COUR - Coursera: Diversified Education Offerings Prove Costly

2023-03-08 14:29:17 ET

Summary

- Coursera's top line grew by 26% YoY to $523.8 million through diverse revenue channels, however, net losses deepen to $175.4 million.

- Coursera reports 300 partners and 118 million registered learners, but 30% of total revenue is generated through five partners.

- I'm cautious of the declining bottom line, increasing cost of revenue and operational expenses as the business grows, fierce competition and ongoing macroeconomic uncertainties.

Coursera, Inc. ( COUR ) is a small-cap stock with a market cap of $1.78 billion, most famous for offering free courses online by top universities, educational institutions and industry leaders. While the company is young and growing globally through diverse revenue streams, including a recurring revenue model and multi-year partnership contracts, losses have been deepening for four consecutive years. The stock price has lost 77.04% in value since its IPO, and the management has forecasted weak performance predictions for the 2023 financial year.

Stock trend since IPO (SeekingAlpha.com)

{kind=link}

COUR is partnered with leading institutions and companies, a front runner in teaching AI technologies, growing in the number of courses, users and partners and could play a critical role in helping workers upskill for the changing job market and stay relevant. However, the increase in losses as the company grows, the increase in revenue and operational costs are a cause for concern amidst ongoing macroeconomic uncertainties and fierce competition. Therefore I do not recommend buying the stock and give it a hold rating.

Overview

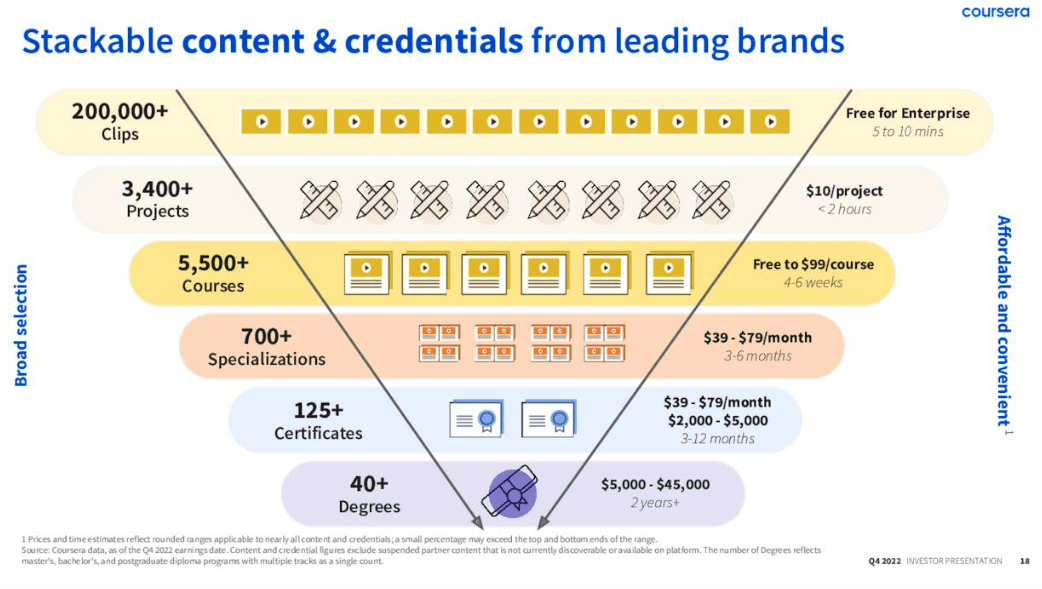

COUR is an online education company offering various courses and degrees to individuals and businesses rolled out through 300 partnerships with well-recognized universities, educational institutions and industry leaders across the globe, such as Stanford, Google ( GOOGL ) (GOOG) and Accenture ( ACN ). 30% of its revenue is from five partners. One is GOOGL, which brings in a lot of revenue , albeit at a hefty fee . COUR makes money through tuition, access fees, certification and enterprise subscription service partnerships with businesses looking to provide courses for their employees, as shown below.

