X - Commercial Metals Company Is Small But Mighty

Summary

- 2023 Will Present New Challenges for Commercial Metals Company.

- Commercial Metals' balance sheet improvement provides future flexibility and strength against macro headwinds.

- Commercial Metals Company valuations remain reasonable.

Commercial Metals Company ( CMC ) produces and recycles steel and steel products through a range of assets, including recycling facilities, eight mini mills, two micro mills, and fabrication facilities in the United States and Poland. CMC is a leading producer of rebar in the U.S., with a market share of 35%, and primarily serves the construction industry. Although CMC is small compared to its peers, with a market cap of under $6B, it is positioned exceptionally well and should provide shareholders with continued upside over the long term. Out of 8 sell-side analysts I track that cover CMC, three have a buy rating and 5 have a hold rating pointing to limited enthusiasm for the name. Although the upcoming year won't be without challenges, the opportunity in front of CMC is substantial. Let me explain why.

In 2023, metal spreads will be under pressure

While 2022 was a highly successful year for Commercial Metals Company, this new year is likely to present some challenges. There is a good likelihood of a small decrease in North American finished steel volumes in the current quarter, which is in line with past trends. I also anticipate more difficult market conditions in Europe due to the ongoing energy crisis and slowing industrial and residential activity. Additionally, metal spreads in North America and Europe will be under pressure in the current quarter due to changes in raw material prices and increased supplies of long products which could erode some margins.

However, there are plenty of positive tailwinds for CMC

Despite a few dark clouds, there are enough silver linings and positive tailwinds to help Commercial Metals Company through 2023. In fact, I expect several factors to contribute to growth in the construction industry and demand for steel products in the coming months and years. One of these is the recent federal infrastructure package, which includes a significant increase in funding for surface transportation and is expected to lead to the addition of 1.5 million tons of incremental annual rebar consumption, with related projects expected to enter the pipeline in 2023.

The Dodge Momentum Index has also been showing strength, with the August reading being the second highest in 14 years and indications of strength in commercial and institutional non-residential starts. CMC has also reported strong downstream bid activity, with average pricing reaching a new record in 4Q 2022 and volumes being the second-highest ever, across a range of sectors and geographies. This tells me that expansion is taking place in non-residential spending over the next 9 to 12 months, with 19 consecutive months of expansionary readings and the southern U.S. being the strongest region. Non-residential investment is often driven by residential construction, with local infrastructure and non-residential investments supporting newly formed residential communities, which generally follow residential construction by 12 to 18 months. Perhaps most importantly, there is structural trend towards reshoring critical industries, with several large projects already underway and the potential for more industries to be targeted as the global supply chain continues to be rebalanced. The ongoing Ukraine war has highlighted the vulnerabilities of key industrial commodities to unexpected events. This will benefit CMC.

CMC has a record backlog of downstream orders, which are currently at historically high levels in terms of both volume and average pricing. The company has also invested approximately $900 million in working capital since the end of FY 2020. CMC's highly flexible operations network allows them to optimize production across facilities and products in a variety of demand scenarios.

