CRSP - Crispr Therapeutics Is Overvalued (Rating Downgrade)

2024-01-02 00:58:59 ET

Summary

- Casgevy's FDA approval is a key advance in gene editing for SCD, yet it faces high costs and a limited market due to specialized treatment needs.

- Casgevy's complex treatment, including stem cell processes, necessitates costly, specialized centers, limiting patient access.

- Intense competition from bluebird bio’s Lyfgenia and concerns over Casgevy’s safety, efficacy, and cost-effectiveness affect market penetration.

- Recommend "sell" due to operational hurdles, competitive pressures, overvaluation, and uncertain long-term prospects despite scientific progress.

At a Glance

Casgevy's recent FDA nod marks a pivotal moment in gene-editing treatments, advancing my earlier insights on CRISPR Therapeutics ( CRSP ). Notably, CRISPR's stock has climbed in 2023, following speculation about Casgevy's FDA review. Operational and financial hurdles, however, loom large. Priced at a hefty $2.2 million, Casgevy's affordability and widespread application come into question. Establishing necessary centers for its administration is costly, limiting its reach, especially to a specific group—those 12 and older suffering from severe Sickle Cell Disease [SCD]. Potential long-term safety and efficacy concerns add to these barriers. The market's skepticism is evident in TD Cowen's downgraded rating, echoing concerns about competition, particularly from bluebird bio's ( BLUE ) Lyfgenia. Despite these obstacles, CRISPR's financial stability, underpinned by robust cash reserves and controlled expenses, offers some solace. Yet, investor sentiment is mixed: institutional interest is high, but insider sales and fluctuating growth forecasts paint a complex picture. This context sets the stage for a detailed examination, hinting at a cautious investment approach amidst a backdrop of high market expectations and tangible operational roadblocks.

Sickle Cell Breakthrough Meets Market Reality: The Casgevy Conundrum

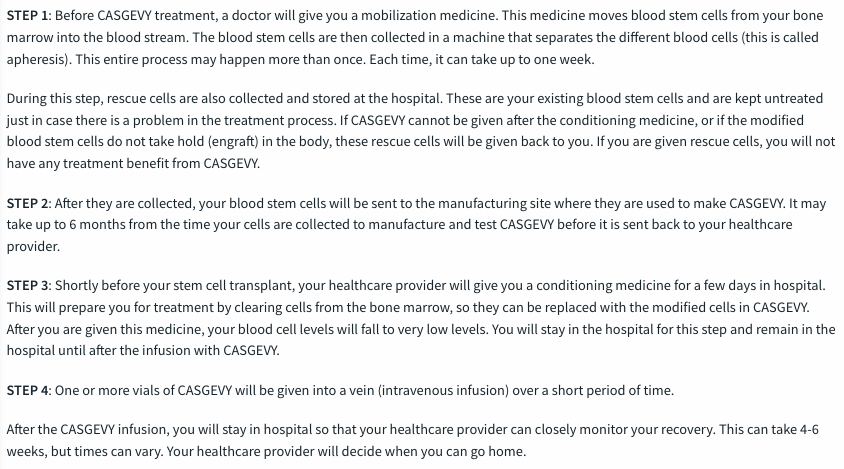

Casgevy's approval for SCD marks a significant advance in gene-editing therapies, but its path in 2024 looks to be tempered by a series of complex and costly challenges. The need for specialized treatment centers is a major bottleneck. CRISPR's partner, Vertex ( VRTX ), plans to establish around 50 such centers in the U.S. , a process hampered by the significant time and resources required for setup and staff training. The complexity of Casgevy's treatment process, which involves multiple stages including stem cell mobilization, modification, and transplantation, demands specialized medical infrastructure and extends the overall treatment duration, limiting patient turnover.

{kind=link}

Furthermore, Casgevy's approval for patients aged 12 and older with severe SCD narrows its immediate market scope. Financially, the therapy’s steep $2.2 million price raises questions about its cost-effectiveness and insurance coverage, especially in comparison to existing, more affordable SCD treatments. Dr. Lin recently wrote about this in a blog post.

Although the lifetime medical costs associated with sickle cell disease average $1.7 million , insurance companies may be unwilling to pay the exceptionally high up-front cost of this curative therapy. Compared with standard of care, one analysis found gene therapy to be an equitable strategy for U.S. patients per distributional cost-effectiveness analysis standards. Obstacles in addition to cost include needing to undergo chemotherapy and being hospitalized for months until the patient’s immune system recovers.

Safety and long-term efficacy concerns, particularly regarding potential off-target genetic effects, may also lead to cautious adoption among healthcare providers and patients. Moreover, the therapy’s global accessibility is limited. In regions like sub-Saharan Africa, where SCD is highly prevalent, the focus remains on more accessible treatments, highlighting a stark disparity in healthcare resource allocation.

TD Cowen's recent downgrading of CRISPR's stock to underperform, largely driven by what they deem an "irrational" valuation and apprehensions surrounding the launch of Casgevy for sickle cell disease, resonates with the broader challenges I highlighted. The investment bank's skepticism hinges on the expected market penetration of Casgevy. Despite CRISPR's projection of 16,000 eligible patients, TD Cowen anticipates a significantly lower real-world uptake, owing to competition from bluebird bio’s Lyfgenia and inherent treatment challenges.

