CBRL - Cracker Barrel Old Country Store Is Potentially Nourishing

2023-08-23 05:45:30 ET

Summary

- Cracker Barrel Old Country Store is a chain of restaurants and gift shops employing +70K that focuses on Southern country themes.

- The company's stock has tumbled, and the company faces headwinds as declining traffic and rising costs bring shareholders risks.

- CBRL's finances are stable; there is potentially higher revenue and earnings and lower debt with a share price move up of 10% to 15% in the future.

Southern Comfort

The hospitality industry, especially restaurants and food companies, is one of our favorite subjects of study. We have written quite a few articles about them as investment opportunities for Seeking Alpha and our followers.

The industry offers an insightful peek into the national culture's traditions, taboos, habits, tastes, and the powerful influences shaping the national spirit and mindset. The Consumer Discretionary Select Sector SPDR Fund (XLY) and others for investing in hospitality and restaurants are trending up 28% YTD.

Doing business since 1969, first in Tennessee under the moniker Cracker Barrel, the Cracker Barrel Old Country Store, Inc. (CBRL) grew into a +$3B American chain of restaurants, gift shops, and a slew of subsidiaries. Cracker Barrel nurtures the theme of Southern country, i.e., plain, simple, and unsophisticated tastes in food, environment, and ambiance. Its "down-home menu has items like chicken and dumplings, meatloaf, fried chicken, and breakfast all day." Last year, many locations added alcohol and fashionable drinks to the menu.

{kind=link}

Risks Are Trending Up

Past stumbles might easily trend into sustained tumbling. In April '23, the shares topped $118 but sell today for ~$83. The share price fell about 5% since the Q3 quarter report . Short interest is a high 9.57%. The stock's Beta is 1.16. We characterize 50% of the media articles about Cracker Barrel as positive compared to +60% of articles about the rest of the industry.

The Board turned to an outsider from Taco Bell to announce last month the hiring of a new President and CEO. The Chief Exec has for the last 5 years been with Taco Bell. Implementation of fresh ideas is going to take many months in a company with more than 73K employees.

