TRIN - Crescent Capital: Joining The Ranks Of High Yield BDCs In My Income Compounder Portfolio

2023-09-14 11:17:46 ET

Summary

- I discuss the importance of balancing risk and return in an investment portfolio.

- I share my personal investment strategy of focusing on income generation for retirement.

- I recommend Crescent Capital BDC as a potential investment due to its attractive dividend yield and strong management.

While composing my thoughts for this article I was intrigued by a recent article, Latest Memo From Howard Marks: Fewer Losers, Or More Winners? , that landed in my Inbox. In that memo, he asks the question whether it is better to have More Winners, or Fewer Losers in your portfolio? Obviously, the best answer is both. But that is not a realistic outcome for most investors who tend to take either too much risk (thus resulting in too many losers - or "learners" as I like to call them because I always learn something), or not enough risk, resulting in too little in risk-adjusted returns. He summarizes his thoughts with this paragraph:

If alpha is the ability to earn return without taking fully commensurate risk, investors possessing it can do so by either reducing risk while giving up less return or by increasing potential return with a less-than-commensurate increase in risk.

If you have followed my writing over the years, you will recognize that I am willing to take on more risk in my investments than the "average" investor. In fact, when I first got started with Seeking Alpha in 2016, I called my IRA holdings my No Guts, No Glory portfolio.

Over the years my investing strategy and my goals for investing have evolved. I am now much less concerned with growing my overall portfolio value and more interested in growing my future income stream to support my retirement years. I now refer to my IRA holdings as my Income Compounder portfolio. I did an update on my IC portfolio earlier this year, and it continues to evolve as I have now retired and have rolled over some additional funds from my employer retirement account. I am also now receiving a pension as an additional source of income.

My need for income from my investments remains a future need and because I have additional sources of income - pension, income from my writing, and eventually Social Security, I am still adding to my Income Compounder portfolio, which I have modeled after Steven Bavaria's Income Factory approach. As my investing strategy has evolved from Growth to Income, he does a good job of explaining why you do not necessarily need to pick more "winners" in order to grow your total return when you invest for income (bold emphasis is mine, highlighting the approach that I am taking).

There are lots of ways for investors to earn that long-term 9-10% equity return that most of us seek. We can do it through growth stocks that generate little cash income but produce capital gains sufficient to meet our target. We can take a middle-of-the-road approach and invest in unexciting but predictable blue-chip dividend-payers that split the difference between cash dividends and modest (but hopefully steady) growth. Or we can utilize an even higher yield strategy where we "create our own growth" over time through reinvesting and compounding, without having to worry much about growth and market volatility.

While some readers may see the term high yield and think that automatically equals high risk, other more astute investors may understand that is not always the case. However, the level of risk that one is willing to take will also determine the degree to which those returns produce the alpha that investor is seeking, as described in the Howard Marks memo. In my case, I like dividend paying securities such as BDCs (Business Development Companies) that yield 10% or more annually and offer some potential capital gains to boot.

Overview of Crescent Capital

One recent addition to my portfolio that meets my investment criteria is Crescent Capital BDC, Inc. (CCAP). There are many publicly traded BDCs (about 50 according to the BDC Universe on CEFData.com) to choose from. I already own several others and have recently written about Trinity Capital (TRIN) and CION Investment (CION).

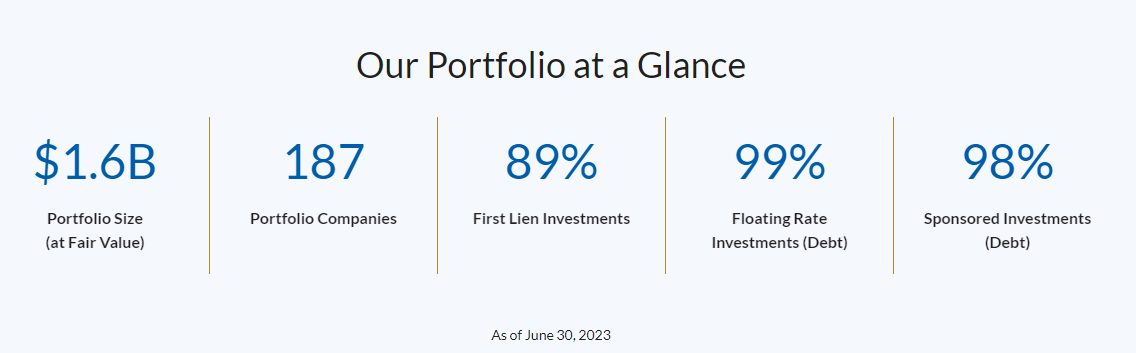

Like TRIN and CION, CCAP is relatively new to the publicly traded world of BDCs. CCAP started in 2015, then went public in February 2020 and is externally managed by Crescent Capital Group, a subsidiary of SLC Management (part of SunLife, who acquired a majority interest in Crescent in 2021). Crescent had over $39 billion in assets under management as of September 30, 2022. CCAP is structured as a BDC that lends to private, middle market companies in the US. From the company website, the portfolio summary shows a portfolio value of about $1.6B as of 6/30/23.

