BBCP - Concrete Pumping Holdings: A Potential Recovery In Construction Market Should Drive Shares Higher

2023-12-12 09:34:40 ET

Summary

- Concrete Pumping Holdings, Inc. is well-positioned to benefit from government stimulus and potential interest rate cycle reversal, driving growth in commercial and infrastructure markets.

- The company has posted strong revenue growth, with increases in its U.S. Concrete Pumping, U.K. operations, and Eco-Pan segments.

- Margins are expected to improve due to operating leverage, price increases, focus on higher-margin projects, and an increasing mix of high-margin Eco-Pan business.

Investment Thesis

Concrete Pumping Holdings' stock (BBCP) is up slightly since my previous coverage in August. The company is well-positioned to benefit from strength in the large commercial and infrastructure end markets fueled by multiyear tailwinds from government stimulus such as the Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA). In addition, the potential interest rate cycle reversal next year could catalyze recovery in residential and light commercial markets as well. Moreover, the company's revenue growth is poised to benefit from market share gains from cross-selling opportunities in the Eco-Pan business.

The outlook for margin growth is also good, supported by the advantages of operating leverage derived from sales growth. The improving end-market conditions should facilitate the company's ability to implement price increases and concentrate on higher-margin projects. Moreover, the strong growth in the higher-margin Eco-Pan business should enhance the sales mix positively. Considering the reasonable valuation and good growth prospects, I believe BBCP stock is a good buy.

Revenue Analysis and Outlook

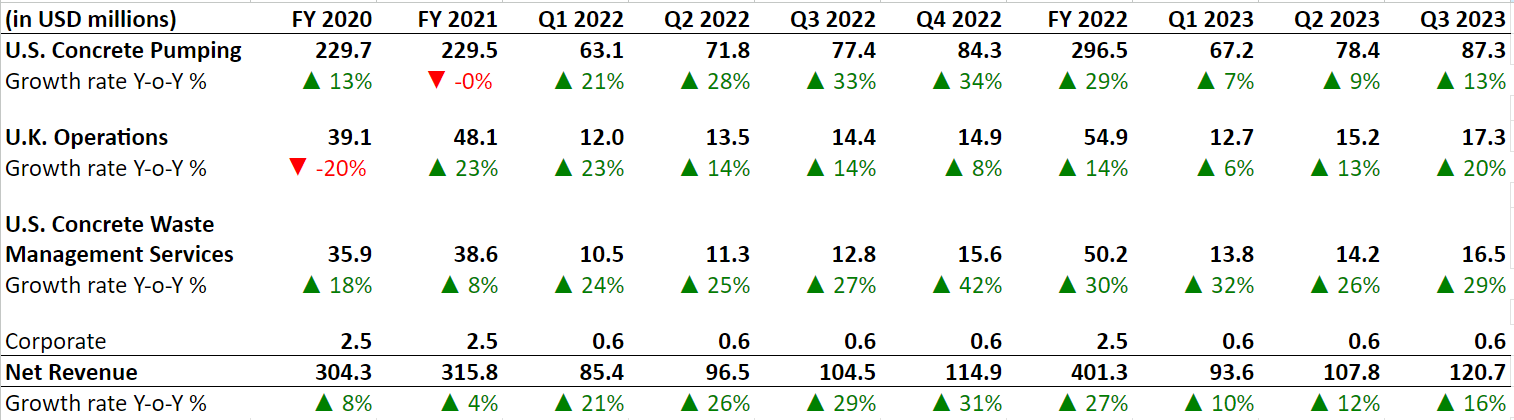

BBCP has posted strong growth in recent years, benefiting from good execution, strong end market demand as well as M&A. In the third quarter of 2023, the company's U.S. Concrete Pumping segment revenue grew 13% Y/Y driven by a $5.6 million contribution from the Coastal Carolina acquisition and pricing improvements. In the U.K. operations segment, which primarily operates under the Camfaud brand, revenues increased by 20% Y/Y ( 18% Y/Y excluding the impact of FX translation), mainly due to improved pricing across the U.K. region. In the U.S. Concrete Waste Management Services segment, which primarily operates under the Eco-Pan brand, revenues rose by 29% Y/Y organically, attributed to continued market expansion and penetration of the Eco-Pan business and pricing improvements. On a consolidated basis, revenues increased 16% Y/Y to $120.7 million in the third quarter.

