CBRL - Cracker Barrel: Valuation Improving After The Drop

2023-10-08 02:19:16 ET

Summary

- Cracker Barrel has been one of the worst-performing restaurant stocks over the past two years, and disappointing industry-wide traffic in Q3 suggests a foggy outlook for its fiscal Q1 results.

- In addition, the ~90% payout ratio means a turnaround is needed to support its dividend, and industry-wide traffic certainly isn't providing any help short term.

- In this update, we'll dig into the recent results, industry-wide trends, and whether the stock is offering a margin of safety yet.

While the restaurant industry group has had a rough few months, few names have suffered as badly as Cracker Barrel Old Country Store ( CBRL ), which is now down 28% year-to-date and over 60% from its highs reached in 2018. This underperformance can be attributed to lackluster sales performance and continued margin compression, with operating margins sinking by over 400 basis points since 2017 and the company seeing industry-lagging unit growth with just ~11% growth in the past six years despite the acquisition of Maple Street. Unfortunately, the company's FY2023 results weren't much better, and with earnings taking another dive on a year-over-year basis, the company's payout ratio has spiked above 90%, up from ~55% in FY2017.

Although this doesn't mean that a dividend cut is imminent, it certainly puts a question mark around the dividend if the company can't turn things around soon. Meanwhile, although some investors might have hoped for a better start to its fiscal year, industry-wide traffic is not providing any help, with casual dining traffic sinking again in September to its worst levels year-to-date, with a further deceleration on a monthly basis. This is consistent with Cracker Barrel flagging a soft start to 2024 (quarter starting July 29th) in its year-end results, suggesting little reprieve from what's been a disappointing trailing-twelve-month traffic trend for the company. Let's look at the recent results and developments below:

{kind=link}

Recent Results & Q1 2024 Outlook

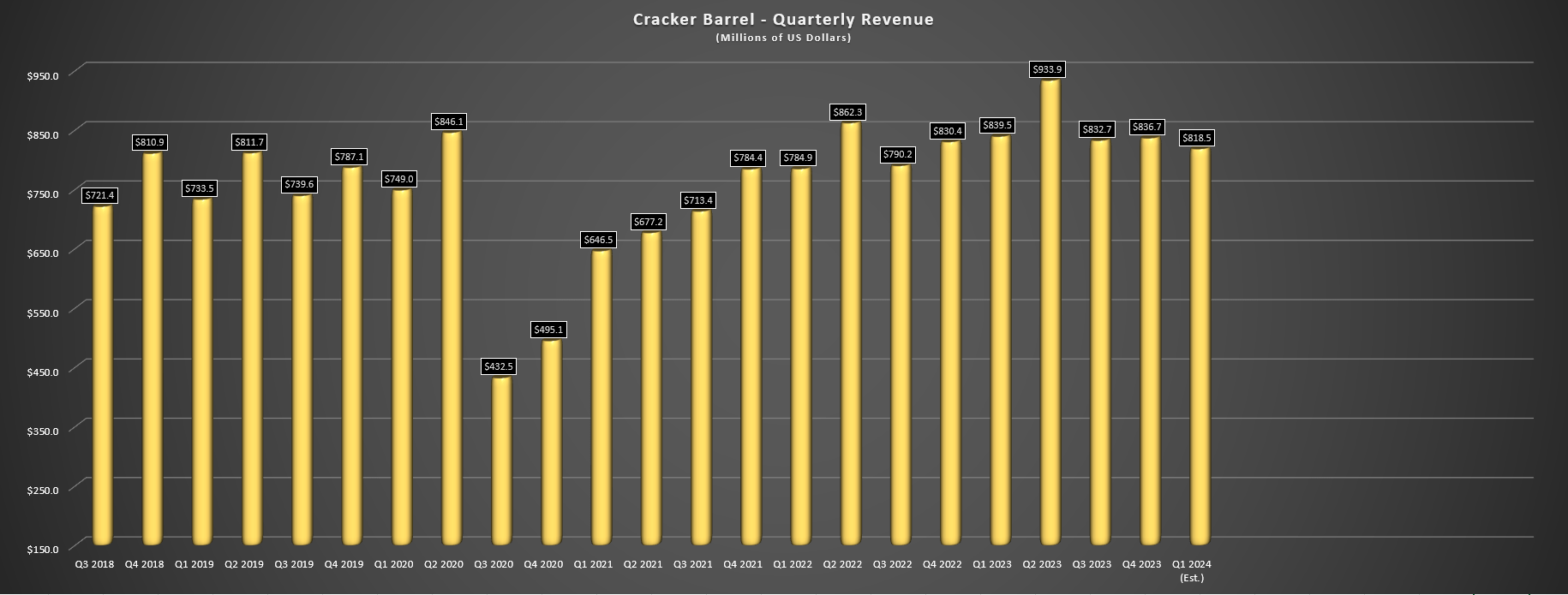

Cracker Barrel released its fiscal Q4 and FY2023 results last month, reporting quarterly revenue of $836.7 million, a 1% increase year-over-year that was below expectations according to the company. These results were more disappointing given that the company was running with high single digit menu pricing in the period which implied a sharp decline in traffic, and the company reported comp restaurant sales growth of just 2.4% in the period while comparable retail sales growth sunk 6.8%. On a two-year stacked basis, this resulted in 8.5% and [-] 3.8% comp sales for its restaurant and retail segment, respectively, which is not all that inspiring. Cracker Barrel noted that its softness showed up in all cohorts, and that its over 65 age group that appears to be more judicious on where they spend with value in mind saw more softness than its younger cohort.

