COMM - CommScope Q3: Worsening Financial Performance

2023-12-14 17:10:03 ET

Summary

- COMM has consistently experienced a decline in revenues and profits, with weak demand and challenging macro conditions expected to continue in the near future.

- The company's Q3 FY2023 results showed a decline in revenue and profits across all segments except for NICS, which saw a 12% increase in revenue.

- COMM's high debt and poor financial performance pose significant risks.

Investment Thesis

CommScope Holding Company, Inc. ( COMM ) is a network solutions provider headquartered in Claremont, North Carolina. In this thesis, I will analyze its third-quarter results and its future growth prospects. I will also be analyzing its valuation at current price levels and the stock's upside potential. COMM has consistently witnessed a decline in revenues and profits, and the situation doesn't seem to be improving in the near future. I believe weak demand and challenging macro conditions will keep its revenues muted throughout FY23 and FY24, and hence, I assign a Hold rating for COMM.

Company Overview

COMM is a global player in infrastructure solutions for communications networks. It is known for providing a comprehensive suite of network infrastructure solutions. This includes products such as fiber optic and copper cables, connectivity solutions, and wireless infrastructure products. Its business can be categorized into five segments: Connectivity and Cable Solutions [CCS], Networking, Intelligent Cellular and Security Solutions [NICS], Outdoor Wireless Networks [OWN], Access Network Solutions segments [ANS], and Home. COMM has a global presence, with most of its revenue generated from the United States, followed by EMEA countries and Asia Pacific.

Q3 FY2023 Result

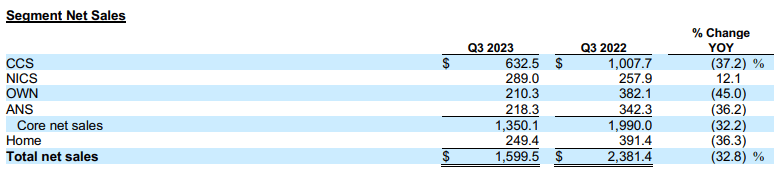

COMM posted weak third-quarter results on November 9th , missing the market revenue and EPS estimates by 4% and 7.2%, respectively. The company experienced a decline in revenue and profits across all business segments except NICS. The NICS business segment witnessed a y-o-y 12% increase in revenue; the rest reported a significant fall on the sales front. Its product, called RUCKUS One, which is an AI-driven cloud-native platform, primarily drove revenue growth in the NICS segment. I believe this segment will keep outperforming other segments in the coming quarters, given the increasing demand for AI-based solutions. What is disappointing is that the company has not been able to capitalize on the tailwind in the CCS industry; it is losing clients despite increasing demand for connectivity solutions. The management is optimistic about a recovery in the CCS segment, but I believe it will have to come up with new strategies to increase its client base rather than focusing on cost-cutting, as this is costing them severely in terms of sales.

{kind=link}

COMM reported total net sales of $1.6 billion , a steep decline of 32.8% compared to $2.38 billion in the same quarter last year. As per my analysis, the fall in revenue from the CCS segment primarily dragged the revenues. The CCS segment witnessed a fall of 37.2% in revenues to $632 million, compared to $1007 million in the corresponding quarter last year. As per management, the clients are cutting back on new orders as a cost-cutting measure due to high interest expenses, but I think the problem is much deeper. COMM is focusing excessively on cutting costs, which is hampering its revenue growth. The NICS segment reported revenues of $289 million, up 12% compared to $258 million in the same quarter last year. The OWN segment revenues stood at $210.3 million, down 45% compared to $349.1 million in the same quarter last year. One thing I would like to highlight is that the ANS and Home segments reported a one-time goodwill impairment charge of $425.9 million and an intangible asset impairment charge of $469.2 million, respectively. These charges don't have any impact on its cash flow, but it was a step to adjust to the current market value of its ANS and Home brand. It reported a net loss of $828.7 million, compared to net profit of $23 million in the same quarter last year. Reflecting a diluted loss per share of $3.98, compared to EPS of $0.04 in Q3 FY22. If we take away the asset impairment charges, then as per non-GAAP accounting measures, it reported a diluted EPS of $0.13. It showed improvement in the non-GAAP net income primarily by cutting down on its operational expenses. However, these cost-cutting measures came at the cost of reduced headcount and dedicated resources in all business segments.

Overall, the company failed to impress me on multiple parameters, including revenue growth and operational expansion. The management's FY23 guidance doesn't exude much confidence either, with FY23 Core adjusted EBITDA guidance in the range of $1-$1.05 billion from earlier guidance of $1.15-$1.25 billion. The management expects to face macroeconomic headwinds and expects the number to be stressed even in FY24. I believe it must take steps to ramp up its sales strategies, specifically in the United States, focusing on driving the NICS segment products and capitalizing on the transition towards AI that many companies are targeting. Given the current situation, I would recommend existing to hold the stock, but initiating a new buying position is not advisable.

Key Risk Factor

High Debt: When we look at its balance sheet, the situation gets even worse. As of September 30, 2023, it reported cash and cash equivalent of $519 million against long-term debt of $9.35 billion. It ended the quarter with a net leverage ratio of 6.7x. Generally, a net leverage ratio above 2.5x is considered problematic depending on the kind of industry any company is operating in. With respect to COMM, which operates in a low capital-intensive industry, a net leverage ratio of 6.7x is quite severe. This is putting significant stress on the company's balance sheet, which could result in serious problems for the company, given its poor financial performance. The high debt is resulting in sizable interest expenses for the company. To put this in perspective, it incurred interest expenses of $171.3 million in Q3 FY23, compared to $150.9 million in the same quarter last year, denting its profit margins. I would recommend investors consider this risk before investing in COMM.

Valuation

COMM is currently trading at a share price of $2.6, a YTD decline of 65%. It has a market cap of $481.5 million. It is trading at a forward non-GAAP P/E multiple of 3.5x with an FY23 EPS estimate of $0.74. Comparing this to the sector P/E of 23.5x, I believe it is trading at a cheap valuation. But this isn't necessarily a positive aspect; the cheap valuation is a result of a fall in price and not an increase in earnings. The stock price has witnessed a steep decline in the past few months, and this is the only reason behind my assigning a hold rating for the stock, as the downside seems capped at current price levels. I would recommend existing investors hold the stock for now but utilize any pullback in stock price and exit the stock at the $3.3-$3.8 level.

Conclusion

The revenues have been consistently deteriorating, which shows no signs of material improvement in the upcoming quarters. Weak EBITDA guidance and headwind projections from the management don't instill much confidence either. It has a high debt obligation, which could have a severe impact on the company if it continues to perform poorly. Considering all these growth and risk factors, I assign a Hold rating for COMM.

For further details see:

CommScope Q3: Worsening Financial Performance