BBCP's Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I am optimistic about the company's revenue outlook. The company derives all of its revenues from construction end markets and a potential reversal in the interest rate cycle starting mid-2024 could catalyze its revenue growth as lower interest rates helps to increase the return on investment for construction projects and this could boost demand.

End market-wise, the company derives ~60% of its revenues from commercial, ~28% from residential, and ~12% from publicly funded infrastructure market.

In the commercial end-market, the company is experiencing positive momentum in heavy construction and large-scale commercial projects, such as semiconductor fabrication plants, electric vehicle and battery manufacturing plants, and tech/data centers. The recent reshoring trend, driven by companies seeking to expand their domestic footprint and incentivized by federal funding initiatives like the CHIPS and Science Act and the Inflation Reduction Act, is contributing to the increased demand for heavy manufacturing construction. I anticipate this demand will remain robust over the next few years, supported by the ongoing deployment of federal funds and the multiyear nature of these projects.

While light commercial construction has been seeing some softness due to the high-interest rate environment, I expect this market to also improve next year once the interest rate cycle starts reversing.

In the residential market, the demand environment has remained relatively resilient so far despite high interest rates due to ongoing structural supply-demand imbalance in housing due to over a decade of underbuilding of new homes since the great recession. I believe this market should see a swift recovery once the interest rate cycle reverses due to the pent-up demand in the market.

On the infrastructure side, the company is well-placed to benefit as fund deployment under the Infrastructure Investment and Jobs Act continues to accelerate. On its last earnings call, management noted improved visibility on these funds and called it a five-year plus tailwind. Below is the relevant excerpt.

We will continue to work to win projects at the state and local levels and look forward to renewed investment in the U.S. with the Infrastructure Investment and Jobs Act. We continue to see an improved visibility of funds flowing to numerous projects, many of which are located in existing markets where we operate. We plan to aggressively pursue these project opportunities and believe it has the potential to be a five-year plus tailwind for our business."

-Bruce Young, CEO, on BBCP Q3 earnings call

In addition to end-market improvement, the company is also well-placed to increase its market share, especially in its U.S. Concrete Waste Management Services segment which operates under the Eco-Pan brand. This segment saw a 29% Y/Y increase in organic revenue last quarter and has strong multiyear growth prospects driven by cross-selling opportunities with U.S. Concrete Pumping clients. Every concrete placement necessitates a washout service. While the company's concrete pumping business has a market share of ~17%, the market share of its Eco-Pan business is only mid-single-digits. So, there is a good market share gain opportunity for Eco-Pan business as the company cross-sells Eco-Pan services to its existing concrete pumping clients. The company has been very successful in this regard as is evident from strong growth in the Eco-Pan business in the recent quarters and I expect the double-digit growth in this business to continue.

Overall, the company has strong growth prospects moving forward, driven by government stimulus from IIJA, CHIPS and Science Act, and Inflation Rection Act helping large commercial construction and Infrastructure end markets; a potential reversal in the interest rate cycle next year should help residential and light commercial construction; and the market share gain opportunity in Eco-Pan business.

