CBRL - Cracker Barrel Is A Good Buy At Current Levels

2023-04-17 10:44:02 ET

Summary

- Revenue should benefit from price increases, a diversifying demographic customer mix, growth of the catering business, and resumption of new unit expansion.

- Moderating inflationary pressure, and improving productivity should help margin growth.

- Valuation is attractive.

Investment Thesis

Cracker Barrel Old Country Store ( CBRL ) is expected to benefit from its revenue growth through price increases, a more diversified demographic customer mix, an expanding catering business, and resuming new unit expansion which should offset the slowdown in traffic. On the margin front, moderating inflationary pressure and productivity initiatives along with price increases should support margin recovery in the coming quarters and beyond FY23. The stock is trading below its historical levels and combined with good revenue and margin growth prospects ahead, the stock is a good buy at the current levels.

Revenue Analysis and Outlook

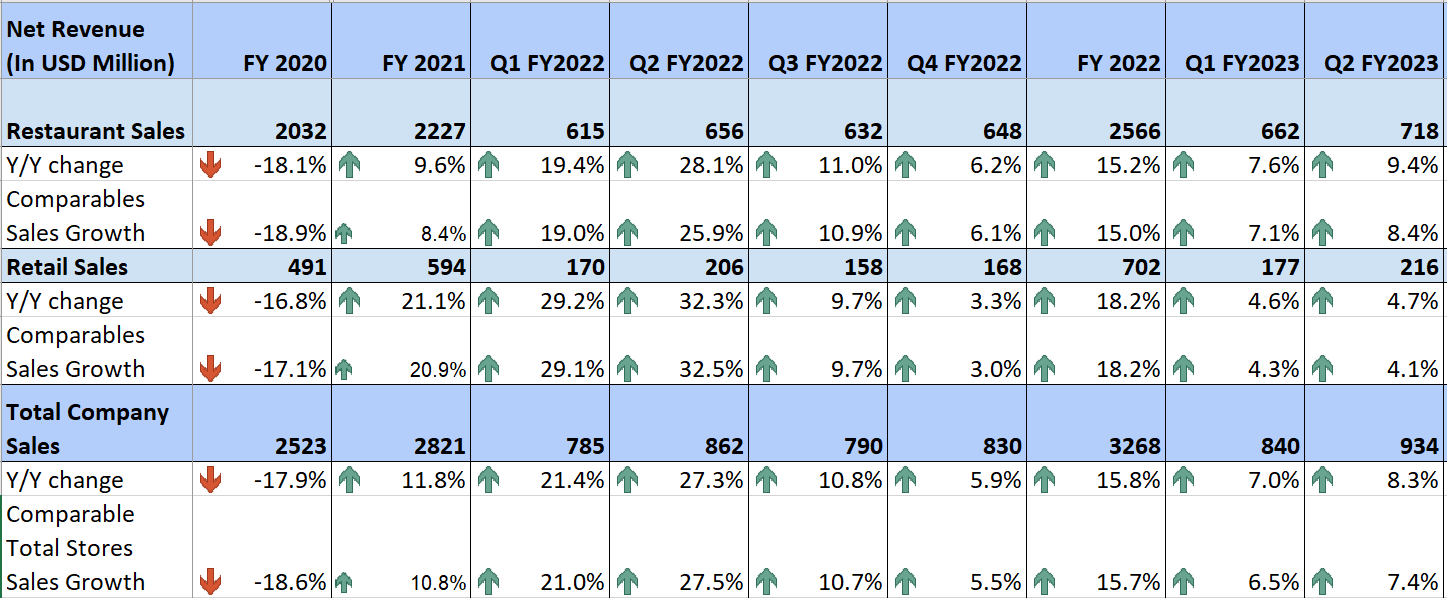

After Covid-related disruptions in FY2020, Cracker Barrel's revenue has seen good growth over the last couple of years due to easing travel restrictions, an increase in off-premise sales, and continuous menu enhancements.

In the second quarter of fiscal 2023, these trends continued, and sales were further boosted by pricing initiatives and increased demand for both restaurant services and retail products during the holiday season. This resulted in an 8.3% YoY increase in sales, which reached $934 million. On a comparable same-store basis, total company sales grew by 7.4%.

{kind=link}

CBRL’s Historical Revenue (Company Data, GS Analytics Research)

Moving forward, CBRL should continue to experience revenue growth due to price increases, expanding off-premise services, resuming new unit expansion, and increasing the traffic of younger customers.

