GVA - Concrete Pumping Holdings: Solid Upside Still Exists

Summary

- The management team at Concrete Pumping Holdings has done well to grow the business as of late, with sales, profits and cash flows rising.

- This is impressive in the current environment, as is management's guidance for 2023.

- Add in how cheap shares are, and the firm warrants upside from here.

One of the companies that I have been bullish on that has demonstrated some rather robust results as of late is Concrete Pumping Holdings ( BBCP ). The firm, which provides customers with concrete pumping services across the US and the UK, continues to generate strong sales growth and excellent profitability. The current expectation by management is that this trend will continue at least through the 2023 fiscal year. Add on top of this the fact that shares of the business are attractively priced at this moment, and I do believe that the ‘buy’ rating I assigned the stock previously still makes sense.

Pumping out gains

Back in the middle of November of last year, I revisited Concrete Pumping Holdings to see how the company was doing from a fundamental perspective. Even though shares of the business had fallen during that time while the broader market generated upside, fundamental data was promising. Sales and cash flow figures were both coming in strong and shares of the business looked to be trading on the cheap. So even though the general market sentiment was against the firm, I held strong in my belief that upside potential should exist. Since then, management has done quite well. While the S&P 500 is up 3.4%, shares of the business have jumped by 9%.

{kind=link}

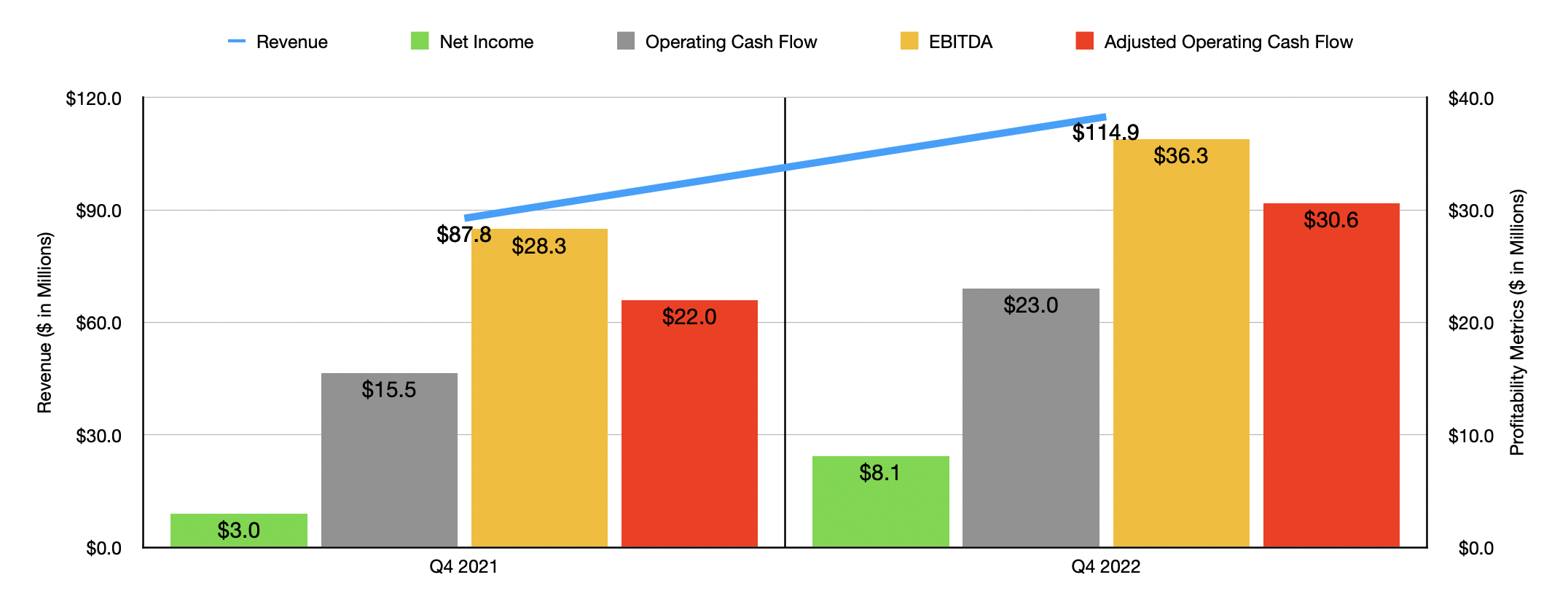

This increase came on the back of robust fundamental data. For instance, during the final quarter of the company's 2022 fiscal year , the only quarter for which new data is available that was not available when I last wrote about it, revenue came in at $114.9 million. That's 30.9% higher than the $87.8 million the company generated only one year earlier. There were multiple contributors, according to management, to this significant sales increase. Primarily, it was driven by robust organic growth caused by higher volumes and rate-per-hour increases that the company charged. Having said that, acquisitions, such as the firm's purchase of Hi-Tech Concrete Pumping Services, its purchase of Pioneer Concrete Pumping, and its purchase of Coastal Carolina Pumping, aided the company's top line. All combined, these were responsible for $11.9 million of the sales increase from one year’s fourth quarter to the next.

The rise in revenue brought with it strong profit increases. Net income jumped from $3 million to $8.1 million. In addition to benefiting from the rise in sales, the company saw its general and administrative costs decline from 29.1% of revenue to 26.2%. This drop, when applied to the revenue the company reported for the final quarter, translated to an extra $3.3 million in additional pre-tax profits. Other profitability metrics followed suit. Operating cash flow, for instance, popped from $15.5 million to $23 million. If we adjust for changes in working capital, it would have risen from $22 million to $30.6 million. Meanwhile, EBITDA for the company expanded from $28.3 million to $36.3 million.