Margin Analysis and Outlook

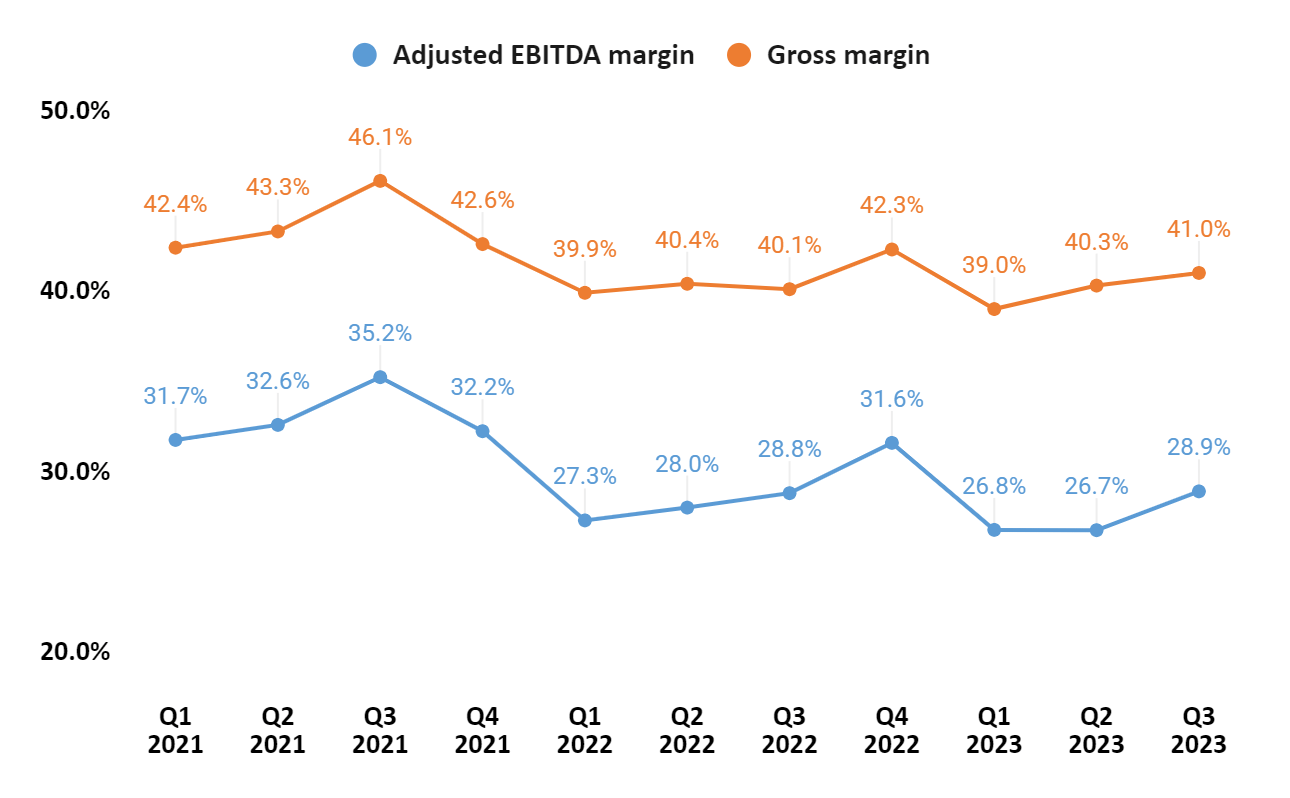

In Q3 2023, the company saw a 90 bps Y/Y expansion in gross margin to 41% and a 10 bps Y/Y expansion in adjusted EBITDA margin to 28.9% driven by strong Y/Y revenue growth and the easing of diesel fuel prices which more than offset the higher inflationary costs related to labor inflation.