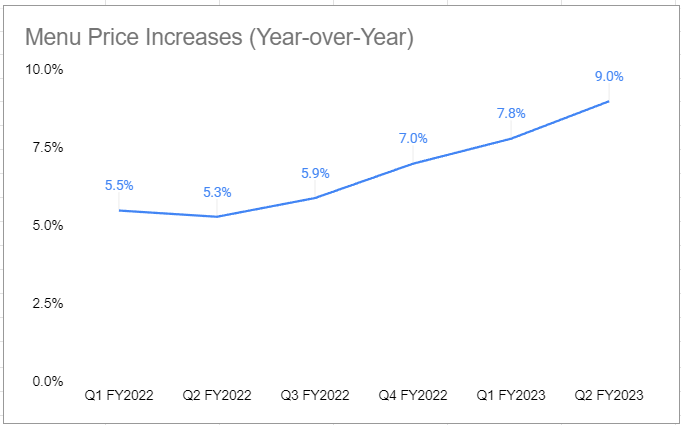

As with many industries, the restaurant sector is facing inflationary pressures and is increasing prices to maintain margins. CBRL has implemented multiple pricing increases in recent quarters, and the company plans for additional price increases in the upcoming quarters. This is expected to lead to average check growth and support revenue growth going forward.

{kind=link}

CBRL’s Historical Price Increases (Company Data, GS Analytics Research)

Furthermore, CBRL's off-premise business has grown significantly from pre-pandemic levels over the past couple of fiscal years. The off-premise business is comprised of 40% individual to-go pick-up, 40% third-party delivery, and 20% catering services. To-go pick-up and third-party delivery are benefiting from changing consumer preferences toward online services, and catering services are also growing at a rapid pace. In Q2FY23, catering services grew by 40% YoY, and the company aims to increase catering as a percentage of the total off-premise mix to 25% and reach around $100 million in sales by the end of FY23. To achieve this, the company is doubling down on catering services' marketing and expanding the delivery network for catering so that all stores can offer this service. I expect CBRL's off-premise business to continue to drive the company's sales growth.

Moreover, the company's new unit expansion was disrupted during the pandemic due to supply chain constraints and labor unavailability, leading to construction delays. These headwinds have begun to ease, which should allow for the resumption of new unit expansion in the coming years. CBRL is also focusing on expanding Maple Street Biscuit Company ((MSBC)), which management believes offers a long-term growth opportunity for CBRL by expanding its footprint in urban and suburban areas. The company plans to open 3-4 new Cracker Barrel locations and approximately 15 new MSBC locations in FY23 at the low end of its guidance. As supply chain constraints further ease, we can see store growth acceleration in FY24.

CBRL is also actively diversifying its demographic mix and increasing the traffic of younger customers in its stores. It has introduced menu items that appeal to this age group, such as beer and wine, which are gaining positive traction, and online payments, which increases convenience.

While there are concerns about a macroeconomic slowdown, I believe the company-specific initiatives can offset them. Management has guided for a 7-9% reported sales growth for FY23, which looks achievable due to the anticipated 8.5% price increases for the full year. CBRL's longer-term growth outlook also looks positive and should benefit from new unit expansion, the increasing catering business, and the growth of a younger customer base.

