COMM - CommScope: Not The Right Time To Buy

2023-09-21 08:36:52 ET

Summary

- CommScope Holding's sales are being impacted by high customer inventory levels and the macroeconomic environment.

- The stock has been downgraded by Seeking Alpha's Quant rating system.

- Also, its competitive positioning is not exceptional, while momentum indicators also point to a downside.

- The company may have longer-term opportunities with its RUCKUS One platform, advancements in Wi-Fi technology, and depending on how its debt repayment plan is received by the market.

- In the meantime, I have a Sell position.

CommScope Holding ( COMM ) is not a stock you want to touch at this moment, as according to its own management, in addition to the uncertain macroeconomic environment, sales are also being impacted by higher customer inventory levels.

Also, at $3.42 per share, its price-to-sales multiple trades at a discount of more than 90% compared to other information technology stocks, but, at the same time, it has been downgraded to Strong Sell from Hold by Seeking Alpha's Quant rating system.

In these conditions, the aim of this thesis is to elaborate on the downside risks while also trying to identify potential bright spots, using mainly data from the earnings transcript, and the financial statements, as well as consider competitive positioning.

First, I highlight the reasons for the downgrade.

Reasons for Downgrade

This North Carolina-based communications and technology infrastructure provider designs and manufactures networking products for a range of customers, including schools, hospitals, and U.S. federal agencies . Its most prominent subsidiary is Ruckus.

