CBRL - Cracker Barrel's Difficult 2 Years From COVID Right Into A Recession

Summary

- Cracker Barrel stock has weathered significant disruptions to its business in the past couple of years.

- I like the management team, but the company isn't back to its prior form yet.

- I'm not certain the trajectory is adequate to make up for the risks, the valuation isn't all that appealing, and the company has shifted to repurchases vs. their special dividends.

- CBRL is a hold, but I wouldn't judge you for selling it.

I'm taking a break from my recent string of articles to revisit a company I haven't spent a lot of time on recently. It's among the first I covered on this site, and I think it will be constructive to take a look at how they've performed since I last covered the Cracker Barrel stock.

{kind=link}

Well, you can't win them all. I was bullish on Cracker Barrel (NYSE:CBRL) in 2016, but quite a lot has changed. Firstly, CBRL has always been a pretty heavy draw for the older cohorts in America, and they were by and large the most affected by the pandemic.

Company Presentation

Adding to that, CBRL benefits pretty heavily from travel, which was also heavily affected. Add into that the surges in inflation, high gas prices, and overall macroeconomic malaise with a looming recession, and things haven't looked all that rosy for CBRL for the last few years. Some perspective from the most recent earnings call:

I would say, in general, our 65 plus guests in spite of things like that social security increase are still we're seeing all-time lows or near all-time lows with their sentiment. And I think that with pressure in terms of food, gas and rent and all of that being up significantly more, right? Food inflation in the grocery store is up 20%. So -- and gas prices, although they're low today, it's been incredibly volatile, up, down, up, down. And so their sentiment is very negative. Their outlook for the future. Their financial and security is very high.

So I think even though we have seen some improvement in our trend with our 65 plus guests, there is still quite a bit of recovery left for us with that group.