{kind=link}

The company completed the merger with First Eagle Capital BDC (formerly FRDC) in March of this year, resulting in the combined portfolio size of $1.6B.

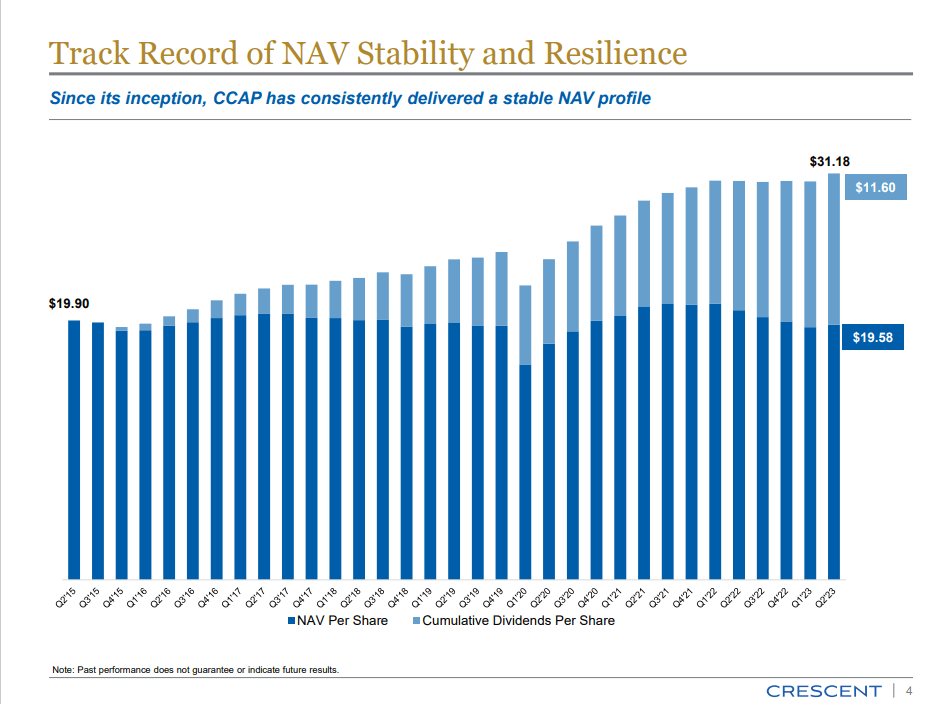

CCAP uses a relatively conservative investment strategy with nearly 90% in first lien loans, about 2.2% at cost in non-accruals as of June 30 (down from 2.7% in Q1), and with a debt-to-equity ratio of about 1.19x as of the end of Q2. The company has a good track record of NAV stability while paying out a cumulative $11.60 in dividends as shown in this slide from the Q2 2023 investor presentation.

