XLU - Consider This Before Investing In Utilities Just For The Dividends

Summary

- Utilities throw off reliable cash flows and beat the S&P500 in the 2022 bear market. However, due to rising interest rates, risks have increased and viable alternatives have emerged.

- In this article, I provide a different, yet income-oriented, perspective on utility stocks in general, and Duke Energy, The Southern Company, WEC Energy Group and Dominion Energy in particular.

- I compare their cash flows with those of de facto credit-risk-free government bonds, taking into account various dividend growth scenarios.

- Depending on the individual investment horizon, government bonds or high-quality corporate bonds can be a sensible alternative to utility stocks or broadly diversified ETFs like the Utilities Select Sector SPDR ETF XLU.

Introduction

In principle, utility stocks offer a lot of shelter from the storm during an economic downturn or in times of heightened economic uncertainty. While the sharp sell-off in March 2020 due to broad-based lockdown measures to contain the spread of SARS-CoV-2 was a rather special situation, the more "conventional" bear market of 2022 once again illustrates this point:

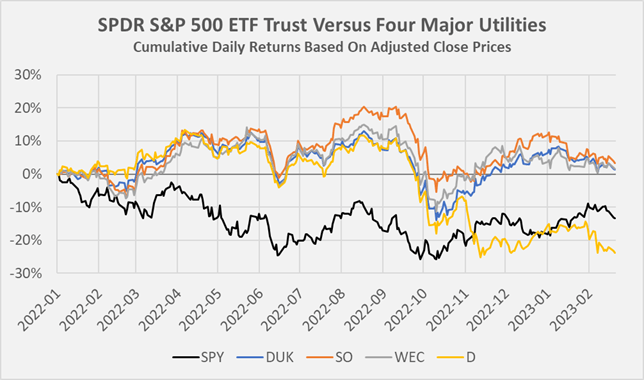

Figure 1: Cumulative daily returns of SPY, DUK, SO, WEC, and D since January 2022 (own work, based on daily adjusted close prices according to Yahoo Finance)

{kind=link}

Duke Energy ( DUK ), The Southern Company ( SO ), and WEC Energy Group ( WEC ), for example, performed very similarly and significantly outperformed the S&P 500 (e.g., SPY ) last year. Dominion Energy ( D ) is a somewhat different animal in that the stock sold off after management announced a business review following third quarter results and investors are likely still in shock from the 2020 dividend cut that was required as part of the company's transition out of non-regulated businesses.

While the selloff in the broader market was largely due to the sharp rise in interest rates and therefore perfectly understandable - higher discount rates put more pressure on growth stocks than stocks with current cash flows - it is still surprising that DUK, SO and WEC were largely flat year-over-year. After all, of course, higher rates hurt the typically highly leveraged utilities due to increasingly unfavorable refinancing transactions. Probably, utility investors are thinking one step ahead, assuming that interest rates will be lowered in the event of a recession.

My regular readers know I am an income-oriented value investor. As such, I naturally gravitate toward dividend stocks, as bonds were not an option for a number of years. While I'm not a big fan of utility stocks in general, I recognize their value as a reliable source of income - in particular against the backdrop of a zero interest rate environment - and therefore own a very small percentage of my portfolio in such stocks. However, since 2022, Treasuries, which are de facto credit risk-free, have been yielding 4% on an annual basis if held to maturity. So the question rightly arises whether the argument often put forward in favor of equities - TINA, There Is No Alternative - is actually true in the context of utility stocks, or whether the Federal Reserve is now once again presenting us with a viable alternative.

In this article, I take a look at the abovementioned utilities DUK, SO, WEC and D to see if it makes sense to buy these stocks, or a broadly diversified ETF like the Utilities Select Sector SPDR ETF ( XLU ), from an income generation perspective.

However, I won't go into detail about operational aspects of the individual companies, as I already posted an in-depth discussion of Duke Energy Corp., The Southern Company and WEC Energy Group Inc. some time ago. I published an update on DUK in May 2022, and on SO very recently , in which I discuss its 2022 results. Those unfamiliar with Dominion Energy should check out the great articles by fellow contributors Harrison Schwartz (bearish) and Ray Merola (bullish).

Does It Make Sense to Buy Treasuries - Or Other Bonds - Instead Of Utility Stocks?

I think the first question to answer is the intended investment purpose. In general, I think it's safe to assume that investors own utilities for the dividends. Not only do these dividends provide a fairly reliable income on a quarterly basis, but they also help maintain purchasing power as long as they grow at or above the investor's personal inflation rate. Remember - it's important not to compare dividend yields to the rate of inflation. That would be akin to comparing the speed of one car to the acceleration of another.