{kind=link}

{kind=link}

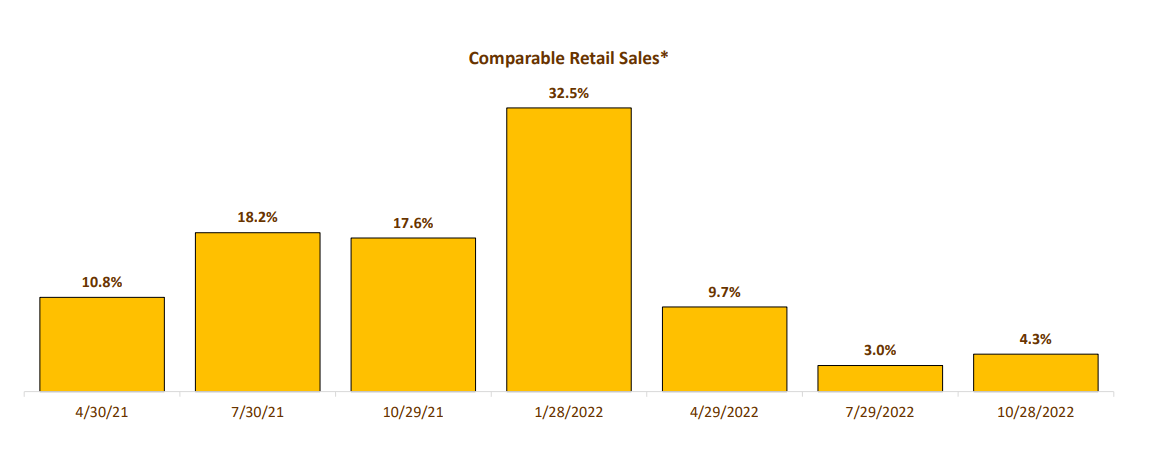

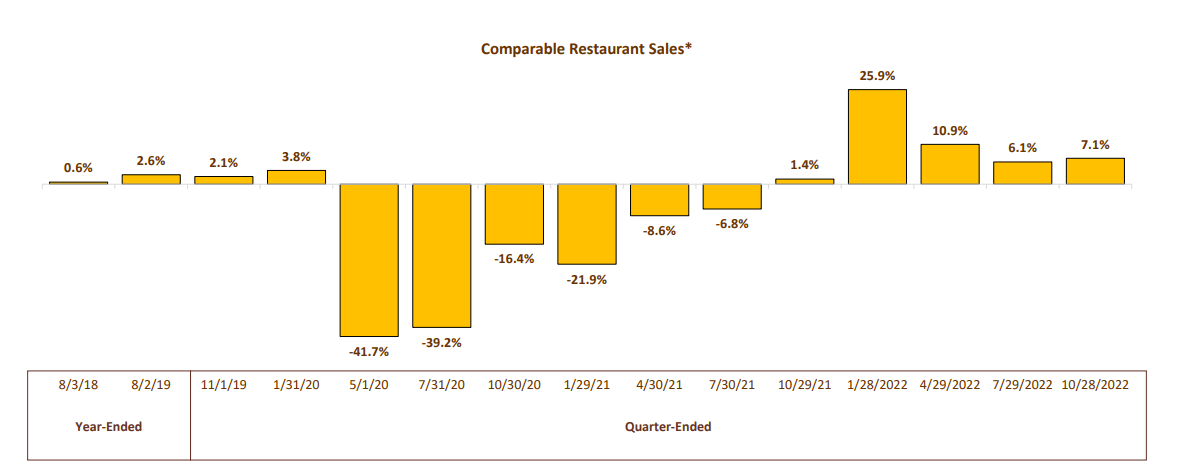

Sales have recovered somewhat from the pandemic, but they only recently regained pre-Covid values. Retail accounts for about 20% of revenues, listed at the top, and the restaurant/off-site accounts for the remainder. It takes a lot to bounce back from the shock of a global pandemic straight into an economic slowdown. Although sales have rebounded, earnings haven't yet, and the path for that to happen in the short term is rather murky.

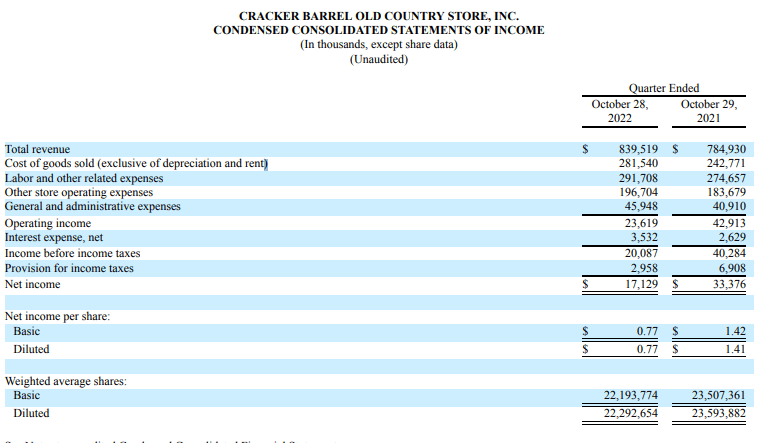

In the most recent quarter, the company drove 7% sales growth, with comparable store sales up 7.1% for restaurant and 4.3% for retail. However, the vast majority of these comp's were driven by pricing increases in response to inflationary and freight cost pressures on the company. Not seeing traffic and basket improvements isn't the most bullish sign.

{kind=link}

Looking at margins, COGS was up to 33.5% of revenues from 30.9% due to inflation and freight. Inventories increased by $51M due to right-sizing and establishing adequate inventories to counter potential supply chain issues based on the earnings call discussion. Add 5-6% wage inflation expected on the full year, and that's a recipe for operating margin compression, which has trended down pretty steadily over the past several quarters.

This slowing down in overall profitability is concerning, but management is confident in its initiatives including improvements in labor to drive a full-year operating margin of 4%, up from 3.6% this quarter. With the shifting environment, management was able to provide full year 2023 guidance of 6-8% revenue growth with 3-4 new CB restaurants and 15-20 new Maple Street locations for a total of $125M in capex. My takeaway is there isn't likely to be significant acceleration from this quarter through the end of the year barring unforeseen improvements in factors out of the company's hands to drive up profitability. Some perspective from the call:

Now we do have some things going the other way, for example, eggs and dairy and some produce items. But in aggregate, our expectation is that produce is going to move down. And what we are experiencing is things are together, meeting our expectations, but it's taken a little bit longer than we originally expected. So as a result, we expect our COGS story, which is going to be a really big driver of our margin improvement and profitability improvement. We expect a lot of that to come to come to fruition in Q4.

