BBCP - Concrete Pumping Holdings: Good Growth Prospects At Attractive Valuation

2023-03-26 03:50:44 ET

Summary

- BBCP should witness growth in commercial and infrastructure end markets. This growth, coupled with market share gains, expansion of Eco-Pan, and benefits from recent acquisitions, should drive revenue growth.

- The adjusted EBITDA margin should improve, driven by lower diesel prices and mix shift towards higher-margin commercial projects.

- Valuation is attractive.

Investment Thesis

Concrete Pumping Holdings, Inc. ( BBCP ) is expected to see an increase in volume in the commercial and infrastructure end market. This coupled with benefits from recently acquired businesses, market share gain and Eco-pan expansion should drive increased revenue in FY2023.

The margin outlook is also good and the adjusted EBITDA margin should improve in FY2023 due to lower diesel prices and mix shift towards higher-margin commercial projects. BBCP Stock is trading at an attractive valuation which coupled with good growth prospects make it a buy.

Revenue Analysis & Outlook

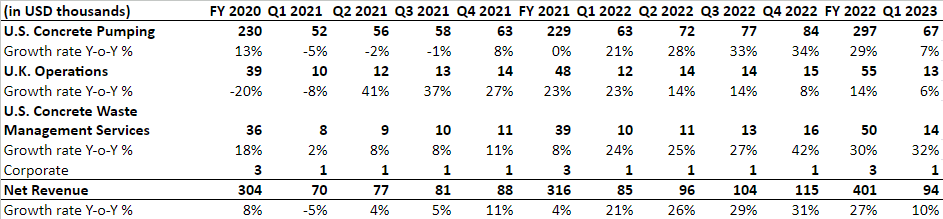

BBCP's business model, which focuses on market share gains, M&A, and expansion of ECO-Pan offering, demonstrated resilience and helped the company generate good results in the last few years. This momentum continued in the first quarter of FY2023, with a 10% Y/Y increase in revenue driven by volume growth from recent acquisitions, organic growth in Eco-Pan, and price improvements.

BBCP’s Historical Revenue Growth (Company data, GS Analytics Research)

{kind=link}

Looking ahead, while there are some concerns around volume slowdown in residential end markets, volume growth in the commercial and infrastructure end markets should more than offset it. Additionally, benefits from recently acquired businesses and BBCP's focus on market share gain and Eco-Pan expansion are expected to provide additional upside to revenue growth.

End markets

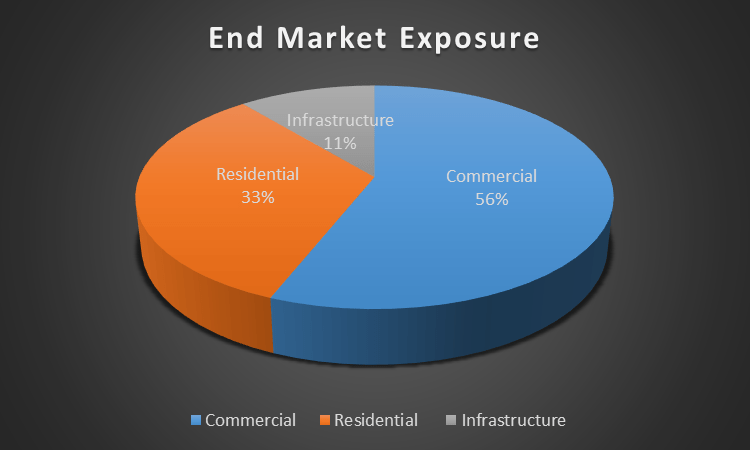

The company derives ~56% of its revenue from Commercial, ~11% of its revenue from Infrastructure and the rest from the Residential end market.

{kind=link}

Demand in the commercial end market is expected to remain healthy in the coming years, driven by the ongoing trend of onshoring manufacturing facilities. Supply chain constraints and material unavailability have affected many industries in 2022, leading many companies to start onshore manufacturing facilities. For example, Micron recently announced a ~ $40 billion investment for its US manufacturing facilities. The US government has also announced CHIPS and Science Act which earmarks funds to encourage reshoring. This means more construction by commercial clients and should help BBCP. Further, the recovery in the hospitality sector as the economy reopens and travel resumes should also create a healthy environment for the construction industry and benefit BBCP.

The infrastructure end market is expected to remain resilient, with benefits from the HS2 high-speed rail line project in the UK providing tailwind to revenue in the coming quarters. HS2 is a concrete-intensive high-speed railway project being built from London to the North-West, linking the biggest cities in Scotland with Manchester, Birmingham and London. Another big driver in infrastructure end market is the Infrastructure Investment and Jobs Act (IIJA) which includes a $110 billion investment by the US government for roads, bridges, and major projects. Although the company has not included benefits from IIJA in its revenue guidance for FY2023, I believed that orders related to IIJA should also start benefiting the company in towards the back half of this year.

The residential end is expected to remain under pressure in the near term due to high-interest rates. The interest rate increases by Federal Reserve have started to impact the housing market and there has been a significant slowdown in housing starts. However, I see light at the end of the tunnel and believe the Federal Reserve should be less hawkish post the recent banking fiasco. So, the housing market is likely to bottom this year and we can start seeing some recovery in this end-market as well from the next year.

