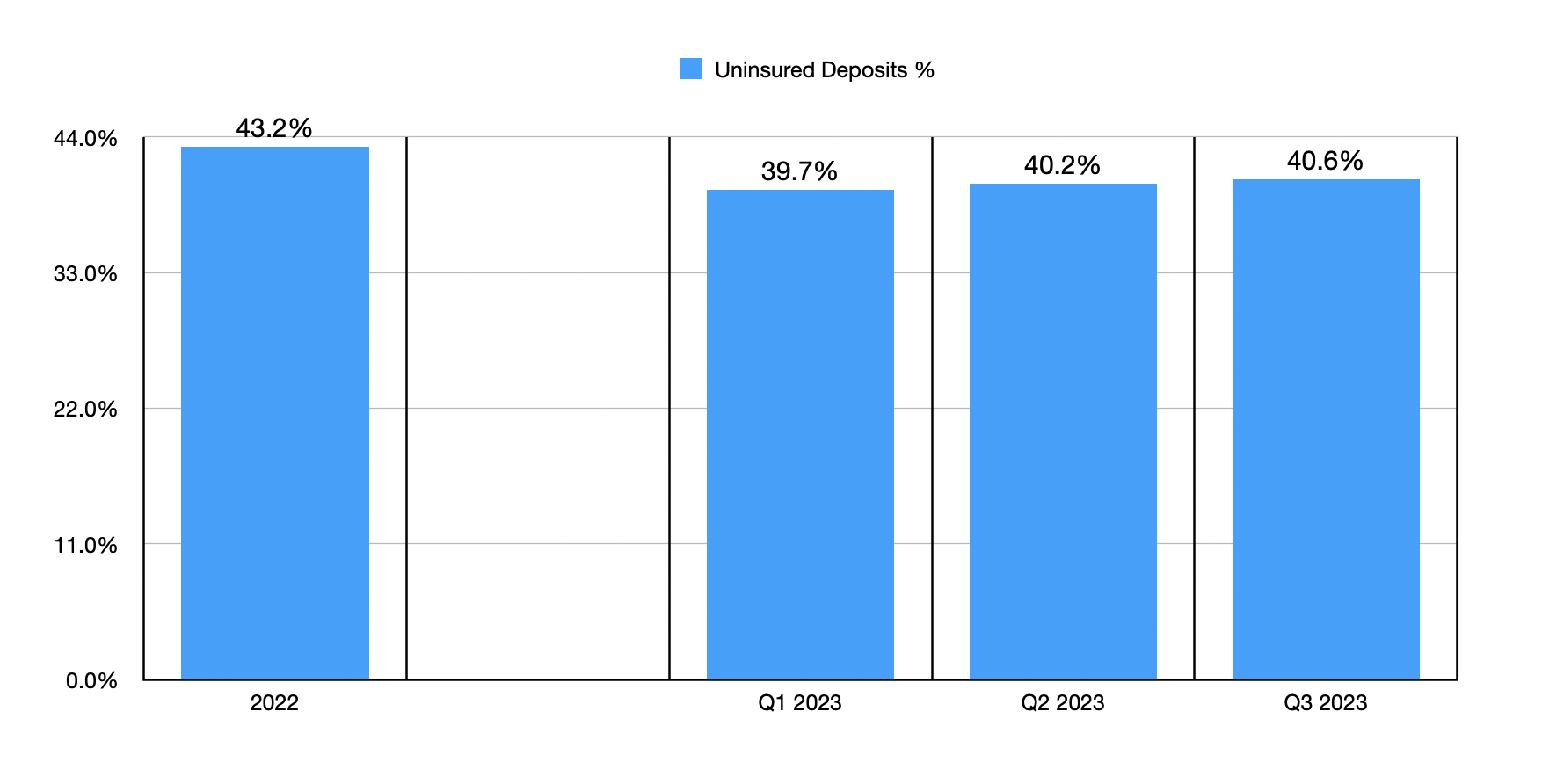

When the banking crisis began, a lot of focus from investors in this space centered around deposits and uninsured deposit exposure. After all, it was a massive decline in deposits in response to high uninsured deposit exposure that caused the crisis to begin with. At the end of 2022 , Commerce Bancshares boasted $26.19 billion worth of deposits. But by the end of the first quarter, deposits had fallen $1.50 billion to $24.68 billion. That's a rather sizable drop. And a lot of that decline was driven by a drop in uninsured deposit exposure from 43.2% of all deposits to 39.7%.

{kind=link}

Those who follow the institution closely were probably relieved when, in the second quarter of 2023, deposits jumped to $25.87 billion. That increase of $1.19 billion was driven largely by a rise in uninsured deposits amounting to $600 million. That brought uninsured deposit exposure up to 40.2%, but that was still lower than the 43.2% seen at the end of 2022. Unfortunately, hopes that the bleeding was over were dashed when, in the third quarter, deposits fell back to $25.09 billion. At the same time, uninsured deposit exposure ticked up further to 40.6%. So what we have here is a bank that, after a brief reprieve, has now started to show some additional signs of weakness when it comes to the most important of its metrics.