Diverse content availability for consumers and businesses (Investor presentation 2023)

{kind=link}

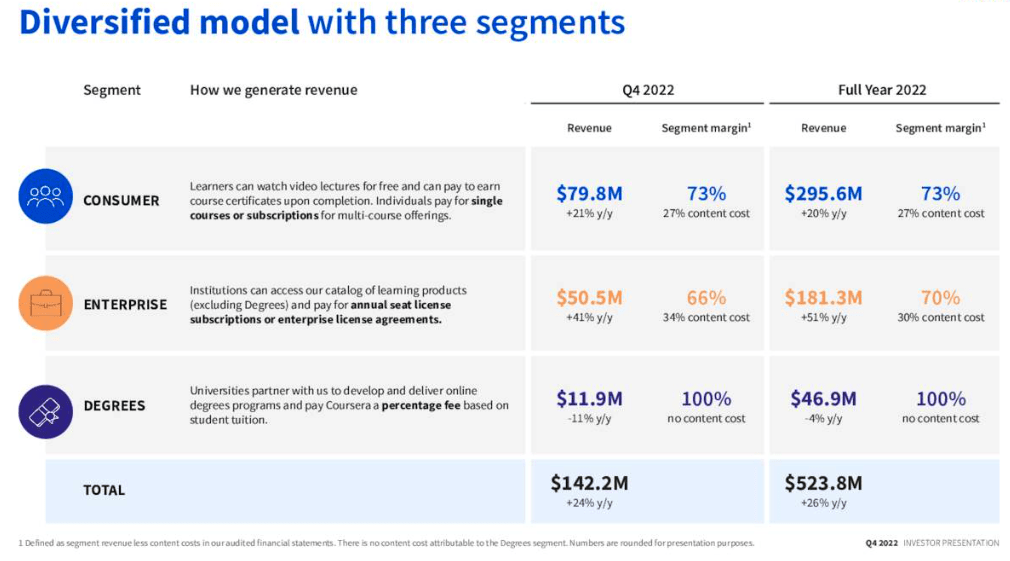

The company has three revenue streams. Its largest segment is consumer revenue, which increased in FY2022 by 20% YoY to $295.53 million, with a gross profit margin of 73%, due to ongoing demand for micro-credentials in the entry-level professional certificate section. The second segment is enterprise revenue which increased by 51% YoY to $181.28 million for the entire year, with a gross profit margin of 70%, with the total number of paying enterprise consumers increasing by 43% YoY, 1,149 in Q4 2022. Lastly, degree revenue decreased by 4% due to fewer student enrollments, accounting for $46.88 million and an attractive gross margin of 100%.

Revenue segments (Investor presentation 2023)

{kind=link}

The company is expanding its course offerings, certificates, number of partners and growing student numbers. However, its diverse business models have not been profitable due to increased expenses as the business grows. One tailwind that has been discussed is COUR's role in creating content for generative AI, for which there is a predicted high demand . Further long-term tailwinds are a digital transformation and a rise in remote work, which incentivize individuals to take on additional studies to participate in the changing supply and demand of jobs and stay relevant.

Financials and valuation

COUR is a young and growing company which only recently IPOd in March 2021. However, the stock price has been declining ever since, and while the company is increasing its revenue and users, we see an alarming increase in year-on-year losses. Total revenue for FY 2022 grew by 26% YoY to $523.8 million, with 118 million registered learners increasing its annual recurring revenue. One major red flag is the increase in net losses to a loss of $175.4 million in FY2022 from a loss of $145.2 million in FY2021.

Annual financial overview (Finance.Yahoo.com)

We can see a high cost of revenue at $192.2 million for FY2022, investing in the backend, such as fees paid to partners, servers, cloud computing and the expenses connected to content delivery. Furthermore, operational expenses significantly increased yearly to $508.8 million, with a focus on sales and marketing at $227.67 million for FY2022. This is connected to their contract agreement with GOOGL, which has recently gone through an update for FY23, which is expected to decrease these expenses but increase the COUR's revenue cost. One risk is that COUR cannot effectively reduce costs as the business expands.

