DDOG - Confluent: The Data Streaming Leader

Summary

- Confluent, Inc.'s user markets for data streaming have a long runway ahead.

- Open source Apache Kafka is ubiquitously used for data streaming.

- Confluent's wheelhouse is scalable data streaming and infrastructure management, which is a key differentiator for applications and software platforms in Kafka.

- Confluent has a competitive advantage because its founders originally built Kafka and provide several unique processes in Kafka data streaming.

- Confluent is expensive and a Hold for now, but it is definitely worth buying around $20.

Why Confluent?

Deluge of Data - Data production has reached a magnitude where it becomes imperative to process, store, analyze, and enrich to the benefit of the customer. Data converges from several sources and needs to be collected, summarized, queried and streamed in real-time. This is the Confluent, Inc. ( CFLT ) wheelhouse.

Data production and streaming are done in Apache Kafka, a language that was built by Confluent's co-founders at LinkedIn. While Kafka is open source, scalability for complex operations needs a platform like Confluent.

Scalability and low latency dissemination of data - The sheer magnitude of data production makes it imperative to constantly improve the process so that it can be done in real-time, low latency.

A data in motion ecosystem - which is reliant of stream processing or data in constant motion, i.e., moving data from one location to another. Stream processing platforms are essential to this ecosystem. Publishers of data send out data without a clear identification of the subscriber, which is commonly known as the publish-subscribe pattern, which makes faster dissemination of data essential to the process.

The trend of a data deluge from Ad Tech, IoT, and Auto to name a few industries constantly churns out data, creating a lot of demand for Confluent's platforms. This graph is from an Applied Materials ( AMAT ) investor presentation showing how Industrial IoT, Home IoT, and Automotive are going to make the bulk of data generation in the future.

A Data Deluge (Applied Materials)

Confluent's Strengths

Maintenance, product enhancement and scale

Apache Kafka is the backbone of data stream processing, it is the major hosting service used by hyperscalers and cloud service providers. Confluent is the largest scalable, product enhancement and maintaining service within Apache Kafka. Its knowledge and expertise is essential for consumers like Snowflake Inc. ( SNOW ), which uses an open core model to build upon it. Snowflake provides all that is necessary for data streaming for its clients, but it cannot maintain it nor can it enhance it at scale, economically without Confluence's support. Confluence is the improved layer.

From Michelin's use case (emphasis mine) - How Michelin Cut Kafka Costs by 35% with Confluent Cloud :

But Michelin's newly acquired architecture wasn't without growing pains. Open source Kafka proved difficult to self-manage for the company, even with the addition of three full-time employees dedicated to overseeing the clusters. The on-premise Kafka environment was in constant need of maintenance and operational management by in-house Kafka developers, making it very difficult to scale as Michelin's use cases became increasingly complex . While open source Kafka had helped Michelin jumpstart their event-driven transformation, it was time for the company's next bold move-a leap to the cloud. It was at this point that Michelin knew they needed a managed Kafka service to alleviate the burden of Kafka operations and smooth the migration of their data from on premise to a Microsoft Azure cloud environment. Enter Confluent.

Richer product features

Confluent stock also provides self-service user interfaces and other tools. It simplifies building an application on top of an event stream, bringing data streaming and synchronous querying together. It also provides a fully managed service, since data streaming is constant it requires 100% maintenance.

A symbiotic relationship with hyperscalers

Like other open core models , Confluent is building products and services around the open source Kafka project. When it partners with hyperscalers, it gives them the options to provide more add-on services for its clients. Sometimes this can be a dealbreaker and product differentiator. Also, Confluent Cloud is agnostic and can be deployed across multi-clouds - so clients can access the same Kafka installations across on-premise and cloud systems.

This is an important product differentiator, and the need for multi-cloud deployment creates a symbiotic relationship between cloud providers such as Amazon ( AMZN ) and Microsoft ( MSFT ) to team up with Confluence. Hyperscalers find it advantageous to team up with Confluence rather than compete with them, it is a lot cheaper to partner with them than to build it from the ground up the way Confluence has done.

Besides, because of the relationship, revenue streams also add up for the hyperscalers with added necessities for storage and analysis.

Also for example, if a consumer is moving from on-premise to cloud, Confluent can bring that relationship to hyperscalers.

Confluent Revenue Streams

Confluent Revenue Segments (Confluent, Seeking Alpha, Fountainhead)

ARR - Annual Recurring Revenue.

RPO - Remaining Performance Obligations.

Confluent's big focus is the Confluent Cloud Platform. Confluent Cloud focuses on cloud management while platform is self-service. Cloud Platform has grown exponentially from $14Mn in revenues in 2019 to $211 Mn last year and contributes 36% of Confluent's total, on pace to vault over the self-service Confluent Platform. Confluent needs a very strong Confluent Cloud segment to continue to grow customers with ARR (Annual Recurring Revenues) over $100,000. From the strong growth, this has been a successful strategy and even the backlog of Remaining Performance Obligations shows that growth remains strong.