Margin Analysis and Outlook

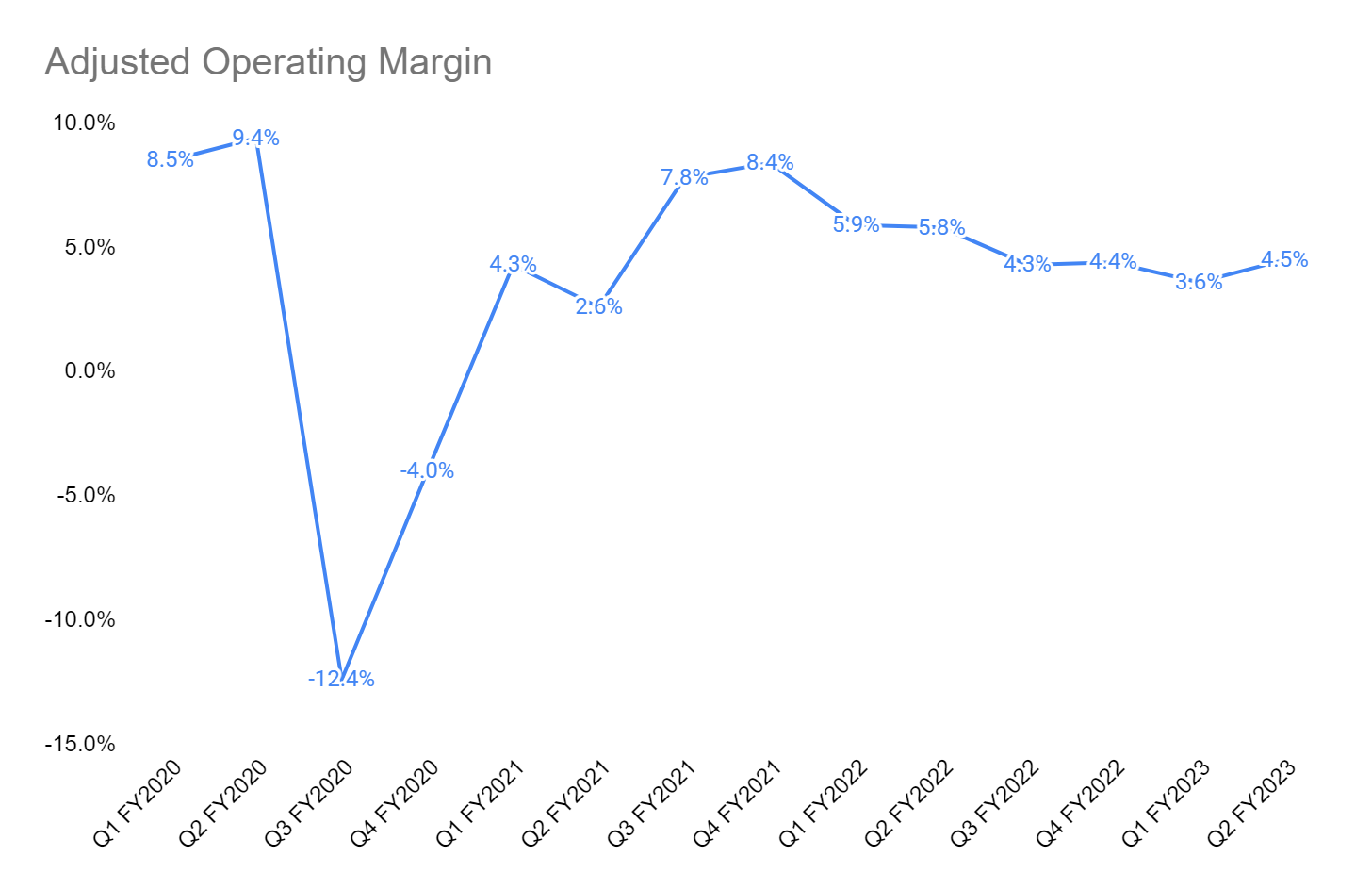

Since the beginning of the fiscal year 2022, CBRL's adjusted operating margin has been negatively impacted by inflationary commodity costs, including poultry, oils, grains, and dairy, as well as higher labor wages. The company has been trying to offset these inflationary headwinds through price increases.

In the second quarter of the fiscal year 2023, the inflationary headwinds persisted as the company experienced a total of 12.5% Y/Y inflation during the quarter, which was partially offset by pricing and a favorable menu mix. As a result, the adjusted operating margin declined by 130 basis points year over year to 4.5%.

{kind=link}

CBRL’s Historical Adjusted Operating Margin ( Company Data, GS Analytics Research)

Looking ahead, moderating inflationary pressures should help margins in the coming quarters. CBRL expects mid-single-digit inflation in Q3 and low single-digit inflation in Q4, which should be offset by high-single-digit price increases.

Furthermore, CBRL is implementing cost-saving and productivity-enhancing measures, such as a labor management system across 300 of its stores. This system improves cost visibility and increases productivity by matching labor to the specific time of day and type of business. These initiatives are expected to generate $25 million in cost savings in 2023 and more in the coming years. As a result, in 2HFY23 and beyond, we should expect some improvement in adjusted operating margin as inflation moderates and productivity initiatives take hold.

Valuation and Conclusion

Cracker Barrel is currently trading at a 19.18x FY23 consensus EPS estimate of $5.92 and a 15.80x FY24 consensus EPS estimate of $7.18, which is below its historical 5-year average forward P/E of 22.96x. The company has good growth prospects as it should see revenue growth benefits from price increases, expanding off-premise services, resuming new unit expansion, and increasing the traffic of younger customers. This should offset any macroeconomic-related slowdown in the guest traffic. In addition to revenue, margins should also benefit from price increases, moderating inflation, and improvement in productivity. Hence, lower than historical valuation and good revenue and margin growth prospects make the stock a good buy.

For further details see:

Cracker Barrel Is A Good Buy At Current Levels