TMUS - Crown Castle Deserves An Upgrade Ahead Of Earnings

2023-10-10 11:32:06 ET

Summary

- Crown Castle's stock has dropped 32.6% year to date and 5.4% in the past month, presenting a buying opportunity.

- Analysts are forecasting a 2.1% decline in revenue for the third quarter, but historically, the company has shown revenue growth.

- Profit per share is expected to decline from $0.97 to $0.83, and other profitability metrics should be closely monitored.

- Despite these issues, the company looks attractive and should be seriously considered.

Later this month, the management team at telecommunications infrastructure giant Crown Castle ( CCI ) is expected to announce financial results covering the third quarter of its 2023 fiscal year. Leading up to that time, it seems as though investors are not terribly optimistic about what the future holds. Due in part to the fact that analysts are forecasting revenue and profits to decrease year over year, the stock to fall on hard times, dropping 32.6% year to date. And in the past month alone, it's down 5.4%. While this is painful for existing investors, it does represent a remarkable buying opportunity for investors. And with the prospect of even stronger economic data down the road, and given how cheap the stock now appears to be, I've decided to increase my rating on the business from a ‘buy’ to a "strong buy."

Keep a look out for headline news

After the market closes on Oct. 18, the management team at Crown Castle will announce financial results covering the third quarter of the company's 2023 fiscal year. Leading up to that time, there are some important financial metrics that analysts should be paying attention to. At the top of the list, literally, will be the revenue reported by management. At present, analysts are forecasting sales of $1.71 billion. If this comes to fruition, it would actually represent a decline of 2.1% compared to the $1.75 billion the company generated at the same time last year.

{kind=link}

To those who follow the company closely, a drop in sales may seem unrealistic. Historically, management has done a great job of growing the firm's top line. In each of the past three fiscal years, revenue has risen compared to the year prior. And so far this year, financial performance is looking up. During the second quarter of 2023, for instance, revenue came in at $1.87 billion. That's 7.7% above the $1.73 billion generated one year earlier. And for the first half of this year, revenue of $3.64 billion was 4.7% above what was generated the same time of 2022.

{kind=link}

To be perfectly truthful with you, I'm very skeptical of a sales decline. But this does not mean that such a decline cannot occur. In July of this year, for instance, management did initiate a restructuring plan that, amongst other things, discontinued the company's installation services for the Towers business that it operates. We don't know how large of an impact this might have on revenue. But we do know that it will cause restructuring and related charges of roughly $120 million between the third and fourth quarters of this year. Even so, there's some hope of growth during this time. Very probably, Towers site rental revenue will drop modestly because it did increase by only $8 million in the first half of this year compared to the same time last year, climbing from $2.15 billion to $2.16 billion. The real growth, however, will come from the Fiber site rental revenue. In the first half of this year, it totaled $1.19 billion. That's 20.3% above the $990 million generated the same time last year.

On the bottom line, the picture should be different. Because of the aforementioned restructuring activities, analysts believe that earnings this quarter will also be lower year over year. The current expectation is for the company to generate profits per share of $0.83. This would represent a decline from the $0.97 per share reported one year earlier. If this comes to fruition, it would translate to net profits falling from $418 million last year to $360 million the same time this year. Management has not provided guidance when it comes to other profitability metrics. But investors would be wise to keep a close eye out on them. For context, operating cash flow in the third quarter of last year was $701 million. If we adjust for changes in working capital, we get $897 million. FFO, or funds from operations, ended up being $838 million, while the adjusted figure for it was $804 million. And finally, EBITDA for the company totaled $1.08 billion. Once again, for the first half of this year, and for the most recent quarter, almost all of these metrics were higher than the same time last year. So this would represent a departure from recent historical results.

Guidance will be interesting

Generally speaking, companies in this space are known for stable and reliable financial results. It's rare to see material changes in guidance for the current fiscal year. And even when we do see such changes, they tend to be small. As an example, we need to only look at guidance as provided by management during its second quarter earnings release. In the second quarter earnings release, management said that site rental revenue would come in between $6.488 billion and $6.533 billion. That still matches guidance that was provided for the year when management reported financial results for 2022.

{kind=link}

On the other hand, during the second quarter earnings release, management did revise down guidance for key profitability metrics. These revisions can be seen in the table above. In short, we're looking at differences of between $35 million and $65 million relative to what prior guidance called for. Restructuring activities, combined with higher interest expense caused by a mixture of higher net debt and higher interest rates, will almost certainly account for the vast majority, or perhaps even all of, this reduction in bottom line guidance.