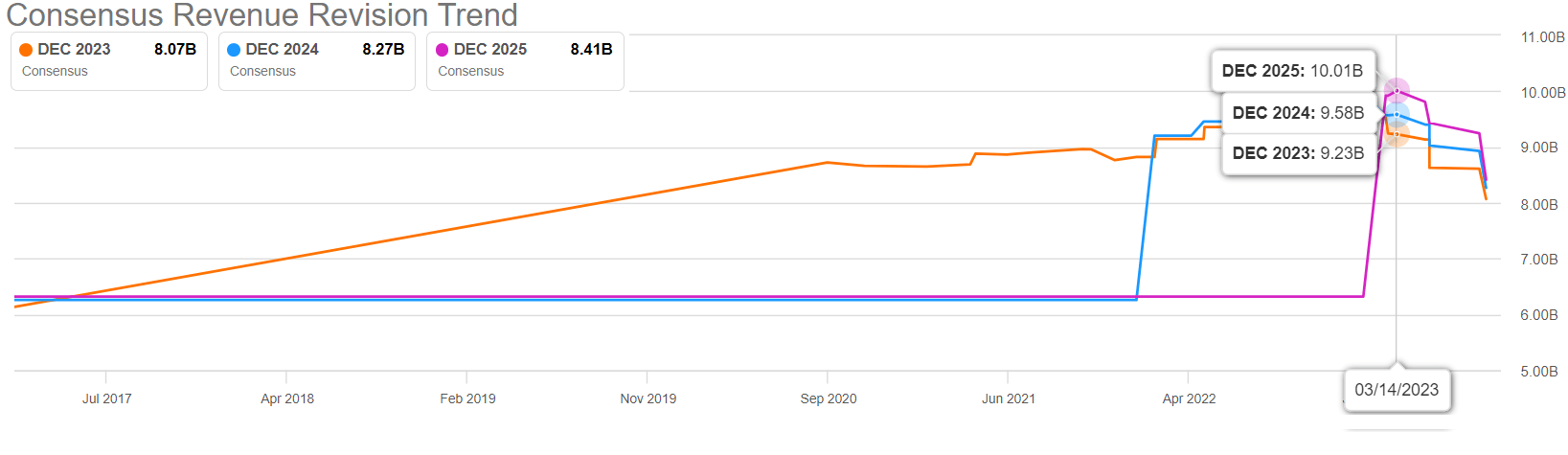

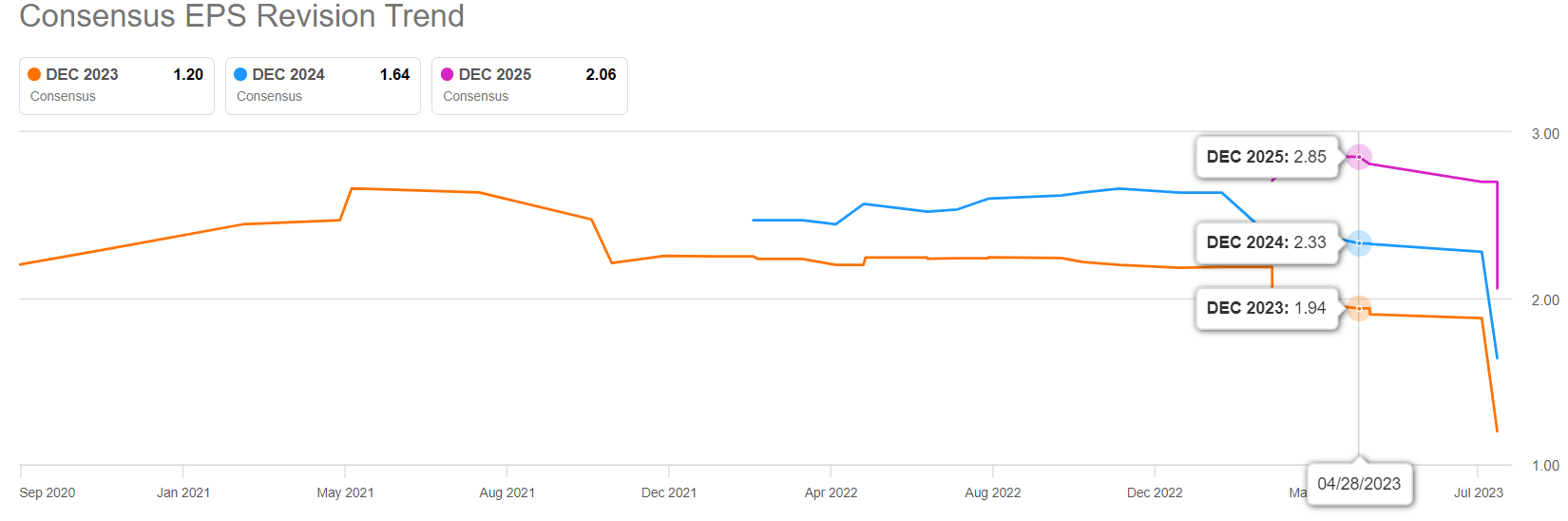

Diving into the financial results, the company's consolidated sales of $1.92 billion in the second quarter of 2023 (Q2) represented a 16.6% decline from the same period last year. Additionally, its adjusted EPS dropped to $0.19 compared to $0.41 in Q2-2022 while at the same time, it missed both revenue and earnings consensus estimates made by analysts. However, even before that, there had been successive downward EPS and revenue growth revisions as charted below.

Thus, the top-line consensus estimate of $9.23 billion prevalent on March 14 was downgraded to $8.63 billion on May 5, before being further cut to $8.61 billion. Eventually, the estimate stood at only $8.07 billion on the 18th of this month.

Consensus Revenue Revision Trend (Seeking Alpha) Consensus EPS Revision Trend (Seeking Alpha)

{kind=link}

{kind=link}

Furthermore, as shown below, there were also successive downgrades for the consensus EPS estimate, from $1.94 on April 28 to $1.20 currently, or a 38% drop.

This deterioration in expected topline and bottom line is validated by the demand outlook which is expected to be impacted during the second half of the year which means continued pressure on sales. Now, there is a $150 million cost savings plan but only about 60% of the benefits should be reaped this year, or $90 million which is far too low to have a meaningful impact on this year's expected revenue deficit of $1.158 billion, or the difference between the fiscal year 2022's $9.228 billion and this year's consensus estimate of $8.07 billion.

In these circumstances, it appears difficult for the company to reverse the negative trend, especially given that the latest CPI figures show the annual inflation rate to have accelerated to 3.7% in August or 0.1% above market forecasts. This means that the Federal Reserve may have to keep interest rates higher for longer as was confirmed by Chairman Powell during the September 20 meeting. This in turn does not augur well for economic growth across the board.

