COST - Costco's Earnings: A Few Thoughts On The Special Dividend And The Fee Hike

2023-12-11 08:00:00 ET

Summary

- COST stock recently broke the $600 resistance and is now trading at its all-time high, raising concerns about overvaluation.

- Investors are waiting for Costco to announce its membership fee hike, which usually happens every six years, and the possibility of a special dividend.

- The strength of Costco's business model, focused on membership fees and high renewal rates, is what makes it a long-term investment opportunity.

Introduction

Earnings season may be ending, but, right around this time, we have one of the most interesting and important reports coming out: Costco's ( COST ).

The stock just recently broke the $600 resistance and is now trading at its ATH. In addition, its multiples have expanded and fostered new concerns about the overvaluation of the stock.

Finally, investors are now waiting for the company to announce its membership fee hike, which usually happens every six years and, considering the pile of cash on its balance sheet, for the special dividend as well.

While these are certainly important facts to consider, my investment case for Costco isn't grounded neither on the pace of fee hikes nor on the payment of the special dividends. Don't get me wrong: it is pleasant to receive an extra and hefty paycheck. And the membership program catches a lot of my attention as it deals with the core of Costco's business. But, what makes me confident about Costco over the long-term are not these "special treats". Rather, it is the company itself and its high-quality business model, that convinces me about holding onto Costco for the very long-term.

In this article, as we approach Costco's Q1 2024 earnings, I would like to share what I am expecting and what I will look for in the report.

Summary of previous coverage

No matter what is going on in the economy, Costco seems to be not only an all-weather company, but also one whose operations always shine as value-creative and value-accretive for all its stakeholders. In other words, Costco is one of those companies proving how a good business can thrive in many different situations.

When there were fears of a recession a year ago, we looked back at how Costco overcame the ones in the past. At that time, Costco was being downgraded by Wells Fargo, while I was actually putting the trigger.

When retailers were hit this year by shoplifting, we understood how it was an issue for Target ( TGT ), DICK'S ( DKS ) or Dollar General ( DG ) but not for Costco.

What is Costco's secret? It's simple and effective business model, standing on two pillars: being a top-line company and having its membership program .

For those who are unfamiliar with this model, it is important to know Costco is a wholesale retailer whose customers need to be members to shop at Costco's warehouses. Here, merchandise is usually stored on racks and displayed on pallets containing large quantities.

Costco conceives itself not really as a retail seller, but as a buyer on behalf of its members. These members, on turn, go to the warehouses to pick up whatever goods they need among those Costco has bargained and purchased. Costco usually marks up its merchandise 12-14%, selling at almost no profit. In fact, its profits come mainly from its membership fees. Therefore, for Costco, a decline in sales is not that concerning as for other retailers because what holds up the bottom line is the membership program. As long as its members renew their membership, Costco's bottom-line is insulated from major economic downturns. As of now, Costco's renewal rate is 92.7% in the U.S. and Canada and 90.4% worldwide, as we can read in the last 2023 Annual Report.

The impact of the membership fees on Costco's bottom line

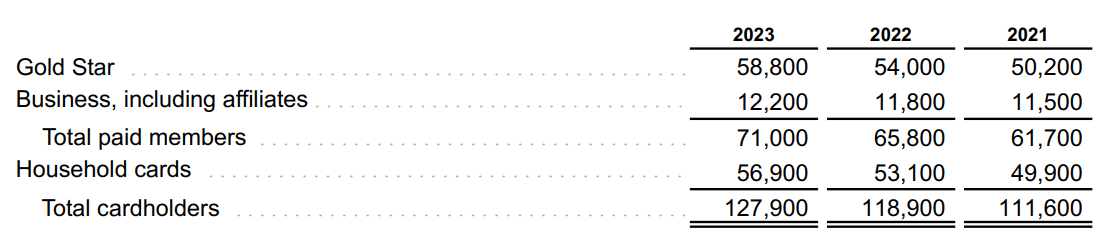

As we can see from the data shown below, Costco ended its fiscally year 2023 on September 3rd and at that time it had 71 million total paid members (member data are reported in thousands).

