ACTV - Core CPI Has Likely Bottomed At 5.5% - The Fed To Hike Into The Recession

2023-04-10 13:15:39 ET

Summary

- Core CPI has likely bottomed at the 5.5% level.

- Thus, the Fed is likely to keep the monetary policy tight, despite the unfolding recession.

- As a result, the overvalued QQQ stocks are likely to re-enter the bear market.

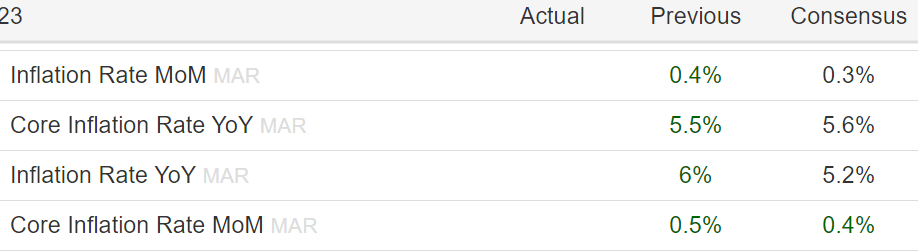

The CPI expectations for March

I have been warning that the disinflationary trend from "peak inflation" in 2022 is likely to be short lived.

Let's look at the inflation expectations for March, to be released on April 12. The consensus expectation for core CPI is 5.6%, which is higher than 5.5% in February. On the other hand, the headline CPI is expected to fall to 5.2% from 6% in February. However, the big drop in headline CPI inflation is due to the base effect, as the price of energy spiked last year due to the Russian invasion of Ukraine.

Thus, the core CPI inflation is the main driver for the Fed policy outlook, with the market implications. In fact, Fed Chair Jay Powell has been clear that the service inflation ex housing is the key metric in evaluating the "sticky inflation" pressures.

{kind=link}

Trading Economics

What's ahead for April?

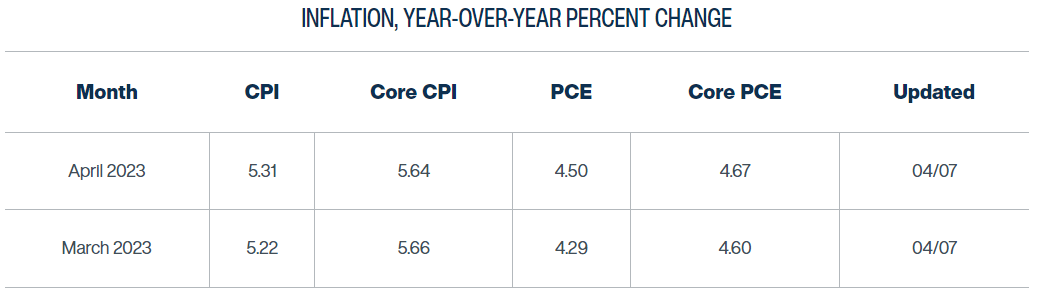

The Cleveland Fed is publishing the Inflation Nowcast on a daily basis, and the latest update is generally consistent with the market consensus expectations for March, although there is the risk that the core CPI comes at the higher than expected 5.7% reading (if you round up the 5.66% Nowcast expectation).

However, the Nowcast core CPI forecast for April is still at 5.6%, which suggests that the disinflationary trend in the core CPI has really plateaued at a very high level at around 5.5%.