{kind=link}

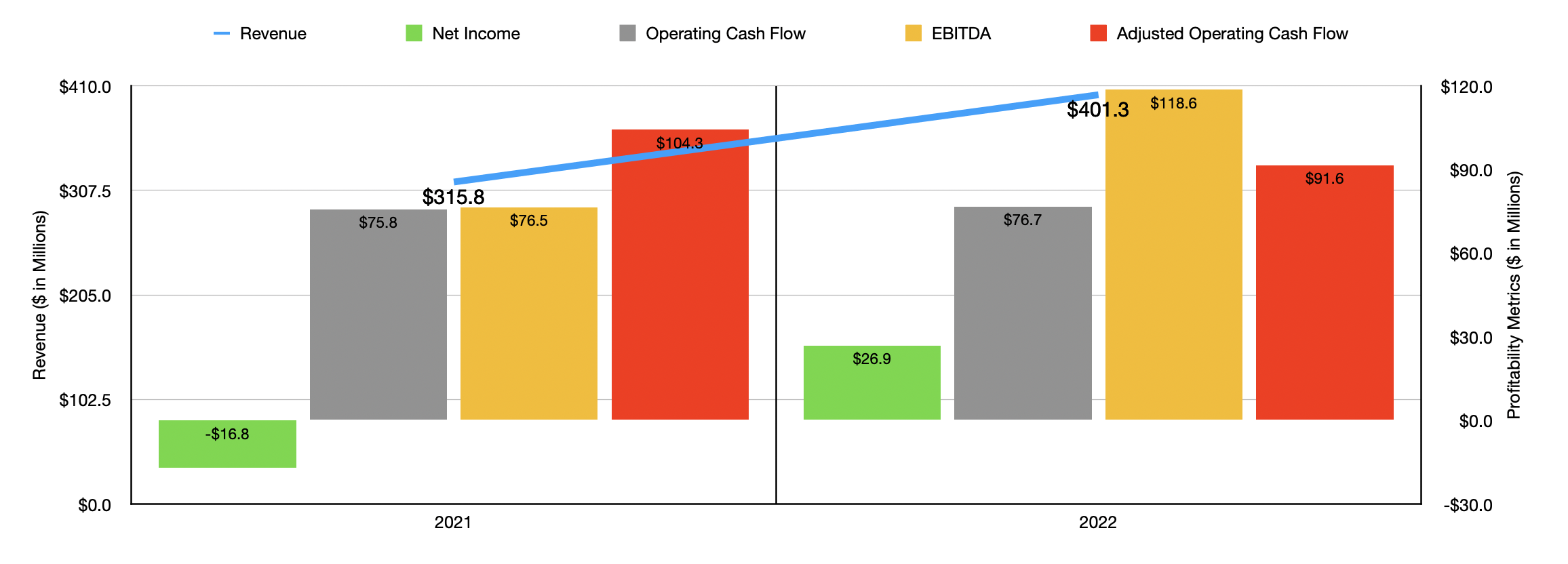

The strong performance achieved in the final quarter of 2022 was very helpful in sales and profits for the 2022 fiscal year in its entirety. For the year, revenue totaled $401.3 million. That's a nice improvement over the $315.8 million generated only one year earlier. The company went from generating a net loss of $16.8 million in 2021 to generating a profit of $26.9 million in 2022. Operating cash flow inched up from $75.8 million to $76.7 million. But the adjusted figure for this rose from $76.5 million to $91.6 million. And finally, we have EBITDA. This metric rose from $104.3 million in 2021 to $118.6 million in 2022. Management felt so confident in the company's financial condition that, in response to its robust financial results, they announced a $10 million increase to their share buyback program last month. That brings their current share buyback capacity up to $17.3 million.

When it comes to the 2023 fiscal year, management has provided a good deal of guidance . Revenue is currently expected to be between $420 million and $445 million. On the bottom line, the company said that EBITDA should be between $125 million and $135 million, while free cash flow is expected to be between $65 million and $75 million. No guidance was given for other profitability metrics. But if we assume that they will increase at the same rate that EBITDA is forecasted to, then we would expect net income of $29.5 million and adjusted operating cash flow of $100.4 million.