{kind=link}

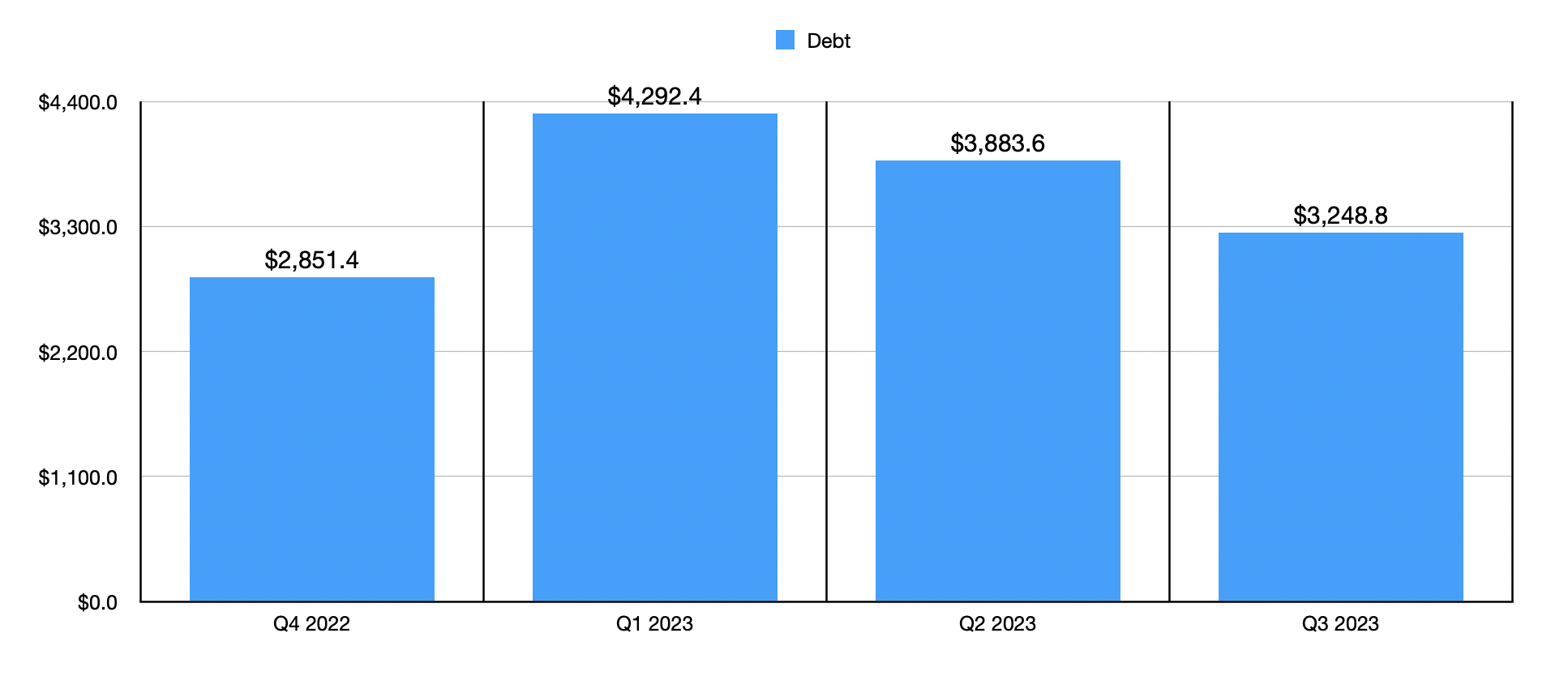

This is not the only thing that investors should be concerned about. As an example, debt still remains a bit elevated compared to what it was at the end of 2022. After spiking from $2.85 billion to $4.29 billion in the first quarter of 2023, debt continued to fall. But as of the end of the most recent quarter, it still stood at $3.25 billion. The good news is that this has come even at a time when cash on hand continues to grow. Cash and cash equivalents at the end of 2022 totaled $841.6 million. Today, that number is $2.21 billion, which is lower than the $2.94 billion seen in the second quarter. But even so, it represents a surge compared to 2022.

{kind=link}

Unfortunately, the rise in cash and partial improvement in debt has come at the expense of a reduction in securities that the bank has. At the end of 2022, the firm had $12.52 billion of securities. This metric fell to $11.55 billion in the first quarter of 2023 before dropping even more to $10.14 billion by the end of the third quarter. Furthermore, for those who don't like access to mortgage-backed securities, the fact that 53% of the value of the company's loan portfolio is comprised of those assets might be concerning. Another 23% involves other asset-backed securities of an unspecified nature.

The one piece of good news is that, even as some of these other metrics have worsened, the value of loans owned by the company only increased. At the end of 2022, loans totaled $16.30 billion on the company's balance sheet. In every quarter since then, this number has risen. And as of the most recent quarter, it totaled $17.13 billion. I do know that many investors are worried about exposure to office assets. And that is because of the high vacancy rates that they have. But the good news is that only about 14% of the company's commercial loans, by value, fall under this category. This translates to roughly 2.9% of overall loans that are classified as office assets. That's toward the lower end of the scale from what I have seen as far as banks go.