And at that point, we'll be -- we expect to be well above prior year. So at that point, we have some commodity deflation, and we are also getting more full benefit of the pricing actions. We've been taking multiple pricing actions throughout the year. So all of that together culminates then. The overall expectation is similar. It's not the same to where we started our fiscal it's just pushed out a little bit.

Management was relatively confident the company would start to see improvement into Q4, which is something I would wait to see before jumping in with the way things have been going for CBRL. It's not surprising the company isn't making any bold assertions or initiating knee-jerk reactions based on my time owning the company. They move methodically with most every decision, testing things out in small clusters of restaurants before rolling them out and mostly staying conservative.

Looking at SG&A expense as a percentage of revenues, it's back in line with pre-Covid, which is a good sign of management's initiatives to rein in costs.

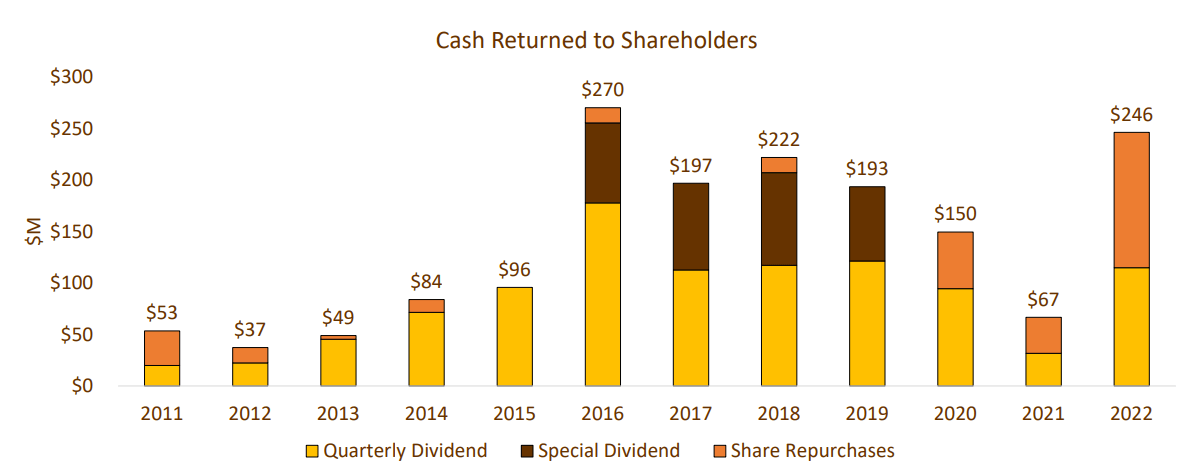

As far as the balance sheet goes, the company isn't in a bad spot. Total debt came in at $484M, with $108M in free cash flow last year. The company has shifted its focus away from the special dividends I was so fond of before Covid. With lower profitability and difficult operating environments, the company cut its dividend, removing it from the consistent dividend growers club. Since 2020, management has chosen to return capital to shareholders more in the form of share repurchases. Considering the stock shot back up to all-time highs in 2021 before crashing back down, this likely resulted in some waste, in hindsight. C'est la vie, special dividends don't appear to be making a comeback.