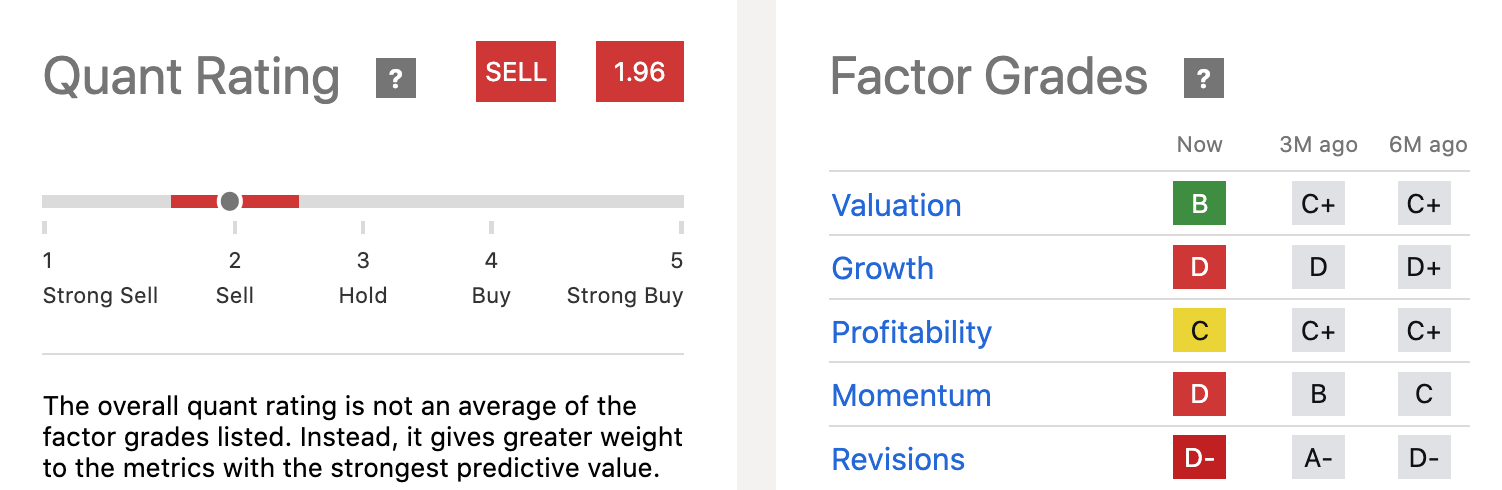

The SA Quant Rating shifted over the last year from assessing the stock as a Buy opportunity, to Hold between December '22 and July '23, and now as a forthright Sell. We like the industry, and the appeal to middle-income patrons, and believe Cracker Barrel is a potential opportunity worth a Hold rating at this time. But other factors give as pause for now.

More Risks

Our concerns for retail value investors include Crackle Barrel assets dropping and declining traffic, perhaps foreboding a trend. Cracker Barrel, like all restaurants, suffers from these constant headwinds: rising wages for labor and labor shortages, rising food prices, and space and occupancy costs.

SA recently issued a warning that the company's growth rate is below par in most metrics of its Total Return Index. Moreover, momentum and profitability are given slipping Factor Grades.

{kind=link}

Assets dropped between July '22 and May '23 from approximately $317M to $273M respectively. Cash and equivalents fell from ~$45M to $22.45M. There was less traffic and lower catering/takeout numbers. Total revenue for 9 months ending April 28, '23 was $2.6B versus $2.43B ending in April '22. All facets comprising operating costs were up while concomitantly operating income dived over 9 months from $120M to $79M; net income dived to $61.58M compared to $98.5M.

In the last quarter reported in June '23 (Q3), revenue was +5.4% Y/Y but less than anticipated. Restaurant sales rose 7.4% but casual dining traffic declined (3.2%) in the last quarter. Comparable gift store sales were reported -4.6%. We cannot say for sure but it will be interesting to learn more about declines in traffic in the current quarter after a boycott call of Cracker Barrel for having honored Pride Month in June. The next quarterly report announcement is expected on September 26, 2023.

Other matters undergirding our concerns include:

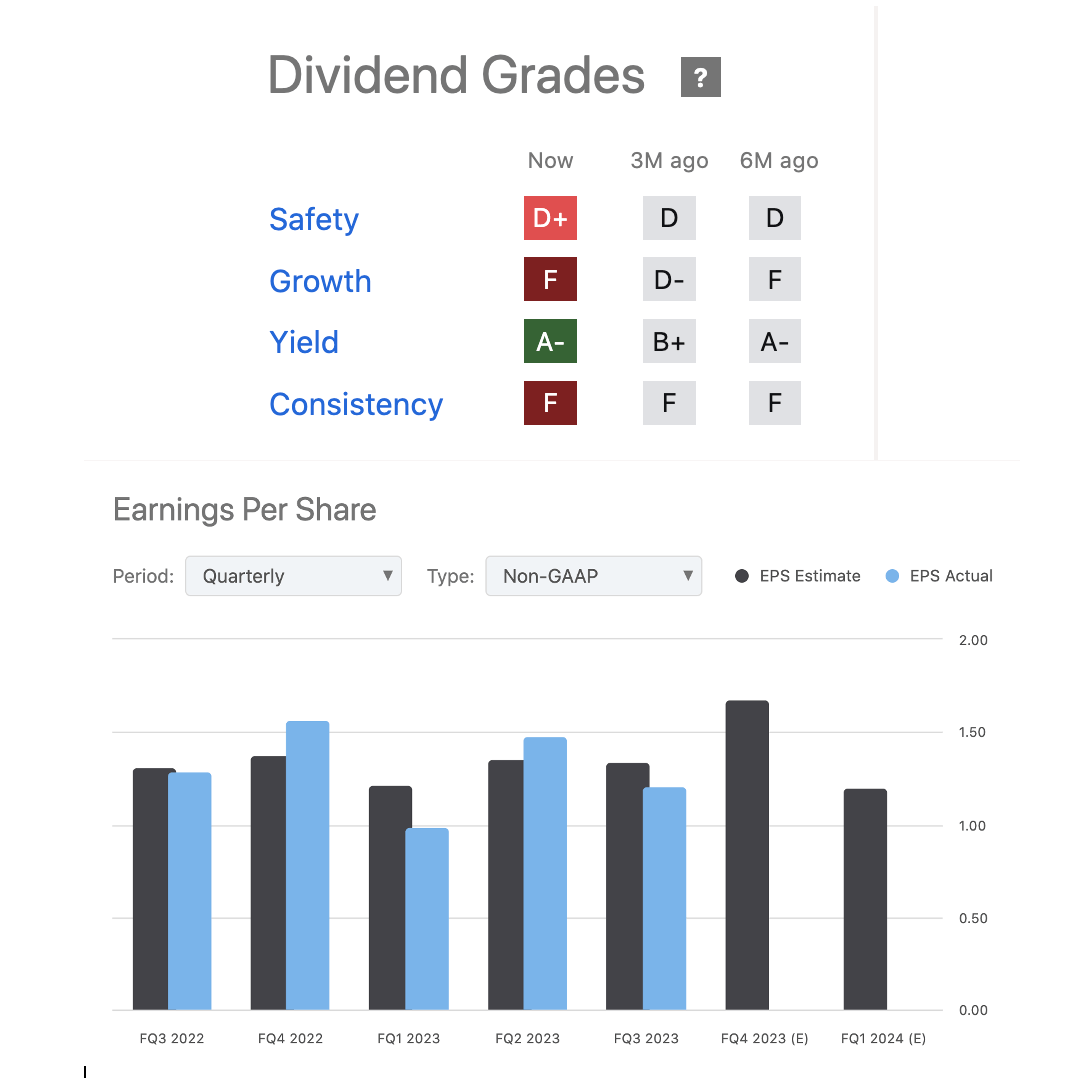

- the rollercoaster quarterly EPS

- the unsettling grades for the dividend; 6.26% yield (Fwd) is attractive but the rest of the measures (safety, growth, and consistency) are in negative territory and have been for over a year

- the dividend is not covered well by cash flows

- the company's net income margin of 2.76% is lower than last year (4.2%) and below the full-service restaurant industry average of ~5%

- volume drives margins in the restaurant business, so if traffic slides further than already noted be prepared for declining profitability, margins, and dividend might decline