{kind=link}

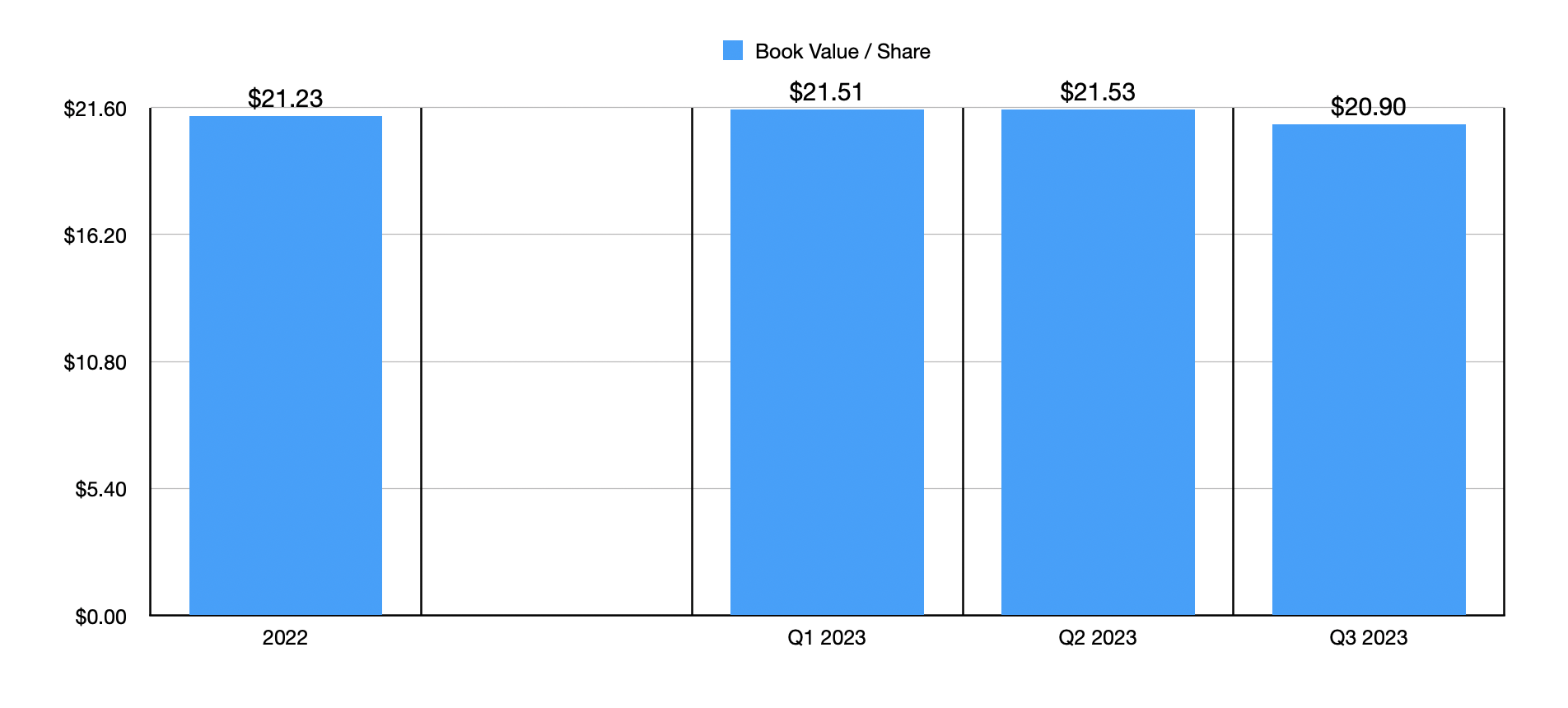

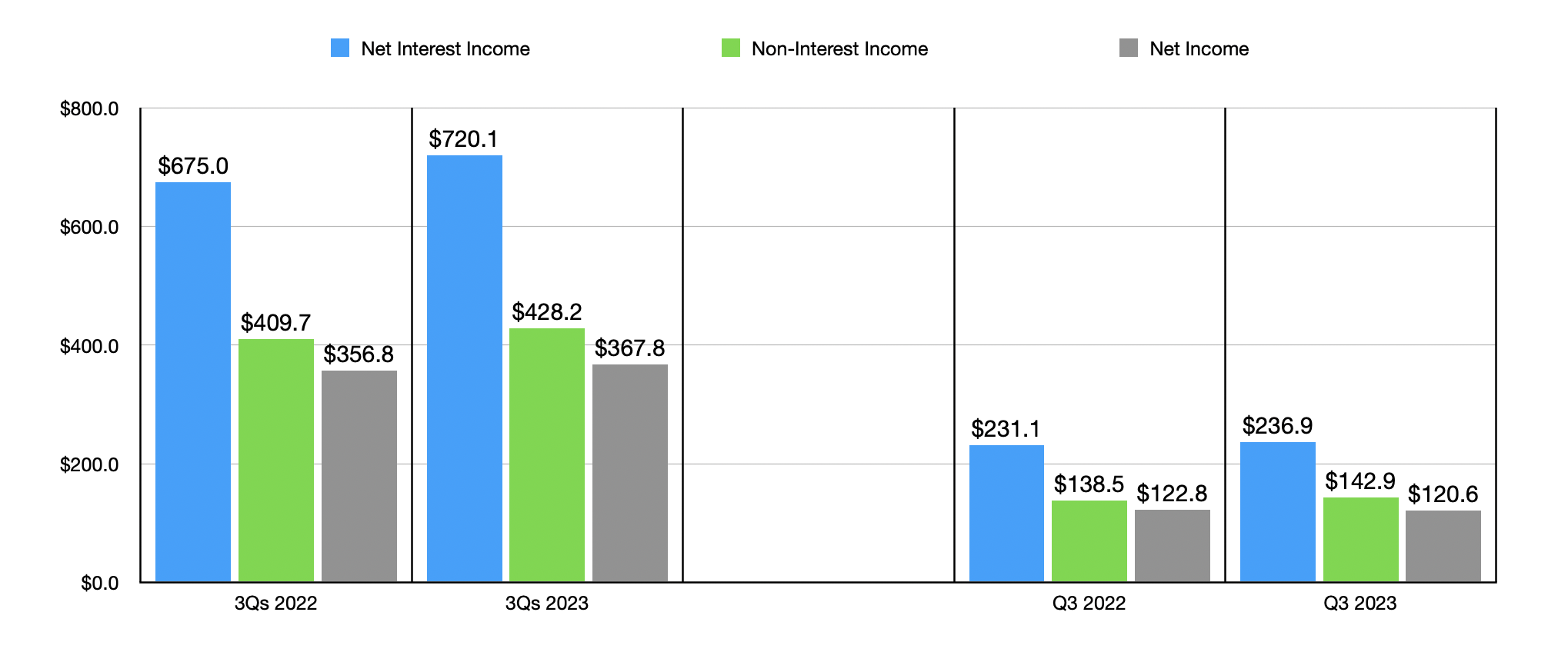

There have been some other issues as well. As you can see in the chart above, the book value per share for the institution recently dropped from $21.53 in the second quarter to $20.90 in the third quarter. That loan is not a huge deal. But when factoring in the other weaknesses across the board, it is something for investors to pay attention to moving forward. And lastly, as you can see in the chart below, overall revenue and profits for the institution are actually up so far this year. But in the third quarter on its own, net profits did decline slightly. Unfortunately, that was driven mostly by higher salaries and rising occupancy costs. As time goes on, these can be absorbed. But that doesn't change the fact that they are having a modest impact on profitability now.

