CA - Crescent Point Is About To Become The Second Largest Montney Producer

2023-11-14 12:42:34 ET

Summary

- Crescent Point Energy announces $2.55 billion acquisition of Hammerhead Energy.

- Crescent Point reports bolstering their high-quality Montney assets with estimated FY24 production of 94mboe/d.

- The acquisition will increase Crescent Point's production by 23% and total proved and probable reserves by 25%.

All figures are in CAD unless otherwise stated.

Crescent Point Energy ( CPG ) recently announced its intentions to acquire Hammerhead Energy ( HHRS ) in a deal valued at $2.55b. This announcement doesn’t come as a surprise given the massive amount of consolidation occurring in the industry. With forward estimates of 2.07x – 2.29x EV/EBITDA based on management’s production estimates of 200-204mboe/d, I assign CPG and HHRS BUY ratings with a price target for CPG of $11.46/share. Because HHRS shares will trace the value of CPG until conversion, I don’t believe it to be prudent to provide a price target given that the total value of the deal has been announced.

This article will primarily focus on Crescent Point and the business combination. Please read my analysis on Hammerhead Energy here .

Crescent Point Operations and Financial Analysis

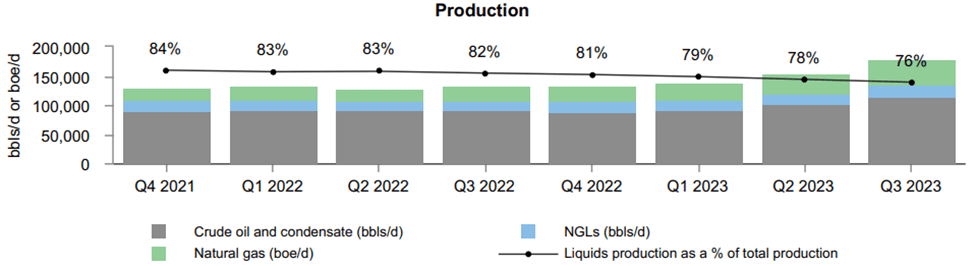

Crescent Point reported a significant improvement in operations in Q3’23 and has now surpassed their guidance from FY22 with daily production reaching 180mboe/d. This improvement is the result of their Montney asset acquisition and further development in their Kaybob Duvernay assets. Overall, the firm invested $315.5mm and drilled 52 wells during Q3’23. Operations were challenged given the -6% y/y decline in condensate prices and -37% in NGL pricing for the quarter due to higher storage volumes in Western Canada. Pricing was offset by higher volumes produced.

Throughout the last two years, Crescent Point has spent significant sums in acquiring assets in the Kaybob Duvernay region. These assets are comprised of a $900mm acquisition from Shell in 2021 and a $370mm acquisition from Paramount resources in January 2023. The firm acquired their Montney assets on May 10, 2023, for $1.7b and will further bolster these assets at the close of the Hammerhead Energy acquisition. Development CAPEX for the first nine months of 2023 equated to $859.8mm for development of their Kaybob Duvernay assets with a total of 128 gross wells drilled. The firm anticipated to spend $1.05-1.15b in CAPEX for FY23, leaving $190-290mm for Q4’23. Total capital investment between developments and acquisitions for the first nine months of 2023 has totaled $2,993mm.

On the flipside, Crescent Point has been focusing on displacing non-core assets, such as those in North Dakota. As of Q3’23, Crescent Point has completely exited the US market for producing assets and is focusing their attention on their Canadian assets. This resulted in a significant operating loss as a result of deferred tax expense of $249mm and impairment charges of $773mm, resulting in a net loss of -809.9mm. Adjusting for all non-operating charges, the firm netted $315mm with adjusted fund flows from operations reaching $687mm for Q3’23.

For Q3’23, 76% of their production was crude oil and liquids with the remainder in natural gas. Across their Montney assets, Gold Creek West produces 58% liquids, Gold Creek East 57% liquids, and Karr 79% liquids.

{kind=link}

Pre-Hammerhead acquisition, this region is expected to produce 38mble/d in 2024. Hammerhead is expected to bring 56mble/d of production to the Montney assets for a pro forma daily production of 94mboe/d with an aggregate of 50% liquids and oil.

Corporate Reports

Total pro forma production across all assets is expected to grow to 204mboe/d and 260mboe/d by FY24 and FY28, respectively. Bear in mind the 180mboe/d seen in Q3’23 includes 30mboe/d from their discontinued North Dakota assets and should pull back to 150mboe/d.

