TMUS - Crown Castle's Improved Valuation Makes It Attractive

2023-05-31 04:49:34 ET

Summary

- Crown Castle is on the cusp of a Sprint-related earnings growth trough.

- This churn will be a one-time event while tower fundamentals remain in secular growth.

- With the now cheap market price, I view CCI favorably.

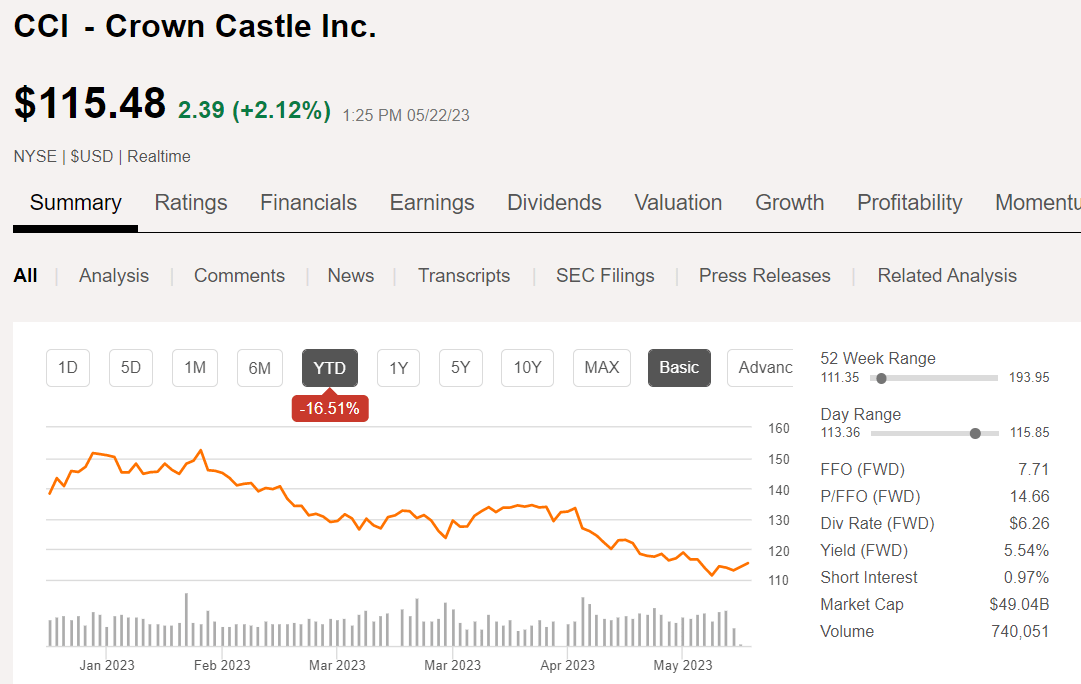

Crown Castle ( CCI ) has gotten extremely cheap relative to its history as the stock price dropped by 35%. Given the size of the company this magnitude of price move does not happen from a few errant trades in the way that it often does with microcap and small cap REITs. The roughly 1/3 drop represents an approximately $25 billion decrease in market value resulting from wide spread institutional selling. This warrants investigation and a fresh analysis on the prospects of CCI at its new reduced price. Specifically, we dig into the following:

- Real headwind: Sprint churn

- Small cell viability and proliferation

- Small cell profitability with regard to sharing

- Fiber as an independent asset class

- Fiber as it fits into the tower model

- Overall forward growth

- Valuation relative to history

- Valuation relative to peer tower REITs

- Valuation relative to growth prospects

But first, let me open with a conjecture as to why CCI's price has fallen so far.

DISH worse than Sprint

When T-Mobile ( TMUS ) bought Sprint it was initially considered neutral to the tower REITs. Sell side analysts thought it was neutral and market prices didn't respond in a clear direction. The basic idea was that there would be a full offset.

So as you know, towers use a shared infrastructure model in which the same macro tower is leased to multiple different operators. This allowed TMUS, AT&T ( T ), Verizon ( VZ ), and Sprint to all have coverage over the location with just a single macro tower. It is much more efficient than each of the 4 carriers building their own tower and much of that efficiency was captured by the tower REITs in the form of exceedingly high margins.