{kind=link}

Q2 Earnings Summary

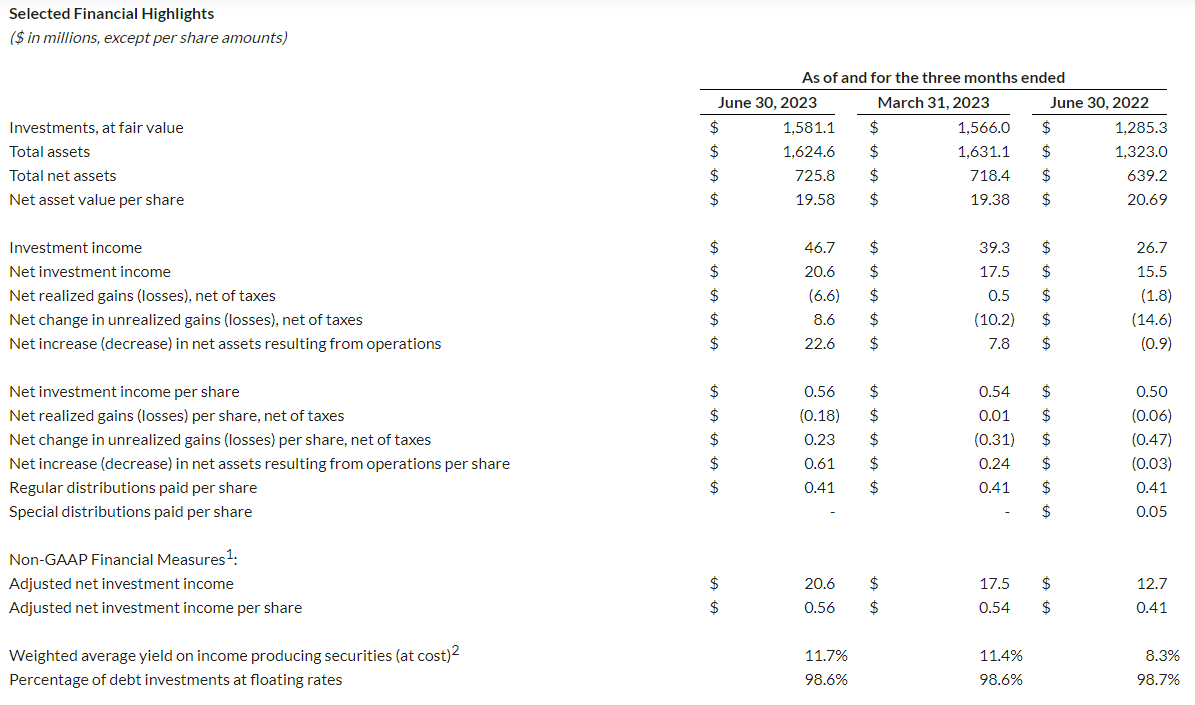

On August 9, 2023, the company reported Q2 earnings for the quarter ending June 30. The NAV reported as of quarter end was $19.58 (as indicated in the chart above) and NII was $20.6 million, or $0.56 per share. The Board declared a regular cash dividend of $0.41 to be paid on October 16 for shareholders on record as of September 29, 2023. In addition, the Board declared a supplemental dividend of $0.08 per share to be paid on September 15 with a record date of August 31. In the earnings report, the company also had this to say about future supplemental dividends:

Going forward, in addition to a quarterly base dividend of $0.41 per share, the Company's Board expects to also declare, when applicable, a formula-based quarterly supplemental dividend in an amount to be determined each quarter.

Considering that the NII for the quarter easily covered the base dividend plus supplemental with spillover income to spare, it would not surprise me at all to see another $0.08 supplemental dividend declared in Q3 when they report results in November. At the current market price of $16.34, the base dividend plus supplemental (assuming the same amount is paid each quarter going forward) works out to a forward annual yield of about 12%.

In addition, the company balance sheet remains strong with $21.5 million in cash at quarter end with $314.5 million in undrawn capacity on its credit facilities.

Financial highlights from the company earnings report are shown in the table below and include a QoQ increase in the weighted average yield on income producing securities from 11.4% in Q1 to 11.7% in Q2 in addition to the increase in NAV and NII.

{kind=link}

Management is Shareholder Friendly

As some commenters have noted , the management of CCAP has demonstrated that they are both competent and shareholder friendly. On the Q2 earnings call , company President/CEO Jason Breaux made note of the first "inaugural" supplemental dividend and discussed plans for future supplementals:

For the second quarter, we're pleased to declare an inaugural supplemental dividend of $0.08 per share, payable on September 15. As detailed on Slide 7 of our earnings presentation, it is calculated as 50% of net investment income in excess of our regular $0.41 per share dividend, subject to a measurement test. CCAP's NII per share has been comfortably outpacing the base dividend for some time, which we have seen accelerate in recent quarters as higher underlying reference rates have resulted in higher portfolio yields, given our 99% floating rate portfolio.

Like other BDCs that I follow, the high percentage of floating rate loans in the portfolio has benefited immensely from the Fed's increasing interest rates and CCAP appears to be well-positioned to continue to benefit from rising rates for at least the remainder of 2023, and perhaps well into 2024 based on current indications including August CPI coming in hotter than expected.