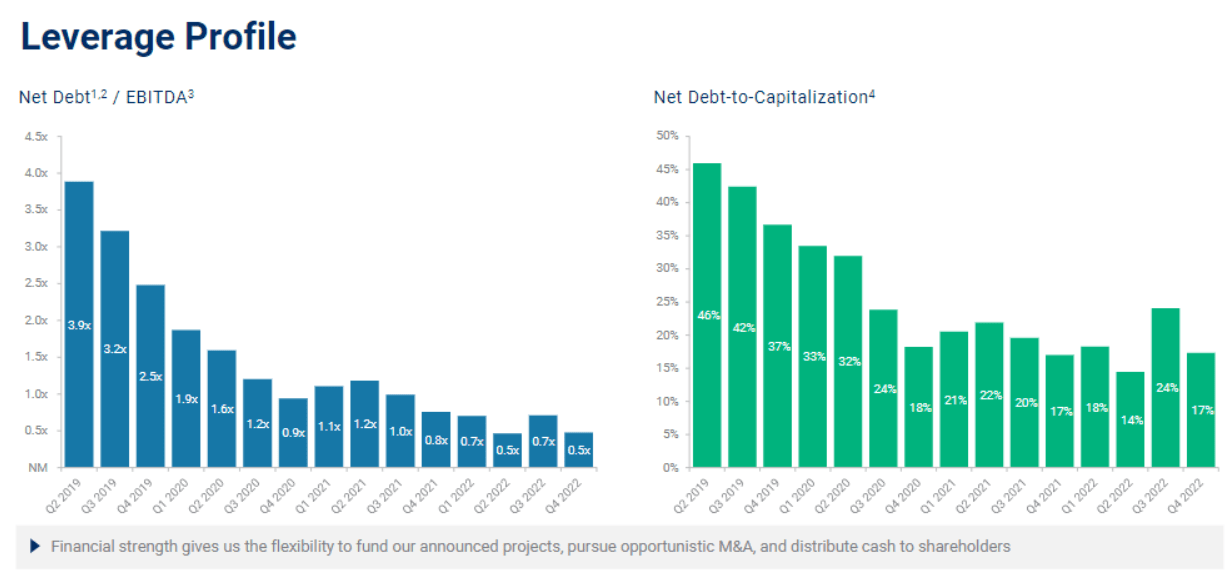

CMC has materially improved its leverage profile, giving it flexibility

{kind=link}

CMC has materially improved its leverage profile over the past three years with Net Debt/EBITDA sliding from 3.9x to 0.5x between Q2 2019 and Q4 2022. Having a strong financial foundation gives CMC the ability to fund their announced projects, pursue opportunistic mergers and acquisitions, and distribute cash to shareholders. This financial flexibility allows the company to take advantage of new opportunities and invest in their business, while also returning value to shareholders. This can help to drive long-term growth and shareholder value.

Significant capital returns to shareholders continue

CMC's debt reduction has not come at the expense of shareholder capital return. CMC shareholder cash distribution programs have included a $350 million share repurchase program ($188 million remaining) and a quarterly dividend of $0.16 per share, which was increased by 14% in Q4 2022. These programs are in place despite the company also working to pay down debt. The company continues to demonstrate commitment to returning excess cash to its investors.

CMC going from strength to strength

CMC has made significant progress in implementing their strategic plan for growth. They have completed the acquisition of Tensar, which will provide a new platform for growth, and the timing for the commissioning of Arizona 2 is on track, with startup expected in the spring of 2023. The company has also announced plans to build a fourth micro mill in the Eastern United States and is in the process of finalizing the site selection. CMC has also introduced a carbon-neutral line of long steel products called RebarZero, which provides the construction industry with a net-zero solution from the mill to the job site. Despite facing disruptions related to the Ukraine war, the European energy crisis, and global supply chain challenges, CMC Europe achieved record financial performance.

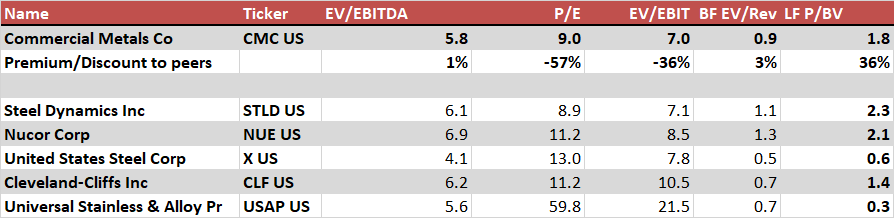

CMC trades at a share discount

{kind=link}

Despite CMC's strong share price performance, its valuations remain reasonable. The company trades at a share discount on a P/E and EV/EBIT basis and virtually in line when compared to peers on an EV/EBITDA and EV/Revenue basis. Perhaps a small discount is warranted given the smaller size of CMC compared to Steel Dynamics and Nucor.

Investors cannot overlook Commercial Metals Company's relative resilience to the housing slowdown given its business mix. This resilience combined with its balance sheet strength should help CMC outperform its peers over the medium term. Commercial Metals Company deserves to be bought on weakness.

For further details see:

Commercial Metals Company Is Small But Mighty