{kind=link}

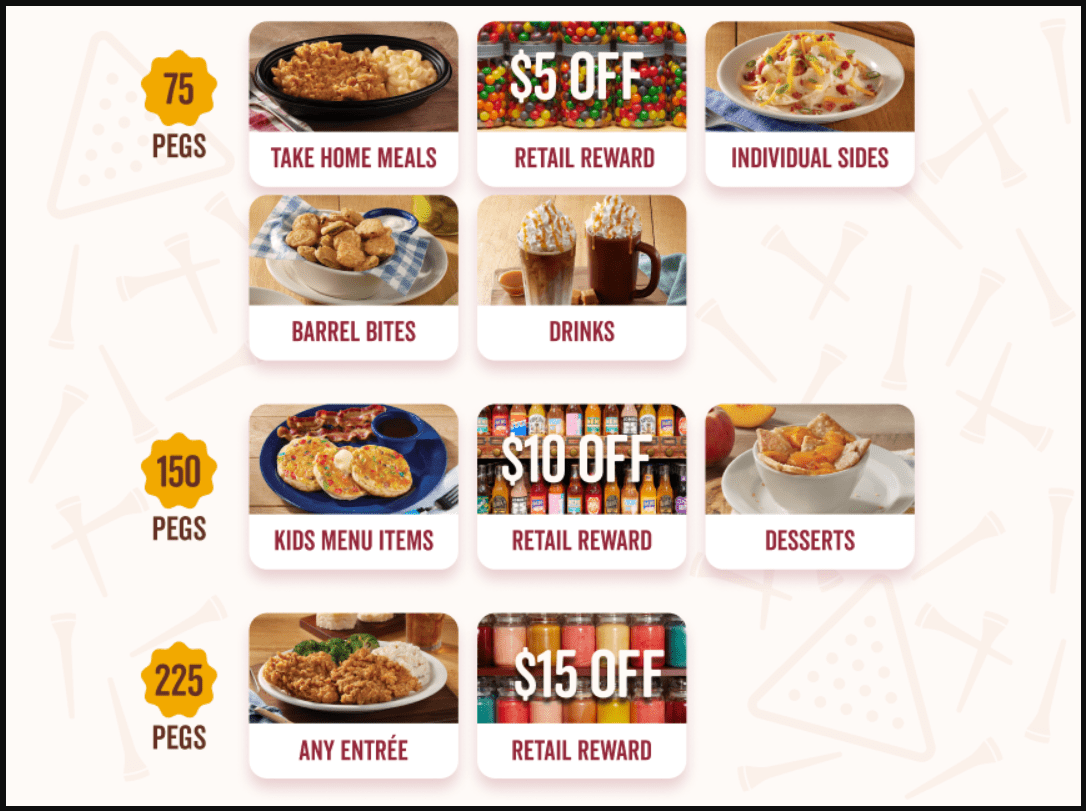

While the company is looking to boost traffic with a new Rewards Program that it believes "has the potential to be the best and most exciting in the industry", it is coming from behind with several other brands having a multi-year head start on their Rewards Programs. And while the program will award pegs ($1 per peg) for each dollar spent to redeem for meals, retail items, and appetizers/desserts that could help drive sales for its younger cohort, it's early to say whether this will resonate as much with its more value conscious 65+ cohort that may be getting priced out of casual dining a little after three years of above average menu price increases. Making matters worse, the environment has become more promotional, with Cracker Barrel's value proposition shining less when others are leaning into value as well to drive sales.

