COUR - Coursera: Proper Execution Of AI/ML Strategy To Unlock Higher Margins And Growth

2023-05-11 13:50:09 ET

Summary

- Despite the secular growth prospects, Coursera's growth has been declining and profitability has been unsteady.

- The use of ML and generative AI technologies is a step in the right direction to drive learners' growth and conversions at lower costs.

- With ~$780 million of cash & cash equivalent, Coursera may be tempted to make a few acquisitions to bolster growth. I expect 25% - 30% growth post FY 2023.

Coursera (COUR) is a leading online learning platform that provides access to high-quality courses, certificates, and degree programs from top universities and organizations around the world. Founded in 2012 by two Stanford computer science professors, Coursera has quickly become one of the most recognizable brands in the online higher education space, with a reputation for providing rigorous, engaging courses that are highly valued by employers and learners alike.

Driven by the secular demand for online learning and skills-based education globally, Coursera has seen exceptional growth over the years, with over 120 million registered learners and partnerships with over 300 universities and educators, including Yale, Stanford, and the University of Michigan. In March 2021, Coursera went public with an initial public offering ((IPO)), raising $519 million at a $4.3 billion valuation.

As much as it is an attractive growth prospect, Coursera is still a company that needs to demonstrate the sustainability of its business model through more disciplined execution. YTD, Coursera has been trading sideways. It is now trading at +$11 per share with a P/S of ~3x. This makes it an attractive long-term entry point for investors who believe in the company's growth potential and are willing to tolerate short-term volatility.

Overall, I am assigning an overweight rating for Coursera in this first coverage. Aside from the attractive buying opportunity from the technical perspective at present, I consider the following catalysts to benefit the stock:

- The ongoing application of Machine Learning/ML and generative AI technologies to automate course language translation and content production to drive higher user growth and conversions at lower costs as well as faster time-to-market/TTM.

- Strong balance sheet creates an opportunity to explore acquisitions to bolster growth and increase market share.

In this coverage, I will discuss Coursera's fundamentals, including its products, business models, and competition. I will further analyze the catalysts and risks around the stock at present, to understand how they impact the fundamentals of the stock going forward. In the end, I will consolidate all this information into a target price projection for Coursera.

Product And Business Models

Coursera offers a range of online learning products, including courses, certificates, and degree programs, as well as enterprise solutions for businesses and government organizations.

{kind=link}

Coursera breaks down its business into 3 key segments and has different monetization model for each:

- Consumer: As of the end of FY 2022 , Coursera offers over 5.5k courses in a variety of subjects, ranging from business and technology to arts and humanities. These courses are taught by instructors from top universities and organizations. Coursera's business model here is primarily based on a freemium model, where learners can access free courses, but must pay a fee for access to premium content, such as certificates and degree programs.

- Enterprise solutions: Coursera offers enterprise solutions for businesses and government organizations, including customized online learning programs and tools for employee development. These solutions can be tailored to meet the specific needs of each organization and can help improve employee productivity and retention. Coursera makes money by charging subscription fees or offering enterprise license agreements.

- Degrees: Coursera offers online degree programs in partnership with leading universities around the world. These programs include bachelor's and master's degrees in subjects such as computer science, business, and data science. The degrees are fully accredited and offer a flexible, affordable alternative to traditional on-campus programs. In this business, universities pay Coursera a percentage of fees based on student tuition.