Each tower could have each of the 4 main carriers on it which functionally made its rent 4X.

Well, when TMUS bought Sprint, the combined entity would no longer need equipment for both TMUS and Sprint on the tower so it was known that as Sprint leases expired they would not be renewed in locations where TMUS was a common tenant. In many cases this takes rent on shared macro towers from 4X to 3X.

Clearly that aspect of the merger is a bad thing for tower REITs. As part of allowing the merger to go through, however, the FCC required that a 4th entity come in such that there would still be 4 major carriers. Their goal behind the ruling was to ensure a certain level of competition so as to keep prices low for consumers. The side effect of this goal is that the tower REITs would get a 4th tenant thus restoring their rent to 4X.

A tower REIT doesn't really care if its 4th largest tenant is Sprint of DISH Network (DISH). It merely cares that there is a 4th tenant.

Thus, the market saw the FCC ruling demanding there be a 4th tenant and the Sprint churn to be fully offsetting which made the merger roughly neutral to the tower REITs.

In practice, however, the merger has quite clearly been a negative for the tower sector, at least so far. Sprint churn has been happening at the expected pace of leases rolling off while DISH has been exceedingly slow to lease up the towers. While DISH is obligated by the FCC to build out its network, they are dragging their heels on the pace of buildout, I suspect for 2 reasons:

- DISH is not in great financial shape.

- DISH doesn't really have material revenue associated with its network.

Do you know anybody with a DISH connected cell phone? I sure don't.

The slow DISH lease-up has affected all the tower REITs more or less equally while the Sprint churn has been quite unequal.

On 1/11/23 I alerted subscribers of Portfolio Income Solutions that I thought American Tower (AMT) would outperform CCI due largely to CCI's heavy Sprint churn in 2025. In contrast, AMT has had much more even churn spread out over about a decade with much of the churn already in AMT's FFO numbers.

CCI had previously been floating as if it was somehow immune to Sprint churn but eventually the market figured out that it is just happening all at once and the stock dropped rather sharply in 2023.

{kind=link}

The Sprint churn is now evident in CCI's forward consensus estimates. Notice how both FFO/share and AFFO/share are expected to decline through 2025 which is the time period in which the bulk of the Sprint leases are expiring.

{kind=link}

I feel fairly confident in this being the primary impetus for the selloff in CCI.

What I will now explore is whether the selloff went too far and perhaps CCI is a great value now.

Small Cells

Small cells used to be synonymous with 5G, but that is no longer a real distinction because macro towers are also fully capable of 5G. In fact, most of the 5G network buildout so far is on macro towers.

Smalls cells serve as a supplement to macro towers with 2 main functions:

- Increase capacity

- Cover dark spots caused by tall buildings or other obstacles blocking macro tower coverage

In more rural or even medium density areas a macro tower can usually fully handle the demand for data in terms of capacity. This may change over time as data usage continues to rise, but for now, small cells are overwhelmingly used for dense population areas with particularly high data demand. The data demand can become so high that it overwhelms the macro tower even if the macro tower has full coverage over the area.

The small cells built within the radius of the macro tower can handle the majority of the data volume within their smaller radii which alleviates the burden of the macro tower making the connection more effective for the entire area.

The buildout of small cells is chugging along nicely. Crown Castle already has 120,000 small cells on air or under contract.

Challenges and opportunity

One of the nice aspects of small cells is that it doesn't require the footprint of a macro tower or the expensive infrastructure. They can be affixed to already existing public objects with CCI's favorite being on top of street lights. As such the potential sites for small cells are abundant with the main difficulty to building them being the cost of the equipment itself and getting local permissions.

I view the rather minimal infrastructure cost as a negative for CCI and the red tape as a positive for CCI.

The thing that makes towers such a lucrative business is the shared infrastructure in which the same site can be leased to 3 tenants without DISH or 4 tenants with DISH. Small cells can also be leased to multiple tenants but I don't think the REIT will have quite the same leasing power as they do with macro towers because the infrastructure cost just isn't that high.