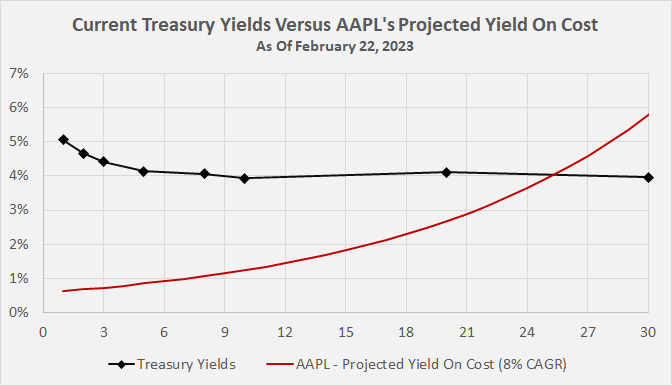

However, when government bond yields or high-quality corporate bond yields are higher than current stock dividend yields - especially in the context of stocks with modest capital appreciation at best (such as utilities) - it's important to look more closely. I suspect no one would buy Apple stock ( AAPL ) today to use the dividend checks to pay bills starting tomorrow. Its current yield is 0.62%, and assuming a fairly optimistic long-term dividend growth rate of 8% each year, it would take investors 25 years to reach the current yield on a long-term Treasury (Figure 2). Of course, the total cash flow generated over this period would be much lower as well - an Apple investor would have earned roughly $4.5k in dividends compared to almost $10k received by an investor in 30-year Treasuries. Of course, this thought experiment does not take into account capital gains.

Figure 2: Current Treasury yields versus the projected yield on cost of Apple stock (own work)

{kind=link}

While it makes little sense to apply this thought experiment to a growth stock like Apple, I think it has merit in the context of stocks held primarily for their dividend income. With this in mind, I will discuss three case studies for the utility stocks mentioned above.

Case 1: Utilities Are Maintaining Their Current Percentage Dividend Growth Rates

Mature utilities, which are in the process of retiring their coal plants and increasingly switching to nuclear and alternative forms of energy (solar and wind), typically increase their dividends by about 2% to 4% per year. WEC, somewhat surprisingly, continues to grow its dividend at a compound annual growth rate ((CAGR)) of 7% to 8%. This is partly due to lower capital expenditures (108% of three-year average operating cash flow) than DUK and SO (about 120% of three-year average operating cash flow), but also due to the historically lower leverage. Five years ago, WEC's debt to EBITDA ratio was only about 4.7 compared to 5.9 and 5.8 for DUK and SO, respectively. From this perspective, and given that WEC was still generating about 40% of its nearly 8 gigawatts nameplate capacity from coal-fired plants at the time of my original review , a slowdown in dividend growth is a reasonable expectation, at least over the long term. As noted in the introduction, Dominion Energy is special in that it had to cut its dividend by about a third as it slowly moves away from unregulated businesses. Now, after the recent sell-off, the stock is yielding 4.6%, higher than DUK and SO (both 4.1%) and significantly higher than WEC (3.4%).

Against this backdrop, management's intention not to raise the dividend in the short term is fairly easy to digest. Longer term, I think Dominion can return to modest dividend growth as it divests non-regulated businesses, but of course the current net debt of 6.4 times EBITDA and significant capital expenditures (160% of average OCF over the last three years) should also be considered. As an aside, Duke is also considering selling its non-regulated renewables business, but it is an insignificant contributor to the company's earnings.

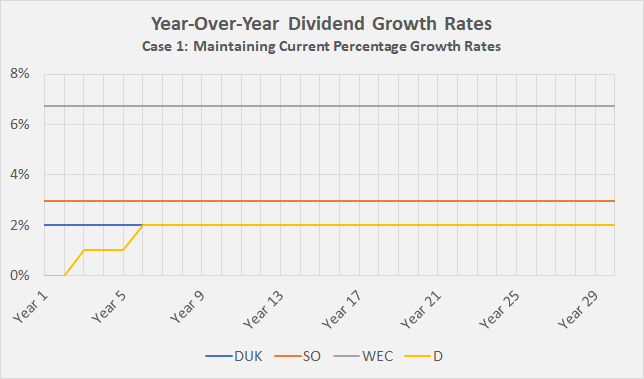

In this example, I assume that the four utilities will maintain their current dividend growth percentages (Figure 3). Given that D will likely be able to return to modest dividend growth, I have assumed normalization to a 2% dividend growth rate over the next six years.

