COUR - Coursera's Valuation Gets A Passing Grade But Just Barely

2023-03-08 03:23:39 ET

Summary

- We were not impressed with Coursera's Q4 and FY2022 results, nor the guidance it provided for 2023.

- Growth continues decelerating, and the company has yet to show meaningful operating leverage.

- We believe the current EV/Revenues multiple of ~2x is appropriate given the risks and potential rewards.

Coursera ( COUR ) has been a train wreck of an investment since it went public, losing approximately two thirds of its value from the IPO price of $33 per share, and more than three quarters of its value from its all-time high. While some of the decline can be attributed to decelerating growth, we would argue that a big reason for the massive decline is simply that the valuation was excessive to begin with.

When we began coverage of Coursera shares had already fallen significantly, and we still found the valuation to be quite stretched. The main reason we rated shares as a "Sell" was that the company was not showing much in the form of operating leverage, and that the valuation was still quite high with an EV/Revenues multiple of ~5.5x. We also said that unless the company did a better job at controlling costs we would rather stay on the sidelines. We thought a 2x multiple was more appropriate, which at the time meant a share price of ~$10. With shares trading around $11 per share, we believe it is a good time to take another look at the company.

Seeking Alpha

Q4 and FY2022 Results

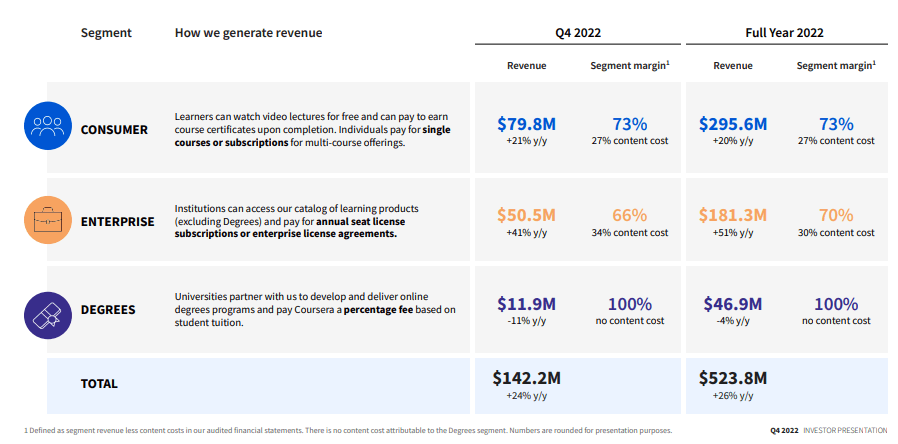

In Q4 Coursera generated total revenue of $142.2 million , which was an increase of 24% y/y, as a result of growth in its Consumer and Enterprise segments. Gross profit was $88.9 million, up 24% y/y, which represents a 63% gross margin, basically flat y/y. Net loss was $6.5 million, or 4.6% of revenue, and adjusted EBITDA was a loss of $5.8 million, roughly 4.1% of revenue. For the full-year revenue was $523.8 million and the adjusted EBITDA loss as a percentage of revenue was 7.1%. The slide below summarizes the Q4 and FY2022 results. A couple of things worth noting are that it was disappointing to see revenue in the Degrees segment down ~11% y/y in Q4, as well as margin deterioration in the Enterprise segment.

Coursera Investor Presentation

{kind=link}

Financials

We are still not seeing significant operating leverage with Coursera as revenue increases. This remains a top concern, as the operating margin is deeply in the negative and not showing meaningful improvement.

It does not help that the company has ramped up stock-based compensation, currently running at ~24% of quarterly revenues. We believe this to be excessive, and hope the company will start moderating this expense.

Growth

Revenue has kept growing, but the growth rate has seen significant deceleration. We believe it is getting more difficult to justify the lack of profitability when the company is only delivering growth of ~23%. It will be difficult to get investors to pay higher multiples unless the company either re-ignites growth, or shows a clear path to profitability.