It is quite burdensome for a carrier to have to build its own macro tower but substantially less burdensome to simply build their own small cell. Thus, I don't think small cells will be a 3X revenue or 4X revenues proposition by leasing to 3 or 4 tenants. I suspect it will be more like a 2X with each tenant paying about 60% of what it would have to pay for rent as a sole tenant. Still a great business model, just not the extraordinary success that macro towers have been for the past 20 years.

One potential aspect that could give shared infrastructure owners such as the tower REITs full negotiating power is the red tape. Local governance bodies are not going to want 4 separate small cells on the same street corner (one for each carrier). They would be much more likely to approve a single small cell owned by a neutral third party that is shared among the 4 carriers. If the red tape does indeed become a barrier to supply, small cells could mimic the macro tower's extreme success.

All the tower REITs will be deep in the small cell game over time. The primary differentiating factor for CCI is its fiber.

Fiber - an early disappointment but long term vertical integration advantage

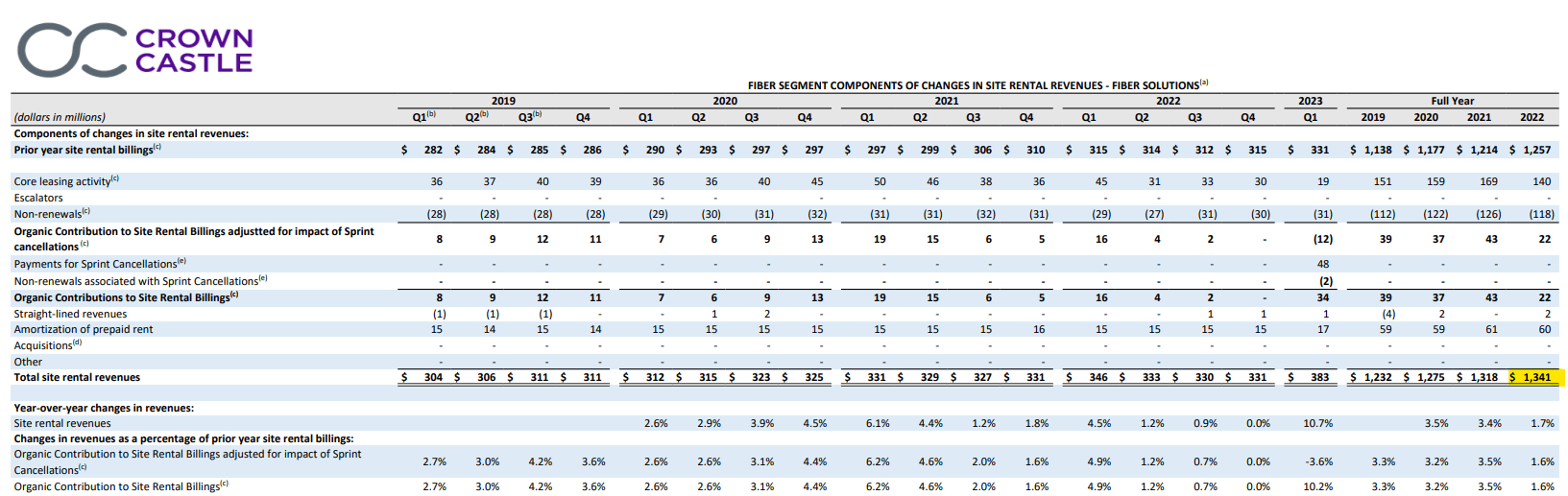

CCI would disagree with me on this, but so far fiber has been rather disappointing as a revenue driver for CCI. Considering the massive network CCI owns at 85,000 route miles of fiber, the fiber solutions revenue of $1.341B in 2022 strikes me as somewhat low.

{kind=link}

Fiber solutions is growing, but only at a pace of about 3% per year.

