COUR - Coursera: Staying Cautious For Now

2023-03-09 02:19:46 ET

Summary

- Coursera is down over 70% since going public in 2021.

- The online learning company operates in a huge market that is continuing to expand.

- Its fourth-quarter earnings results are solid but guidance indicates a meaningful slowdown in top-line growth.

- The current multiples are still higher than peers.

- I rate the company as a hold.

Investment Thesis

Coursera ( COUR ) has been performing badly since going public in 2021, with shares down over 70% at the moment. The company operates in the massive online learning market that continues to expand which offers solid tailwinds. Its latest earnings showed decent revenue growth and bottom-line improvement but the guidance signals quite a deceleration in the top line, which is concerning. Despite the drop, the company's current valuation is still meaningfully above peers. I do not see much further upside from current levels and I rate COUR stock as a hold.

Market Opportunity

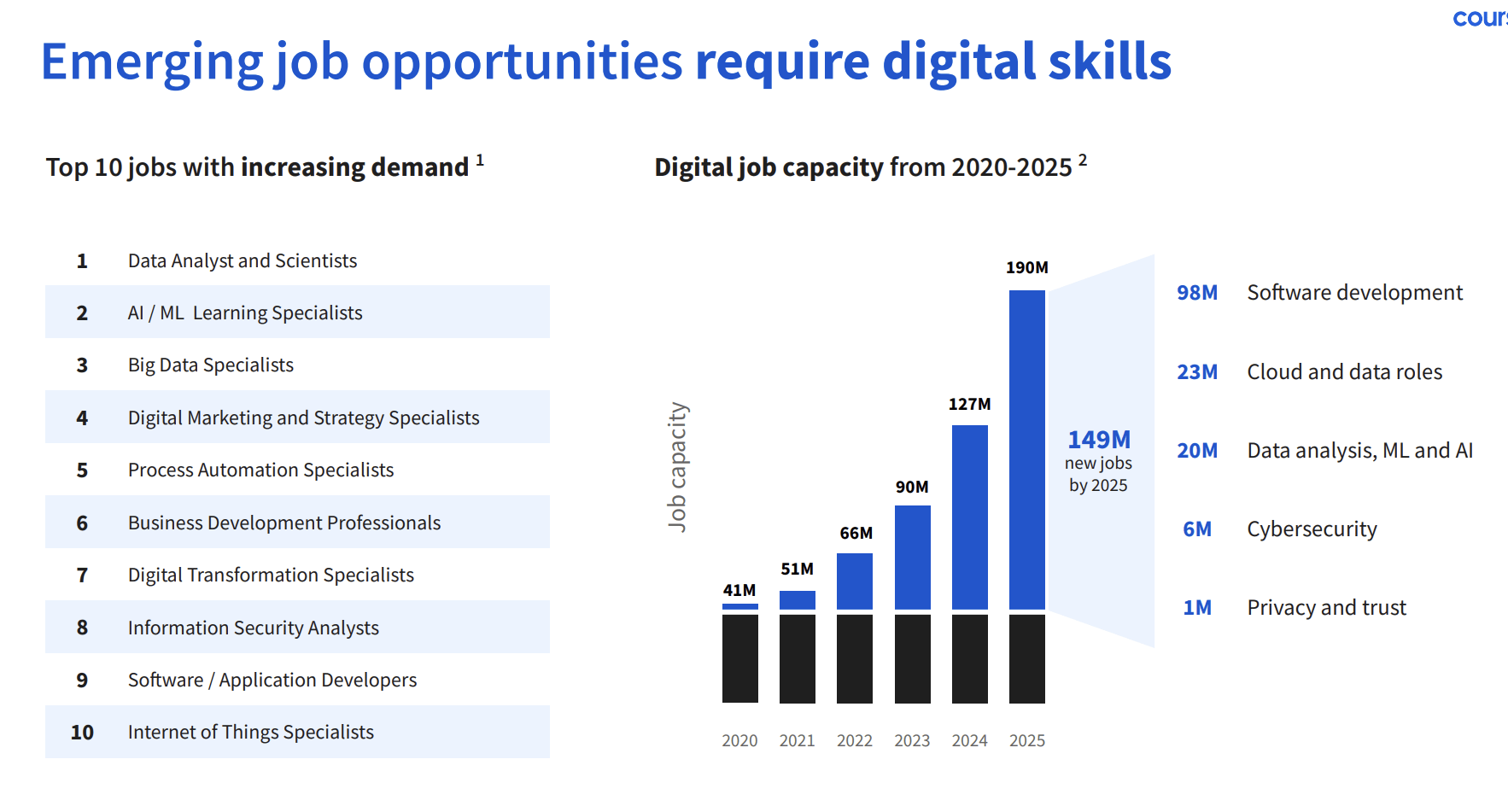

Coursera is an online learning platform founded back in 2010. Unlike Udemy ( UDMY ) which offers courses uploaded by individuals, the company partners with over 300 notable universities and companies such as Stanford and Google ( GOOG ) (GOOGL) to offer specialized degrees or courses for users. It covers multiple subjects ranging from data science to music. The company currently has over 5,500 courses and nearly 120 million users. Online learning is a massive market that continues to expand quickly. According to Statista , its TAM (total addressable market) is expected to grow from $166.6 billion in 2023 to $238.4 billion in 2030, representing a solid CAGR (compounded annual growth rate) of around 9.4%.

There are several factors fueling the expansion. Firstly, online learning offers a significantly cheaper option compared to traditional education which is very expensive in most countries, especially for specialized courses. Besides, those who reside in remote areas might not be able to attend in-person sessions or may not have access to any nearby educational alternatives. Online learning is the most practical choice for them as the internet infrastructures are significantly more accessible and dependable.

Digital transformation also substantially disrupted the demand for different skills. For example, AI tools are reducing the need for data entry work while skills like coding and design are seeing increasing demand. Many employees may have to re-skill in order to remain competitive. According to Udemy , it is estimated that 50% of employees will need re-skilling and 40% of core skills will change in the next five years. I believe the ongoing expansion of the market will continue to be a growth driver for the company.