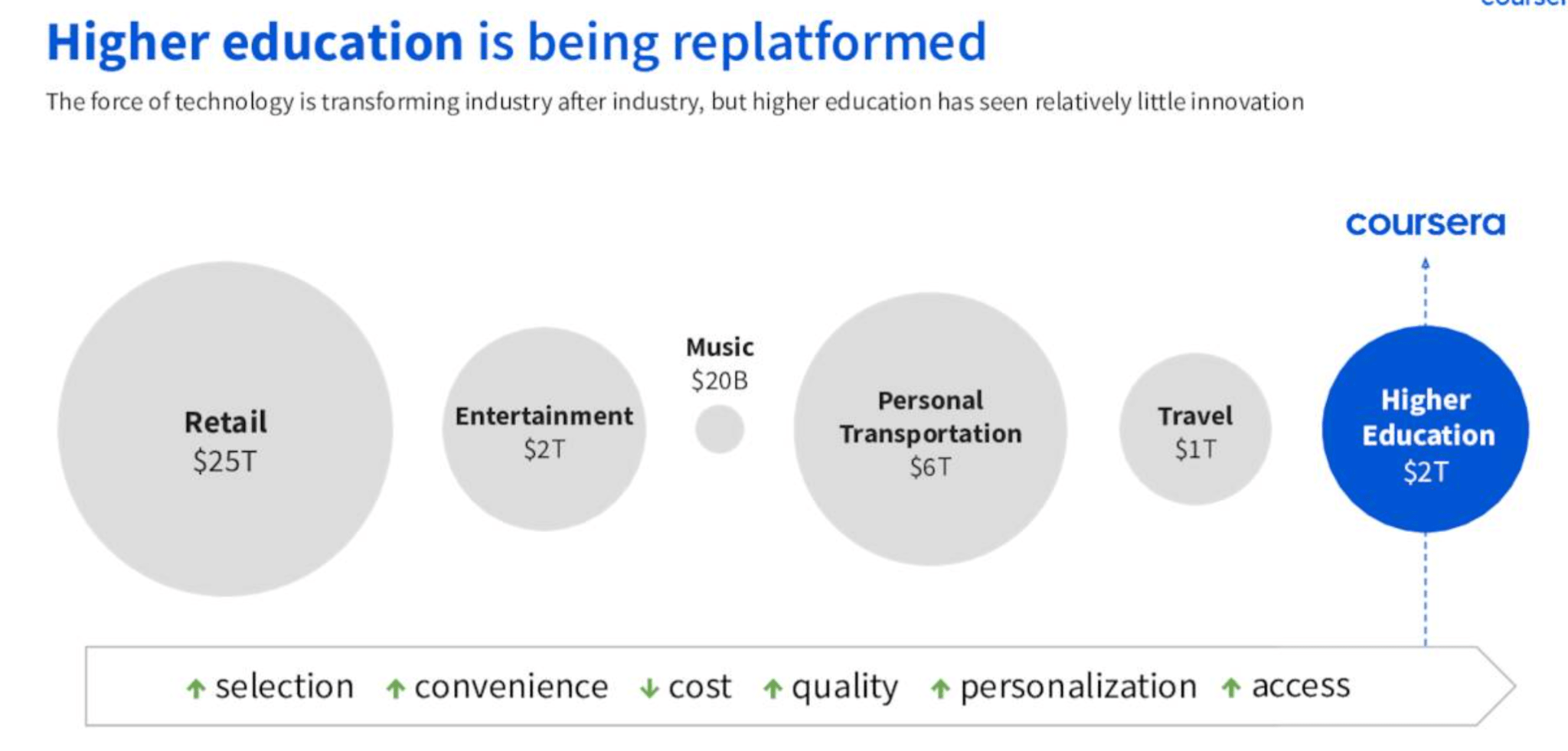

Market And Competition

In its Q1 presentation, Coursera estimates the higher education TAM size to be ~$2 trillion. From the surface, it seems like a massive market. The online share of the market, however, would probably be a lot smaller, though rapidly expanding. Based on a report by HolonIQ , the digital spend of the global education industry in general is expected to be 5.1% of the TAM as of 2023.

{kind=link}

If we apply that number to Coursera's estimated TAM, it would yield $100 billion. While it is merely a rough estimation, the actual TAM size for online higher education today would probably be somewhere at the lower-end range of $100 billion - $2 trillion, which means that it is still a sufficiently large market.

In addition, online higher education is also a fragmented market, and Coursera consistently faces competition in various forms across its business segments:

- In the Consumer/Degree segment, there are online platforms such as 2U (TWOU)/edX, which offer similar courses and degrees directly to consumers, as well as Udemy (UDMY) and LinkedIn/Lynda (MSFT).

- In the Degree segment, Coursera also identifies traditional universities as competitors, considering that they develop competing in-house online degree programs.

- In the Enterprise Segment, competitions typically come from corporate training companies such as Skillsoft (SKIL), Pluralsight, and Udacity. These companies offer training programs to corporations and their employees for the purpose of reskilling and upskilling.