Figure 3: Projected dividend growth rates for case 1 for DUK, SO, WEC, and D; note that I employed a return to growth to 2% in the case of D due to its ongoing transformation (own work)

{kind=link}

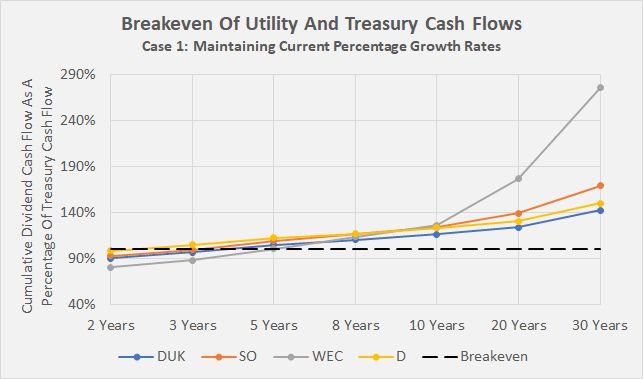

If we compare the cumulative dividend cash flows of the four utilities with those of various Treasuries, we can determine a break-even rate. I have not discounted the cash flows for this example, as this would only complicate things and not contribute to the discussion - after all, the time value of money should be identical in all cases, but of course a higher discount rate for equity-based cash flows makes sense because of the increased credit risk (and other forms of risk).

Figure 4 shows the cumulative dividend cash flows over the years as a percentage of the cumulative cash flows from each government bond. It is easy to see that from a cash flow perspective, Dominion investors are already close to breaking even after two years (the one-year Treasury currently yields 5.06%). Therefore, an investor who is satisfied with a starting yield of 4.6% and does not need immediate growth could be quite satisfied with Dominion's cash flow. Investors in DUK and SO would break even after about three years thanks to current dividend growth. Over the longer term, the one percentage point difference in dividend growth would result in investors in SO doing considerably better than investors in DUK and D, as they would have generated 140% (versus 124% and 130%) of the cash flow of the comparable Treasury after ten years, or 170% (versus 143% and 150%) after thirty years. Expecting Southern Company to maintain a 3% dividend growth rate, unlike Duke Energy, sounds overly optimistic given the significant cost overruns and delays at the Vogtle nuclear plant's units 3 and 4. However, I think that as the units come into service (expected in May or June and early next year, respectively), costs should moderate, so that a continuation of the growth rate is theoretically possible. This assumes, of course, that Southern's interest coverage does not deteriorate materially due to unfavorable refinancing transactions, which should be expected if rates remain higher for longer.

Unsurprisingly, given WEC's much stronger current dividend growth rate (which is assumed to be maintained in the current case), investors would have generated a whopping 180% of the cash flow of a 10-year Treasury or 280% of a 30-year Treasury after the respective holding period.

Figure 4: Breakeven analysis of DUK, SO, WEC and D dividend cash flows with cash flows of selected Treasuries, assuming the companies maintain their current dividend growth rates in percent, and a normalization to 2% in the case of D due to its ongoing transformation (own work)