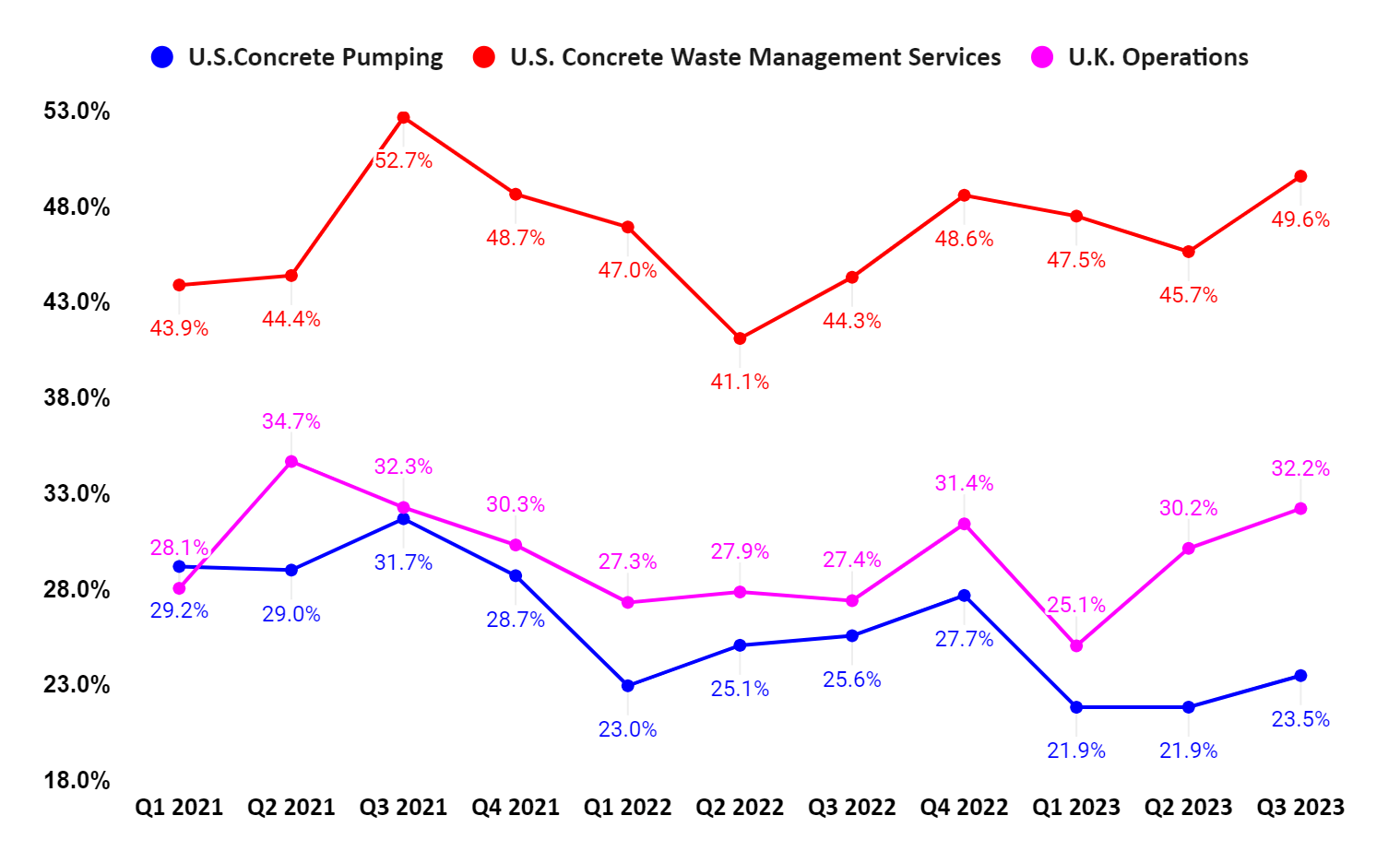

On a segment basis, the adjusted EBITDA margin improved by 480 bps Y/Y in the U.K. operations segment and 530 bps Y/Y in the U.S. Concrete Waste Management Services segment. However, the U.S. Concrete Pumping segment's adjusted EBITDA margin declined by 210 bps Y/Y in the third quarter.

BBCP's Gross Margin and Adjusted EBITDA Margin ( Company Data, GS Analytics Research) BBCP's Segment Wise Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking ahead, the company's margins are expected to gain from operating leverage resulting from increased sales. Additionally, as the interest rate cycle reverses and end market demand improves, the company should find it easier to implement price hikes and adjust rates to counteract labor cost inflation. The end-market strength should also enable the company to concentrate on high-margin projects.

Moreover, I anticipate that the company's Eco-Pan segment will sustain a higher organic growth rate compared to other segments, driven not only by robust end-market demand but also by ongoing market share gains. Eco-Pan has a higher margin than other segments and a higher growth rate there should help lift the company's overall margins.