{kind=link}

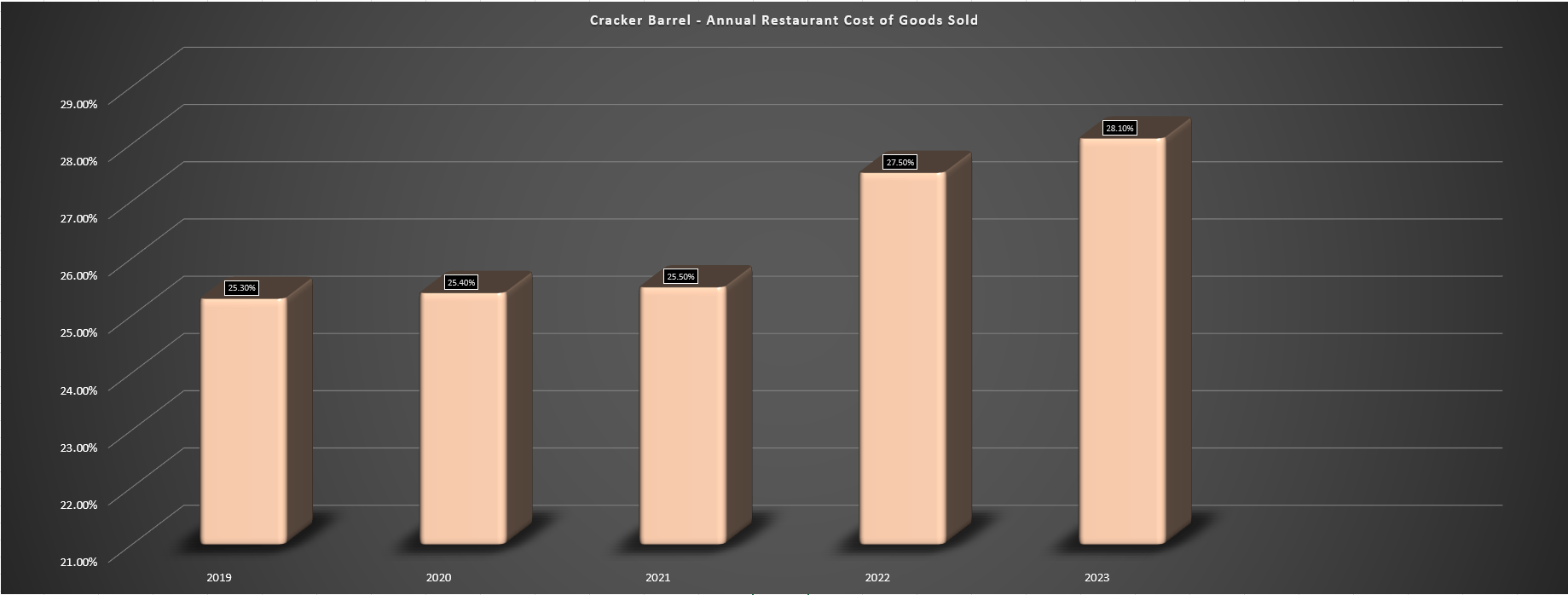

Finally, from a margin and earnings standpoint, there wasn't much to write home about either. This is because annual EPS sunk to $5.47 vs. $6.09 despite continued share repurchases due to higher interest expense, higher G&A, and higher impairment/store closing costs, while restaurant cost of goods sold increasing by 60 basis points to 28.1%, increasing for the fourth consecutive year in a row. And while the company was able to hold the line on labor on a full year basis, G&A was up as a percentage of sales, with operating income sinking yet again. Fortunately, Cracker Barrel was able to find $30 million in cost savings and push its catering business above $100 million for the year, and is confident it has more cost savings in the pipeline this year to help to claw back some margin losses. On a positive note, the company is guiding for commodity deflation which will help to offset the 4.5% wage inflation forecasted in the upcoming quarter.

Industry-Wide Trends

While calendar year 2023 has been a tough year from a traffic standpoint for most segments of the restaurant industry, things have not improved, at least according to OpenTable data which measures seated diners in the United States. In fact, as shown below, January saw strong traffic growth year-over-year after lapping Omicron, and there were brief spikes into double-digit positive territory in February and May, but since May, seated diner growth has struggled to even return to positive territory. Worse, we can see it decelerated through calendar year Q3, suggesting that the softness in early fiscal Q1 2024 that Cracker Barrel was experiencing doesn't seem to have improved. Given this softness, it looks like Cracker Barrel could struggle to deliver above its guidance midpoint of $825 million in fiscal Q1 2024, and this already implied a 2% from the ~$840 million reported last year.

{kind=link}

However, there are two things to be positive about in the upcoming year. For starters, Cracker Barrel has a new President & CEO in Julie Felss Masino that will begin next month, with experience at Yum! Brands ( YUM ) with Taco Bell (International President & North America), Starbucks China ( SBUX ) as Chief Marketing Officer, and VP Global Beverage and Global Merchandise at Starbucks. Finally, she also served as SVP, President & GM of Fisher Price at Mattel ( MAT ). This looks like a very solid appointment given the extensive restaurant and retail experience at major brands, and often new leadership is needed to spur a successful turnaround, and this could help to hammer out a bottom in the stock.