{kind=link}

Debt

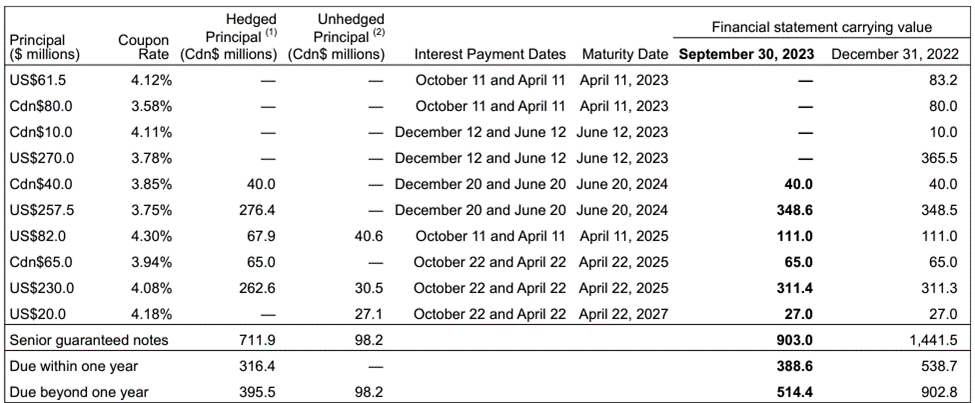

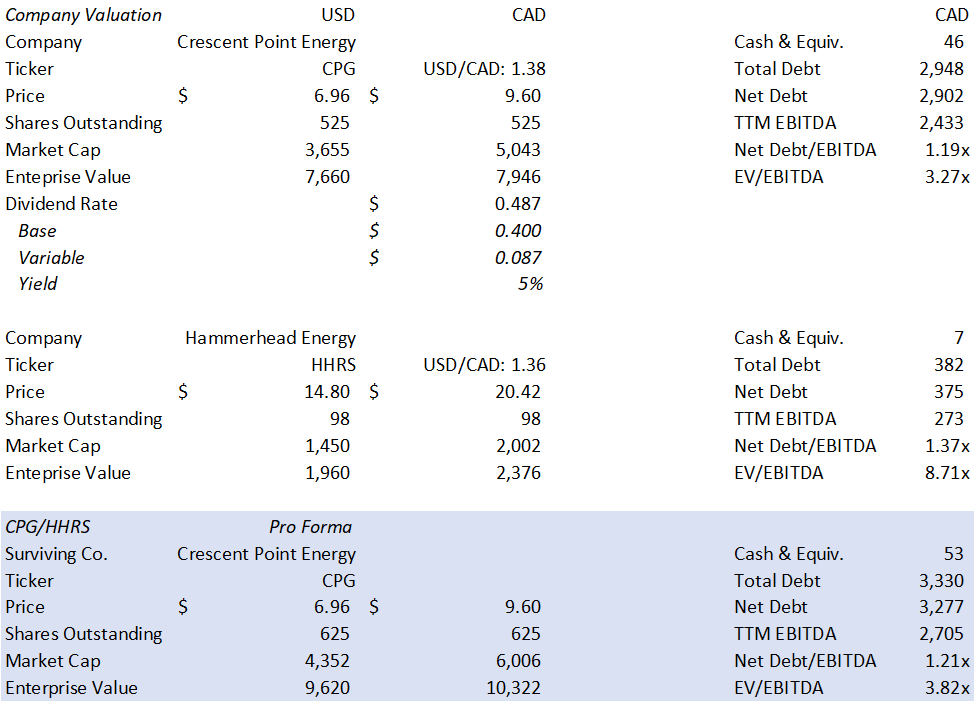

Total debt currently sits at $2,948mm with $46mm in cash on the balance sheet. The firm reduced their net debt load by $124.5mm to $2,902mm. Leverage isn’t necessarily a concern given their low 1.19x Net Debt/EBITDA ratio; however, they may run into some minor challenges given the structure of their debt. As of Q3’23, 30% of Crescent Point’s debt was fixed-rate debt with the remainder floating. Much of this is the result of heavy utilization of their credit facility with $2.08b of the $2.76b drawn with $25.9mm in outstanding letters of credit. The firm also has US$903mm in senior guaranteed notes outstanding with $388.6mm due within one year of Q3’23.

{kind=link}

Crescent Point does hedge a portion of their debt book against forex risks, covering a notional amount of $606.9mm across interest and principal.

Looking ahead to FY24, management increased their expected capital investment from $1.05-1.15b to $1.45-1.55b with the addition of Hammerhead’s assets. 80% of the 2024 capital budget will be to develop their assets in Montney and Kaybob Duvernay with the remaining 20% allocated to their long-cycled assets in Saskatchewan. Their revised production is expected to achieve 200-208mboe/d on the back of this capital investment and is expecting to generate $1-1.2b in free cash flow. The firm also anticipates utilizing 40% of their free cash flow to reduce their net debt. With these target figures and assuming the Hammerhead acquisition is successful, net debt should look closer to $2,797-2,877mm for a net debt/EBITDA ratio of 0.66x-0.74x, assuming all 40% of the allocated excess cash flow goes to net debt improvement.