{kind=link}

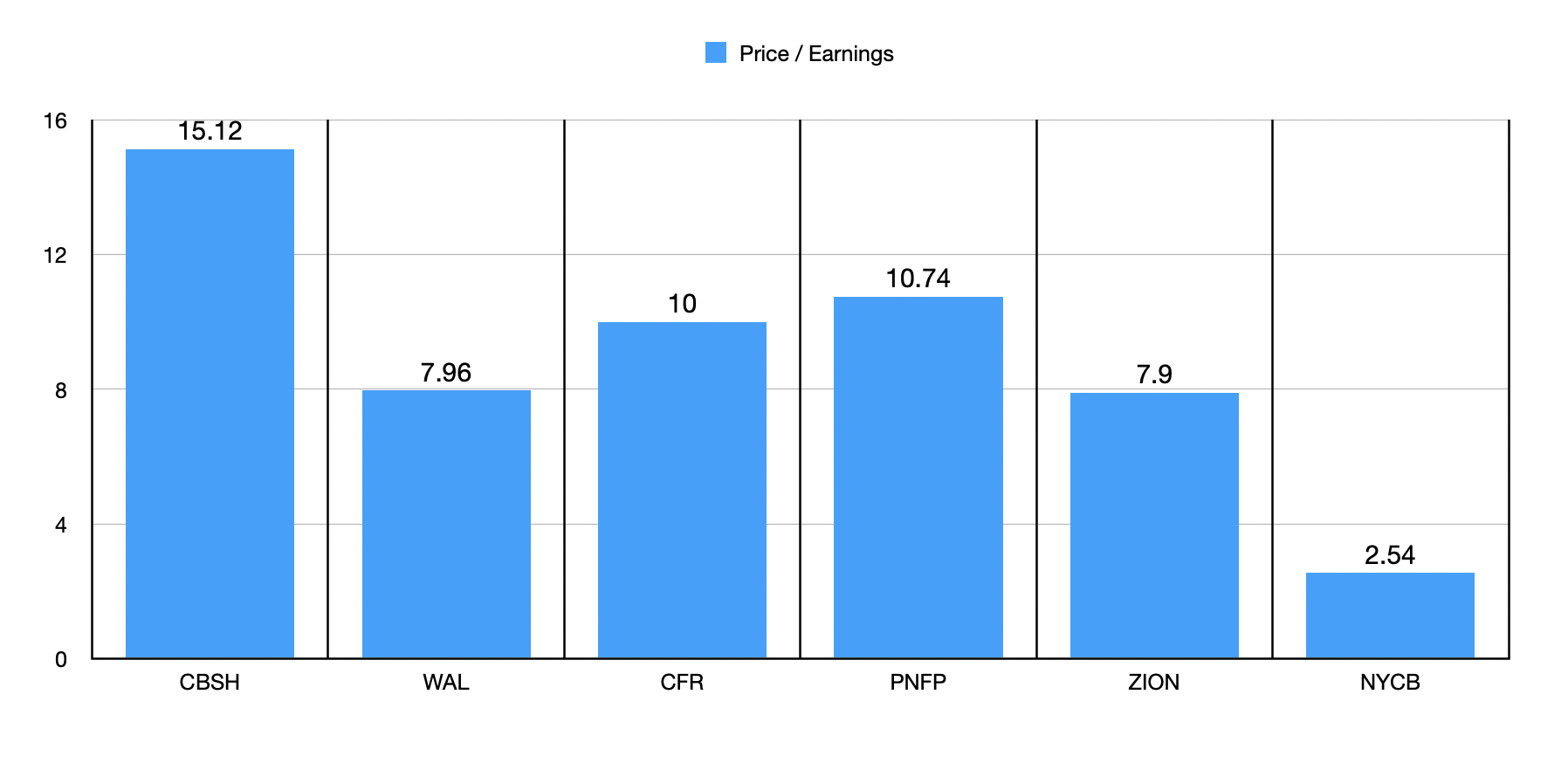

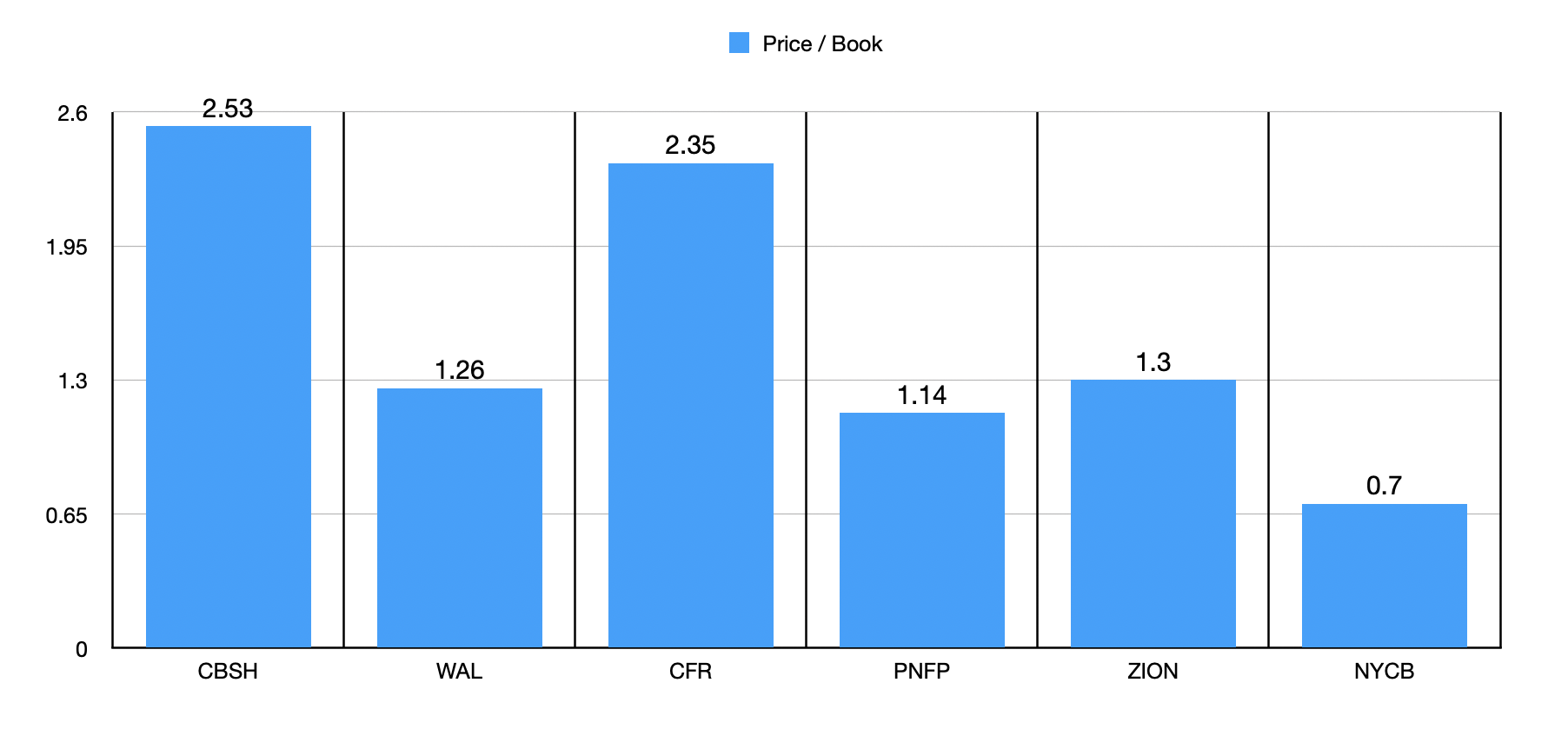

In addition to seeing these weak spots, there's also the fact that shares look rather pricey at this time. Based on my own estimates, earnings for 2023 will end up being $468.1 million. This is based on analysts' estimates for the final quarter of the 2023 fiscal year, with those earnings applied to earnings seen so far for said year. This would imply a price-to-earnings multiple of 15.1 on a forward basis, which is down from the 14.5 reading that we get using data from 2022. Meanwhile, the company is trading at 2.52 times its book value of equity. That makes it one of the more expensive financial institutions that I have covered over the past year or so.

{kind=link}

{kind=link}

To see what I mean when I say that Commerce Bancshares is one of the more expensive players in the financial space that I have looked at recently, I would like to compare the company to five similar firms as shown in the charts above. In those charts, you can see how shares are priced relative to these five other regional banks of similar size using both the price to book approach and the price to earnings approach. In both instances, Commerce Bancshares ended up being the most expensive of the group.