Revenue growth is especially disappointing when considering that the company is still benefiting from above average new registered learners, a trend that started with the Covid pandemic. Still, given the higher base, the 5 million new registered learners the company has been averaging in recent quarters is increasingly a smaller percentage of the total registered learners.

Coursera Investor Presentation

Balance Sheet

One big advantage that Coursera still has is its balance sheet, which allows the company to finance cash burn without having to raise new capital, at least for now. Coursera ended the year with ~$780 million of unrestricted cash, cash equivalents, and marketable securities, and with basically no debt. This gives Coursera a long runway to work on improving its profitability and reduce its cash burn or even start generating cash.

Guidance

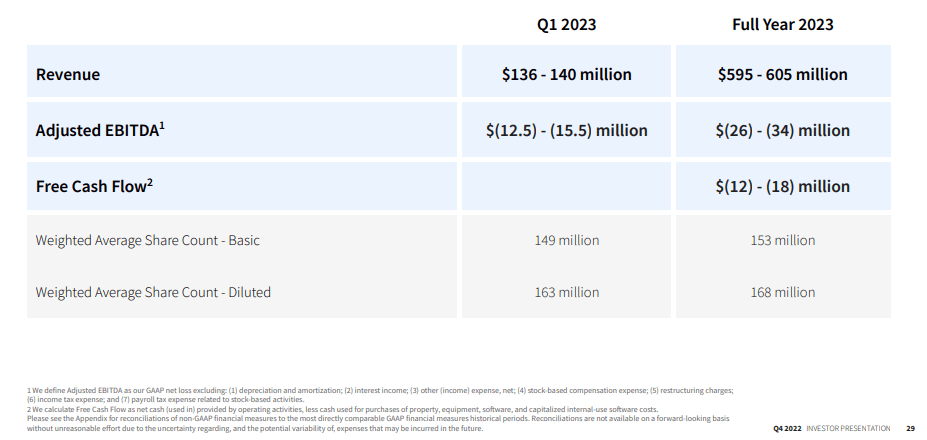

We found guidance to be disappointing, with the company expecting full year revenue of $600 million at the midpoint, which is less than 20% y/y growth, and negative adjusted EBITDA of $26 million to $34 million, a roughly -5% adjusted EBITDA margin at the midpoint of the revenue and EBITDA guidance ranges.

Coursera expects an adjusted EBITDA loss in the first half of the year and anticipates positive EBITDA by its fourth quarter. Shares outstanding are expected to increase by a significant number, which is not surprising given the high SBC.

Coursera Investor Presentation

{kind=link}

Valuation

The good news for Coursera investors is that the valuation is now much more reasonable. The EV/Revenues multiple is currently a little under 2x, given that Coursera sports an enterprise value of ~$1 billion. We think a higher valuation multiple could be justified if the company either accelerates growth, or shows a clear path to profitability.

This EV/Revenues multiple is quite similar to that of other companies going through similar growth deceleration that are also working on proving they can be sustainably profitable. For example, Uber ( UBER ) is trading with an EV/Revenues multiple of ~2.3x, DoorDash ( DASH ) is at ~2.8x, Warby Parker ( WRBY ) is at ~2x, and competitor Udemy ( UDMY ) is at ~1.5x.

Risks

We believe Coursera remains highly speculative, as it continues losing money and is not showing much in the form of operating leverage. On the positive side, it still has a very solid balance sheet that gives it significant runway to work on improving its financials. We would add to the list of risks that growth is rapidly decelerating, and if the trend continues this could put further pressure on its share price.

Conclusion

We were not impressed with Coursera's Q4 and FY2022 results, nor the guidance it provided for 2023. Growth continues decelerating, and the company has yet to show meaningful operating leverage. The company also has excessive stock-based compensation, making it even harder for it to reach profitability. Despite all these issues, the company is still growing and the valuation has come down significantly. We believe an EV/Revenues multiple of ~2x more or less balances the risks and potential rewards, and we are therefore updating our rating to 'Hold' from 'Sell' previously.

For further details see:

Coursera's Valuation Gets A Passing Grade, But Just Barely