- In the Consumer segment, providers of free educational resources such as Khan Academy and YouTube (GOOGL) can also be considered competitors.

The market is expected to see secular growth in the next few years. Particularly, rising demand for overall online education, reskilling/upskilling due to automation, a skill gap in emerging job opportunities such as big data, AI/ML, and data analysis, and limited access to quality higher education globally are driving the growth.

With the rapid pace of technological advancements, automation is rapidly replacing human labor in many industries, leading to a shift in the job market. To keep up with these changes, individuals are seeking opportunities to reskill and upskill themselves to remain competitive in the job market. Online higher education provides an affordable, flexible, and convenient option for these learners.

Additionally, emerging job opportunities in fields such as big data, AI/ML, and data analysis require a new set of skills that are not currently being taught in traditional educational settings. Online higher education can bridge this skills gap by offering specialized courses and programs that provide learners with the necessary skills to excel in these fields.

Moreover, access to quality higher education is limited in many parts of the world, particularly in developing countries. Online higher education offers a solution to this problem by providing learners with access to courses and programs from top universities and institutions around the world, regardless of their location.

Q1 2023 And Financial Highlights

Here is a recap of Coursera's Q1 results :

-

Q1 Revenue of $147.64 million, a 22.6% YoY growth, beating estimate by $8.86 million.

-

Q1 Adjusted EBITDA was -$7.5 million, compared to -$10.5 million a year ago.

-

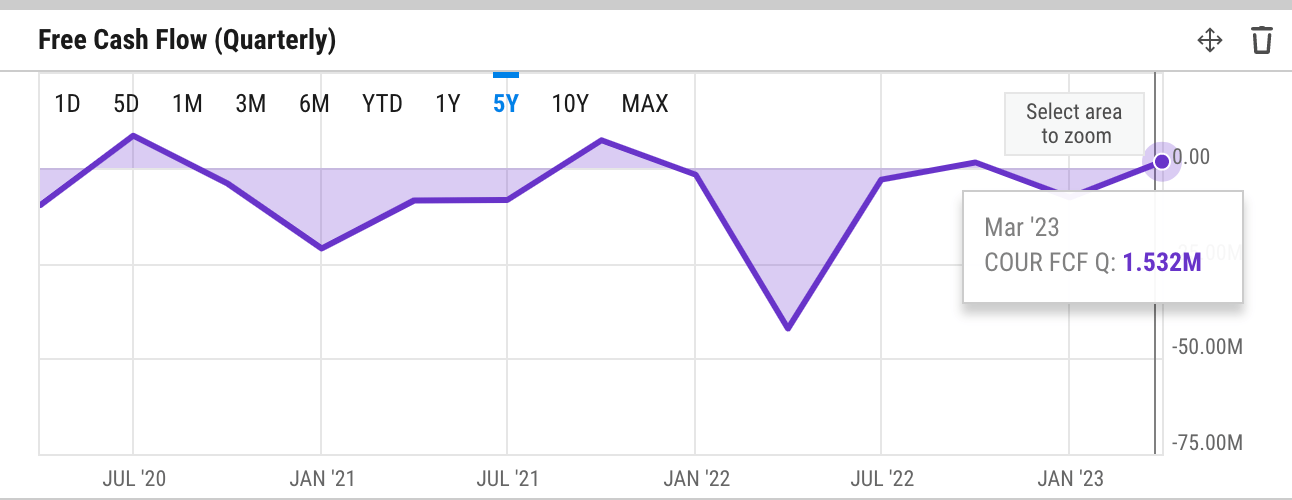

Q1 cash from operations/OCF was $4.7 million, compared to -$38.3 million a year ago. Free cash flow/FCF was $1.5 million, compared to -$42.2 million a year ago.

-

Q2 Revenue in the range of $143 million to $147 million

-

Q2 Adjusted EBITDA in the range of $(13) million to $(16) million

-

FY 2023 Revenue in the range of $600 million to $610 million, a 16% YoY growth at the midpoint range.

-

FY 2023 Adjusted EBITDA in the range of $(26) million to $(34) million.