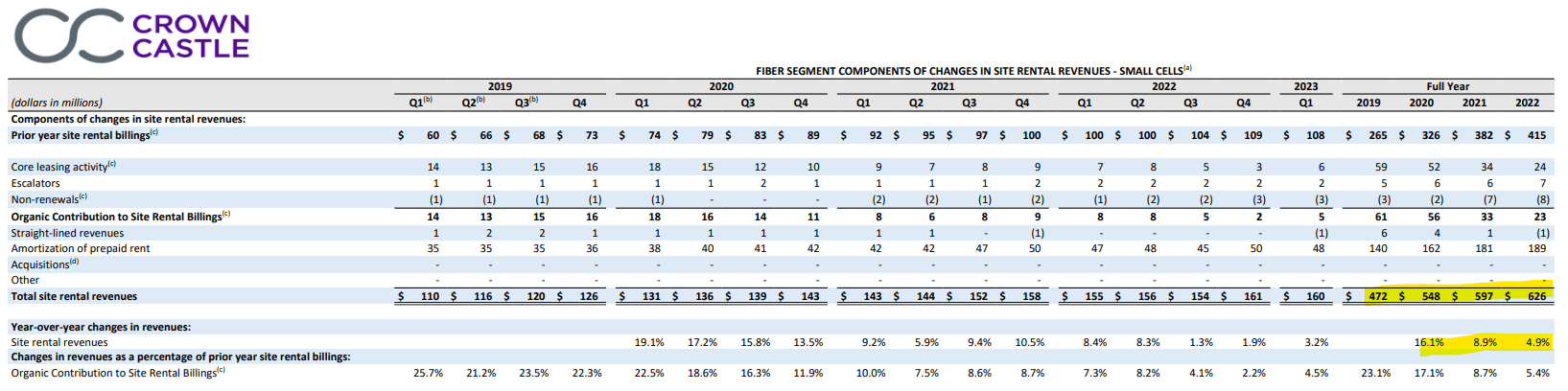

Small cell deployments are a relatively new thing and they could be the key to unlocking the valuable fiber assets. CCI's growth rate in fiber related to small cells is closer to 9% (smoothed over 3 years).

{kind=link}

Just as macro towers need direct fiber connections for backhaul, each small cell needs a fiber connection to the network. I see 3 key advantages to CCI via its fiber as small cells roll out.

- Increased margins via vertical integration

- Increased speed of deployment as it can just connect to its own fiber

- Leasing fiber to other small cell owners

Overall forward growth

According to analyst estimates 2026 FFO per share and AFFO per share look to be roughly the same as in 2023.

That is a grim outlook for a company that spent the past decade growing at a double digit annual pace. The market seems to have priced this in as a secular problem with the extreme 35% selloff.

I see it as more of a one time headwind in the form of Sprint churn. All the growth engines are still going. CCI is still growing at a roughly 10% annual pace. It just so happens that over the next few years they also have negative growth as the Sprint leases churn. So through 2026 the churn is netting out the positive growth.

The reason this distinction matters is that the churn is a finite factor. Once Sprint is at 0% of revenue the churn is done. In contrast, the growth drivers seem more secular in nature. Small cells are in the very early innings and 5G deployment will continue to lend itself to favorable rent rollups through amendments as tenants add equipment to existing macro towers.

It is more of a growth pause followed by a resumption of medium to fast growth.