{kind=link}

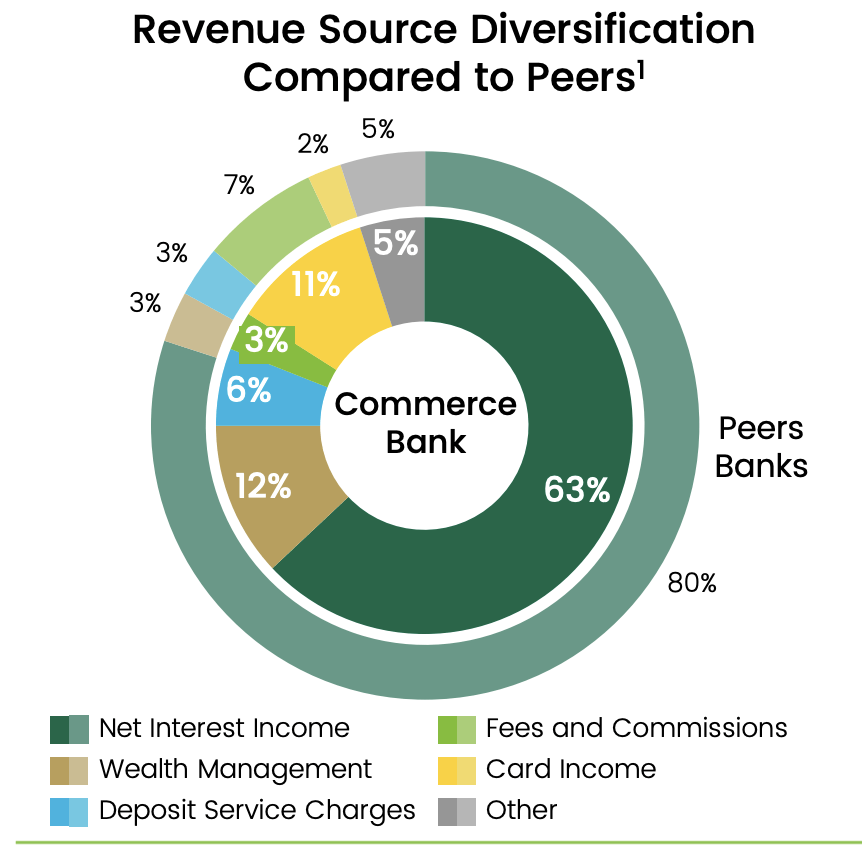

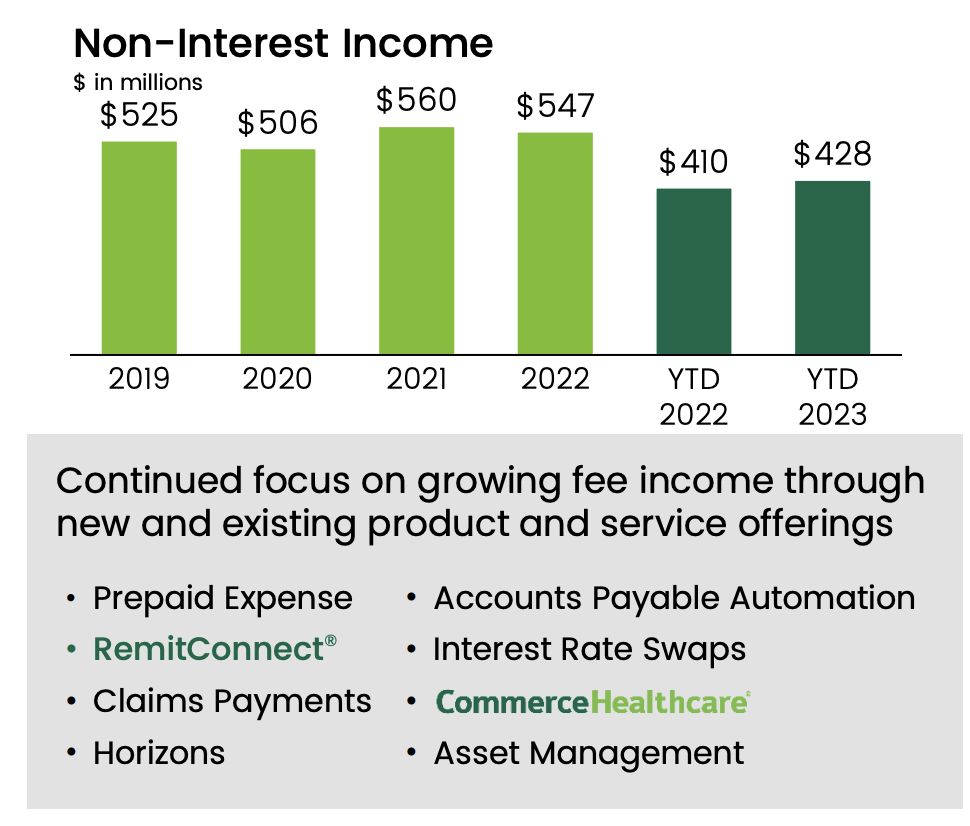

Those who are fans of the enterprise might point out that Commerce Bancshares is a different kind of animal that deserves to be traded at a premium. They would be correct in stating that it is different from many other regional banks of a similar size. As an example, the firm has done well in recent years to diversify its revenue stream away from net interest income. According to management's own estimates , an average of 80% of all revenue generated by similar enterprises comes from net interest income in any given year. But for Commerce Bancshares, that number is 63%. A full 36% of all revenue comes from fees, with the largest chunk, 12%, attributable to wealth management services, while another 11% can be chalked up to card income.