Comparison to Peers

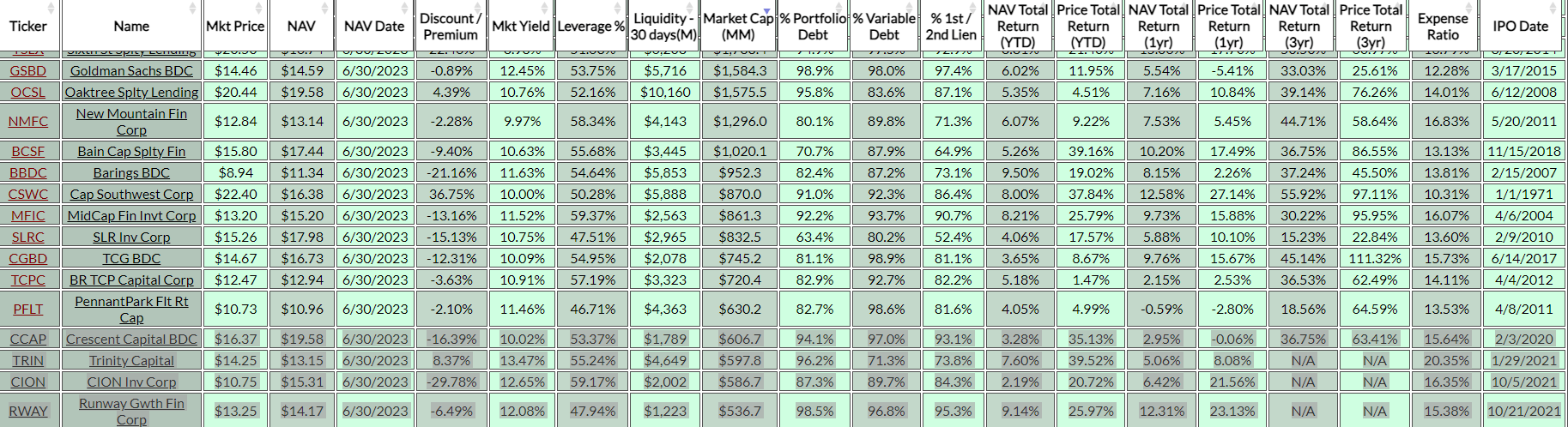

Earlier in the introduction I mentioned that there are several other BDCs that I follow including TRIN, which just announced yet another increase to its dividend, and CION. Another one that I just added to my IC portfolio is Runway Growth Finance Corp. (RWAY). In the BDC Universe I sorted the companies by market cap and all four of these appeared together with market caps between $500M and $600M as shown in the snippet below.

{kind=link}

All four BDCs are relatively new to public trading (CCAP being the "oldest" of the four), yield around 10-12% annually (or more in the case of TRIN), trade at a discount or small premium to NAV, and have performed quite well looking at YTD Total Return based on Price with 20% to nearly 40% returns. I am not here to predict which of the four is the best because as I indicated in the introduction, I don't have to pick the winner. I just need to try to minimize the losers in my portfolio. At this point in the economic cycle, I believe that all four are poised to outperform over the next year or two assuming that we do not suddenly endure a substantial market correction or end up in a recession in 2024.