{kind=link}

Q4 Earnings

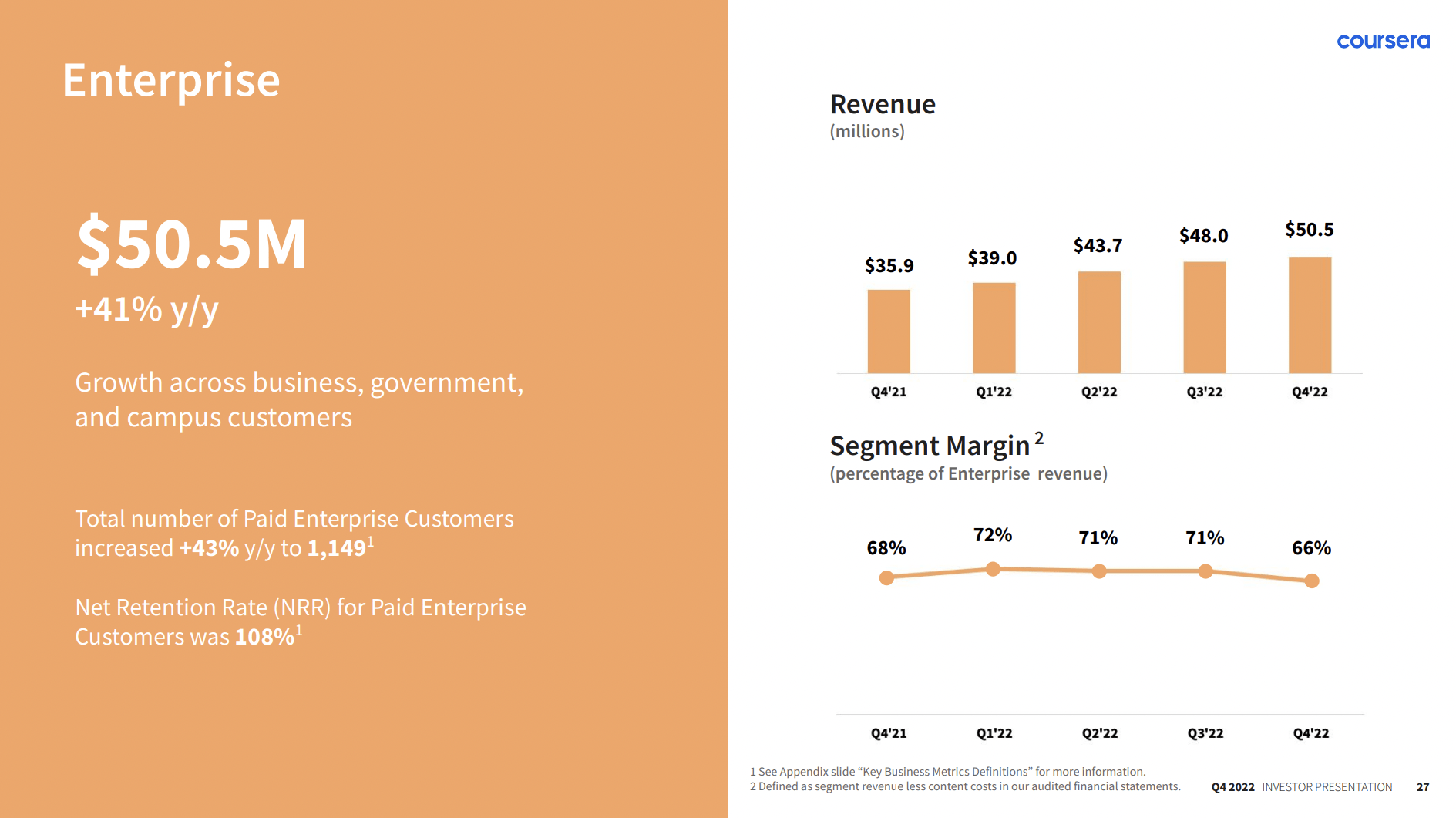

Coursera recently announced its fourth-quarter earnings and the results are pretty mixed. The company reported revenue of $142.2 million, up 24% YoY (year over year) from $115 million. The growth is largely driven by the momentum in the enterprise segment, which continues to land new customers. The number of paid enterprise customers increased by 43% YoY to 1,149. Enterprise revenue grew 41% YoY from $35.9 million to 50.5 million and now accounts for 35.5% of total revenue. The consumer segment also increased by 21% YoY from $65.8 million to $79.8 million, partially offset by the decline in Degree's revenue which dropped 11% YoY from $13.3 million to $11.9 million. Gross profit was $87.9 million, up 23% YoY from $71.3 million. The gross profit margin was flat YoY at 62%.

{kind=link}

Despite still being unprofitable, the bottom line finally showed some improvements as spending slowed. S&M (sales and marketing) expenses only increased 7.5% from $57.6 million to $61.9 million. While R&D (research and development) expenses increased 11.7% from $38.3 million to $42.8 million. This resulted in the adjusted EBITDA improving by 74.5% YoY from negative $(19.6) million to $(5.8) million. Non-GAAP net loss also improved by 73% YoY from $(24.1) million to $(6.5) million, or 4.6% of revenue.

Guidance was the letdown of the report. The company expects revenue for FY23 to be in the range of $595 to $605 million, which represents a YoY growth of just 14.5% at the midpoint. This indicates a meaningful slowdown from 26% in the prior year.

Investor Takeaway

I believe Coursera should have ample growth opportunities in the long term thanks to its large and expanding TAM. However, the guidance and valuation are causing me to stay away for now. The guidance indicates a surprisingly large slowdown in revenue growth from 26% to 15%, with little improvement in the bottom line also. Not to mention the company’s upcoming contract renewal for joint courses with companies like Google, which may further increase their costs and weigh on profitability. The company is currently trading at a Fwd. EV/sales ratio of 1.79x, which represents a 31.6% premium compared to its major competitor Udemy, which is trading at a Fwd. EV/sales ratio of 1.36x while posting similar growth rates. I believe the guidance and valuation should limit Coursera's upside and I rate it as a hold.

For further details see:

Coursera: Staying Cautious For Now