{kind=link}

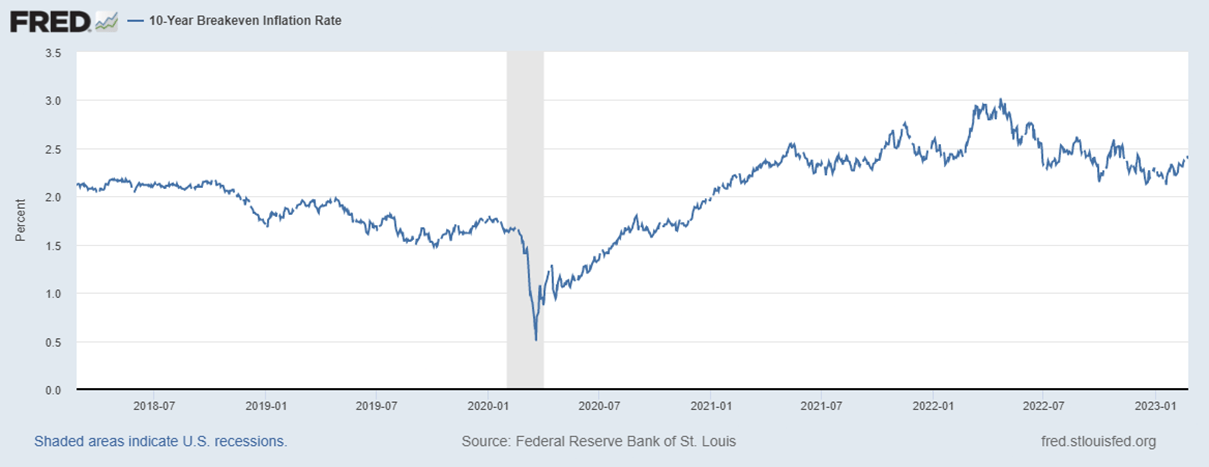

All this, of course, does not take purchasing power into account. According to the 10-year breakeven inflation rate (Figure 5), the market currently expects 2.4% annual inflation over the long term. According to the Federal Reserve Bank of St. Louis, the 30-year breakeven inflation rate is currently expected at a similar 2.2%. So, from this perspective, all of the utilities discussed should be able to grow their dividends in line with inflation, thereby preserving the purchasing power of dividend payouts. For income-oriented investors, this is an inherent advantage of dividend stocks (and inflation-linked bonds), assuming a de facto infinite investment horizon.

Figure 5: Federal Reserve Bank of St. Louis, 10-Year Breakeven Inflation Rate [T10YIE] (retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/T10YIE, February 23, 2023)

{kind=link}

Finally, Table 1 shows the yields on cost for the four utilities in this scenario after five, ten and thirty years. It is clear that income-oriented investors with a limited time horizon should not invest in utility stocks - government bonds deliver similar results with much less risk. The potential downside of equities during a recession or other negative event should not be forgotten - even though utilities are generally less volatile than other stocks. However, over the longer term, dividend growth works its magic, and investors will most likely maintain at least their purchasing power by holding on to high-quality utilities. Of course, given the somewhat optimistic growth expectation for WEC, I would not bet on a 24% yield on cost (see subsequent sections).

Table 1: Yields on cost for DUK, SO, WEC, and D dividends in case 1 (own work)

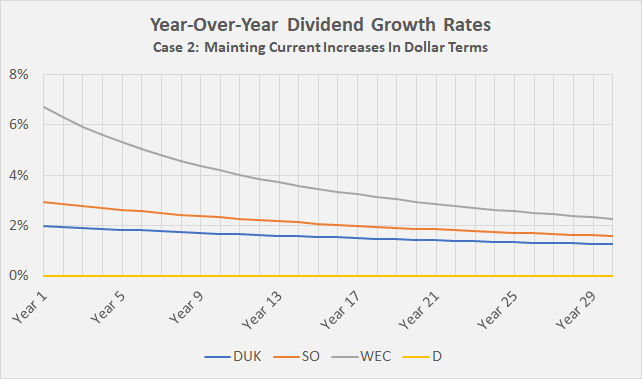

Case 2: Utilities Maintain Their Current Dividend Growth Rates In Dollar Terms

Southern Company, for example, has been increasing its dividend at an annual rate of $0.08 per share for quite some time. In this way, of course, the annual percentage growth rate decreases. While this is definitely not the norm, I must say that I have observed this practice more than once, and I think it is a good way to successfully "sell" a slowdown in dividend growth from a management perspective. Maintaining dividend growth at a fixed dollar amount definitely sounds very consistent.

Figure 6 shows what happens if the Boards of Directors of DUK, SO, and WEC decide to approve dividend growth only in constant dollar amounts from now on. This would mean that dividend growth over the long run (i.e., 100 years+) would asymptotically approach zero. Note that for this example, I did not change Dominion's dividend growth rate to give an indication of how large the impact of a stagnant dividend can be in the long run.

Figure 6: Projected dividend growth rates for case 2 for DUK, SO, WEC, and D (own work)

{kind=link}

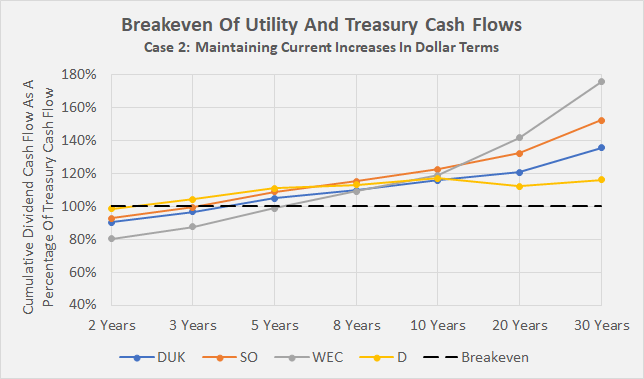

As above, Figure 7 shows the breakeven with selected Treasuries from a cash flow perspective. WEC's cash flow premium is now much less pronounced, which is understandable given its declining growth rate in percentage terms. Nevertheless, the growth rate of the dividend - starting from a fairly high current level - implies a still substantial yield on cost after ten and especially after thirty years (Table 2). Dominion's long-term cash flow premium relative to long-term Treasuries is more or less constant, and the decline relative to 20- and 30-year Treasuries is due to the "dented" and inverted yield curve (Figure 2).