Valuation and Conclusion

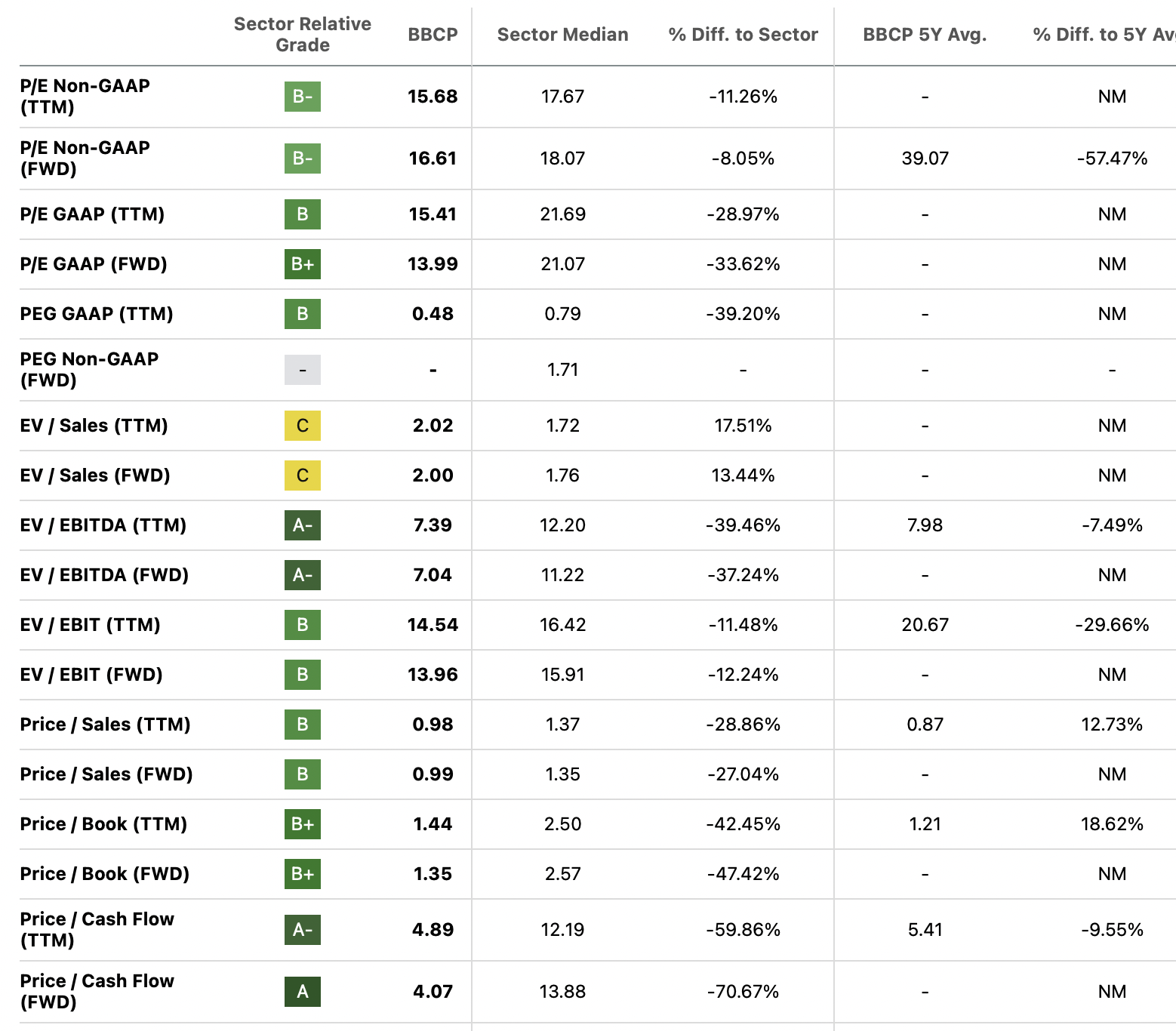

BBCP is currently trading at a 12.96x FY24 consensus EPS estimate of $0.62 and a 9.72x FY25 consensus EPS estimate of $0.82, which is lower than the Company's 5-year average forward P/E of 39.07x. The stock's valuation also compares favorably with the sector median.

BBCP Valuation Grade (Seeking Alpha)

{kind=link}

The company possesses strong revenue growth and margin expansion prospects aided by robust demand in large construction and infrastructure end markets thanks to the federal funding from IIJA, CHIPS and Science Act, and IRA, resiliency in the residential end-market due to the tight supply-demand conditions in this market, Eco-Pan cross-selling and market share gain opportunity, operating leverage and strong organic growth in higher-margin Eco-Pan business. Further, once the interest rate cycle turns next year, the company's light commercial and residential end markets are likely to see a recovery which should benefit the revenue and margin growth. Given the strong growth prospects and a reasonable valuation, I have a buy rating on the BBCP stock.

For further details see:

Concrete Pumping Holdings: A Potential Recovery In Construction Market Should Drive Shares Higher