Looking for a Competitive Edge

Still, there may be longer-term opportunities following the launch of the Ruckus One platform and its availability through a network-as-a-service mode. This is the company's AI-driven cloud platform which delivers everything from service delivery and network assurance to business intelligence within a unified dashboard. Additionally, communications equipment play is making rapid strides in Wi-Fi 7 which is faster than the currently widely available Wi-Fi 6 protocol for communicating wirelessly over phones and laptops, and intends to launch related products in the fourth quarter of this year.

Along the same lines, given that customers accumulated CommScope's product at the height of the supply chain crunch in 2022 despite having the choice to purchase from competitors could also show some strength.

To assess the possibility of a potential edge over competitors, I checked its positioning with respect to wireless products on Gartner's website, namely for access points, switches and cloud connectivity, centralized WiFi management, and IOT where the company offers the Ruckus products range. Detailing further, it competes with the likes of Cisco ( CSCO ), Fortinet ( FTNT ), and Extreme Networks ( EXTR ), among others, and scores more or less the same ratings or 4.7 out of 5. This signifies that CommScope's products while being competitive, do not necessarily possess any exceptional quality which could position the company above competitors.

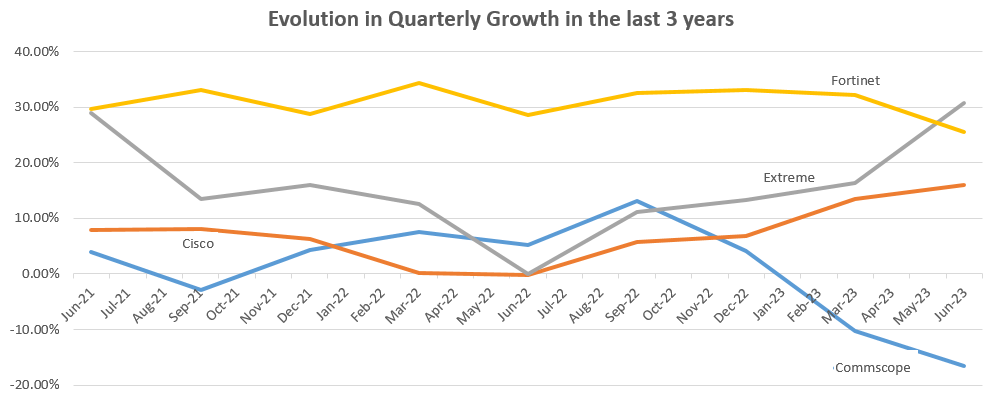

To further validate this observation, I checked the quarterly revenues for the last three years as shown in the charts below.

In this case, CommScope's sales performance has indeed fared better during last year as shown by the blue chart's net uptrend from January to September compared to more muted performances by competitors showing that there was effectively more demand for its wireless products.

Charts Built using data from (Seeking Alpha)

{kind=link}

Now, Cisco did see an uptrend in sales but this came late last year as it was impacted by supply chain issues and, as for Fortinet, its sales progression has been relatively flat during the last three years before coming down in the first half of this year while Extreme has clearly outperformed in 2023.

On the other hand, after the September 2022 quarter, CommScope's sales went on a sharp downtrend in contrast with Cisco and Extreme which have seen improvement. Thus, CommScope's rapidly losing market share can be explained not only by deteriorating macros but also possibly due to the supply chain normalization. In this case, the company appeared to have benefited from its larger inventories during the supply crunch of 2021-2022 as charted in green below which is second only to networking giant Cisco.

Thus, helped by its stronger stock levels going into 2022, it was able to satisfy the connectivity requirements of public cloud and enterprise customers looking to expand their footprint as part of the digital transformation trend.

Discussion and Price Action

Now, it would seem weird why after gaining adoption in supply-constrained conditions last year, the North Carolina-based company did not manage to sustain the uptake for its products in 2023. It could be that after purchasing the company's wireless access points mostly as a result of supply scarcity, customers went back to their preferred suppliers.

Another reason could be related to the ransomware attack.

As such, Hackers allegedly gained access to its network back in April this year and managed to steal data pertaining to one of the company's customer portals as well as its internal intranet. The incident may have taken a toll on the security side of things especially since customers include U.S. federal agencies.