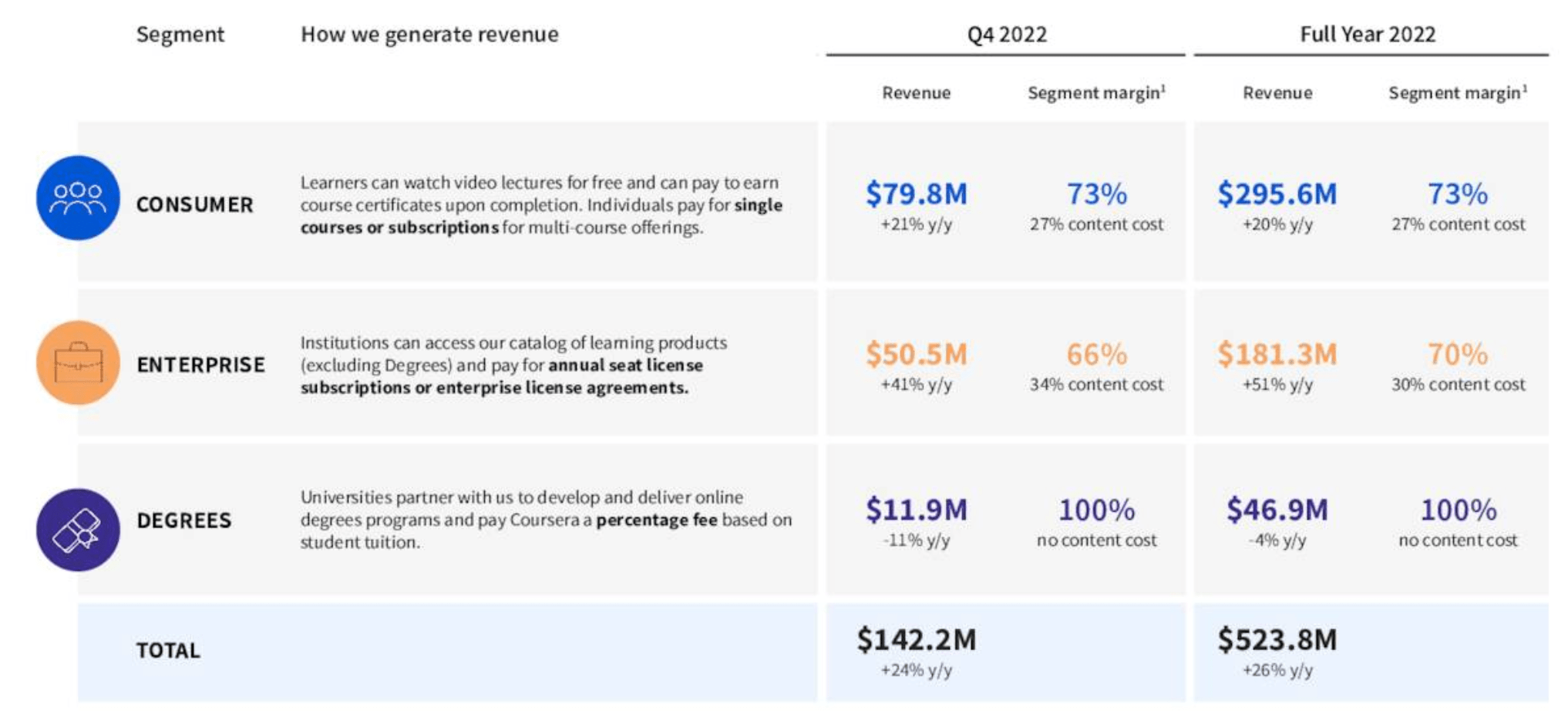

On the revenue side, Coursera saw a relatively decent performance across its business lines. With $82 million in revenue, Consumer remains the largest business segment. The segment saw a 20% growth, driven by the adoption of professional certificate programs. During the quarter, Coursera also recorded 5.5 million new registered learners.

Enterprise segment's revenue reached $52.2 million, representing a YoY growth of 34% collectively across the business/government/campus verticals. The number of Paid Enterprise Customers increased to 1,253, up 37% YoY, with a Net Retention Rate/NRR of 104%. I think that Coursera did relatively well in this segment despite the suggestion by the management that the spending outlook would tighten due to the ongoing macroeconomic downturn.