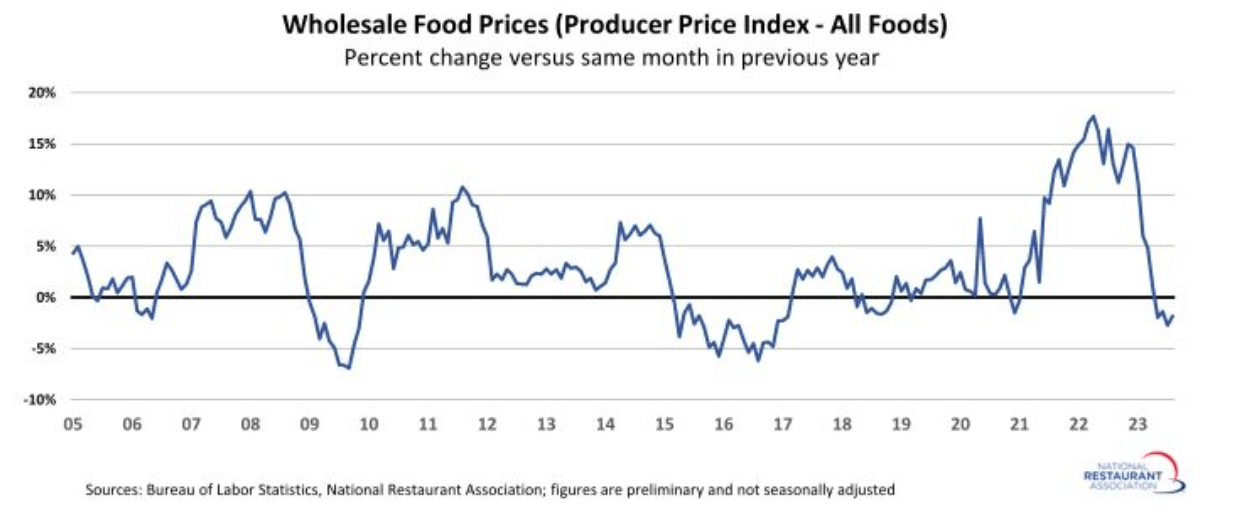

Wholesale Food Prices - National Restaurant Association, BLS

{kind=link}

The second positive development is that although the industry is getting little help from a labor cost standpoint (albeit turnover is at least improving), the restaurant industry has seen a significant improvement in commodity prices which have dipped into negative territory on a year-over-year basis. This is a huge improvement from the double-digit commodity inflation that put a dent in margins last year, and several brands are forecasting low single-digit commodity inflation or commodity deflation in the back half of CY23. So, while Cracker Barrel has seen a steady rise in cost of goods sold for its restaurant business, this minor tailwind coupled with continued work on cost savings should help to stabilize after what's been a tough few years of margin softness. Let's see whether this is priced into the stock yet:

Cracker Barrel - Annual Restaurant COGS - Company Filings, Author's Chart

{kind=link}

Valuation

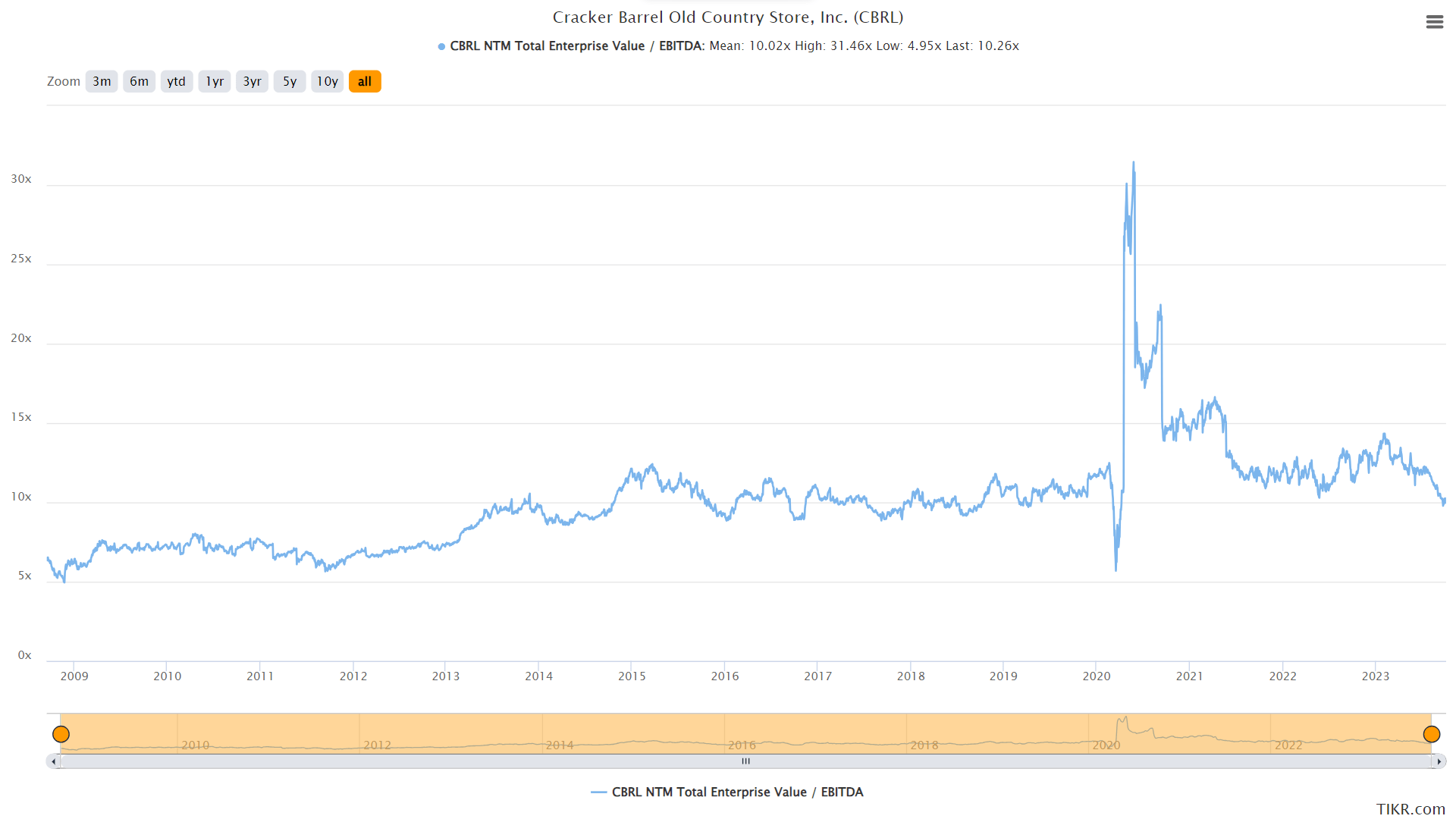

Based on ~22.2 million shares and a share price of $68.00, Cracker Barrel trades at a market cap of ~$1.51 billion and an enterprise value of ~$2.65 billion. This is a significant departure from Cracker Barrel's peak market cap of ~$4.4 billion in 2018, and the relative performance compared to peers has been extremely disappointing even when accounting for the industry-leading dividend yield. Unfortunately, although the stock is down over 55% from its highs, it's hard to argue for the stock being significantly undervalued. This is because even after this violent decline, it's still trading at ~17.5x FY2024 free cash flow estimates on an enterprise value basis, and over 10.0x EV/EBITDA. And while these aren't expensive metrics by any means, I wouldn't consider them as overly attractive for a low-growth that's seeing consistent margin compression, and one that's struggled to maintain earnings power despite aggressive buybacks.

{kind=link}

Worse, while the company has plowed significant capital into buybacks over the past two years to soften the decline in annual earnings per share [EPS], the price at which this capital has been deployed has been less than optimal, with ~350,000 shares repurchased near its highs in FY2021, another ~1.25 million shares repurchased at ~$105.00, and ~171,800 ounces shares repurchased above $101.00 per share last year. And while this has helped to shrink the float by neatly 10%, the company could have done a much more impactful job of retiring shares if it were more patient and waited for a near double-digit free cash flow yield to put money to work. Obviously, this might seem like arguing from the benefit of hindsight, but I think in the current environment, being more judicious with buybacks would have made more sense.

So, what's a fair value for the stock?

Using what I believe to be a more conservative multiple of 10.5x EV/EBITDA estimates of ~$260 million in FY2024, I see a fair value for Cracker Barrel of ~$1.63 billion after subtracting out net debt. This translates to a fair value of $74.10 when dividing by ~22 million shares, suggesting that Cracker Barrel is still not all that undervalued under more conservative assumptions despite its sharp decline. Obviously, some investors may disagree with this assumption and argue that fair value sits much higher. However, for a low-growth restaurant chain in the current market environment (~4.6% risk-free rate), I think this multiple might actually be generous, shown by the stock's long-term chart with its average multiple coming in just over 10.0x.

Measuring from a current share price of $68.00, this points to a 9% upside from current levels or a ~16% total return when including its industry-leading dividend yield of ~7.6%. However, I think it's difficult to entirely rule out a dividend cut when the company is paying out over 90% to shareholders based on FY2024 estimates. Besides, I am looking for a minimum 25% discount to fair value for small-cap stocks to ensure a margin of safety, and after applying this discount, CBRL's ideal buy zone comes in at $55.50 or lower. So, although the reward/risk for the stock has certainly improved following its ~55% correction, I still don't see an adequate margin of safety at current levels, and it's hard to rule out a final leg down in the stock over the next 12 months.

Summary

Cracker Barrel has been one of the worst-performing restaurant stocks over the past two years and while it has got more interesting from a technical standpoint as it nears major support in the $51.00 to $56.00 region, I still don't see enough of a margin of safety at current levels. And with much higher-growth names (~5% unit growth and high single-digit comp sales growth) trading at more attractive free cash flow yields like Aritzia ( ATZAF ), I continue to see more attractive bets elsewhere in the market. That said, the reward/risk setup is finally improving for CBRL with it being more hated, so I would consider the stock from a swing-trading standpoint if we were to see a pullback below $57.00 before December.

For further details see:

Cracker Barrel: Valuation Improving After The Drop