Risks to my Thesis

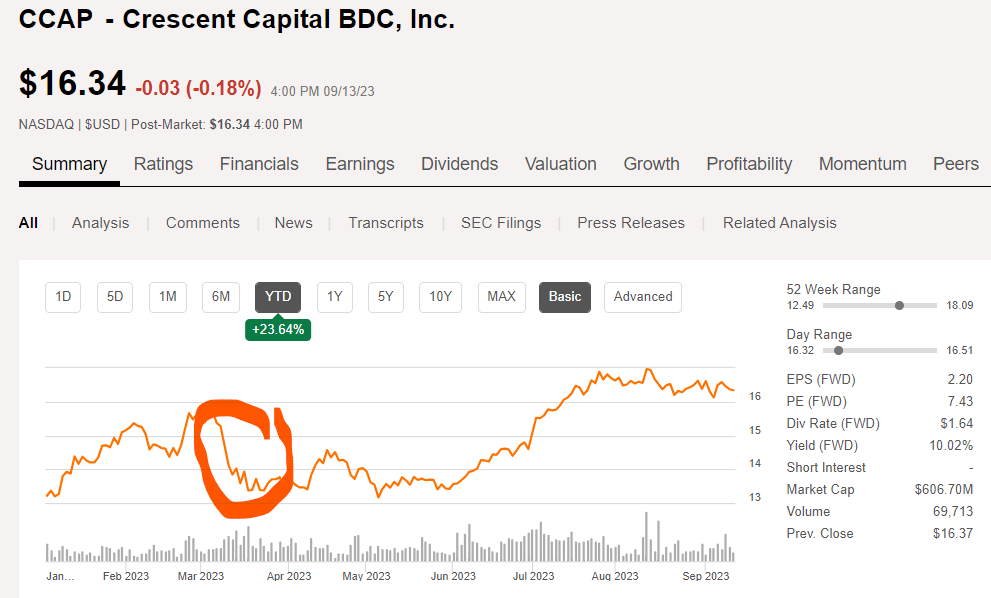

While CCAP has seen a relatively stable NAV over the last several years (including before going public) and non-accruals remain at a low 2% of total portfolio value, there is the risk that the US economy could suddenly nose-dive into recession as some still predict . The end of student loan forgiveness, additional quantitative tightening by the Fed, ongoing geopolitical conflicts, and climate disasters may cause a shift in the market sentiment and send stock prices crashing. Back in March when the SVB bank failure happened and other banks started to show cracks, many BDCs were hammered, and stock prices cratered. The BDCs were fine, but sentiment shifted, and all financial stocks were treated like they were disasters waiting to happen. That impact on the share price can be seen in the chart for CCAP, which also coincided with the completion of the merger with FRDC.

{kind=link}

Also, most market participants now expect the Fed to hold rates steady when they meet next week on September 20. In fact, some believe that the Fed rate hike cycle has already ended. If the Fed decides instead to increase rates again, that could have the effect of causing a market correction, in which case there could be a buying opportunity for CCAP. At the current market price, with the significant discount to CCAP book value of -16% there is some price protection built in. But if market sentiment shifts to the negative side and we do see a market correction, there is always the possibility that the market price for CCAP could drop lower.

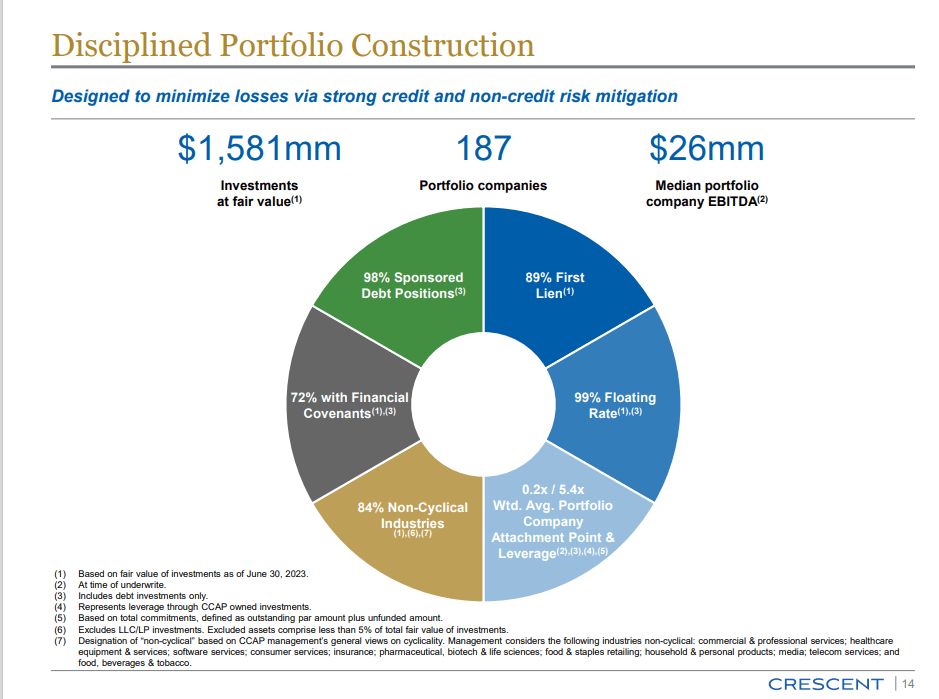

In the company Q2 earnings presentation , they include a slide to illustrate the defensive nature of the portfolio construction. It is designed to minimize losses via strong credit positions and using non-credit risk mitigation measures. This may help in the event of a downturn in the economy.

{kind=link}

Summary and Recommendation

As I alluded to in the introduction to this coverage of CCAP, I have recently received an influx of cash from a rollover of my retirement plan upon retiring last month. I have been looking for new investments to acquire using some of that cash and especially those that pay a generous dividend yield exceeding 10%, or 12% in the case of CCAP when counting the supplemental dividends. I also own several other BDCs including the other 3 mentioned in this article - CION, TRIN, and RWAY. I also own Ares Capital (ARCC), FS KKR Capital (FSK), and Capital Southwest Corp. (CSWC).

The rising interest rate environment has been good for well managed BDCs and the results so far in 2023 speak to the success of CCAP management. They have demonstrated that they are shareholder friendly and are doing a good job of managing credit risk while offering an attractive income with the expectation of future supplemental dividends in upcoming quarters. CCAP may not be "the winner" but I expect it to be a winning investment in my Income Compounder portfolio and I rate it a Buy at the current price.

For further details see:

Crescent Capital: Joining The Ranks Of High Yield BDCs In My Income Compounder Portfolio