{kind=link}

Now, paid cardholders, with the exception of affiliates, can upgrade to an Executive membership, paying an additional $60 fee over the other $60 Gold Star members pay annually. These members earn a 2% reward on purchases up to a maximum reward of $1,000 per year. Executive members totaled 32.3 million, meaning they represented 45.4% of paid members. These are also the members who spend the most. In fact, Costco discloses in its annual report that "the sales penetration of Executive members represented approximately 72.8% of worldwide net sales in 2023".

In my last article on Costco, a reader pointed out in the comment section that it would be interesting to net out the Executive membership rewards against retail sales rather than membership income, to understand better the true strength of the membership program. He suggested to consider gross membership income by adding back to the reported membership income the reduction in sales generated by Executive rewards. In this way it is clearer that retail gross profit and SG&A are even, pointing out how Costco's pricing strategy is designed to offset SG&A expenses, because the real driver of Costco's profitability is the fees.

This means that Costco's most important metrics are not really how sales are growing and how margins are improving. It is far more simple: we need to know if memberships are holding up or not. A decline in sales is thus not really important because it doesn't really hurt Costco's bottom-line because the company runs at a 0 marginal profit as a percentage of retail sales.

Understanding this idea makes us also understand why Costco hasn't raised its membership fee during these years of high inflation. What really matters is Costco's members renewal rate. The more it holds up and even increases, the better the company's bottom line will be. Of course, it has been said more than once that the hike is not a matter of if, but of when. However, this shows Costco's strength. The company is free to decide when to increase its fees because it doesn't rely only on this increase to drive bottom-line growth.