Figure 7: Breakeven analysis of DUK, SO, WEC and D dividend cash flows with cash flows of selected Treasuries, assuming that the companies maintain their current dividend growth rates in dollar terms (own work)

{kind=link}

Table 2: Yields on cost for DUK, SO, WEC, and D dividends in case 2 (own work)

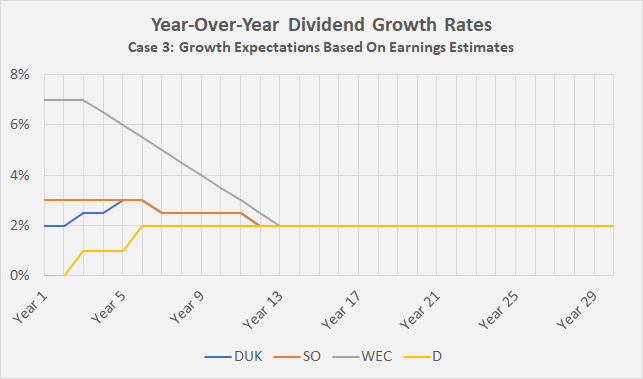

Case 3: Utilities Grow Their Dividends In Line With Earnings Expectations And In The Long Term With The Currently Expected Inflation Rate

While I do not claim that this is an accurate prediction of future reality, the dividend growth estimates in this case are based on current five-year earnings per share expectations for DUK , SO , WEC , and D . Of course, the earnings estimates for Dominion Energy in particular are quite uncertain due to the ongoing business transformation. Nonetheless, I think this approach makes sense, as utilities generally perform very closely to analysts' expectations. This can be illustrated, for example, by analyst scorecards published by FAST Graphs. For the sake of brevity, I have used data from each utility's two-year forward analyst scorecard (2011-2022) and calculated the mean percentage deviation of actual results from analyst estimates and the respective standard deviation (Table 3). In my opinion, WEC Energy Group's good management is also reflected in the very low standard deviation and systematic beating of analyst estimates. I really like it when management teams under-promise and over-deliver.

Table 3: Mean differences and standard deviations of actual earnings from analysts' estimates, based on two-year forward analyst scorecards (own work, based on data obtained from www.fastgraphs.com)

WEC's management expects average earnings growth of about 7% over the next few years, while analysts are somewhat more conservative. Given the significant investment needs over the next few years and probably decades, I think it is reasonable to expect dividend growth to decline to the levels seen at peers Southern and Duke.

At the same time, it should not be forgotten that almost all of WEC's profits are generated in Wisconsin, which is considered a very constructive jurisdiction. Obviously, WEC lacks the diversification of Southern Company and Duke, so a deterioration in Wisconsin's regulatory climate would hit WEC disproportionately hard. Of the three companies, Southern operates in the most favorable jurisdictions, Georgia and Alabama, the latter being the only jurisdiction rated "Above Average/1" by Regulatory Research Associates. Duke also operates in fairly favorable jurisdictions, such as Florida and Tennessee. However, the company also operates in somewhat more challenging - but still constructive - environments, such as North and South Carolina and Indiana. Dominion also operates in the Carolinas as well as Virginia, where the regulatory environment remains adequately constructive. Analysts expect profits to decline over the next two years and return to growth in 2025, which I have factored into my model (Figure 8).