{kind=link}

Cleveland Fed

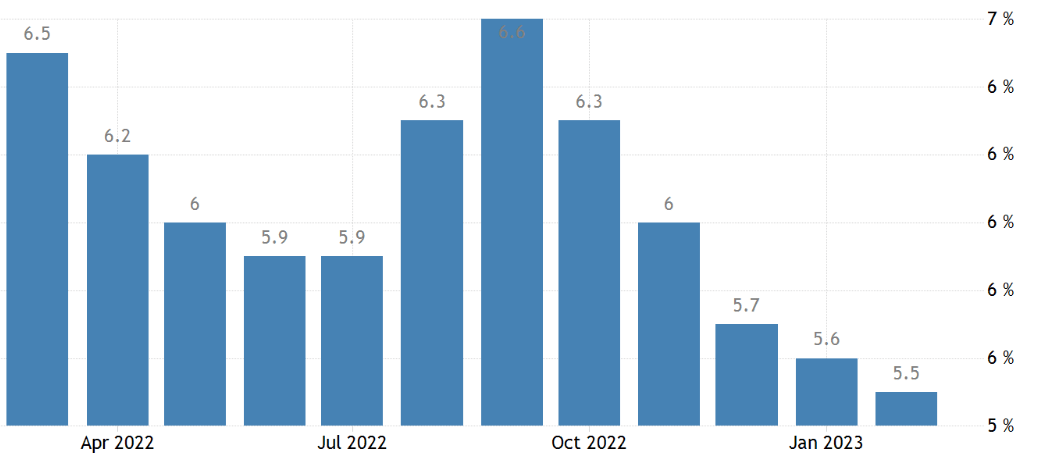

The disinflationary trend has ended

In fact, when you look the recent trend in the core CPI, the March and April core CPI readings are expected to match the January core CPI, which is a just a notch below the December 2022 reading of 5.7%. That would suggest that the core CPI inflation will be in the 5.5-5.7% range for five months - well above the 2% target.

{kind=link}

Trading Economics

As previously stated, the focus is on the core CPI, and specifically the service inflation ex housing. The goods inflation has decreased as the supply chains re-opened. So, this is not a worry anymore? Not true.

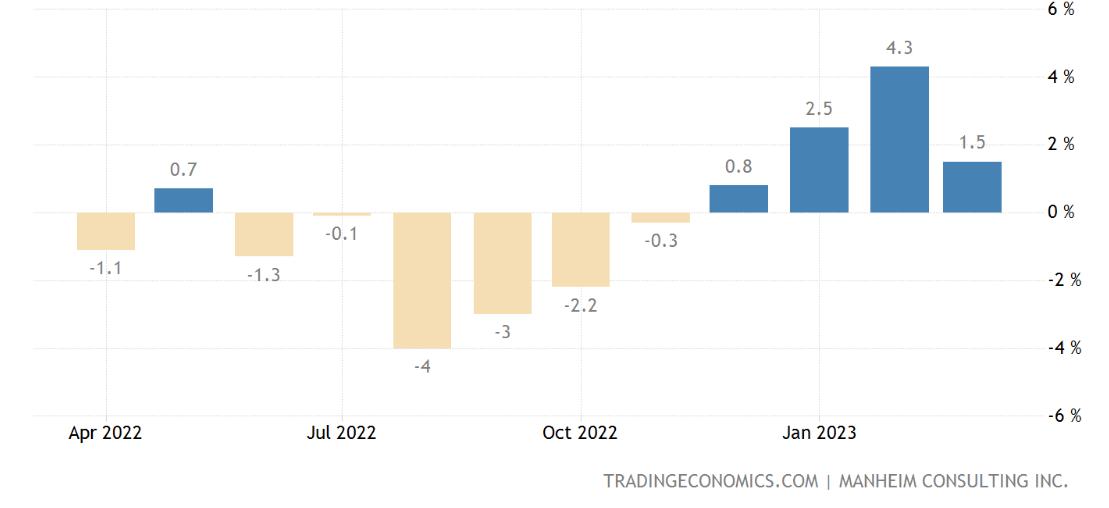

Here's the Manheim index of used car prices, month over month percentage change. The disinflationary trend in used car prices in 2022 has ended in November 2022. Since December 2022, the used price prices have been rising - that's four months of rising used car prices. This also is consistent with the thesis that the disinflationary trend has ended, possibly even for the goods.

{kind=link}

Trading Economics

The geopolitical inflationary shock brewing

The used car prices index is the key inflation indicator. During the COVID crisis many have viewed the used car prices as the COVID-related bubble, which would burst as soon as the supply chains improve.

The used prices have soared because the chip-shortage limited the new car production. However, the chip shortage is not just a transitory COVID -related issue. In fact, the chip-shortage started with the US-China trade war in 2017, and it's about to get much worse with the escalations of the US-China conflict related to Taiwan , which is the major global producer of microprocessors. Thus, the used car prices are a reflection of the geopolitically-induced chip shortage.

Even broadly, the surprise OPEC+ cut in oil production also is potentially a sign that the recent geopolitical tensions could produce an inflationary shock.

...while we could already be in a recession

The inverted 10Y-3mo yield curve spread has been sending the recessionary signal since October of 2022. The recent banking crisis likely is the trigger that pushes the US economy into the recession - by producing a much tighter lending environment and possibly the credit crunch.