Costco Q1 Earnings Forecast

Top-line

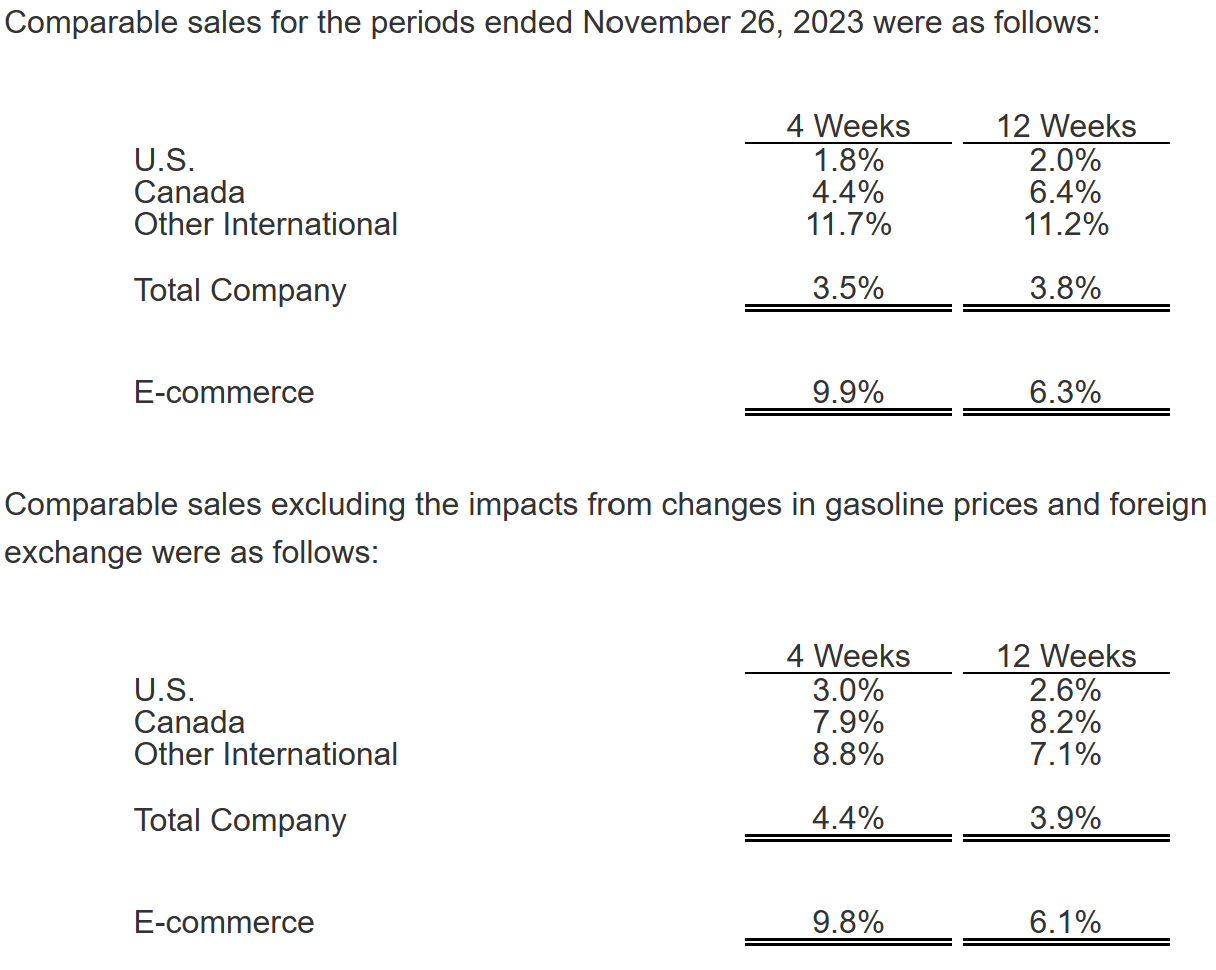

With Costco, it is rather easy to know in advance of the report what the top-line will look like. In fact, Costco releases every month its sales results. As we can see from the last release , Costco comp sales for the quarter are up 3.8% (3.9% excluding gasoline and FX).

This means we should see Costco's net sales around $55.5 billion. As far as membership fees go, we should see a revenue a little above $1 billion. This leads to a revenue estimate of $56.5 billion, which is a bit lower compared to the current consensus of $57.8 billion.

{kind=link}

Considering a net income margin of 2.4%, we can expect Costco's net income to be around $1.4 billion, which, divided by the 442 million shares outstanding, leaves us with EPS of $3.07. Again, this is a bit below the current consensus. Some share repurchases may push Q1 EPS up a bit, but we should keep this number in mind so that we can assess whether the report will be a miss or not.

My take is that Costco could probably miss earnings this time. In this situation, we might have a little sell-off given the price the stock is trading at. But, as I tried to explain above, a slow-down in sales is not a major issue for Costco, as long as memberships go up. This is when investors who understand Costco correctly can take advantage of Mr. Market and buy during dips.

What investors are pricing in

What are investors pricing in to push the stock up to a 43 PE? Well, more and more people are expecting a membership fee hike of $5 and a special dividend. A fee increase of 8.3% would have a direct impact on Costco's earnings, with a big boost to its net income for its correlation with the fee. It means we could expect FY 2024 EPS just shy of $17, which would bring the fwd PE immediately down to 36. This is still high, but more in line with Costco's historical multiples.

Moreover, since Costco initiated its dividend in May 2004 at $0.10 per share or $0.40 annually, the dividend has compounded at a CAGR of 13%.

Costco is a cash cow, and this brings the company to the point it has a cash pile it doesn't need to use to fund new warehouses. When this happens, the company pays a special dividend out to its shareholders. The first special dividend of $7.00 was paid in December 2012, then another one of $5.00 was paid in February 2014. In May 2017, the company paid another special dividend of $7.00. The last special dividend of $10.00 was paid in December 2020. Costco is at record high cash right now: $15.2 billion. Usually, it pays a special dividend every 2–3 years. It could pay a $12 special dividend using around a third of its cash. This would immediately lead to a dividend yield for this year of 2.6%, which is high considering Costco always trades at a dividend yield well below 1%.

In any case, I repeat what I have already written before. The special dividend, though enticing, is not the main reason to be long Costco. Costco is for those investors who are willing to pay a premium because they know Costco's profits are almost bullet-proof and can steadily and consistently grow, leading north the stock as well.

Conclusion

At the moment, though the stock may be actually trading at a mid-30 fwd PE, I would not suggest buying heavily into the stock. Investors who hold large stakes may want to wait for better pullbacks. Investors sitting on the sideline could take advantage of the next dip, which may come after the earnings report, in case Costco misses and doesn't announce neither a special dividend nor a fee hike. In this case, the stock's fwd multiple will further contract because, keep it well in mind, the membership hike will come. As of now, I rate Costco as a hold, but I suggest to keep a close eye on the upcoming report as it may be different from a usual report.

For further details see:

Costco's Earnings: A Few Thoughts On The Special Dividend And The Fee Hike