{kind=link}

Highlights of the transaction

The total offering comes out to $2.55b, including $455mm in assumed debt. This values HHRS at 3.4x earnings Crescent Point announced on November 10, 2023, that they successfully raised the $500mm in their equity issuance with 48,550,000 shares sold at a price of $10.30. In addition to this capital raise, $548mm of the offer will be in equity to HHRS shareholders with the remaining $2b in cash.

{kind=link}

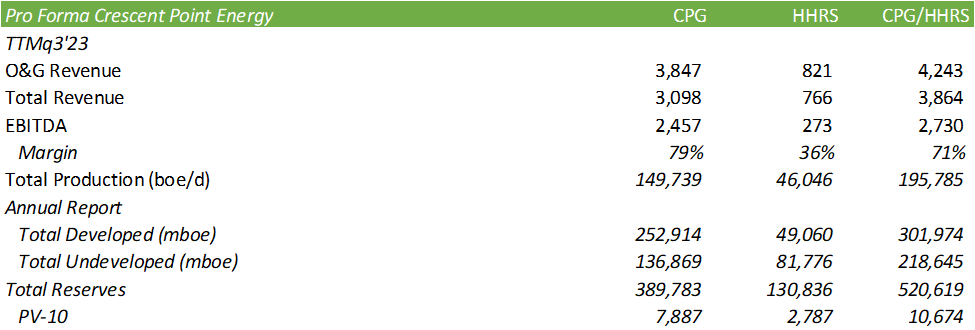

Running the figures, the acquisition isn’t necessarily operationally accretive in the sense of margin expansion; however, the primary purpose of the acquisition is to bolster Crescent Point’s Montney assets. Using trailing figures from Q3’23 for financials and FY22 figures for reserves and PV-10 analysis, we can create a baseline picture of the business combination. Do note, I removed US assets from Crescent Point’s figures given their sale of the North Dakota Assets and have not re-established figures for the duration of the year.

{kind=link}

Overall, the acquisition will increase Crescent Point’s production by 23% and their total proved and probable reserves by 25%.

Shareholder Value

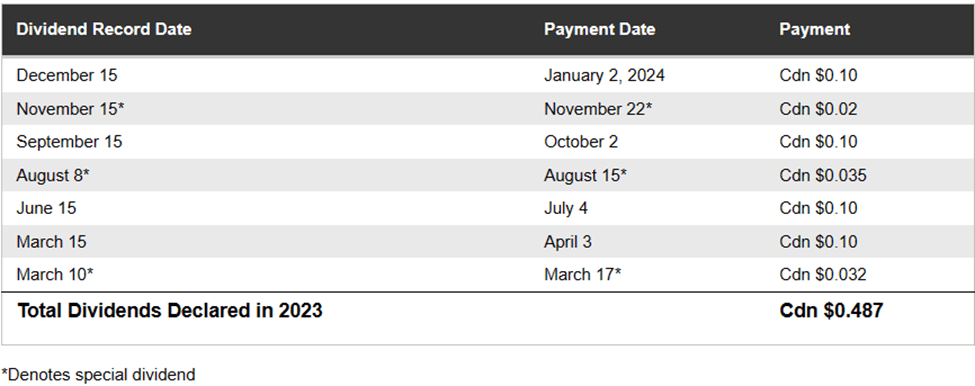

Crescent Point offers a robust shareholder return policy in which 60% of free cash flow is allocated to dividends and share buybacks. As management anticipates earning $1-1.2b in free cash flow in FY24, $600-720mm is anticipated to enhance shareholder returns. The firm’s trailing dividend yield sits at 4% (converted to USD) for a payout of CAD$0.487/share.

{kind=link}

On a valuation basis, CPG shares are expected to trade at a slightly higher premium post-close at 3.82x TTM EV/EBITDA compared to their present valuation of 3.27x. On a forward basis using my assumptions as listed out below, we can expect forward figures to look closer to 2.07x – 2.29x. Given that dilution is already baked into these figures, I provide both CPG and HHRS a BUY recommendation with a price target for CPG shares of $11.46/share. As HHRS shares will trace CPG shares upon conversion, I will not provide a price target for HHRS shares as the total valuation of the deal is known.

{kind=link}

For further details see:

Crescent Point Is About To Become The Second Largest Montney Producer