In fact, many are predicting that we are already in a recession in Q2 of 2023 . However, it's difficult to envision a recession with the still historically tight labor market and the 3.5% unemployment rate.

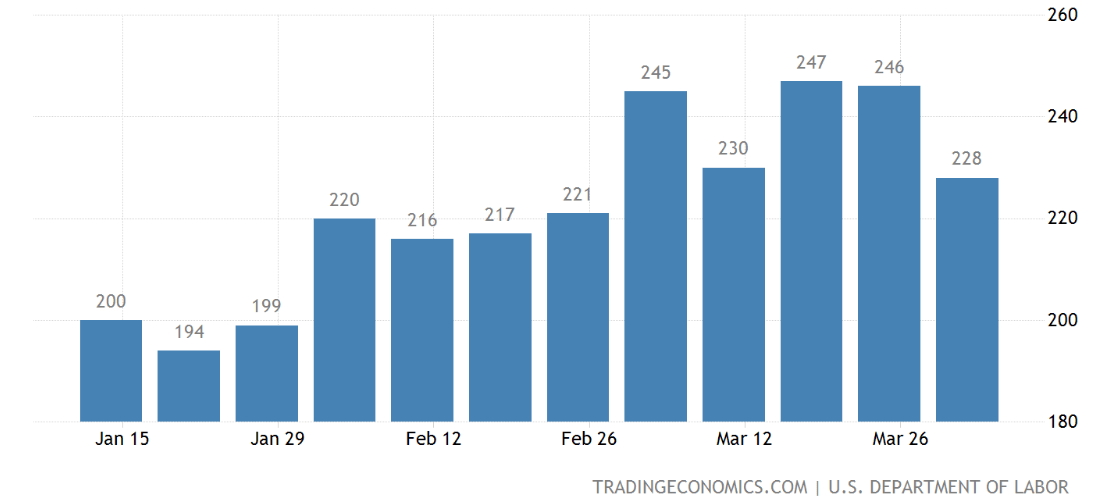

The initial claims for unemployment is the leading indicator for the labor market, and until last week we were told that the new claims were still below the 200K level, which was very low. However, last week we got the major surprise with the new claims revisions.

Initially, the new claims for the week of March 26th were reported at 198K. This number was revised to 246K last week, and the recent new claims number was reported at 228K. These revisions paint a very different picture for the labor market, as we now track the steady rise in the new claims since January 29th - this is consistent with an unfolding recession.

{kind=link}

Trading Economics

The Fed expectations

The market currently expects the Fed to hike by another 25bpt in May (with about 60% probability) and then pause. The first cut is expected by October 2023, with the terminal Federal Funds rate at 2.8% by February 2025.

Thus, the Fed is expected to hike into the likely unfolding recession and keep the monetary policy tight during the recession. This is consistent with the expectations that the core CPI has bottomed at the high level of 5.5%. Thus, the Fed is forced to keep the monetary policy tight to push the unemployment rate to at least 4.5% from the current 3.5%, with the hope that this would lower the service-based inflation and gradually reduce the core CPI to the target 2% level.

The expected monetary policy supports the unfolding Fed-induced recession thesis.

The implications for stock market

The S&P 500 ( SPY ) is up by almost 7% YTD. However, Nasdaq 100 ( QQQ ) is up by over 20% YTD. In fact, the handful of large cap tech/discretionary stocks have supported the entire stock market this year.

Nasdaq 100 is still severally overvalued, even after the 2022 35% peak-to-bottom correction, and the subsequent bounce. The PE ratio for QQQ is 26, and the forward PE ratio is 25 - this is expensive.

Thus, I still view the QQQ as the bursting bubble, temporarily interrupted with the bear market rally. The next leg down in QQQ will be triggered with the unfolding recession, as the earnings get downgraded significantly.

In fact, Apple ( AAPL ), which is the largest component of QQQ, already is seeing some effects of the consumer slowdown as IDC says "Mac shipments fell 40% year-over-year amid PC weakness." This is not a short-term weakness that can be ignored. In fact, the IMF forecasts the slowest economic growth in decades over the next 5 years.

Thus, the combination of the "sticky inflation," the tight monetary policy, and the unfolding recession, all within the framework of the geopolitical tensions, produces a very bearish outlook for the overvalued tech stocks.

For further details see:

Core CPI Has Likely Bottomed At 5.5% - The Fed To Hike Into The Recession