Confluent and The Other Data Doctors

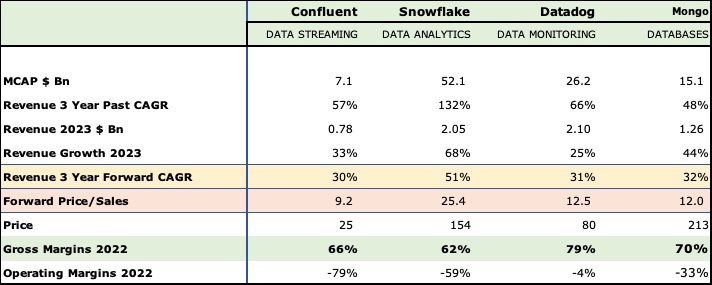

Based on Seeking Alpha consensus estimates, Confluent stacks up quite well with other data doctors; its P/S ratio is actually the lowest, not surprisingly because its 3-Year revenue growth is also the lowest at 30% compared to the others. It is close to Datadog's ( DDOG ) and MongoDB's ( MDB ) projected growth rates of 31% and 32%, respectively. Snowflake towers above the rest with a projected growth of 51%, but gets an equally massive forward sales multiple of 25!.

As we can see, the forward revenue projections are a far cry from the past 3 years' growth - in Confluent's case almost half its growth of 57%. While Snowflake is still projected to grow at a blazing 51% - it is much lower than the 132% it achieved from 2019-2022. Similarly, Datadog and MongoDB also come down from 66% to 31% and 48% to 32%, respectively. The Covid years definitely pulled a lot of growth forward, and new wins are likely to be much harder for the whole segment.

Confluent, Snowflake, Datadog and Mongo (Seeking Alpha, Confluent, Fountainhead)

{kind=link}

None is close to profitability except for Datadog, which has exceptional margins - its gross margins in 2022 are massive at 79% compared to Snowflake at 62%, and Confluent at 66%. At operating levels, it lost only 4% compared to Confluent, which lost a ton at a negative 79% and Snowflake, which too is not close to the green at a negative 59%.

Operating profits matter hugely and especially when money is not abusively cheap anymore - most tech companies need to pull up their socks if they want the markets to give them more respect.

And it is heartening to see that Confluent has heeded that call. From its Q4 2022 earnings release . (Of course, it is still non-GAAP, but one thing at a time....)

"Looking ahead, we are focused on accelerating our timeline to achieve breakeven non-GAAP operating margin by one year exiting Q4 of 2023, while delivering approximately 30% annual revenue growth in 2023."

Investment Rating

I'm rating Confluent as a Hold for the following reasons:

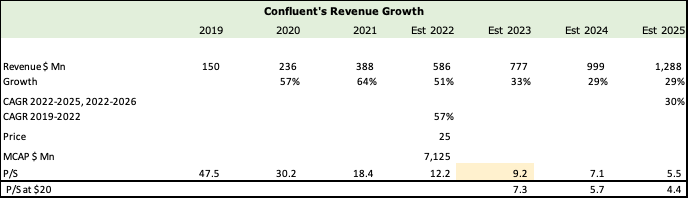

With a 30% estimated forward revenue growth, the P/S of 9.2 at a price of $25 is too expensive right now. The 30% growth is a big drop from the 57% growth in 2019-2022. With 30% growth, the P/S drops to only 5.5 in 2025. Still too rich.

{kind=link}

At a price of $20, the P/S is more palatable at 7.3 today and 4.4 in 2025.

Confluent is far from being profitable - the emphasis on cloud management, a move that takes revenue dollars away from the more profitable cloud platform also doesn't augur well for margins. Cloud Management always requires more resources upfront and unless there is a clear path to a sustainable reduction in overhead and other variable costs, this will keep margins under pressure for a while. Selling managed services also requires more investment in selling resources, as the sales cycles are longer and more difficult.

Having said that, the recent success of Confluent with the Michelin win - which is a clear endorsement of cost saving, scale, and efficiency, reinforces my belief that Confluent has a bright future in an industry, which has use cases across sectors and will continue to grow.

This is a highly specialized niche, and unless their competitors have a dedicated focus to usurp Confluent, this is a significant barrier to entry. Hyperscalers and Cloud providers actually benefit from their symbiotic relationship with Confluent. Humongous players like AWS and Azure getting into this space, which is currently less than 1/100 of their size, is highly unlikely.

Unfortunately, I feel the return on my investment is only worth it at $20, or 20% lower than the current Confluent, Inc. market price of $25. Given my projection that tech stocks will fall with higher interest rates, I'm willing to wait till Confluent, Inc. stock drops. After that, I start buying and below $17-$18, I could definitely back up the truck!

For further details see:

Confluent: The Data Streaming Leader