Valuation

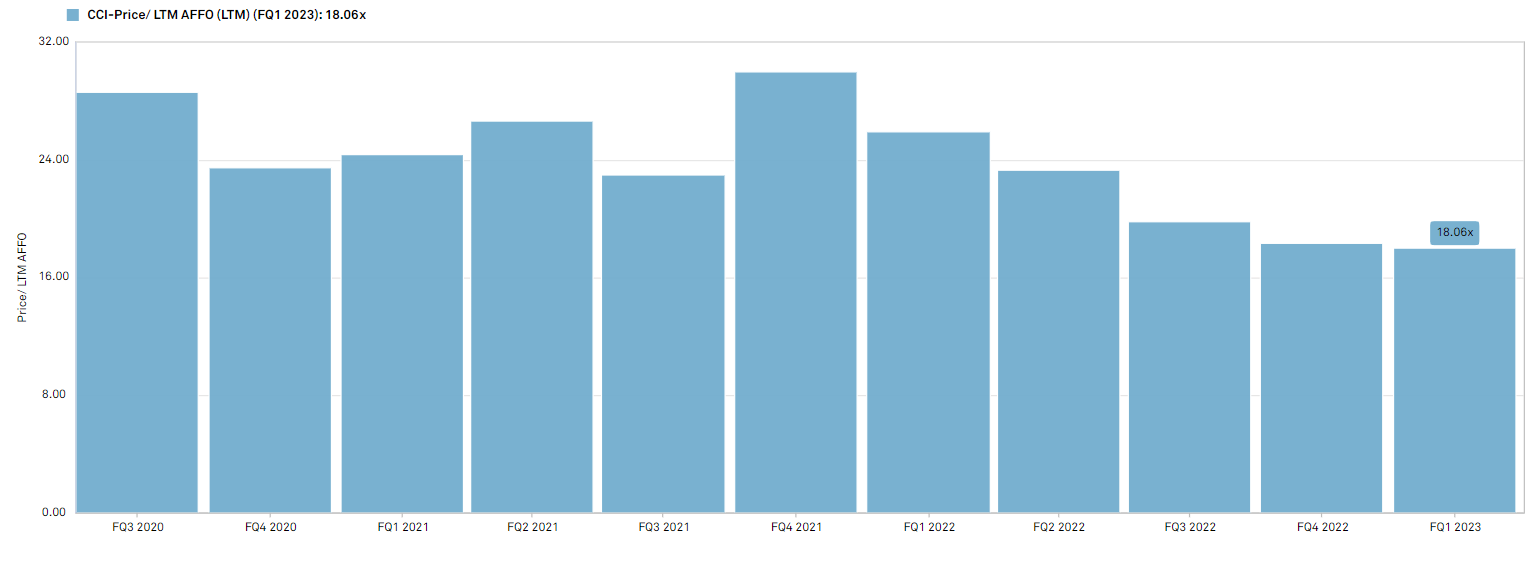

CCI is trading extremely cheaply relative to its own history.

It has often been in the mid 20s P/AFFO on a trailing basis. As of 3/31/23 it was at 18.06X.

{kind=link}

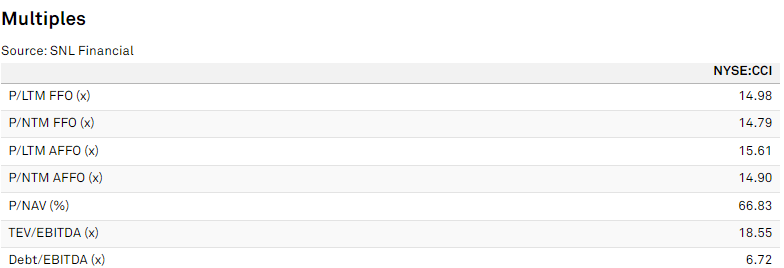

CCI has fallen in price even further since the quarterly data above, now sitting at 15.61X on a trailing AFFO basis and 14.9X on forward AFFO.