TD Cowen’s analysis points out that currently, only about 100 patients per year opt for allogeneic transplants, a number limited due to concerns about side effects—a concern they believe extends to both Casgevy and Lyfgenia. They estimate an increase to 200–300 patients per year seeking such treatments, with Casgevy likely capturing around 60% of this market and Lyfgenia the remaining 40%. This projection casts doubt on the widespread adoption of Casgevy, suggesting more niche market penetration than initially anticipated.

The bank's view that the current high valuation of CRISPR is partly fueled by an aggressive short squeeze further underscores their stance on the stock’s overvaluation. With a price target set at $30, TD Cowen’s perspective aligns with the notion that while Casgevy is a significant scientific advancement, its practical market impact and financial return might not meet the high expectations currently set by the market.

Aside from CRISPR's SCD and transfusion-dependent thalassemia [TDT] treatments, additional CRISPR gene therapy approvals do not appear to be on the horizon anytime soon, as elucidated in a recent Seeking Alpha report .

{kind=link}

Despite its much larger valuation, CRISPR appears to be in a very similar boat to bluebird bio, which has authorized gene therapies for TDT, SCD, and cerebral adrenoleukodystrophy.

CRISPR, undoubtably, warrants a higher valuation than bluebird. CRISPR is flush with cash, while bluebird's stock is witnessing significant dilution as the company faces liquidity constraints amidst high costs. However, given the magnitude of ongoing net losses and the poor market prospects for both firms, a compelling case can be made that CRISPR is on the verge of a similar financial scenario to bluebird, and their valuations are likely to close the gap to some extent.

Q3 Performance

Analyzing CRISPR's latest earnings , the period ending September 30 brought significant changes. Their revenue hit zero in 2023 due to no income from collaborations and grants. Yet, their operating expenses dropped notably, from $182.5 million to $132.4 million, showcasing effortful cost control. The net loss saw a slight improvement, decreasing from $174.5 million to $112.2 million. This hints at ongoing financial challenges. Interestingly, share dilution was minimal. The count of average common shares rose marginally from 78 million to 79.4 million, reflecting a prudent financing strategy that avoided excessive equity dilution.

Financial Health

Shifting focus to their balance sheet , CRISPR's 'cash and equivalents' ($527.8 million) plus 'marketable securities' ($1,212.1 million) total around $1,739.9 million. Their current liabilities, including various expenses and liabilities, sum up to $111.2 million. The current ratio stands at about 15.6, indicating a solid position to cover short-term debts.

Over the past nine months, CRISPR used $164.3 million in operating activities, averaging a monthly burn rate of about $18.3 million. Calculating their cash runway by dividing liquid assets by this monthly rate, we find they can sustain themselves for at least seven years. However, these are past figures and may not fully predict future trends.

Considering their lengthy cash runway and current fiscal standing, it seems unlikely that CRISPR will need more financing soon. They appear financially robust in both short and long terms, thanks to their substantial liquid assets and controlled cash burn.

Market Sentiment

According to Seeking Alpha data, CRSP's market capitalization of $4.97 billion, coupled with high short interest (22.11%) and a substantial 69.26% institutional ownership, presents a complex picture. The high market cap suggests market confidence, yet the significant short interest indicates skepticism about future performance. Growth prospects are volatile: a dramatic sales increase projected for FY 2023 (+26,722.43%) contrasts sharply with a forecasted decline in 2024 (-51.65%). This inconsistency may raise concerns about the sustainability of growth. Stock momentum, outperforming SPY significantly over the past year (+55.22% vs. +23.91%), shows robust market enthusiasm, at least in the short term.

Institutional ownership reveals active management, with 760,903 new positions and 644,402 sold-out positions, indicating a dynamic investment environment. Notable institutions like Ark Investment Management and Capital International Investors adjusting their holdings reflect this active management.

Insider activity , with a net of 148,991 shares sold over the past year, might be perceived as a lack of confidence by insiders in the company's near-term prospects.

Overall, the company's market sentiment appears "adequate," reflecting a mix of optimism in stock momentum and institutional interest against concerns over inconsistent growth prospects and insider selling.

My Analysis and Recommendation

Casgevy's FDA nod for SCD is indeed a landmark for CRISPR. Yet, the stock's surge of 55% in 2023 seems overdone. This does not align with the firm's future challenges. Investors might think about a "Sell" view for a few reasons.

First, Casgevy faces tough operational challenges. These include the need for special centers and complex administration. This will likely slow its market entry and sales. Also, its high cost and limited insurance coverage pose issues for broad use and affordability. Importantly, it is still unknown how safe and effective gene therapies like Casgevy will be in the long run.

Next, competition, notably bluebird bio's Lyfgenia, threatens Casgevy's market position. Lower patient uptake than predicted further weakens its sales forecast.

For investors aiming to profit from a share price fall in 2024, short-selling or put options might be smart moves. Yet, these strategies are risky. They need thorough market analysis and timing. To cut risks, consider stop-loss orders or diversify your investments to lessen the impact of CRISPR's stock swings.

Risks to my "Sell" argument include unexpected good news about Casgevy's use and effectiveness. This could boost investor trust and lift the stock price. Also, advances in CRISPR's other gene therapy projects or new partnerships could improve its financials. Remember, the biotech field is volatile and unpredictable. Changes in market mood and stock values can happen quickly, regardless of company fundamentals.

To sum up, while Casgevy's approval is a scientific breakthrough, its real-world hurdles, competitive risks, and CRISPR's current stock overvaluation call for caution. Investors should watch the changing scene and brace for possible downs and surprise gains in this shifting sector.

For further details see:

Crispr Therapeutics Is Overvalued (Rating Downgrade)