Figure 8: Projected dividend growth rates in percent for DUK, SO, WEC, and D, based on analyst estimates and own projections (own work)

{kind=link}

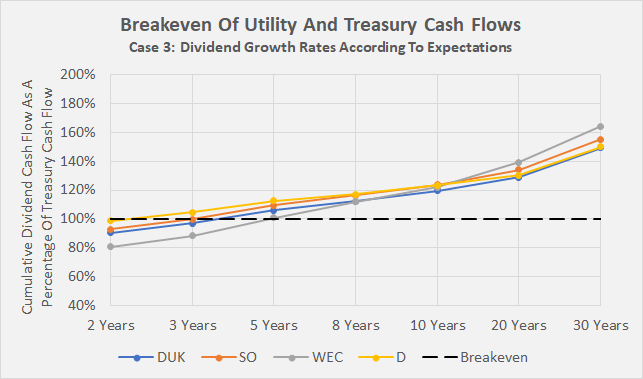

Figure 9 shows the break-even analysis and relative cash flow projections based on the above assumptions. Even assuming a decline to a 2% dividend growth rate over 10 years in the case of WEC, the stock's yield on cost is already higher than its peers after just 10 years - by more than 60 basis points compared to SO and D, and by about 40 basis points compared to DUK. That may not sound like much, but I think the difference is significant and illustrates the power of dividend growth investing, even under relatively conservative assumptions. At the same time, I don't think it makes a lot of sense to favor Dominion over Duke Energy or Southern Company when viewed through the income lens. Granted, the short-term satisfaction is more pronounced because of the higher starting dividend yield, but I think it's reasonable to expect that effect to balance out in the long run.

Figure 9: Breakeven analysis of DUK, SO, WEC and D dividend cash flows with cash flows of selected Treasuries, assuming dividend growth rates based on analyst estimates and own projections (own work) Table 4: Yields on cost for DUK, SO, WEC, and D dividends in case 3 (own work)

{kind=link}

Concluding Remarks

Leaving aside the potential downside risk arising from the ongoing substantial capital expenditures as the transition to alternative energy sources continues, there is nothing wrong with owning utility stocks as income-generating investments, even though 10-year Treasuries are currently yielding almost 4%.

However, it is of utmost importance to consider the time horizon before investing. I acknowledge that it is tempting to use utility stocks to park liquidity because of their typically low volatility and reliable earnings. However, it is important to remember that stocks are assets with a very long duration (see my article on this topic) and therefore should only be bought with a long-term horizon. At the same time, it is important to consider the refinancing risk that is relevant when investing in bonds - not only from the point of view of the contractual maturity, but also in connection with a possible issuer call option.

Even under conservative dividend growth assumptions (case 3), or if management teams choose to increase their dividends by a constant dollar amount going forward (giving the appearance of long-term consistency while percentage growth gradually declines), income investors will most likely do better with utility stocks than with Treasuries. Over only five to eight years, all four utilities will most likely generate stronger cash flows than comparable government bonds. Of course, it may also be worthwhile to consider bonds of high-quality utilities because of their higher yields compared to government bonds, due in part to the credit risk discounted in their valuation. For example, the 2052 bonds of Alabama Power (CUSIP 010392FW3, S&P rating A-) and Georgia Power (CUSIP 373334KR1, S&P rating BBB+) are currently trading at yields of 5.28% and 5.49%, respectively - a solid premium of 130 and 150 basis points over the current 30-year Treasury yield. Shorter maturity bonds such as 010392FU7 (Alabama Power, due 2030) or 373334KL4 (Georgia Power, due 2029) are currently trading at premiums of 90 and 130 basis points, respectively, over the seven-year Treasury.

However, putting myself in the shoes of an investor with predictable liquidity needs in five to eight years from now, I would forgo the small premium, avoid the equity risk, and stick with Treasuries or high-quality corporate bonds. It might also make sense to adopt the concept of a bond/equity "maturity" ladder, where an investor focuses on bonds because of short-term liquidity needs, but also invests a certain amount in utility stocks to take advantage of their ultimately better cash flows. In this context, it is important to take inflation into account - a conventional fixed coupon bond is not a hedge against inflation because its annual payout does not change. In contrast, utilities will likely continue to be able to grow their dividends at an appropriate rate, assuming the regulatory environment does not deteriorate and companies are allowed adequate returns on equity. To mitigate the devastating effects of a dividend cut, as in the case of Dominion Energy, it once again pays to diversify one's holdings by holding a portfolio of individual stocks of utilities that operate in jurisdictions with constructive regulatory climate. Buying a diversified exchange-traded fund like XLU is not a viable alternative, in my view, because its current yield of 3.1% is well below that of 10-year Treasuries and its five-year average distribution growth is only about 3.3%.

Thank you very much for taking the time to read my article. Do you agree or disagree with my conclusions? How did you like it, my style of presentation, the level of detail? Also, if there is anything you'd like me to improve or expand upon in future articles, do let me know in the comments section below.

For further details see:

Consider This Before Investing In Utilities Just For The Dividends