{kind=link}

{kind=link}

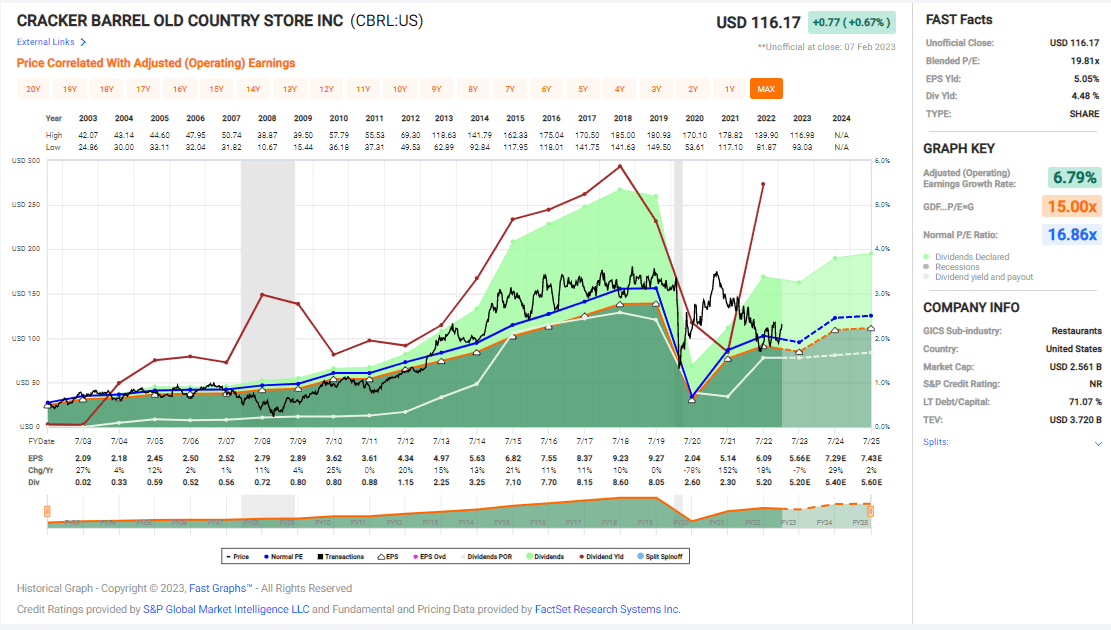

Looking at valuation, the earnings reset in 2020 hasn't bounced back yet. The stock is trading for cheaper than points in 2014, but remains at a little above its long-term valuation at around 20X earnings.

{kind=link}

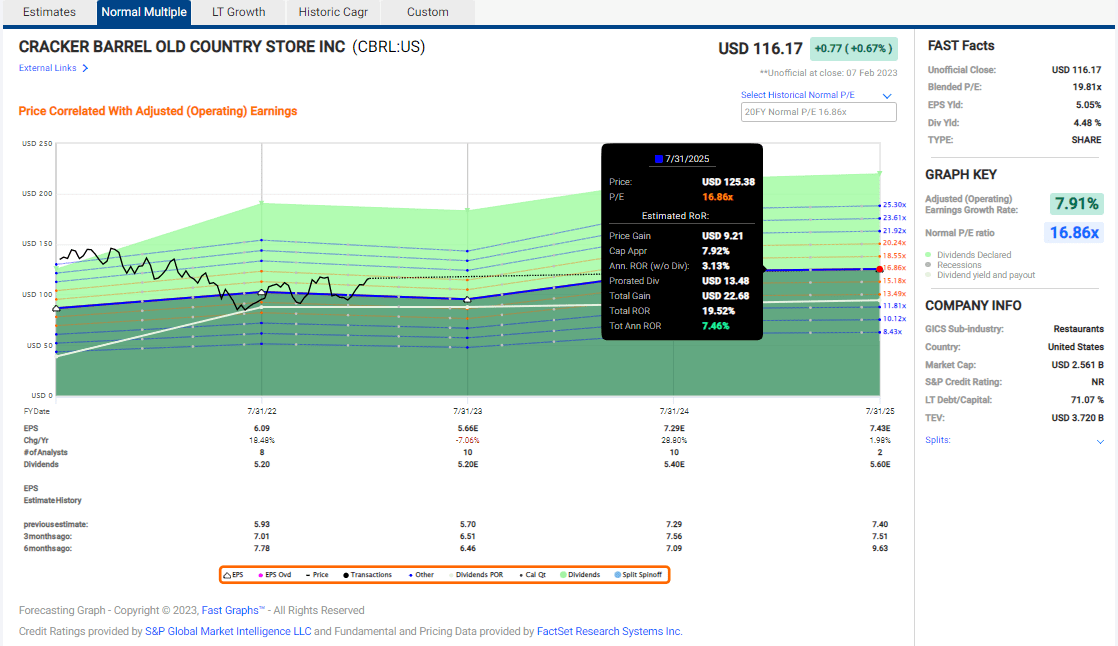

Based on a rerating to 16-17X earnings and analyst estimates for earnings growth, an investment today could yield around an 8% annualized rate of return. There's a lot of unknowns here as CBRL continues to navigate a difficult environment. Management has made good decisions in the past, and the company was on a solid trajectory pre-Covid. This is proven out by looking at the company's earnings growth up until 2019 above. However, the slow growth, changes in capital allocation methods, unclear path for operating margin expansion, and unappealing valuation will keep me away from CBRL for now. I'll rate it as a hold, and I'll take a look at how results are trending over the coming quarters.

For further details see:

Cracker Barrel's Difficult 2 Years, From COVID Right Into A Recession