Annual cost of revenue and operational expenses (sec.gov) Annual cost of revenue (SeekingAlpha.com)

COUR maintains a healthy balance sheet with total cash of $780.47 million and a small debt of $14.45 million. If we look at the liquidity ratios, we see a current ratio of 3.61 and a quick ratio of 3.44. COUR has a TTM-positive free cash flow of $28.72 million. While we are happy that the company has money to invest in its growing business, it has declined from $48.2 million in FY2021.

Levered free cash flow (SeekingAlpha.com)

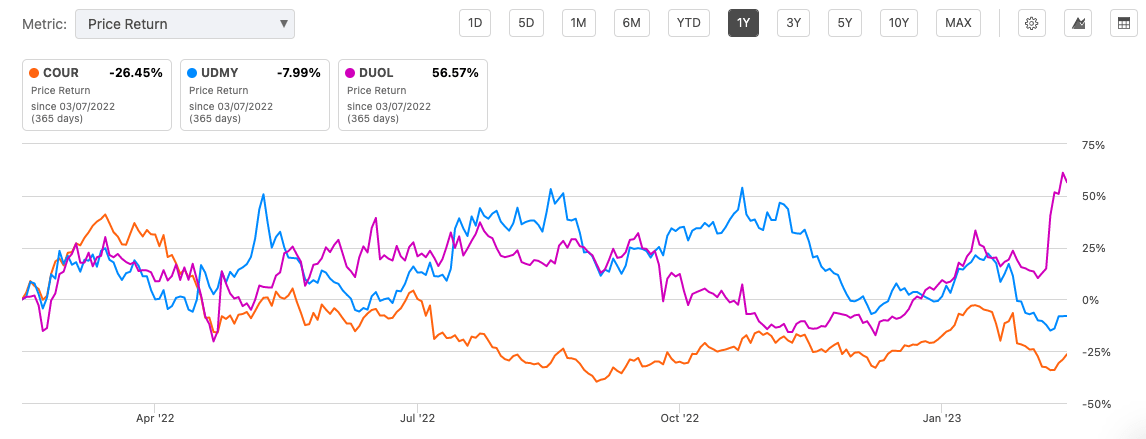

COUR has an enterprise value of $1.01 billion and a market cap of $1.78 billion. Its revenue is experiencing double-digit growth, which is expected for a young company. However, analysts have growing concerns due to the back-to-back losses. The one-year analyst target of $17.85. Recently, COUR received downgrades from Truist Securities analyst Terry Tillman , investment firm Cantor Fitzgerald and analyst Brett Knoblauch, who lowered his target rate to $16. The educational industry is fiercely competitive, with many alternatives from larger and smaller public and private companies. Comparing COUR's price return to Udemy ( UDMY ) and Duolingo ( DUOL ), we can see that it has been the least rewarding of the three stocks to hold over the last year.

Price return over one year (SeekingAlpha.com)

{kind=link}

Risks

The online education industry is highly competitive, sensitive to macro-environmental changes, closely connected to educational funding, legislation and regulations and can be disrupted by new technologies. The company appears to see the latest AI technologies as something that can benefit its platform. However, there is always the possibility that future technologies and competitors could make its offering obsolete. Furthermore, the company does not expect to see profitability in the next financial year and has forecasted revenue between $595 million and $605 million and adjusted EBITDA between negative $26 million and $34 million. Revenue is predicted to fall lower than the consensus of $143.28 million. COUR is an online business that holds a lot of sensitive user data. Although the company has not faced a breach yet, outside companies indicated weaknesses within their online platform . The company must stay on top of potential security breaches. It would harm the brand reputation and the company's future performance.

Final thoughts

While COUR remains a strong online educational brand with diverse solutions for individuals and businesses with impressive top-line growth, the consistent losses as the company grows are worrying. The management team have not painted a particularly optimistic forecast for the financial year of 2023, and the business is bound to some large partner contracts proving costly to run. While the company can play a crucial role in helping workers stay relevant or broaden their skill set to keep up with the changing job market, for now, without profit in sight, I recommend a hold rating.

For further details see:

Coursera: Diversified Education Offerings Prove Costly