{kind=link}

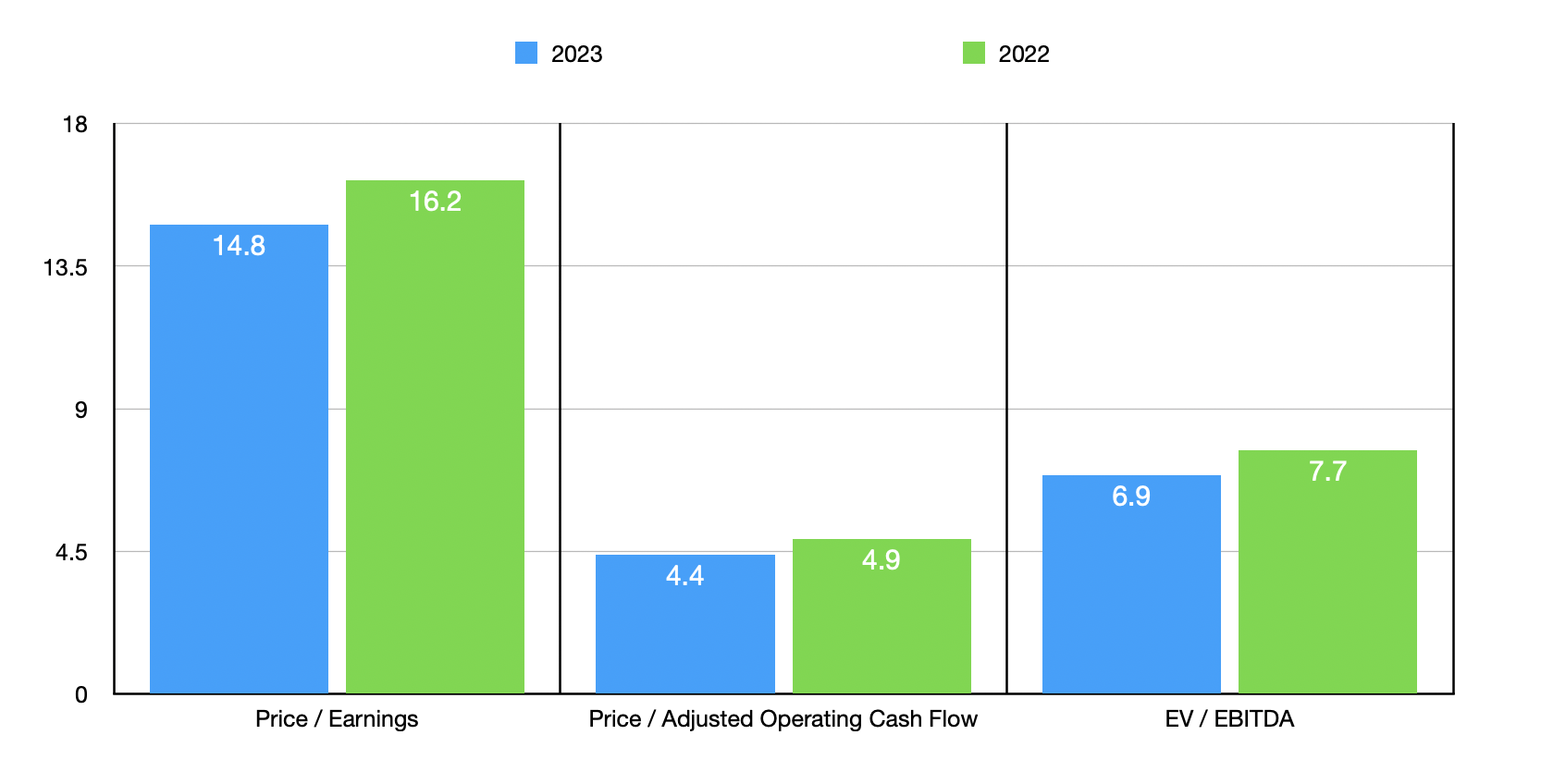

Based on these figures, Concrete Pumping Holdings is currently trading at a forward price-to-earnings multiple of 14.8. The forward price to adjusted operating cash flow multiple should be 4.4, while the forward EV to EBITDA multiple should be 6.9. By comparison, if we use data from the 2022 fiscal year, these multiples would be 16.2, 4.9, and 4.7, respectively. As part of my analysis, I also compared the firm to five similar enterprises. Using the price-to-earnings approach, I calculated that they are trading at multiples of between 8.3 and 35.1. In this case, two of the five companies are cheaper than Concrete Pumping Holdings. Using the price to operating cash flow approach, the range would be from 1.8 to 69.3. And when it comes to the EV to EBITDA approach, the range would be from 5.9 to 32.2. In both of these scenarios, only one of the five firms ends up looking cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Concrete Pumping Holdings |

| 16.2 |

| 4.9 |

| 7.7 |

| Tutor Perini Corporation ( TPC ) |

| 8.3 |

| 1.8 |

| 32.2 |

| Northwest Pipe Company ( NWPX ) |

| 15.3 |

| 11.7 |

| 8.5 |

| Great Lakes Dredge & Dock ( GLDD ) |

| 18.9 |

| 36.8 |

| 7.8 |

| Argan ( AGX ) |

| 26.4 |

| 20.6 |

| 5.9 |

| Granite Construction Incorporated ( GVA ) |

| 35.1 |

| 69.3 |

| 15.6 |

Takeaway

Although you would expect a company like Concrete Pumping Holdings to suffer in the current environment, we have seen no signs of that yet. Sales, profits, and cash flows are all rising nicely. In addition, management believes that the 2023 fiscal year will be even better than 2022 was. The firm is working on buying back stock, even though it's only a token sum. But any sort of investment back into the company should be viewed positively by most shareholders. All of these factors combined make me believe that the firm still represents an attractive opportunity and, as such, I have decided to keep it rated a ‘buy’ to reflect that.

For further details see:

Concrete Pumping Holdings: Solid Upside Still Exists