Meanwhile, Coursera's Degrees segment revenue was $13.4 million, up 1% YoY, with the total number of degree students growing by 10% YoY to 18,095. It remains the smallest business, though considering that Coursera does not produce the content for this business, it has a gross margin of 100%.

{kind=link}

An important thing to highlight here was the contraction of the overall Q1 gross margin to 52% from 64% a year ago due to the extension of a contract with the company's largest industry partner with a revenue-sharing scheme. This contraction was also offset by lower operating expense.

{kind=link}

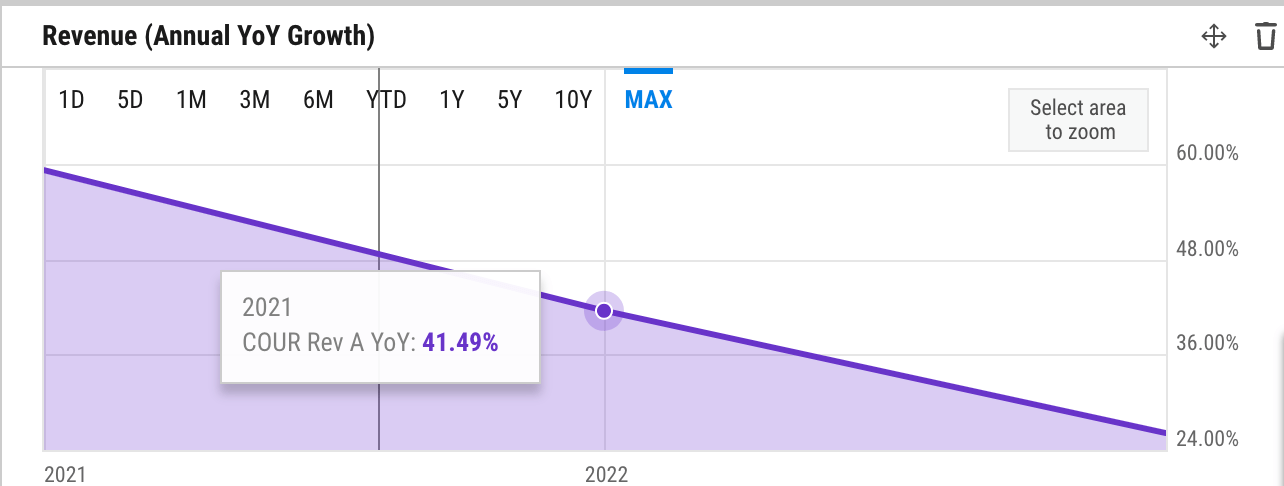

Trend-wise, Coursera's growth has declined from +40% to +50% level in previous years to 20% level today. The management will also expect a lower growth outlook (16% YoY) for FY 2023 due to the ongoing macro downturn, which mostly affects its Enterprise segment.

{kind=link}

Meanwhile, profitability and cash flow appear to be the areas where Coursera needs to improve going forward. FCF generation sees fluctuation and operating margin and EBITDA remain negative, though they typically are quite steady within the -24% to -36% range - it appears that Coursera has been managing these losses and had them under control.

Catalyst

Content production costs remain one of the most expensive cost items for any online education platform. Content production process in a platform like Coursera generally follows several steps, including course planning, structuring, design and development, recording, editing, and then launch and integration into the LMS/Learning Management System, so it can be accessed by learners. Along the process, the content team works closely with instructors, curriculum designers, and subject matter experts.

Excluding the Degree business, which recognizes no cost of revenue due to its business model, Coursera's cost of revenue is primarily made up of content production activities. On average, Coursera spends about ~30% of its revenue on these activities, such as paying fees to educator partners, content translation and captioning, hosting and bandwidth for running and storing content assets, facilities, and paid learners and educator partner support.

I can imagine how appropriate applications of ML and generative AI in supporting or automating these activities would bring down costs, and it is encouraging to see Coursera has taken steps in that direction . The company has hinted at various ways on how it intends to use ML and AI, though I am interested to highlight two of the following key areas where costs can be pressured to drive higher gross margins:

-

Content translation and captioning: as the company mentioned during Q1 earnings call, the company continues to develop an automated system that takes advantage of the recent advancement in ML technology to take over these operationally intensive activities at a much lower cost than the conventional human translation. While quality may be a point of concern, I expect that the system will improve over time.