{kind=link}

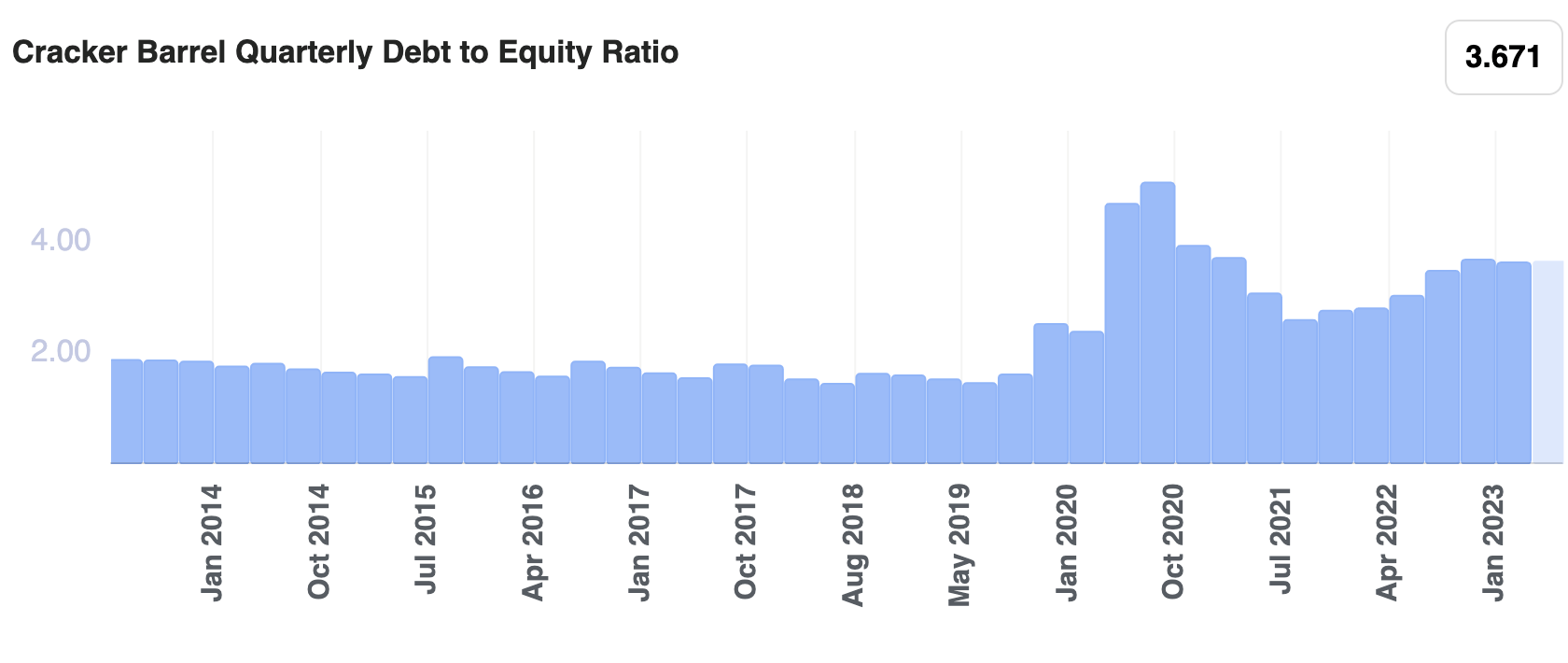

Finally, total debt is $1.2B while cash and equivalents are $22.45M. Its debt-to-equity ratio is almost 94%. Short- and long-term liabilities are not covered by short-term assets. Revenue growth seems to go hand-in-hand with greater debt. Shareholder financial security is potentially imperiled by more interest rate hikes and potential consumer cutbacks on discretionary spending. This might result in diminished traffic in restaurants and gift shops.

{kind=link}

Stable Table For Now

In our opinion, Cracker Barrel's finances are currently stable and the prospect for higher revenue and earnings in 2024 is good. Adding beer, wine, and trendy non-alcoholic drinks to the menu will positively affect the bottom line. The average drink profit margin is 70% to 80%, "far higher than the average food profit margin," according to a senior restaurant marketing guru.

Annual revenue since 2020 increased. It is up from $2.52B in 2020 to $2.82B in 2021, to $3.27B in 2022. We forecast revenue will top $3.45B in 2023. Most of this is from organic growth since Cracker Barrel acquired just 2 companies in the last 5 years. Shareholder return on equity is nearly 20%.

Takeaway

We do not expect any surprises in the September '23 next quarterly report announcement justifying a significantly higher target share price; the impact of the new Chief Officer's policies will not hit for at least 6 to 9 months. Headwinds facing restaurant operators are not waning anytime soon. Adding to the fragility of the financial footing is the substantial debt. In the meantime, Management paid down almost $70M TTM in debt and free cash flow per share rose from $4.62 in July '22 to $5.57 TTM. If free cash flow continues equaling 90% of its EBIT the company will be able to pay down more debt.

The financial and business strengths compared to the risks lead us to conclude that Cracker Barrel's share price might currently be undervalued by 10% to 15%. We believe it is best considered a Hold opportunity for the next few quarters to be mulled over a solid breakfast.

For further details see:

Cracker Barrel Old Country Store Is Potentially Nourishing