In response, CommScope denied that customer information was compromised, and also confirmed that business operations were minimally impacted and additional safeguards were put in place as preventive actions.

However, the incident consumed $1.7 million of adjusted EBITDA in Q2, and when you are a provider of networking infrastructure for large companies worldwide including the government, and your own system has been hacked, it is not only embarrassing for the corporate image, but customers, especially new ones may think twice before selecting you.

Talking reputational damage, a survey by PricewaterhouseCoopers found that 87% of consumers are prepared to walk away from a business where a data breach has occurred. Thus, in addition to putting in place measures to protect itself from bad actors as CommScope has already done, it may also have to do more, like dedicating extra effort to preserving relationships with consumers and regularly communicating the same, for example during earnings calls.

Looking at the price action, in the aftermath of the incident which occurred around April 17, shares fell from around $4.95 to $4.55 before subsequently recovering, with another factor impacting the stock being the debt level and forthcoming maturities, with the nearest one due in 2025. To address this in a proactive way, the company is considering several options to be shared with investors during the next earnings call. Thus, shares could produce an upside around November 3 when third-quarter results are announced especially in case CommScope has been able to reduce debt by performing some opportunistic buybacks of securities, as is planned.

Further Downside Risks and Looking Ahead to 2024

However, in case the debt repayment plan is not well digested by the market, the stock could drop to around $2.55 from the current share price of $3.40 based on a 25% downside, or approximately the same percentage it fell at the beginning of August when Q2's results were announced. This possibility of a downtrend is also supported by momentum indicators whereby the share price is under the 50-day and 100-day SMAs.

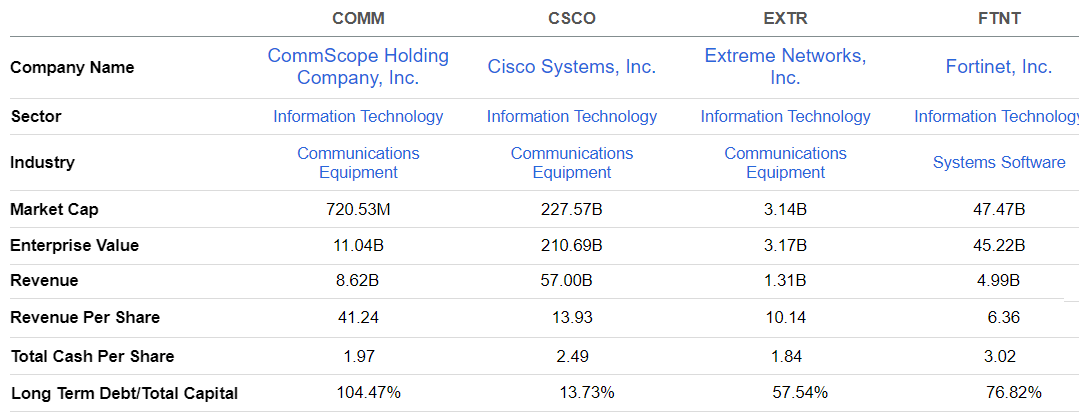

Therefore, I have a Sell position, based mainly on the topline and bottom line downgrades, and after analyzing the finances and actual competitive positioning. Still, for investors who want to position themselves after the drop, while CommScope's debt level remains high relative to peers as shown below, the company still generates cash from operations.

Comparison with Peers (Seeking Alpha)

{kind=link}

Furthermore, looking at opportunities for 2024 and beyond, CommScope's market cap has now shrunk to about $720 million which imparts to it a revenue per share of over $41.24 which is much higher than peers. Also, as I pointed out earlier, it remains significantly undervalued relative to the IT sector.

However, factors to look for before investing are updates on the demand for Ruckus One launched at the end of June, and also for WiFi 7 planned to hit the market in the fourth quarter, or two factors that could improve product competitiveness. Additionally, there is a need to assess how customers' inventory levels have evolved, as well as progression on the debt front. Finally, it is important for the management to identify the benefits in dollar terms to be obtained by aggressively reviewing the cost structure.

For further details see:

CommScope: Not The Right Time To Buy