Market share growth and tuck-in acquisitions

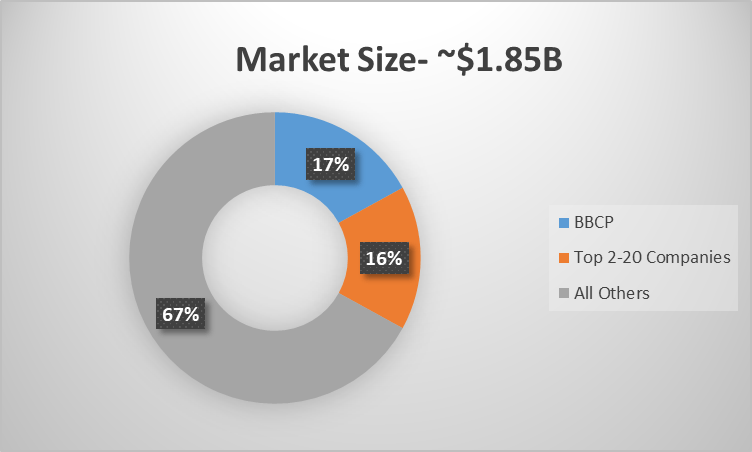

BBCP has a good opportunity to gain market share. The total addressable market size for concrete pumping services in the U.S. is approximately $1.85 billion and BBCP currently holds a 17% share of this market. The company's fleet of specialized equipment and highly-trained operators facilitates significant labour cost savings, shorter concrete placement times, enhanced worksite safety, and efficient concrete washout containment for its customers. These value propositions should help the company increase its market penetration in the future. Moreover, BBCP currently provides concrete pumping services from approximately 95 branch locations across 20 states in the U.S. and serves 16 locations in the U.K. from around 30 branch locations. The company is continuously investing to build a larger fleet of equipment, which should help to expand its business in other regions of the U.S. and the U.K. and gain market share.

U.S. Concrete Pumping Services (Company data, GS Analytics Research)

{kind=link}

In addition to organic growth, tuck-in acquisitions have been a core aspect of BBCP's growth strategy for many years. The recent acquisition of Coastal and Pioneer Concrete Pumping should help the company expand its presence in the Carolinas, Florida, Georgia, and Texas and generate increased revenue in FY2023. In the long term, I expect the company to continue pursuing strategic acquisitions to deepen its local presence and expand into adjacent geographies.

Eco-Pan Opportunity

BBCP's Eco-Pan business is a secular growth tailwind for the company and should continue to generate good revenue growth in the future. This business supports its customers meet regulatory requirements and achieve their sustainable goals by eliminating environmental issues caused by concrete washing. This is a cross-selling opportunity for BBCP's concrete pumping business. The company's concrete pumping business has a market share of ~17% while Eco-Pan's market penetration is only ~5%, indicating a runway for growth.

Eco-pan’s total US market opportunity (Company’s investor presentation)

If we look at the healthy commercial and infrastructure end markets, market share gain opportunity in the concrete pumping business, cross-selling opportunity in the Eco-pan business and inorganic growth prospects, the company should be able to post good growth in the current year. The growth should continue in 2024, once the residential end market bottoms and start recovery and the projects from IIJA funding gain momentum.

Margin Analysis & Outlook

In FY2022, BBCP's adjusted EBITDA margin decreased Y/Y due to diesel price escalation, wage inflation, and increased labour expenses resulting from additional headcount following recent acquisitions. These factors continued to negatively impact margins in the first quarter of FY2023, with the adjusted EBITDA margin down 50 basis points Y/Y.

BBCP Adjusted EBITDA Margin (Company data, GS Analytics Research)

{kind=link}

Looking forward, I believe the adjusted EBITDA margin should improve in the coming quarters, driven by lower diesel prices and higher-margin projects.

Inflationary pressure related to diesel prices has negatively impacted margins in the last few quarters as they increased post-Russia-Ukraine war started. However, diesel prices have been correcting of late. Continued normalisation in diesel prices coupled with easier Y/Y comparison (diesel prices spiked in Feb 2022 and are now meaningfully lower Y/Y) should help the margins. Additionally, volume growth in the commercial end market and a decline in the residential end market should also help mix as the commercial end market typically carries higher margin projects. Further, the synergy benefits from integration of recent acquisitions and operating leverage from higher revenues should also help margins. So, I am optimistic on margin improvement prospects.

Valuation & Conclusion

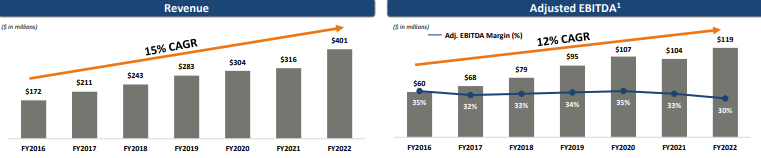

Concrete Pumping Holding Inc. is currently trading at a P/E of 13.79x FY2023 consensus EPS estimates of $0.51 and its EV/EBITDA ((FWD)) is 6.55x . The company’s valuation looks attractive given its solid history of growth. BBCP has grown its revenue at a CAGR of ~15% from FY2016 to FY2022 and Adjusted EBITDA at a CAGR of 12% from FY2016 to FY2022.

BBCP Historical Revenue and EBITDA growth (Company’s investor presentation)

{kind=link}

I expect this growth to continue given the management’s focus on market share gain, inorganic growth, the opportunity to cross-sell Eco-pan offerings, and healthy commercial and infrastructure end markets. While margins have been impacted by inflationary headwinds, I expect it to recover as well in the coming years. Given the company’s good growth and margin expansion prospects continued with an attractive valuation, I believe it is a buy.

For further details see:

Concrete Pumping Holdings: Good Growth Prospects At Attractive Valuation