{kind=link}

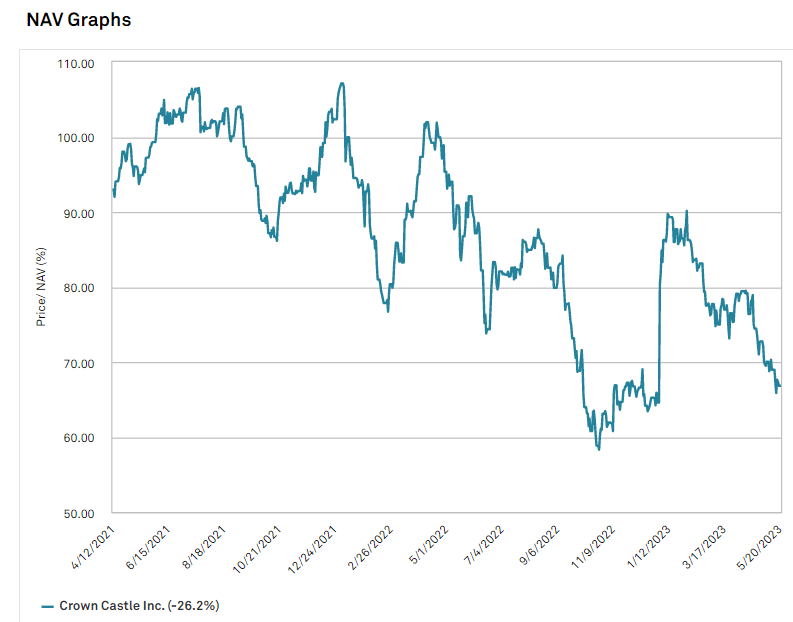

Also notable above is the 66.8% price to net asset value. CCI has historically traded right around 100% of NAV.

{kind=link}

Valuation relative to peers

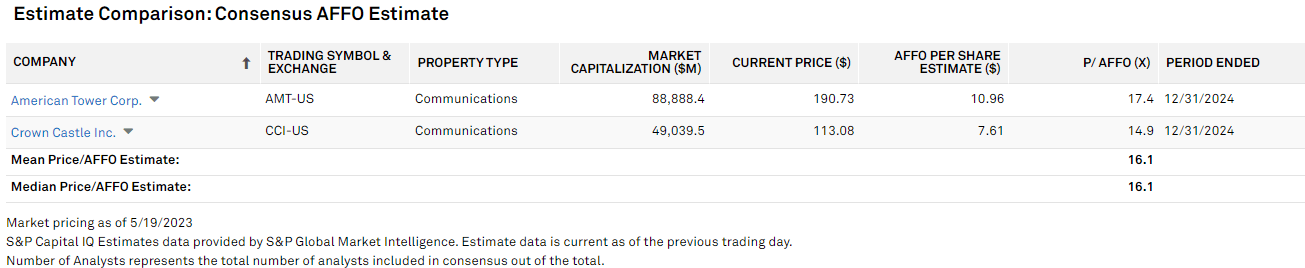

Back in my January article I preferred AMT's valuation as the multiples were rather close but AMT will have less Sprint churn going forward. Today, I think it is much more even as CCI is significantly cheaper at 14.9X 2024 AFFO compared to AMT at 17.4X.

{kind=link}

This gap in multiple should fully make up for the delta in forward Sprint churn.

Valuation relative to forward growth

Given today's interest rate environment, I would consider the following thresholds to be about right for a reliable company:

- 12X AFFO multiple for stable company but no growth

- 15X AFFO multiple for stable with slight growth

- 18X for moderate growth

- 25X for rapid growth

CCI is a bit tricky because it is presently a no growth company through roughly 2026, but beyond that I think it is moderate to rapid growth.

The market tends to be myopic in nature which is probably why it is assigning a 0 to low growth multiple to CCI to reflect the next couple years. However, as a long term holding I think CCI is starting to look quite attractive.

If we fast forward to 2025 when CCI's forward growth rate is more like 8% to 15% the multiple is likely to be much higher that it is today. Thus, even though there is minimal growth between now and then, I think there could be substantial multiple expansion. On top of that, CCI offers a juicy 5.5% dividend while we wait which makes for an ample total return proposition.

Risks to CCI

I cannot emphasize enough the value of the shared infrastructure model. It has made the tower REITs wildly successful. Shared infrastructure and therefore triple dipping on rental revenues is a proven concept in macro towers but not yet a known thing for small cell. The future growth rate of CCI will greatly depend on the extent to which small cells prove to be shared infrastructure. I would be extremely happy with 4 tenants being 3-4X revenues (like the macro towers) and satisfied even if it is merely 2X revenue.

The risk would be a future in which small cells are sufficiently replicable that the carriers can each build their own and not need shared infrastructure. My crystal ball can't see that far so I guess we will find out as time goes on.

For further details see:

Crown Castle's Improved Valuation Makes It Attractive