This kind of diversification is important and often deserves some premium because it means that the company is less reliant on the credit cycle. That should provide it some stability during difficult times. Management has achieved this kind of diversification by focusing on alternative revenue streams like the ones that I already mentioned. On the payments side of the equation, for instance, using data from 2022, the company processed $7.7 billion worth of merchant volume, with total commercial card volume totaling $10.4 billion. That brought in a combined $200 million in payment revenue for the enterprise. Management has other initiatives as well, such as its CommerceHealthcare program, through which it has partnered with over 3,000 healthcare providers and over 500 hospitals spread across all 48 contiguous states. This program sees the company provide a variety of services to its partners such as receivables management solutions, accounts payable solutions, traditional banking services, and more.

{kind=link}

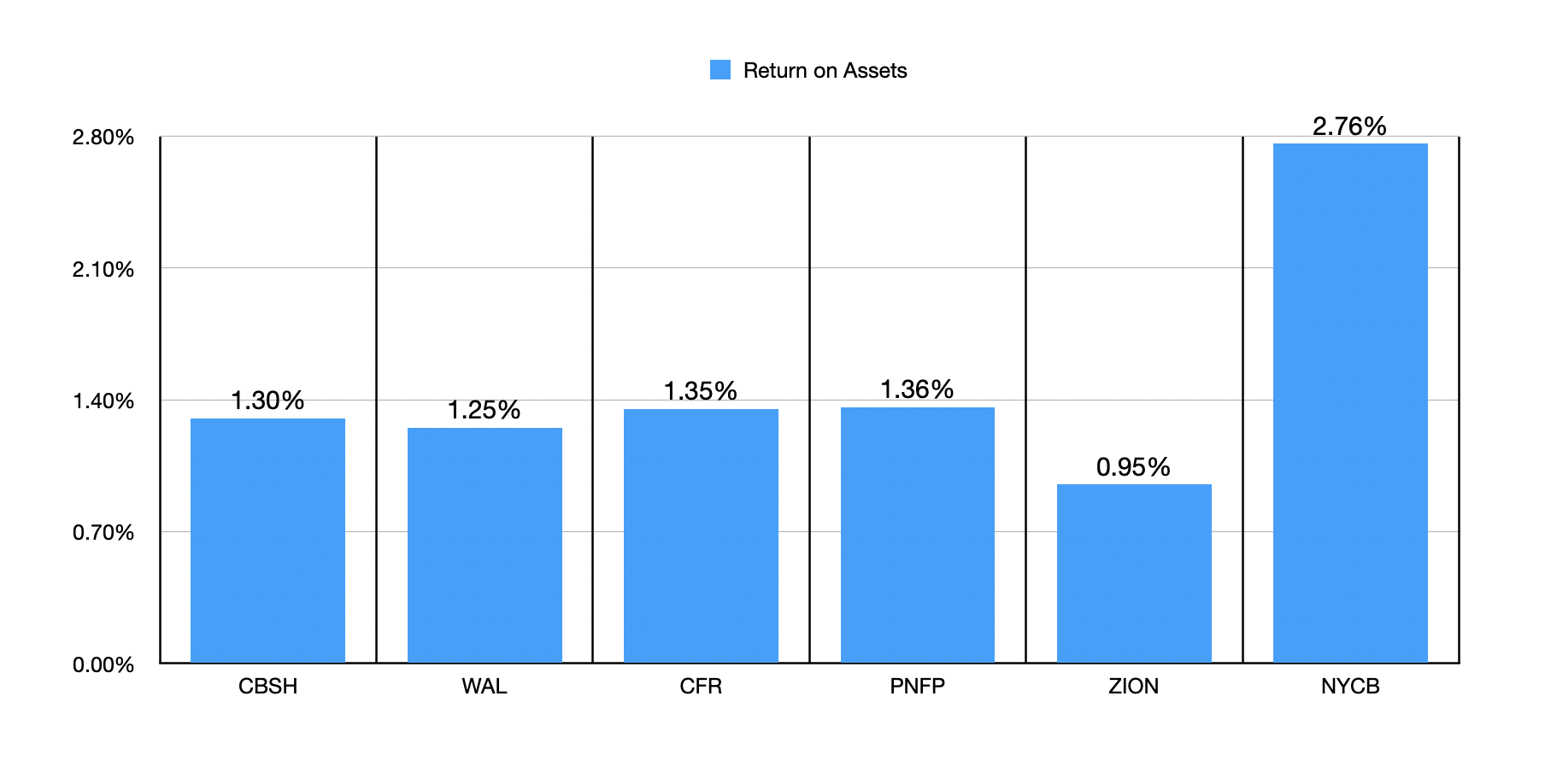

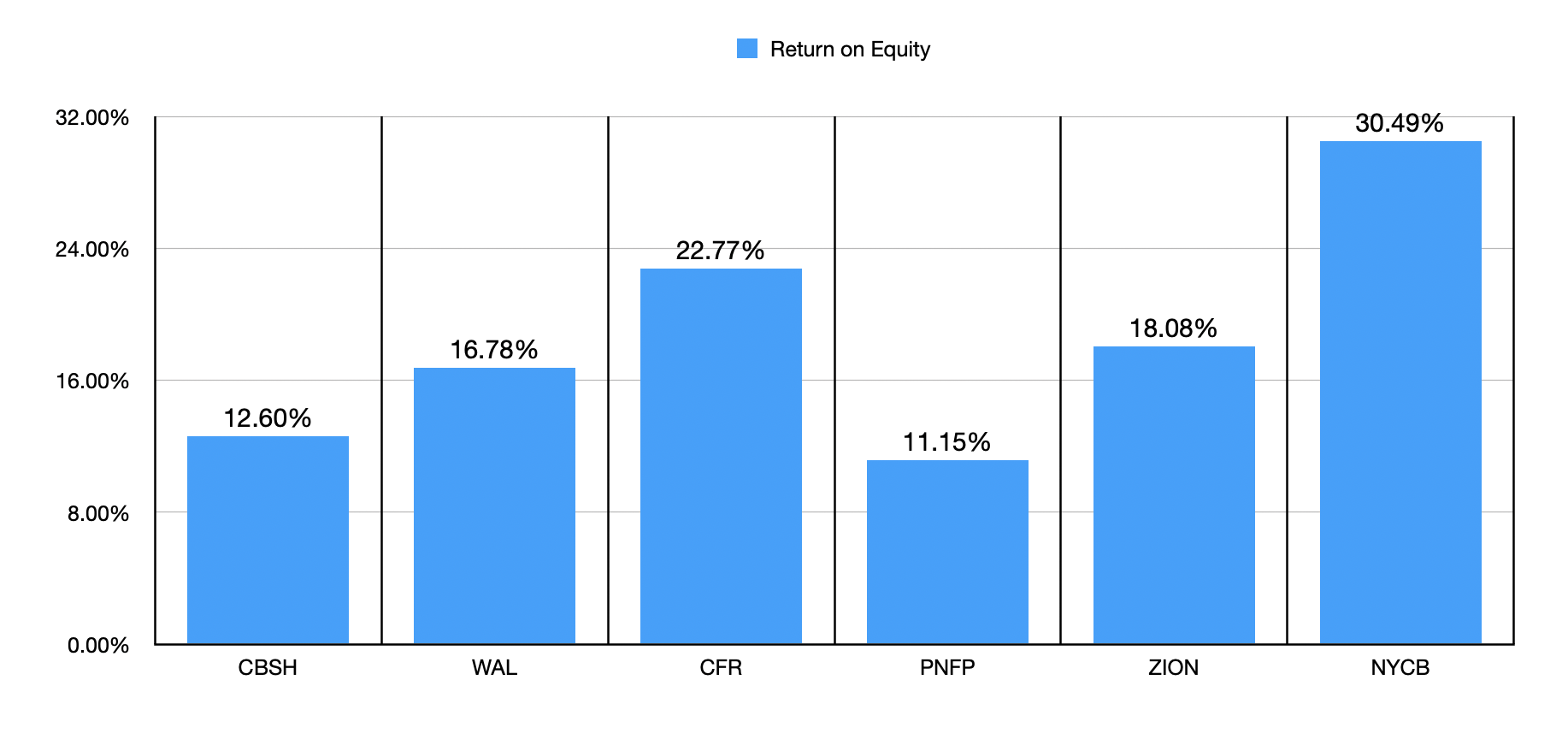

But there are two problems with these non-core functions. First and foremost, for the four years from 2019 through 2022, the company has seen its non-interest income remain in a fairly narrow range. So although the firm might have established for itself a nice alternative source of revenue, it has proven itself unable to grow further in this regard. This might be acceptable if its financial returns were more robust than similar enterprises. But that's not the case either. In the first chart below, you can see the return on assets generated by not only Commerce Bancshares but also the five companies I decided to compare it to. And in the chart below that, you can see the same thing but for the return on equity for each enterprise. When it comes to