-

Learners and educator partner support: The company's plan to also use AI technology to auto-generate course content, structure, and reading materials based on the input of educator partners will also reduce course production TTM. As the process evolves over time, course production will then happen at a better scale and economics.

Moreover, I believe that the use of ML/AI will not only bring down costs but also drive revenue growth, especially from the international markets. For instance, the ML-based translation and captioning technology will increase higher learner acquisition growth and conversion rates globally through localization.

To accelerate growth, I also consider the potential of Coursera leveraging its strong balance sheet to make acquisitions. As of Q1, Coursera has no debt and ~$780 million of cash and cash equivalent.

While I expect that growth will reaccelerate post-FY 2023, the key question here would be whether Coursera can at least bring that up to a sustainable +20% level organically. At an expected FY 2023 revenue of +$600 million, the size appears to be catching up with Coursera, and soon, it will most likely be in a market for M&As. There are definitely opportunities here - as per our highlight, online higher education remains a fragmented market, and consolidation will drive both revenue and market share growth.

The strategy can also be effective in the international market, which is one of the growth levers of Coursera. Overseas players in the similar online higher education space can potentially be a strategic takeover target that can help Coursera expand its learner base, content library, and Enterprise clients.

Valuation/Pricing

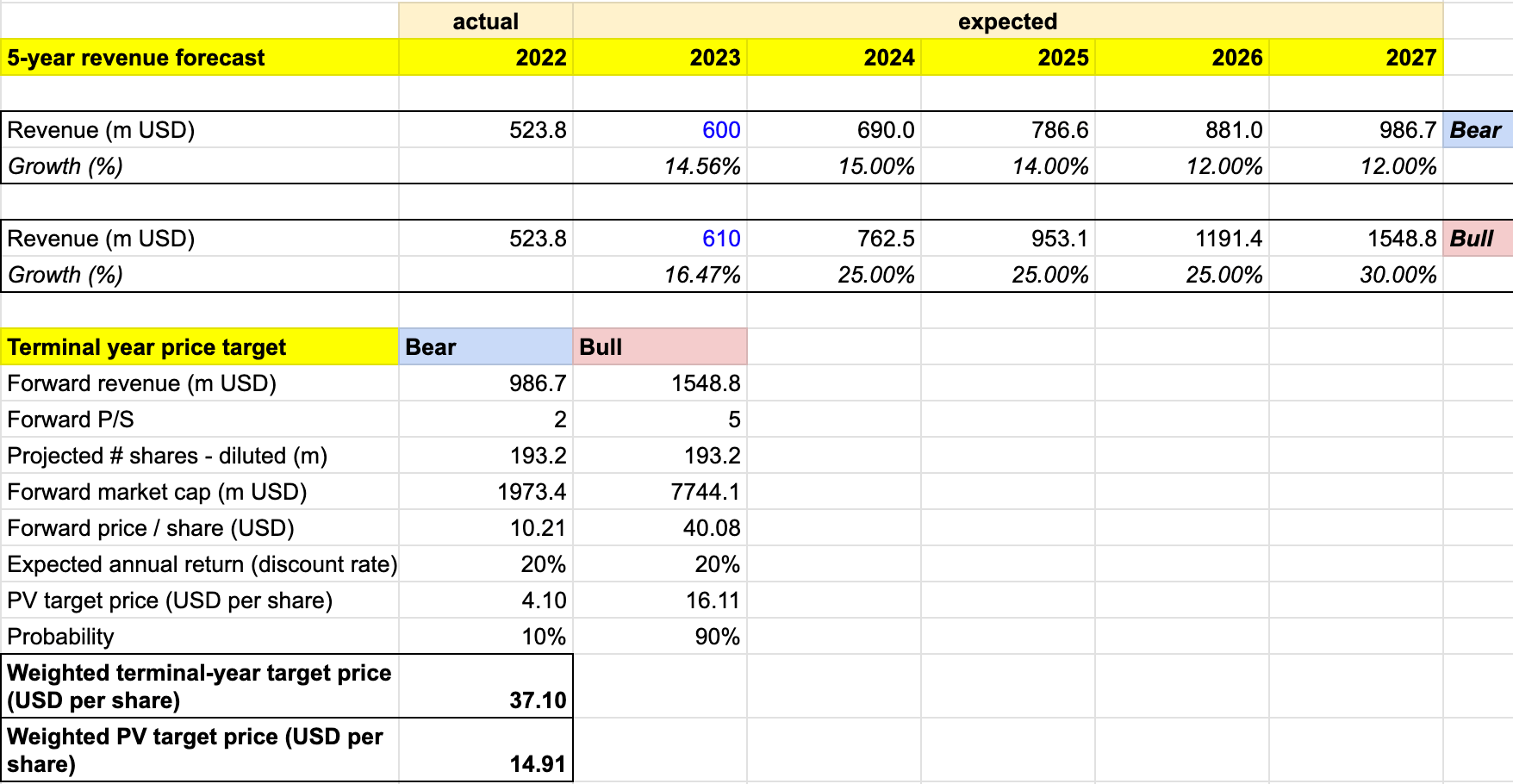

In estimating the price target for Coursera, I consider the following probability-weighted bull vs bear scenario-based 5-year revenue forecast:

-

Bull scenario (90% probability) - macro situation to improve in the FY 2024, and Coursera's revenue growth to reaccelerate to 20% in that year, driven by the uptick in upskilling/reskilling demand as businesses start to rehire talents at the back half of the year in both Consumer and Enterprise segments. Coursera will then experience a steady +25% growth until FY 2026 and then 30% in FY 2027, as the company expands its market share via acquisitions. I also expect that the deeper use of AI/ML for translation and localization starting in FY 2025 onwards will improve cash flow and bottom line. Overall gross margin to expand to ~80%, with steady single-digit FCF/OCF margin and breakeven at the operating margin level.

-

Bear scenario (10% probability) - economic downturn to sustain into FY 2024. Coursera to see 16% revenue growth in FY 2024, the same outlook as in FY 2023. The company continues to see disruption from the specialized provider focusing on high-demand skills. While acquisition of a player in that space may be ideal, Coursera's lack of experience in deal-making results in the company deciding on making an unpopular acquisition deal that further pressures bottom-line and balance sheet. Growth to see steady decline and reach 12% in FY 2027. AI/ML use also produces minimal improvements due to weak execution. Gross margin at +70%, with pretty much unimproved OCF/FCF and profitability outlook from today.

