COUR - Coursera: Solid Performance Deserves A Buy Rating

2023-08-12 08:51:14 ET

Summary

- I recommend a buy due to COUR strong performance and potential for growth in all segments.

- The Consumer segment has shown resilience with consistent learner growth and the potential for over 20% revenue growth.

- The Enterprise segment faces challenges but maintains healthy new bookings and potential demand from new customers.

Overview

My recommendation for Coursera ( COUR ) is a buy rating, as I am very impressed with the consistent, solid performance so far in all the segments. The business is well positioned to take advantage of several tailwinds, and I expect management to take full advantage of its scale and existing relationships to continue growing the business.

Business

COUR operates as an online educational company. The Company partners with universities and organizations to offer classes on their platform. Coursera serves clients worldwide and competes with peers like Udemy.

Recent results & updates

Looking at COUR 2Q23 earnings report , there are a couple of key takeaways.

To begin, COUR's Consumer segment showed continued strength, which further anchored COUR as a countercyclical business, in my opinion, given the current macro environment. Looking back over the past few quarters, the Consumer segment has once again proven its resilience by adding more than 5 million learners for the 11th consecutive quarter. At an aggregate level, the business now has 129 million learners on the platform. Importantly, growth in learners are broad-based, as management noted that they are seeing double-digit growth in students from all over the world (solidifying COUR reach and market presence). I think that management's emphasis on Professional Certifications is one of the major factor in this growth. At their investor day, management reiterated their commitment to expanding their professional certificate offering by launching 50 new certificates this year. 40 such certifications have been announced thus far by COUR. Strong growth in the number of platform partners was also seen in 2Q, with 15 new university partners joining Coursera. Putting it all together, I don't think it's unreasonable to anticipate Consumer segment revenue growth of over 20% for the foreseeable future.

Second, although existing customers' total budgets are under pressure, the Enterprise segment's new bookings remain healthy. Despite a challenging environment for enterprise spending, I believe that COUR's Enterprise segment showed resilience, growing by 24%. Similarly to the consumer segment, the Enterprise segment saw growth thanks to the success of Coursera for Government and Coursera for Campus. However, I believe investors should be aware of the segment's gradual signs of weakness. Specifically, enterprise net adds fell below 100 to 38 in 2Q23, down from 104 in 1Q23; segment customer growth also continued to decelerate, coming in at 34.8%. Thus, as of the end of 2Q23, Coursera counted 1,291 paying customers. The already-weak net additions were further weakened by the 9.3% y/y decline in average revenue per customer. Coursera for Business has also shown signs of weakness, particularly in North America and Europe, according to the company's management, with NRR falling to 97% in 1Q24 from 104% in 1Q23. Overall, I think it's best to wait a couple of quarters before deciding that COUR is in a danger zone. The weakness could be the result of increased sensitivity of corporate budgets, which is causing a pullback in spending, especially on expansion deals. Management did note sustained strength in demand from new customers, which helps to offset the NRR shortfall.

Degrees revenue was boosted by an increasing count of enrolled students and the introduction of a range of fresh courses. My strong faith in this category stems from management's continuous endeavors to expand program offerings for both FY23 and beyond. Notably, this involves the recent addition of two new programs: a bachelor's program from the Indian Institute of Technology Guwahati and a master's program from Colombia's Universidad de los Andes. The array of available Coursera courses has now expanded to 57, up from 45 in 1Q23. It's worth highlighting that management's remarks foster confidence, as they assert that the regulatory uncertainties in the US haven't dampened interest in degree programs. Their optimism in the growth projection for the Degrees segment, with an expected increase of over 25% in FY24, further underscores positive prospects.

As time goes on and more students and courses are added to the COUR platform, I believe it will gain significant economies of scale. Specifically, it is positioned favorably to reap the benefits of secular growth tailwinds associated with the widespread adoption of digital technologies, the ascent of skills development, and the broader transformation of higher and adult education.

Valuation and risk

{kind=link}

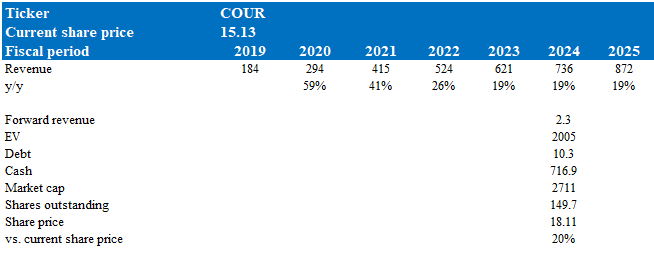

According to my model, COUR is valued at $18.11 in FY24, representing a 20% increase. This target price is based on my growth forecast for the high teens over the next 3 years until FY25. This growth assumption is based on my expectation that COUR can sustain growth equivalent to FY23 guidance, given my strong 2Q23 and my view above.

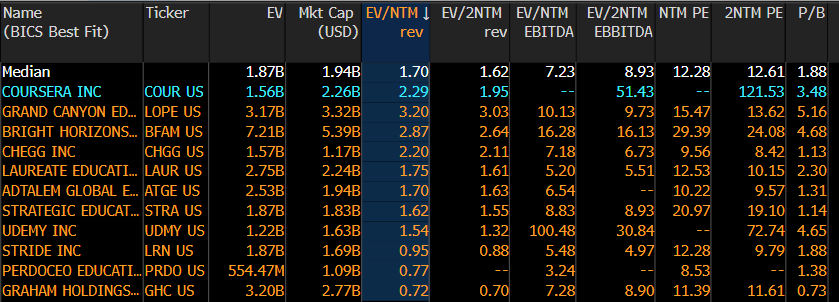

COUR is now trading at 2.3x forward revenue, which I believe will sustain over the near term. When compared to peers, COUR deserves to trade at a premium given its growth expectations and continued positive momentum (in all 3 segments). I note that the entire Educational Services industry has devalued over the past 2 years, and so has COUR accordingly. As such, any rerating at the industry level would certainly help with increasing expected returns.

{kind=link}

The danger here is that most of the content on the Coursera platform comes from established institutions like universities and companies. The company's value proposition will suffer if Coursera is unable to continue attracting these types of partners or if partners do not continue to create content. If that occurred, it would likely create headwinds for their revenues across all three of their segments.

Summary

I recommend a buy rating for COUR based on its impressive and consistent performance across all segments. The company is strategically positioned to capitalize on industry tailwinds, leveraging scale and partnerships for sustained growth. COUR's Consumer segment showcases resilience with steady learner growth. While the Enterprise segment faces challenges, it maintains healthy new bookings and potential demand from new customers. As COUR continues to scale, I expect it to benefit from economies of scale and broader industry transformations.

For further details see:

Coursera: Solid Performance Deserves A Buy Rating