the return on assets, only two of the five companies that I compared it to have readings that are lower than what Commerce Bancshares boasts. And when it comes to the return on equity, this number drops to one. Alternative sources of revenue are only valuable if they create some competitive advantage. And that does not appear to be the case here.

{kind=link}

{kind=link}

This doesn't mean that the picture can't change. On January 18th, management is expected to announce financial results covering the final quarter of the 2023 fiscal year. However, I don't have particularly high hopes that anything monumental will happen in that regard. Analysts, for instance, are forecasting revenue of $384.8 million. That would actually represent a decline from the $391.5 million reported one year earlier. Despite the very high likelihood that non-interest income will continue its year over year growth, it's expected that a decline in the value of securities on a year over year basis for the company will push net interest income down. Analysts also believe that earnings per share would be disappointing. They are forecasting profits of $0.81 per share, which would translate to $100.3 million in income. That would be down from the $1.04 per share, or $131.6 million, that the company reported in the final quarter of 2022.

Takeaway

Fundamentally speaking, Commerce Bancshares isn't bad. But it is far from a great prospect. The renewed drop in deposits, combined with other aforementioned factors, makes me believe that investors would be better off looking for opportunities elsewhere. Whether that is in the banking sector or not is up to them. I do believe that there are still some attractive players in the financial space. But opportunities outside of the financial space are many as well.

For further details see:

Commerce Bancshares: Deterioration Continues