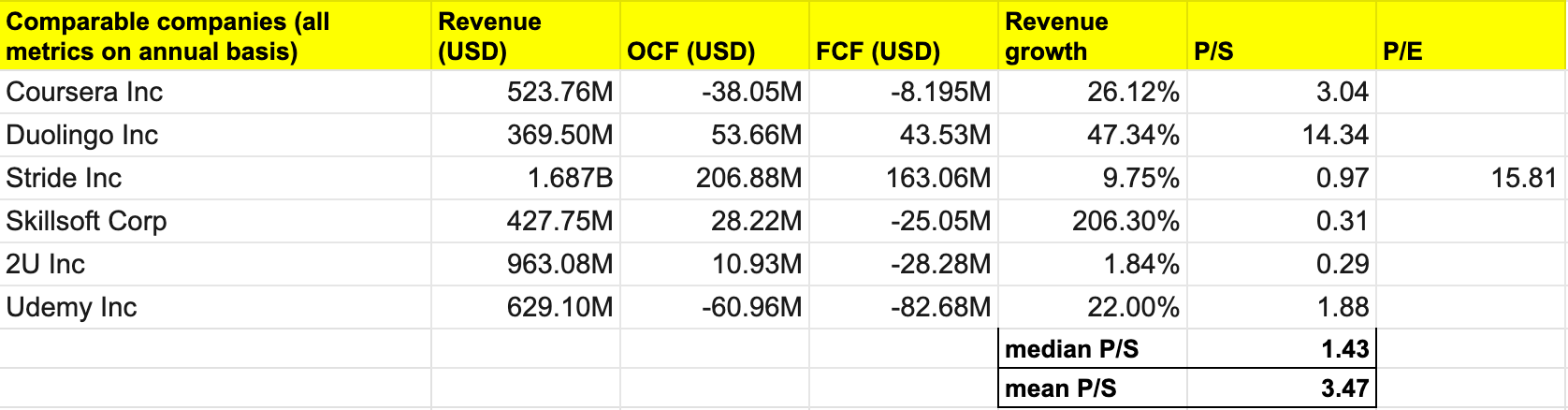

author's own analysis - COUR comparables

{kind=link}

Among the stocks in the comparable universe, Coursera, Udemy, and Duolingo (DUOL) stand out as the companies with the highest P/S multiples. A possible explanation would be that these companies' primary revenue streams are driven by a more scalable, self-service consumer-based business model that often warrants a premium. In the online higher education segment, I would also consider Coursera and Udemy to be head-to-head competitors and co-leaders with prime reputations in the space.

Given my expectation of improved cash flow and profitability outlook, as well as accelerating growth, I would project Coursera's FY 2027 P/S to expand closer to the midpoint range of 2x - 14x, positioning the stock somewhere between Udemy (2x P/S) and Duolingo (14x P/S) in terms of valuation. As such, I believe that a P/S of 5x would be appropriate for the bull scenario, as would a P/S of 2x for the bear scenario. Furthermore, the forward share count also accounts for the 15% - 20% dilution until FY 2027 as well as potential share repurchases. Coursera announced recently that the board has approved a $95 million share repurchase program.

author's own analysis - COUR target price

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2027 weighted target price of +$37 per share in FY 2027. Discounting that target price with a 20% discount rate, I arrived at a Present Value/PV weighted target price of ~$15 per share. The 20% discount rate represents the expected annual return, which is a fair expectation for a growth stock like Coursera.

The $15 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return if COUR shares reach the FY 2027 target price of +$37. As Coursera currently trades at ~$11 per share, the model indicates that the stock is undervalued, creating a buying opportunity today.

Risk

As an online platform company trying to disrupt the higher education market, I would expect Coursera to see challenges. However, I believe that many of the risks can be mitigated by prudent management and monitoring of the competition dynamics and course quality - two areas from which many other risk factors are derived.

Coursera faces intense competition in the online higher education industry. There are numerous other online learning platforms, both established ones and new entrants, that offer similar courses, degrees, and certifications. Some competitors also seem to be better positioned in certain course subjects than generic platforms like Coursera.

Coding schools like Codecademy, which is owned by Skillsoft, for instance, often have a more specialized LMS that integrate with features such as code editor, as well as competitive curriculum that attract learners looking to learn the fastest-growing skills such as data science, AI, and software development. Considering that these subjects will see high demand in years ahead, I feel that Coursera will need to start emphasizing how it can best capture the opportunity and neutralize competition. I think that investors will need to monitor Coursera's progress in this key area in the next few quarters.

In the end, platforms like Coursera will need to carefully manage the quality of its course content, since it is the key element that affects the effectiveness and reputation of Coursera across every other aspect of its business. Nonetheless, managing course quality in a scalable way is challenging and operationally intensive. It remains a difficult problem to solve for players in this space. While the use of AI/ML may help alleviate the problem, overusing those technologies may potentially compromise quality.

Investors should also be aware that while the target price model may indicate undervaluation for the stock, it's important to consider the valuation dynamics of the online education space. The finding suggests that companies in the online education industry do not seem to command premium valuations compared to other sectors. Though I am led to believe that Coursera and Duolingo may be an exception, the model's assumption of expanding the P/S multiple also relies on Coursera consistently outperforming and delivering strong results to justify that premium.

Conclusion

Coursera's been trading sideways YTD, with share price currently hovering around ~$11 per share with relatively weak profitability and cash flow generation outlook. The company also guides declining FY 2023 revenue growth as the unpredictable economic outlook has created conservatism. However, I maintain a belief that Coursera is well-positioned to improve the overall business outlook due to two key catalysts, which include its currently strong balance sheet.

At this point, I am initiating coverage on Coursera with an overweight rating. The current price level presents a buying opportunity, trading at a +25% discount to the target price based on my model. However, investors should carefully evaluate the risks and closely monitor the company's progress in order to make informed investment decisions. The company operates in a fragmented market, and it is important for investors to closely monitor the competitive landscape, particularly the threat posed by other online education providers.

For further details see:

Coursera: Proper Execution Of AI/ML Strategy To Unlock Higher Margins And Growth