Look at leverage and cancellations

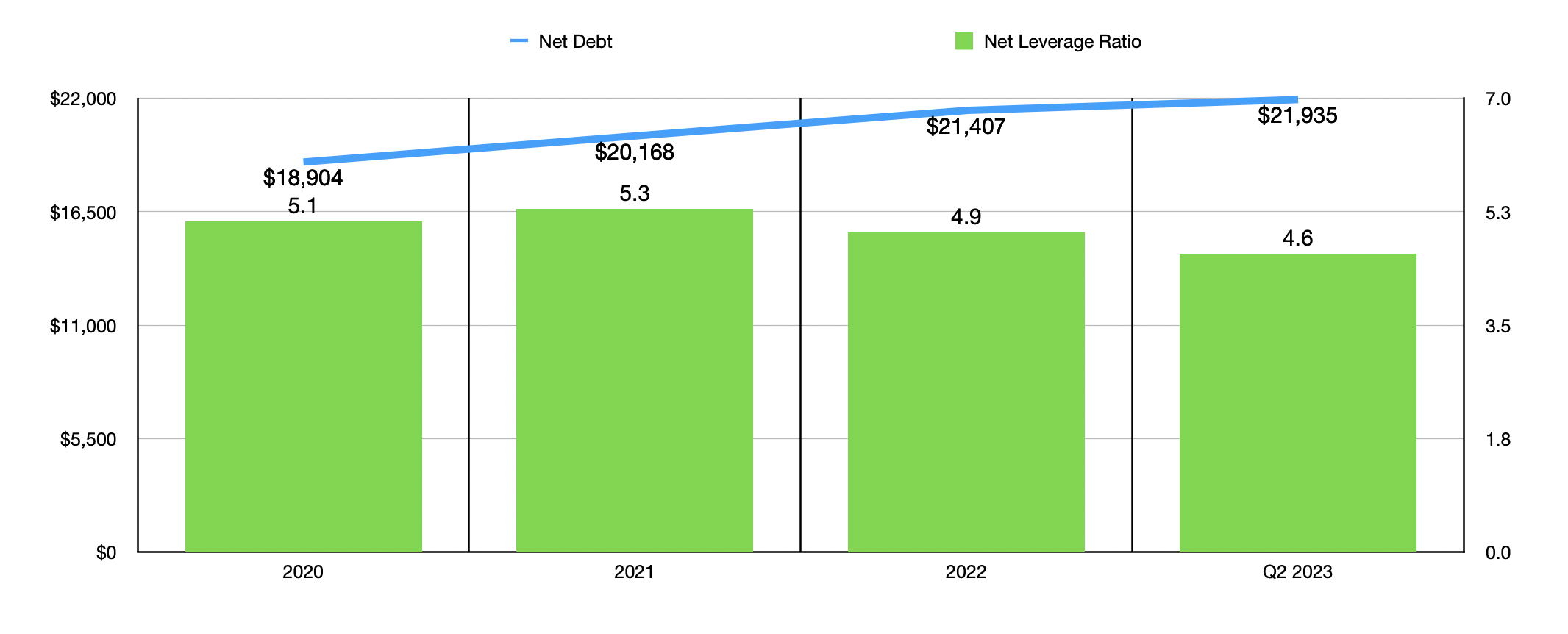

The fact of the matter is that the telecommunications space is very much asset intensive. If you need a proof of this, you need only look at the $21.94 billion in net debt that the company has on its books. This is up from the $18.90 billion the company had at the end of 2020. Even though net debt has increased, net leverage has fallen because of increased profitability. In 2020, the net leverage ratio was 5.1. This ticked up to 5.3 in 2021 before falling to 4.9 in 2022. On a trailing 12-month basis, as of the end of the second quarter, this had fallen further to 4.6. None of these numbers would I consider to be too high for the company. But the lower that net debt is, the more de-risked the company is and the greater its cash flows should be. This is even more true given the high interest rate environment that we are dealing with. This is because $2.74 billion of the debt on the company's books is currently variable in nature. And the vast majority of this does not come to you until 2027.

{kind=link}

One thing that has worried investors about Crown Castle and the space in general is the merger between T-Mobile ( TMUS ) and Sprint. Including the towers that are leased out to Sprint, 53% of the company's towers are leased, subleased, or operated and managed under contracts with T-Mobile and AT&T ( T ) combined. Any major merger such as the one between T-Mobile and Sprint is bound to see some degree of asset consolidation. And part of what has been included in financial guidance for this year for Crown Castle is revenue associated with cancellation payments involving the Sprint network. During the first six months of this year, for instance, it recognized site rental revenue of $154 million associated with these cancellations. And for the year as a whole, it's expected to receive payments of between $160 million and $170 million associated with cancellations. In the long run, as the image below illustrates, it's unlikely that this merger will have any materially negative impact on the company. But some investors are worried that industry consolidation could lead to pricing pressures on telecommunication asset owners.

{kind=link}

Takeaway

Leading and earnings, I believe that analysts are overly bearish when it comes to Crown Castle. It's possible that revenue and profits, particularly the latter, will show some weakness because of the aforementioned items I discussed. But on the whole, the company looks to be incredibly solid and is likely to continue growing nicely in the long run. When I last wrote about the company, shares were quite cheap. And since then, the stock has gotten even cheaper, with shares falling by 10% while the S&P 500 has dropped 2%. Given these changes, and the extreme pessimism of market participants, I believe that now is a great time to upgrade the company from a "buy" to a "strong buy."

For further details see:

Crown Castle Deserves An Upgrade Ahead Of Earnings